|

市场调查报告书

商品编码

1636566

拉丁美洲充电电池:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Latin America Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

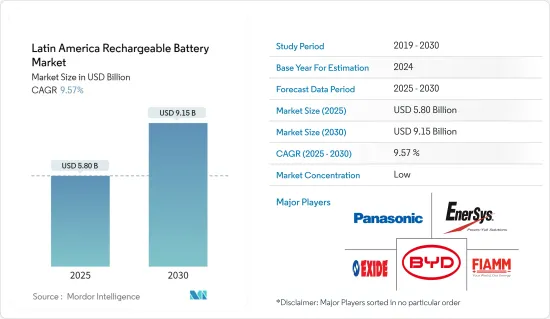

拉丁美洲充电电池市场规模预计到2025年为58亿美元,预计2030年将达到91.5亿美元,预测期内(2025-2030年)复合年增长率为9.57%。

主要亮点

- 从中期来看,锂离子电池价格的下降、电动车普及率的提高以及可再生能源的日益采用预计将在预测期内推动拉丁美洲二次电池市场的发展。

- 相反,原材料供需之间的不匹配将阻碍预测期内的市场成长。

- 然而,资料中心等商业基础设施的需求不断增长,以及电池回收和二次电池应用的需求不断增长,预计将为拉丁美洲二次电池市场创造重大机会。

- 由于电动车销量的快速成长和可再生能源的普及,预计巴西二次电池市场将显着成长。

拉丁美洲充电电池市场趋势

锂离子电池成长显着

- 在预测期内,锂离子电池(LIB)预计将成为拉丁美洲二次电池市场成长最快的细分市场之一。由于其良好的容量重量比,锂离子电池比其他类型的电池更受欢迎。推动锂离子电池采用的其他因素包括卓越的性能(特点是长寿命和低维护)、长寿命和下降的价格趋势。

- 与传统铅酸电池相比,锂离子电池具有明显的技术优势。例如,铅酸电池的使用寿命通常约为 400 至 500 次循环,而可充电锂离子电池的平均寿命令人印象深刻,超过 5,000 次循环。此外,锂离子电池需要较少的维护和更换。它还在整个放电週期中保持稳定的电压,确保连接的电气组件具有更持久的效率。

- 近年来,产业巨头纷纷加强投资力度,注重规模经济和研发,以提高电池性能。这种竞争的加剧大大降低了锂离子电池的价格。由于技术进步、製造优化以及原材料成本降低,锂离子电池的体积加权平均价格已从2013年的780美元/kWh大幅下降至2023年的139美元/kWh。预测显示,2025 年将进一步下降至约 113 美元/kWh,2030 年将进一步下降至 80 美元/kWh,这使得锂离子电池成为越来越有吸引力的选择。

- 从历史上看,锂离子电池主要用于行动电话和笔记型电脑等家用电子电器。然而,随着可再生能源领域的电动车和电池能源储存系统(BESS)越来越依赖锂离子电池,它们的作用正在扩大。

- 儘管拉丁美洲的锂离子电池製造业仍处于起步阶段,但由于该地区丰富的重要原材料蕴藏量和多样化终端用户不断增长的需求,预计该市场将快速成长。

- 拉丁美洲被称为“锂三角”,拥有丰富的锂蕴藏量,这对锂离子电池至关重要。这个三角区包括阿根廷、玻利维亚和智利,这三个国家合计持有全球一半以上的锂蕴藏量。由于阿塔卡马沙漠广泛存在富锂卤水矿床,智利是锂生产的领导者。儘管采矿面临挑战,玻利维亚的乌尤尼盐沼仍然是世界上最大的锂蕴藏量之一。阿根廷在普纳地区拥有盐田,也扮演重要角色。这些国家共同构成全球锂离子电池生产供应链不可或缺的一部分。

- 根据美国地质调查局预测,2023年中期,智利锂产量约44,000吨,阿根廷为9,600吨,巴西为4,900吨。拉丁美洲产量如此之大,在世界锂离子电池领域中占据着至关重要的地位。

- 拉丁美洲国家正在加强深化对电动车供应链的参与。阿根廷、智利、玻利维亚和巴西等国家正在寻求利用其丰富的矿产资源、提高加工能力和汽车製造,将其开采的大部分锂转化为电池化学品。正如阿根廷矿业相关人员强调的那样,该公司也进军电池和电动车的生产。

- 2023年4月,中国领先的电动车製造商比亚迪宣布计画斥资2.9亿美元在智利安託法加斯塔地区兴建一座锂阴极工厂。预计此类策略倡议将在未来几年激增。

- 2023 年中期,阿根廷政府宣布了建造首家锂离子电池工厂的计画。该工厂将使用美国主要矿业公司 Livent Corporation 在当地采购和加工的碳酸锂。该工厂由国有 YPF 子公司 YPF Tecnologia (Y-TEC) 建造,标誌着阿根廷致力于为其丰富的锂蕴藏量增值的承诺。该公司将投资700万美元,目标年产能13MWh、固定式蓄电池1000个。此外,我们强调向热衷于生产锂离子电池的当地公司提供技术转移的机会。

- 锂离子电池因其重量轻、充电速度快、充电週期长和成本下降而有望主导市场,特别是由于该地区锂蕴藏量巨大和工业进步。

巴西,预计将出现显着成长

- 预计巴西将在不久的将来成为拉丁美洲充电电池市场的参与企业。这种快速成长的关键驱动因素是电动车、可再生能源和消费品等各个领域对电池的需求不断增长。此外,该行业的扩张得到了政府支持措施和国内创新的支持。

- 近年来,由于政府的激励措施,电动车(EV)在巴西迅速普及。巴西2023年的电动车销量将达到约52,000辆(33,000辆PHEV、19,000辆BEV),较2022年的18,500辆(10,000辆PHEV、8,500辆BEV)大幅成长。电动车销量的快速成长预计将振兴二次电池市场。

- 从 2024 年 1 月开始,巴西将对 100% 进口电动车 (EV) 征收 10% 的课税。对此,多家中国汽车製造商正活性化本土投资。其中,比亚迪正在巴西建立生产基地,计画于2024年底至2025年初投产,长城汽车工厂计画于2024年投产。这些措施预计将加强巴西国内电动车製造并扩大对二次电池的需求。

- 巴西正在积极努力减少碳排放并减少对石化燃料的依赖,这反映了全球趋势。为了鼓励向电动车过渡,各国政府正在推出各种补贴和激励措施。一个典型的例子是绿色出行创新计划,该计划于 2023年终启动,将于 2024 年至 2028 年间为开发低排放交通技术的公司提供超过 190 亿巴西雷亚尔的税收优惠。这些倡议将加强电动车产业并有利于二次电池市场。

- 除汽车领域外,工业领域也在推动市场成长。越来越多的产业正在将二次电池用于备用电源和可再生能源储存等应用。快速成长的可再生能源领域,特别是太阳能和风能,正在推动对先进电池技术的需求。

- 根据国际可再生能源机构(IRENA)预测,2023年巴西可再生能源装置容量将达到约194GW,较2020年成长28.8%。到2023年,巴西将拥有超过37吉瓦的太阳能发电能力和超过29吉瓦的风力发电能力。随着政府计划进一步提高电池能源储存系统(BESS)的容量,预计对电池储能係统(BESS)的需求将会增加。

- 2024年5月,挪威能源巨头Statkraft AS宣布投资9.26亿雷亚尔(1.807亿美元),在巴西巴伊亚的两个风电场安装275兆瓦的太阳能发电能力。该太阳能资产名为 Sol de Brotas,将与 519MW Ventos de Santa Eugenia 联合发电厂和 79.8MW Morro do Cruzeiro 风力发电联合发电厂整合。

- Sol de Brotas 计划于 2024 年建成,将使用 BESS 技术,并将分阶段开始运营:Morro do Cruzeiro 于 2025 年 8 月开始运营,Ventos de Santa Eugenia 于 2025 年 11 月开始运营。

- 2023年初,美国Fractal EMS和巴西You.On在巴西整合了30MW/60MWh电池储能係统(BESS)。 Fractal EMS 强调,BESS 将优化尖峰负载期间的电力供应,提高输电弹性并减少对调峰电站的依赖。此类计划显示巴西对工业二次电池的需求不断增长,尤其是 Fractal EMS 的设备无关方法以及 You.On 选择科华逆变器和 CATL 液冷电池。

- 鑑于这些动态,巴西二次电池市场可能在短期内显着成长。

拉丁美洲充电电池产业概况

拉丁美洲充电电池市场较为分散。该市场的主要企业包括(排名不分先后)Exide Industries Ltd、BYD Company Ltd、FIAMM Energy Technology SpA、Panasonic Holdings Corporation 和 EnerSys。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电动车的扩张

- 增加可再生能源的部署

- 抑制因素

- 原料供需不匹配

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品/服务的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 科技

- 铅酸电池

- 锂离子

- 其他技术(NiMh、Nicd 等)

- 目的

- 汽车电池

- 工业电池(用于电源、固定电池(电信、UPS、能源储存系统(ESS) 等)

- 可携式电池(家用电子电器产品等)

- 其他的

- 地区

- 巴西

- 墨西哥

- 智利

- 哥伦比亚

- 阿根廷

- 其他拉丁美洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- BYD Company Ltd

- EnerSys

- Panasonic Holdings Corporation

- Exide Industries Ltd

- FIAMM Energy Technology SpA

- C&D Technologies Inc.

- Duracell Inc.

- Saft Groupe SA

- Clarios

- Acumuladores Moura SA

- 其他知名公司名单(公司名称、总部地点、收益、相关产品、业务部门、联络资讯等)

- 市场排名分析

第七章 市场机会及未来趋势

- 资料中心等商业基础设施的需求

- 电池回收和二次利用的需求

简介目录

Product Code: 50004072

The Latin America Rechargeable Battery Market size is estimated at USD 5.80 billion in 2025, and is expected to reach USD 9.15 billion by 2030, at a CAGR of 9.57% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing adoption of renewable energy are expected to drive the Latin America rechargeable battery market during the forecast period.

- Conversely, a mismatch in the demand and supply of raw materials is poised to impede the market's growth during the forecast period.

- However, rising demand from commercial infrastructures like data centers, coupled with the growing need for battery recycling and the second-life application of batteries, is set to unlock vast opportunities for the rechargeable battery market in Latin America.

- Brazil stands to see substantial growth in the rechargeable battery market, driven by surging electric vehicle sales and a broader adoption of renewable energy in the region.

Latin America Rechargeable Battery Market Trends

Lithium-ion Batteries to Witness Significant Growth

- During the forecast period, lithium-ion batteries (LIB) are poised to be among the fastest-growing segments in the Latin American rechargeable battery market. Their favorable capacity-to-weight ratio is making lithium-ion batteries increasingly popular compared to other types. Additional factors driving their adoption include superior performance (characterized by longevity and low maintenance), an extended shelf life, and a downward trend in prices.

- Offering distinct technical advantages, lithium-ion (Li-ion) batteries outshine traditional lead-acid batteries. For instance, while lead-acid batteries typically last for about 400-500 cycles, rechargeable Li-ion batteries boast an impressive average of over 5,000 cycles. Furthermore, Li-ion batteries demand less frequent maintenance and replacement. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for connected electrical components.

- In recent years, major industry players have ramped up investments, focusing on economies of scale and R&D to boost battery performance. This surge in competition has led to a notable drop in lithium-ion battery prices. Thanks to technological advancements, manufacturing optimizations, and falling raw material costs, the volume-weighted average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further decline to approximately USD 113/kWh by 2025 and USD 80/kWh by 2030, making lithium-ion batteries an increasingly attractive option.

- Historically, lithium-ion batteries found their primary application in consumer electronics like mobile phones and laptops. However, their role has expanded, with electric vehicles and battery energy storage systems (BESS) in the renewable energy sector increasingly relying on them.

- While the lithium-ion battery manufacturing industry in Latin America is still in its nascent stages, the region's abundant reserves of essential raw materials and the surging demand from diverse end-users signal a rapid market growth.

- Latin America, often dubbed the Lithium Triangle, boasts vast lithium reserves, a crucial component for lithium-ion batteries. This triangle encompasses Argentina, Bolivia, and Chile, collectively holding over half of the world's known lithium reserves. Chile leads in production, thanks to its extensive lithium-rich brine deposits in the Atacama Desert. Bolivia's Salar de Uyuni stands out as one of the globe's largest lithium reserves, despite extraction challenges. Argentina, with its salt flats in the Puna region, also plays a significant role. Together, these nations are integral to the global lithium-ion battery production supply chain.

- According to the US Geological Survey, lithium production figures for mid-2023 were approximately 44,000 metric tons in Chile, 9,600 metric tons in Argentina, and 4,900 metric tons in Brazil. Such substantial output positions Latin America as a pivotal player in the global lithium-ion battery landscape.

- Latin American countries are intensifying efforts to deepen their involvement in the electric vehicle supply chain. By capitalizing on their mineral wealth, enhancing processing capabilities, and eyeing vehicle manufacturing, nations like Argentina, Chile, Bolivia, and Brazil aim to transform more of their mined lithium into battery chemicals. They're also venturing into battery and electric vehicle manufacturing, as highlighted by Argentina's mining officials.

- In April 2023, BYD Co Ltd, China's leading electric vehicle manufacturer, announced plans for a USD 290 million lithium cathode factory in Chile's Antofagasta region, as reported by Chile's economic development agency, CORFO. Such strategic moves are expected to proliferate in the coming years.

- In mid-2023, the Argentinean government revealed plans for its inaugural lithium-ion battery plant. This facility will utilize lithium carbonate sourced and processed locally by US mining giant Livent Corporation. Constructed by YPF Tecnologia (Y-TEC), a subsidiary of the state-owned YPF, the plant signifies Argentina's commitment to adding value to its rich lithium reserves. With a USD 7 million investment, the facility aims for an annual production capacity of 13MWh, translating to 1,000 stationary energy storage batteries. Moreover, it emphasizes technology transfer opportunities for local firms keen on lithium-ion battery production.

- Given their lightweight nature, rapid charging capabilities, extended charging cycles, and the backdrop of declining costs, lithium-ion batteries are set to dominate the market, especially with the region's significant lithium reserves and industry advancements.

Brazil is Expected to Witness Significant Growth

- Brazil is poised to emerge as a dominant player in the Latin American rechargeable battery market in the near future. This surge is primarily fueled by the escalating demand for batteries across diverse sectors, notably electric mobility, renewable energy, and consumer goods. Furthermore, the industry's expansion is bolstered by supportive government initiatives and technological innovations within the nation.

- Recently, Brazil has seen a swift uptick in electric vehicle (EV) adoption, thanks to government-backed incentives. In 2023, Brazil's EV sales reached approximately 52,000 units (33,000 PHEV and 19,000 BEV), a substantial leap from 2022's 18,500 units (10,000 PHEV and 8,500 BEV). This surge in EV sales is anticipated to bolster the rechargeable battery market in the years ahead.

- Starting January 2024, Brazil imposed a 10% tax on imported 100% electric vehicles (EVs), set to escalate to 18% in July and peak at 35% by July 2026. In response, several Chinese automakers are ramping up local investments. Notably, BYD is establishing a manufacturing complex in Brazil, targeting production by late 2024 or early 2025, while Great Wall Motor's plant is set to commence operations in 2024. These moves are expected to enhance Brazil's domestic EV manufacturing and amplify the demand for rechargeable batteries.

- Echoing global trends, Brazil is actively working to curtail carbon emissions and reduce fossil fuel reliance. To facilitate this transition to electric mobility, the government has rolled out various subsidies and incentives. A prime example is the Green Mobility and Innovation Programme launched at the end of 2023, offering over BRA 19 billion in tax incentives from 2024 to 2028 for companies developing low-emission transport technologies. Such initiatives are poised to bolster the EV sector, subsequently benefiting the rechargeable battery market.

- Beyond the automotive realm, the industrial sector is also driving market growth. Industries are increasingly turning to rechargeable batteries for applications like backup power and renewable energy storage. The burgeoning renewable energy sector, especially solar and wind, is fueling the demand for advanced battery technologies.

- According to the International Renewable Energy Agency (IRENA), Brazil's renewable energy capacity reached about 194 GW in 2023, marking a 28.8% increase from 2020. In 2023, Brazil boasted over 37 GW in solar and 29 GW in wind energy capacities. With government plans to further boost these capacities, the demand for battery energy storage systems (BESS) is set to rise.

- In May 2024, Norwegian energy giant Statkraft AS unveiled a BRL 926 million (USD 180.7 million) investment to install 275 MW of solar capacity at two wind parks in Bahia, Brazil. The solar asset, named Sol de Brotas, will integrate with the 519 MW Ventos de Santa Eugenia complex and the 79.8 MW Morro do Cruzeiro wind power complex.

- Scheduled for construction in 2024, Sol de Brotas will utilize BESS technology, with operations commencing in phases: Morro do Cruzeiro in August 2025 and Ventos de Santa Eugenia in November 2025.

- In early 2023, United States-based Fractal EMS Inc and Brazil's You.On integrated a 30 MW/60 MWh battery energy storage system (BESS) in Brazil. Fractal EMS highlighted that the BESS will optimize power delivery during peak loads, enhancing transmission line resilience and reducing reliance on peaker plants. Such projects, especially with Fractal EMS's equipment-agnostic approach and You.On's choice of Kehua inverters and CATL liquid-cooled batteries, signal a growing trend in Brazil, boosting the demand for industrial rechargeable batteries.

- Given these dynamics, Brazil's rechargeable battery market is set for substantial growth in the foreseeable future.

Latin America Rechargeable Battery Industry Overview

The Latin Americarechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Exide Industries Ltd, BYD Company Ltd, FIAMM Energy Technology SpA, Panasonic Holdings Corporation, and EnerSys.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Growing Renewable Energy Installation

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Mexico

- 5.3.3 Chile

- 5.3.4 Colombia

- 5.3.5 Argentina

- 5.3.6 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 EnerSys

- 6.3.3 Panasonic Holdings Corporation

- 6.3.4 Exide Industries Ltd

- 6.3.5 FIAMM Energy Technology SpA

- 6.3.6 C&D Technologies Inc.

- 6.3.7 Duracell Inc.

- 6.3.8 Saft Groupe SA

- 6.3.9 Clarios

- 6.3.10 Acumuladores Moura S.A.

- 6.4 List of Other Prominent Companies (Company Name, Headquarters, Revenue, Relevant Products, Operating Sector, Contact Details, etc.) (In Brief Tabular Format)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Demand from Commercial Infrastructures Such as Data Centers

- 7.2 Need for a Battery Recycling and Second-life Applications

02-2729-4219

+886-2-2729-4219

充电电池市场:2026-2032年全球市场预测(按电池类型、电压、外形尺寸、应用和销售管道)

充电电池市场:2026-2032年全球市场预测(按电池类型、电压、外形尺寸、应用和销售管道) 充电电池市场规模、份额、趋势和预测:按电池类型、容量、应用和地区划分,2026-2034年

充电电池市场规模、份额、趋势和预测:按电池类型、容量、应用和地区划分,2026-2034年 全球先进可充电电池回收市场(2026-2046)日本可充电电池市场规模、份额、趋势及预测(按电池类型、容量、应用和地区划分,2026年至2034年)柔性锂陶瓷电池市场按类型、应用和最终用户划分,全球预测(2026-2032年)

全球先进可充电电池回收市场(2026-2046)日本可充电电池市场规模、份额、趋势及预测(按电池类型、容量、应用和地区划分,2026年至2034年)柔性锂陶瓷电池市场按类型、应用和最终用户划分,全球预测(2026-2032年) 全球可充电电池市场(2024-2035 年)- 第 32 版

全球可充电电池市场(2024-2035 年)- 第 32 版 充电灯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

充电灯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 东南亚充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)中东/北非二次电池市场占有率分析、产业趋势、成长预测(2025-2030)中东充电电池:市场占有率分析、产业趋势与成长预测(2025-2030)

东南亚充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)中东/北非二次电池市场占有率分析、产业趋势、成长预测(2025-2030)中东充电电池:市场占有率分析、产业趋势与成长预测(2025-2030)

▼