|

市场调查报告书

商品编码

1636485

中国电动汽车电池阳极:市场占有率分析、产业趋势/统计、成长预测(2025-2030)China Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

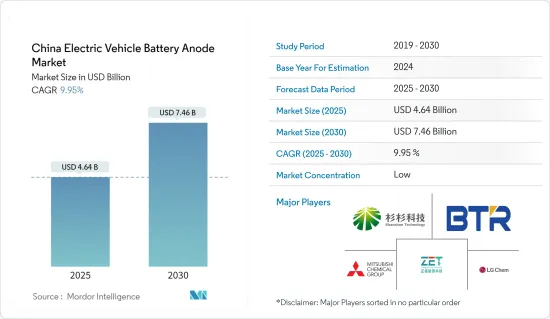

预计2025年中国电动车电池阳极市场规模为46.4亿美元,2030年将达74.6亿美元,预测期间(2025-2030年)复合年增长率为9.95%。

主要亮点

- 从中期来看,政府对电池製造的支持政策和投资以及锂离子电池价格的下降预计将在预测期内推动市场。

- 另一方面,阳极材料的高製造成本预计将抑制未来市场的成长。

- 然而,阳极材料和高效电解质的持续研究和进步可能会提供市场成长的机会。

中国电动汽车动力电池阳极市场趋势

锂离子电池类型预计将占据较大份额

- 最初,锂离子电池主要为行动电话、电脑等家用电器提供动力。然而,锂离子电池的使用已显着扩大,成为中国混合动力汽车和纯电动车(EV)的主要动力来源。这种转变主要是由电动车的环境效益所推动的,电动车不排放二氧化碳和氮氧化物等温室气体。

- 锂离子电池具有高能量密度、经济高效且高效的特点,使其成为电动车(EV)的首选。这种采用的增加推动了製造过程中对阳极材料的需求增加。

- 此外,锂离子材料成本的下降也是电动车锂离子电池製造需求增加的主要原因。 2023年,锂离子电池组的价格将与前一年同期比较%,达到139美元/kWh。随着电池价格下降,电动车将变得更加便宜,从而提高其采用率和市场占有率。需求的激增推动了包括负极在内的电池组件消费量的增加,并推动了提高电池性能的技术进步。

- 未来,技术创新可望提高电动车用锂离子电池的效率,同时对负极材料的需求将会增加。

- 例如,2024年4月,中国电动车製造商宁德时代新能源科技有限公司推出了电动车的磷酸锂铁锂(LFP)电池。这种新型电池的能量密度为205Wh/kg,比目前此类电池的技术水准高出近8%。预计此类发展将增加预测期内对电动车锂离子阳极材料的需求。

- 此外,根据中国工业监督製定的《汽车产业绿色低碳发展蓝图1.0》,到2025年,中国乘用车新能源汽车销售将成长。这样的蓝图也有望为中国电动车负极製造带来未来的机会。

- 因此,由于电动车中锂离子电池的使用量增加和价格下降,预计锂离子电池阳极细分市场在预测期内将大幅成长。

政府对电池製造的政策和投资预计将推动市场

- 政府的支持政策和对电池製造的大量投资正在推动中国电动车电池製造的发展,预计这将增加对电动车电池阳极的需求。政府提供直接财政支援、税收减免和补贴,以降低製造商的成本并鼓励对先进设备的投资。中国电动车製造商受惠于政府补贴。例如,一辆续航里程超过400公里的纯电动插电式汽车将获得12,600元人民币(约2,000美元)的补贴。同时,续航里程为300-400公里的汽车将获得9,100元人民币(约1,400美元)的补贴。

- 此外,中国对电动车日益增长的需求正在推动电动车电池製造计划的投资,并创造了对电动车电池阳极材料的潜在需求。根据国际能源总署(IEA)预测,2023年中国电动车电池需求量将为417GWh,高于去年的314GWh。

- 此外,电动车销量的不断增长正促使电池製造商加大对电动车电池生产的投资,从而创造了对电动车电池阳极材料的需求。根据国际能源总署 (IEA) 预测,2023 年电动车销量将达到 810 万辆,超过 2022 年的 590 万辆。

- 未来,随着国内电动车生产的快速发展以及电动车电池製造投资的增加,电动车电池负极材料的需求预计将增加。例如,2024年5月,中国宣布将投资8.45亿美元开发下一代电池技术,为电动车提供动力。此类投资可能会在预测期内刺激电动车电池製造的需求。

- 因此,政府的支持政策和对电池製造的投资预计将推动市场。

中国电动汽车动力电池阳极产业概况

中国电动车电池阳极市场呈现半分割状态。该市场的主要企业(排名不分先后)包括上海杉杉科技、贝特瑞新材料集团、江西郑都新能源科技、三菱化学集团和LG化学集团。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 电池製造的政府政策和投资

- 降低电池原物料成本

- 抑制因素

- 负极材料製造成本高

- 促进因素

- 供应链分析

- PESTLE分析

- 投资分析

第五章市场区隔

- 依电池类型

- 锂离子

- 铅酸电池

- 其他电池类型

- 按材质

- 锂

- 石墨

- 硅

- 其他的

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Shanghai Shanshan Technology Co., Ltd.

- BTR New Material Group Co., Ltd.

- Jiangxi Zhengtuo New Energy Technology

- Mitsubishi Chemical Group.

- Shanghai Putailai New Energy Technology

- Targray Industries Inc.

- Ningbo Shanshan Co., Ltd.

- LG Chemical Group

- Tokai Carbon Co., Ltd.

- Resonac Holdings Corporation.

- List of Other Prominent Companies

- 市场排名分析

第七章 市场机会及未来趋势

- 加大其他阳极材料的研发力度

简介目录

Product Code: 50003754

The China Electric Vehicle Battery Anode Market size is estimated at USD 4.64 billion in 2025, and is expected to reach USD 7.46 billion by 2030, at a CAGR of 9.95% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, supportive government policies and investments in battery manufacturing and the decreasing price of lithium-ion batteries are expected to drive the market in the forecast period.

- On the other hand, high production cost for anode materials is expected to restrain market growth in the future.

- Nevertheless, the ongoing research and advancement in anode material and efficient electrolytes may offer opportunities for market growth.

China Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Type is Expected to Have a Major Share

- Initially, lithium-ion batteries primarily powered consumer electronics, including mobile phones and personal computers. However, their application has broadened significantly, making them the dominant power source for hybrid and fully electric vehicles (EVs) in China. This transition is primarily driven by the environmental advantages of EVs, which emit no CO2, nitrogen oxides, or other greenhouse gases.

- Due to their high energy density, cost-effectiveness, and efficiency, lithium-ion batteries have become the preferred choice for electric vehicles (EVs). This growing adoption has spurred a rising demand for anode materials during the manufacturing process.

- Further, the decreasing cost of lithium-ion materials is also a significant reason for the increasing demand for lithium-ion battery manufacturing for electric vehicles. In 2023, the price of lithium-ion battery packs decreased by 14% compared to the previous year to USD139/kWh. As battery prices drop, EVs become more affordable, increasing adoption and a larger market share for electric vehicles. This surge in demand will drive higher consumption of battery components, including the anode, and encourage technological advancements to improve battery performance.

- In the future, as technological innovations enhance the efficiency of lithium-ion batteries in electric vehicles, the demand for anode materials is projected to rise simultaneously.

- For instance, in April 2024, Contemporary Amperex Technology Co., a Chinese electric vehicle manufacturer, launched a lithium iron phosphate (LFP) battery for electric vehicles. The new battery has an energy density of 205 Wh per kg, almost 8% higher than the current state of the art for such batteries. Such developments are expected to boost the demand for EV lithium-ion anode materials in the forecast period.

- Additionally, as per Automotive Industry Green and Low-Carbon Development Roadmap 1.0 developed under the supervision of China's Ministry of Industry and Information Technology, electric car sales in China for passenger new energy vehicle (NEV) is expected to reach a 50% share by 2025. Such roadmaps are expected to raise a futuristic oppotunity for EV anode manufacturing too in China.

- Thus, owing to the increasing use of lithium-ion batteries in electric vehicles and decreasing prices, the lithium-ion battery anode segment is expected to grow significantly in the forecast period.

Government Policies and Investments Towards Battery Manufacturing is Expected to Drive the Market

- A combination of supportive government policies and significant investment in battery production drives China's EV battery manufacturing, which, in turn, is expected to boost the demand for electric vehicle battery anodes. The government offers direct financial support, tax incentives, and subsidies, reducing manufacturers' costs and encouraging investment in advanced equipment. Manufacturers of electric vehicles in China benefit from government subsidies. For instance, all-electric plug-in cars boasting a range exceeding 400 km qualify for a subsidy of RMB 12,600 (around USD 2,000). Meanwhile, those ranging between 300 to 400 km receive a subsidy of RMB 9,100 (approximately USD 1,400).

- Further, the country's increasing demand for electric vehicles is fueling investment in electric vehicle battery manufacturing projects, thereby creating a potential need for electric vehicle battery anode materials. According to the International Energy Agency, in 2023, the demand for electric vehicle batteries in China accounted for 417 GWh, up from 314 GWh last year.

- Moreover, rising electric vehicle sales are motivating battery manufacturing companies to invest more in EV battery production, thereby creating demand for EV battery anode materials. According to the International Energy Agency, in 2023, the country's total EV car sales accounted for 8.1 million, higher than 5.9 million in 2022.

- In the future, the demand for EV battery anode materials is expected to increase as the country rushes towards manufacturing electric vehicles, and investments are expected to grow in EV battery manufacturing. For instance, in May 2024, China announced to invest 845 USD million to develop next-generation battery technology powering electricl vehicles. Such investments will boost the demand for electric vehicle battery manufacturing in the forecast period.

- Thus, supportive government policies and investments in battery manufacturing are expected to drive the market.

China Electric Vehicle Battery Anode Industry Overview

The China electric vehicle battery anode market is semi-fragmented. Some of the major players in the market (in no particular order) include Shanghai Shanshan Technology Co., Ltd., BTR New Material Group Co., Ltd., Jiangxi Zhengtuo New Energy Technology, Mitsubishi Chemical Group., and LG Chemical Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 High Production Cost for Anode Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shanghai Shanshan Technology Co., Ltd.

- 6.3.2 BTR New Material Group Co., Ltd.

- 6.3.3 Jiangxi Zhengtuo New Energy Technology

- 6.3.4 Mitsubishi Chemical Group.

- 6.3.5 Shanghai Putailai New Energy Technology

- 6.3.6 Targray Industries Inc.

- 6.3.7 Ningbo Shanshan Co., Ltd.

- 6.3.8 LG Chemical Group

- 6.3.9 Tokai Carbon Co., Ltd.

- 6.3.10 Resonac Holdings Corporation.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Anode Materials

02-2729-4219

+886-2-2729-4219

电动车电池阳极市场-全球产业规模、份额、趋势、机会和预测(按电池类型、材料类型、地区和竞争细分,2020-2030 年)

电动车电池阳极市场-全球产业规模、份额、趋势、机会和预测(按电池类型、材料类型、地区和竞争细分,2020-2030 年) 东协电动车电池阳极:市场占有率分析、产业趋势、成长预测(2025-2030)义大利电动汽车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030)亚太地区电动汽车电池阳极:市场占有率分析、产业趋势与成长预测(2025-2030)欧洲电动车电池负极:市场占有率分析、产业趋势/统计、成长预测(2025-2030)美国电动汽车电池负极:市场占有率分析、产业趋势及成长预测(2025-2030)英国电动车电池负极:市场占有率分析、产业趋势及成长预测(2025-2030)

东协电动车电池阳极:市场占有率分析、产业趋势、成长预测(2025-2030)义大利电动汽车电池负极:市场占有率分析、产业趋势、成长预测(2025-2030)亚太地区电动汽车电池阳极:市场占有率分析、产业趋势与成长预测(2025-2030)欧洲电动车电池负极:市场占有率分析、产业趋势/统计、成长预测(2025-2030)美国电动汽车电池负极:市场占有率分析、产业趋势及成长预测(2025-2030)英国电动车电池负极:市场占有率分析、产业趋势及成长预测(2025-2030)