|

市场调查报告书

商品编码

1632080

亚太地区智慧卡:市场占有率分析、产业趋势与成长预测(2025-2030 年)Asia Pacific Smart Card - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

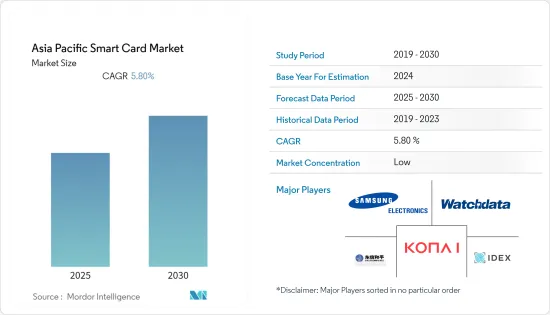

预计亚太地区智慧卡市场在预测期内的复合年增长率为 5.8%。

主要亮点

- 各种政府流程的数位化不断提高,以及获取政府服务所需的ID卡的需求不断增加,正在创造新的潜在市场机会。除此之外,透过提供医疗保健、许可、社会福利文件等,政府当局正在实施智慧卡,从而加速未来几年的市场成长。

- 高效储存资料、对非接触式和非现金付款偏好的改变以及付款流程数位化的趋势不断增长,正在推动医疗保健、零售和酒店业对智慧卡的需求。此外,透过区块链技术出现的新兴客户资讯安全技术以及智慧卡在亚太地区人口最多的国家的广泛采用预计将为智慧卡製造商提供利润丰厚的成长潜力。

- 此外,安全性和小型化是IC卡技术发展最快的两个领域。随着世界向更安全的 EMV 银行卡过渡,最新一代的智慧卡现在具有完整的片上加密功能,显着提高了整个产业的卡片安全性。此外,智慧卡正在被小型化为更多样化的外形尺寸,例如迷你标籤和智慧型穿戴装置。随着智慧卡越来越多地与电话和生物识别技术一起用作二因素凭证,这种趋势可能会持续下去。

- 此外,付款卡无疑是日常生活和商业的重要组成部分。根据智慧付款协会 (SPA) 的数据,实体店大约 90% 的非现金消费者付款是透过银行卡进行的。此外,根据 SPA 的数据,支付卡直接或间接促进了 40-60% 的线上付款。

- 自疫情爆发以来,触碰付款的需求增加,各行各业对智慧卡的接受度正在推动市场向前发展。此外,智慧卡在门禁和个人识别应用中的高渗透率、电子政府服务对智慧卡的需求不断增长以及网路购物和银行业务的需求不断增长,预计将在预测期内推动智慧卡市场的成长。

- 此外,由于全球消费者对非接触式付款方式的需求不断增加,因此 COVID-19 大流行预计将促进市场成长。部署电子销售点 (EPOS) 终端的高昂成本以及行动钱包和付款应用程式的持续使用预计将在未来几年限制智慧卡的需求。

亚太地区智能卡市场趋势

BFSI 产业在亚太地区智慧卡普及率中占据主要份额

- 在 BFSI 中使用智慧卡有几个优点,包括保护个人资料和安全交易。智慧卡在 BFSI 领域也用作信用卡、签帐金融卡、支付认证卡和存取控制卡。透过将资金装入智慧卡,它可以用作电子钱包,并可以使用加密通讯协定转移到自动贩卖机或帐户。

- 此外,随着技术的进步,诈欺操作的数量也在增加。因此,卡片和付款领域变得数位化,引入了 EMV 晶片、PIN 卡和行动电子钱包等新的付款方式。在 BFSI 领域,由于智慧卡上储存的资料难以破解,智慧卡变得越来越流行。

- 例如,2021年1月,总部位于新加坡的新兴企业StashFin与印度SBM银行合作,推出了一款储值卡。该合作伙伴关係旨在透过让银行帐户的个人更容易使用智慧卡获得信贷来缩小印度的信贷缺口。

- 随着各金融机构意识到这一趋势,生物辨识非接触式 IC 卡可能会在预测期内在 BFSI 产业中流行。此外,安全始终是重中之重,因为关键的财务业务是业务的核心。例如,IDEMIA正在利用生物辨识技术推动IC卡的发展。

- 同样,2021 年 2 月,ICICI 银行与 Greater Chennai Corporation 和 Chennai Smart City Limited 合作推出了「Namma Chennai 智慧卡」。这种RuPay联名非接触式储值卡将安装在GCC中心,以实现税金和公用事业收费等各种数位付款。该储值卡也可用于在清奈及全国各地的零售商店和电子商务网站付款。

中国主导亚太地区智慧卡成长

- 中国是最早废除支票并引入非接触式付款的国家之一,带动了亚洲数位卡的发展。该国已在包括交通在内的各个行业引入了智慧卡。随着中国政府控制行业并鼓励整合产业以提高在全球市场的竞争力,预计大中型企业将迅速整合。

- 此外,许多中国银行正在开发数位人民币硬钱包,中国人民银行已表示客户将能够在实体钱包和数位钱包中持有数位货币。中国人民银行(PBOC)扩大了中央银行数位货币(CBDC)试点范围,将非接触式「硬钱包」和NFC可穿戴设备纳入其中,允许客户使用数位人民币在商店和公共交通上购买商品。服务。

- 例如,中国建设银行在 2021 年 6 月表示,将试行生物识别「硬钱包」智慧卡,允许客户储存数位人民币,并使用指纹来验证使用央行数位货币的付款。先进的指纹辨识和身份验证用于保护卡上储存的价值。

- 此外,IDEX Biometrics ASA 于 2021 年 11 月宣布,中国银联已核准解决方案合作伙伴恆宝股份有限公司的最新生物辨识智慧卡认证 (CUP)。这款新卡采用IDEX Biometrics的感测器和生物辨识软体解决方案,已通过中国银行卡检测中心(BCTC)的所有要求。此智慧付款卡可实现多用途应用、安全的全球付款以及存取控制和个人识别等附加功能。

亚太地区智慧卡产业概况

亚太地区智慧卡市场竞争激烈,多家全球和地区公司都在争取市场占有率。儘管该市场进入门槛较高,但少数新参与企业取得了成功。此市场的特点是产品中/高度差异化、产品渗透率不断提高、竞争水平较高。解决方案通常作为捆绑销售,其中浓缩服务似乎是整个套件的一部分。

- 2022 年 6 月 - Wisecard Technology 和 Zwipe 宣布建立合作伙伴关係,为亚太地区的消费者提供生物识别付款卡。 Wisecard 为 Zwipe Pay 生物辨识付款卡提供客製化脚本,使银行和卡片个人化机构能够更快速、更有效地部署该卡。

- 2022 年 1 月 - 全球创新半导体技术领导者三星电子宣布推出 S3B512C,这是一款具有改进安全功能的新型指纹安全 IC(积体电路)。新系统已通过 EMVCo 和 CC EAL 6+ 认证,并符合万事达卡针对生物识别付款卡的最新 BEPS(生物辨识评估计画摘要)标准。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- COVID-19 对市场的影响

第五章市场动态

- 市场驱动因素

- 智慧卡广泛应用于存取控制和个人识别应用。

- 非接触式付款需求不断成长

- 市场挑战

- 隐私和安全问题以及标准化问题

- 行动电子钱包的出现影响智慧卡需求

第六章 市场细分

- 按类型

- 接触式

- 非接触式

- 按最终用户

- BFSI

- 资讯科技/通讯

- 政府机构

- 运输

- 其他最终用户产业(教育、医疗保健、娱乐等)

- 按国家/地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

第七章 竞争格局

- 公司简介

- Samsung Electronics Co. ltd.

- Watchdata Co., Ltd.

- KONA I Co., Ltd.

- Eastcompeace Technology Co., Ltd

- IDEX Biometrics ASA

- Seshaasai Business Forms Pvt Ltd.

- Advanced Card Systems Ltd.(ACS)

- Pura Group

- Asia Credit Card Production Ltd.

- Thales Group

- Assa Abloy AB

- IDEMIA SAS(Advent International, Inc.)

第八章投资分析

第九章 未来市场展望

The Asia Pacific Smart Card Market is expected to register a CAGR of 5.8% during the forecast period.

Key Highlights

- The increasing digitalization of different government processes and the rising demand for identity cards necessary to access government services create new potential market opportunities. Along with that, the provision of healthcare, licenses, and social benefit documentation of people has resulted in government authorities' introduction of smart cards, hence accelerating the market's growth in the coming years.

- The growing trend of storing data effectively, shifting preferences toward contactless and cashless payments, and digitizing payment processes drive demand for smart cards in healthcare, retail, and hospitality. Additionally, blockchain technology's new customer information security technique and the widespread use of smart cards in the APAC region's most populous nation are projected to provide profitable growth possibilities for smart card producers.

- Also, security and miniaturization are two areas where smart card technology is evolving most quickly. With worldwide migration to higher security EMV banking cards, the newest generation of smart cards is capable of full on-chip cryptography, significantly increasing the security of cards across the industry. In addition, smart cards are increasingly miniaturized into more diverse form factors, such as mini-tags and smart wearables. These trends will continue as smart cards, along with phones or biometrics, are increasingly used as a two-factor credential.

- Additionally, Payment cards are, without even a doubt, essential in everyday life and business. According to the Smart Payment Association (SPA), about 90% of non-cash consumer payments in physical establishments are conducted with cards; in reality, payment cards are essential for obtaining cash. Furthermore, according to the SPA, payment cards facilitate 40-60% of online payments, either directly or indirectly.

- The increased need for a tap-and-pay payment method following the pandemic and the expanding acceptance of smart cards in various industries propel the market forward. Furthermore, high smart card penetration in access control and personal identification applications, rising need for smart cards to access e-government services, and rising demand for online shopping and banking drive smart card market growth throughout the forecast period.

- Furthermore, the COVID-19 pandemic is expected to boost market growth due to consumers' growing need for contactless payment methods worldwide. The expensive cost of implementing electronic point of sale system (EPOS) terminals and the expanding use of mobile wallets and payment applications are expected to limit smart card demand in the coming years.

APAC Smart Card Market Trends

BFSI Sector will Hold Significant Share in Smart Card Deployment Across Asia Pacific

- Smart card usage in BFSI has several advantages, including personal data protection and secure transactions. Smart cards are also employed in the BFSI sector as credit or debit cards, payment authentication cards, and access control cards. It can be used as an electronic wallet by putting funds into the smart card, which can then be transferred using cryptographic protocols to a vending machine or an account.

- Furthermore, as technology progresses, the number of fraudulent operations has risen. As a result, the card and payments sector has undergone a digital transition, with new payment methods, including EMV chips, PIN cards, and mobile wallets, being introduced. Smart cards are gaining traction in the BFSI sector, owing to the difficulty decoding the data stored on them.

- For instance, in January 2021, StashFin, a Singapore-based neo banking start-up, teamed with SBM Bank India to develop a contactless prepaid card powered by VISA and equipped with an EMV chip that provides greater safety and security. The alliance aims to close the credit gap in India by giving underbanked individuals simple access to credit using smart cards.

- Biometric contactless smart cards will likely gain popularity in the BFSI industry over the forecast period, with various financial institutions recognizing the trend. Furthermore, because critical financial operations are at the heart of a business, security is always a top priority. IDEMIA, for example, is advancing the evolution of smart cards by utilizing biometric technologies.

- Similarly, in February 2021, ICICI Bank announced the 'Namma Chennai Smart Card' launch in collaboration with Greater Chennai Corporation and Chennai Smart City Limited. This Rupay-powered co-branded contactless prepaid card at GCC centers would enable various digital payments such as tax and utility bills. The prepaid card can also be used to make retail payments in Chennai, India, and in retail outlets and e-commerce websites around the country.

China will Dominate Smart Card Growth in Asia Pacific

- China was one of the first countries to phase out checks in favor of contactless payments, which led to the developing of digital cards across Asia. The country has implemented smart cards in various industries, including transportation. Since the Chinese government has encouraged industry consolidation to control the industry and improve competitiveness in the global market, rapid consolidation between medium-sized and big businesses is expected.

- In addition, numerous Chinese banks are working on digital yuan hard wallets, and the People's Bank of China has indicated that clients will be able to hold digital currency in both physical and digital wallets. The People's Bank of China (PBOC) has expanded its central bank digital currency (CBDC) trial to include a contactless "hard wallet" and NFC wearables that allow customers to use their digital yuan to pay for goods and services in stores and on public transportation.

- For instance, China Construction Bank stated in June 2021 that it would be testing a biometric 'hard wallet' smart card that would allow clients to store digital yuan and confirm payments made using the central bank's digital currency using their fingerprint. Advanced fingerprint recognition and authentication are used to secure the card's stored value.

- In addition, IDEX Biometrics ASA stated in November 2021 that China UnionPay had approved the latest biometric smart card from its solution partner Hengbao Corporation Ltd for certification (CUP). The new card, which uses IDEX Biometrics' sensor and biometric software solution, passed all China's Bank Card Test Center's requirements (BCTC). This smart card will all be possible with multi-use applications, secure global payments, and additional capabilities such as access control and personal identification.

APAC Smart Card Industry Overview

Several worldwide and regional firms compete for market share in the Asia Pacific smart card market, which is highly competitive. Despite the market's high barriers to entry for new competitors, a few newcomers have achieved traction. Moderate/high product differentiation, increasing product penetration levels, and high competition levels characterize this market. The solutions are usually sold as a bundle, making the condensed offering appear part of the whole suite.

- June 2022 - Wisecard Technology and Zwipe are set to unveil their collaboration to provide biometric payment cards to consumers of Asia Pacific (APAC). Wisecard will supply pre-built customization scripts for Zwipe Pay biometric payment cards, allowing banks and card personalization bureaus to install the cards significantly quicker and more effectively.

- January 2022 - Samsung Electronics Co., Ltd., a global leader in innovative semiconductor technology, has unveiled the S3B512C, a new fingerprint security IC (integrated circuit) with improved security features. The new system is EMVCo and CC EAL 6+ certified, and it meets Mastercard's latest Biometric Evaluation Plan Summary (BEPS) criteria for biometric payment cards.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Smart Cards are Being Extensively Used in Access Control and Personal Identification Applications

- 5.1.2 Growing Demand for Contactless Payments

- 5.2 Market Challenges

- 5.2.1 Privacy and Security Issues and Standardization Concerns

- 5.2.2 Emergence of Mobile Wallets Impacting Demand for Smart Cards

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 Contact-based

- 6.1.2 Contact-less

- 6.2 End-User

- 6.2.1 BFSI

- 6.2.2 IT and Telecommunication

- 6.2.3 Government

- 6.2.4 Transportation

- 6.2.5 Other End-user Industries (Education, Healthcare, Entertainment, etc.)

- 6.3 Country

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India

- 6.3.4 South Korea

- 6.3.5 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Samsung Electronics Co. ltd.

- 7.1.2 Watchdata Co., Ltd.

- 7.1.3 KONA I Co., Ltd.

- 7.1.4 Eastcompeace Technology Co., Ltd

- 7.1.5 IDEX Biometrics ASA

- 7.1.6 Seshaasai Business Forms Pvt Ltd.

- 7.1.7 Advanced Card Systems Ltd. (ACS)

- 7.1.8 Pura Group

- 7.1.9 Asia Credit Card Production Ltd.

- 7.1.10 Thales Group

- 7.1.11 Assa Abloy AB

- 7.1.12 IDEMIA SAS (Advent International, Inc.)

8 INVESTMENT ANALYSIS

9 FUTURE MARKET OUTLOOK

生物识别智慧支付卡市场:按卡片类型、认证技术、介面类型、通路和最终用户划分,全球预测,2026-2032年

生物识别智慧支付卡市场:按卡片类型、认证技术、介面类型、通路和最终用户划分,全球预测,2026-2032年 政府智能卡市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和功能划分晶片级安全增强市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、製程、最终用户、解决方案划分智慧卡市场分析及预测(至2035年):类型、产品、服务、技术、组件、应用、材质类型、部署类型与最终用户

政府智能卡市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和功能划分晶片级安全增强市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、製程、最终用户、解决方案划分智慧卡市场分析及预测(至2035年):类型、产品、服务、技术、组件、应用、材质类型、部署类型与最终用户 2026年全球双介面积体电路卡市场报告

2026年全球双介面积体电路卡市场报告 智慧卡MCU市场-全球产业规模、份额、趋势、机会及预测(依产品、功能、终端用户产业、地区及竞争格局划分),2021-2031年人工智慧智慧型装置市场:2026-2032年全球预测(按产品类型、最终用户、部署类型、公司规模和通路划分)数位电视智慧型装置市场按面板技术、萤幕大小、解析度、作业系统和销售管道-全球预测(2026-2032 年)

智慧卡MCU市场-全球产业规模、份额、趋势、机会及预测(依产品、功能、终端用户产业、地区及竞争格局划分),2021-2031年人工智慧智慧型装置市场:2026-2032年全球预测(按产品类型、最终用户、部署类型、公司规模和通路划分)数位电视智慧型装置市场按面板技术、萤幕大小、解析度、作业系统和销售管道-全球预测(2026-2032 年) 智慧卡市场规模、份额和成长分析(按类型、组件、功能、应用和地区划分)—2026-2033年产业预测

智慧卡市场规模、份额和成长分析(按类型、组件、功能、应用和地区划分)—2026-2033年产业预测 智慧卡市场机会、成长要素、产业趋势分析及预测(2026年至2035年)

智慧卡市场机会、成长要素、产业趋势分析及预测(2026年至2035年)