|

市场调查报告书

商品编码

1637857

德国垃圾焚化发电:市场占有率分析、产业趋势、成长预测(2025-2030)Germany Waste-to-Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

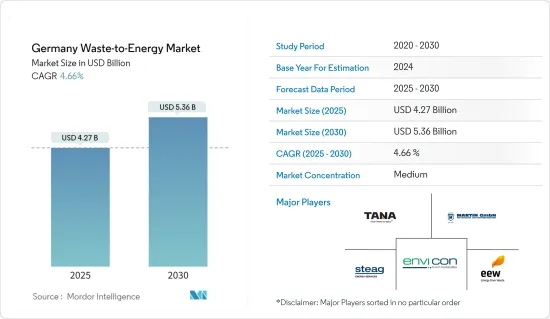

德国垃圾焚化发电市场规模预计到2025年为42.7亿美元,预计2030年将达到53.6亿美元,预测期间(2025-2030年)复合年增长率为4.66%。

主要亮点

- 大量废弃物产生是该国的一个紧迫问题,废弃物发电被认为是满足该国不断增长的电力和废弃物管理需求的最有前途和可持续的解决方案之一。废弃物产生量的增加、为满足永续城市生活需求而对废弃物管理的兴趣日益浓厚,以及对非石化燃料能源来源的日益关注,正在推动该国废弃物能源市场的采用。

- 然而,德国的废弃物回收率仍位居世界前列,废弃物焚烧,这正在影响该国的市场成长。此外,欧盟委员会决定将欧洲转变为更循环的经济,并在 2035 年之前将城市固态废弃物的回收率提高到 65% 以上,预计将对马苏垃圾焚化市场产生影响。

新兴的垃圾焚化发电技术,例如 Dendro Liquid Energy (DLE),其效率提高了四倍,并且具有工厂无排放气体或废水问题等其他优点,预计将在未来几年继续相关人员。的机会。

德国废弃物发电市场趋势

基于热的废弃物能源转化主导市场

- 在热力或都市垃圾焚烧方法中,燃烧废弃物会产生废气。这些废气产生蒸气用于发电以及区域供热和製冷。

- 焚烧过程的主要目的是减少都市固态废弃物(MSW)的体积和质量,并使废弃物在燃烧过程中保持化学惰性,而不需要额外的燃料。如果过程中收集的废弃物的热值超过 7 MJ/kg,则认为使用焚化炉既经济又有效率。

- 就技术而言,热处理在垃圾发电市场中最为普遍。在热条件下,焚烧是最广泛和核准的技术。根据联邦统计局(Destatis)统计,截至 2021 年,德国有超过 156 座废弃物正在运作。然而,较低的初始投资、资本成本和每吨运行维护成本使得协同处理和气化成为经济的选择。德国未来的废弃物流将根据可用于热处理的废弃物和残留物的出现和可用性以及能源回收设施的能力发展来确定。

- 目前,焚烧是最知名的垃圾焚化发电技术。气化和热解过程产生可燃合成气(syngas),用于发电或进一步精製和提炼用于燃气涡轮机和发动机中直接发电。

- 根据国际可再生能源机构预测,2022年德国生质能源装置容量将为9,880兆瓦,高于2021年的9,825兆瓦。因此,德国垃圾焚化发电市场预计将随着生质能源能的增加而成长。

- 另一方面,德国在处理城市废弃物方面已将重点从处置转向预防和回收。都市废弃物仅占该国产生的所有废弃物的 10% 左右,但预防城市固体废弃物可以减少整个废弃物转化阶段和所消费产品的生命週期对环境的影响。

- 对各种废弃物管理方法的生命週期评估表明,与透过燃烧产生能量相比,废弃物预防、再利用、回收和堆肥等替代策略可产生三到五倍的能量。

- 例如,在焚化炉中燃烧一吨纸会产生约 8,200 兆焦耳的能量。然而,如果回收相同的材料,将节省约 35,200 兆焦耳的能源。因此,包括德国在内的一些欧洲国家开始关注回收利用,这对研究市场来说是一种限制。

- 然而,德国废弃物能源产出的增加被认为主要是由于 2005 年因甲烷排放增加而禁止掩埋。对掩埋的禁令可能会增加对垃圾焚化发电发电厂的需求,以容纳最初掩埋的废弃物。

- 基于上述情况,基于热的废弃物能源转换预计将主导市场。

德国废弃物回收率上升预计将抑制市场

- 德国的回收率很高:家庭废弃物为67.6%,工业废弃物和商业废弃物为70%左右。此外,儘管废弃物产生量迅速增加,但德国仅有156座热废弃物厂在运作,处理量超过2,500万吨。此外,废弃物的能源效率有限,预计将阻碍该国垃圾焚化发电市场的成长。

- 德国的废弃物回收率仍位居世界前列,比废弃物焚烧具有更好的经济效益,影响该国的市场成长。

- 此外,欧盟委员会通过一项决议,将欧洲转变为循环经济,到2035年将城市固态废弃物的回收率提高到65%以上,预计将对焚烧市场产生影响。

- 此外,固态燃烧残渣的最终处理困难且昂贵,造成严重的环境问题。此外,垃圾焚化发电市场波动较大,长期缺乏稳定的市场环境也预计将限制其在预测期内的成长。

- 因此,鑑于上述几点,预计由于德国废弃物回收率的提高,市场将受到限制。

德国垃圾焚化发电产业概况

德国废弃物市场适度细分。主要企业(排名不分先后)包括 Tana Oy、Martin GmbH、Envi Con &Plant Engineering GmbH、EEW Energy from Waste 和 STEAG Energy Services GmbH。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义与研究假设

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 至2028年市场规模及需求预测(单位:十亿美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 产生大量生活废弃物

- 日益关注非石化燃料来源

- 抑制因素

- 德国的废弃物回收率

- 促进因素

- 供应链分析

- PESTLE分析

第五章市场区隔

- 科技

- 身体的

- 热

- 生物

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Tana Oy

- Martin GmbH

- Envi Con & Plant Engineering GmbH

- STEAG Energy Services GmbH

- EEW Energy from Waste GmbH

第七章 市场机会及未来趋势

- 新兴的废弃物技术,如 Dendro Liquid Energy (DLE)

The Germany Waste-to-Energy Market size is estimated at USD 4.27 billion in 2025, and is expected to reach USD 5.36 billion by 2030, at a CAGR of 4.66% during the forecast period (2025-2030).

Key Highlights

- With the high amount of waste generation becoming a pressing issue in the country, harnessing energy from waste is considered one of the most promising and sustainable solutions for the country's growing electricity and waste management needs. The increasing amount of waste generation, the growing concerns for its management to meet the need for sustainable urban living, and the increasing focus on non-fossil fuel sources of energy have been driving the adoption of the waste-to-energy market in the country.

- However, the recycling rate of waste in Germany remains among the highest in the world and also offers greater economic benefits than waste incineration, which has affected market growth in the country. Besides, the adoption of the resolution by the European Commission to turn Europe into a more circular economy and boost recycling of municipal solid waste to more than 65% by 2035 is expected to affect the market for incineration as well.

The emerging waste-to-energy technologies, such as Dendro Liquid Energy (DLE), which is four times more efficient in terms of electricity generation and has the additional benefit of no emission discharge or effluent problems at plant sites, are expected to create significant opportunities for the market players over the coming years.

Waste to Energy Germany Market Trends

Thermal Based Waste-to-Energy Conversion is Dominating the Market

- Thermal or municipal solid waste incineration involves waste combustion, which generates flue gases. These flue gases produce steam for electricity production and district heating or cooling.

- The primary goal of the incineration process is to reduce the volume and mass of municipal solid waste (MSW) and to make the waste chemically inert in a combustion process without the need for additional fuel. The utilization of the incineration facility is considered economical and productive when the waste collected for the process has a calorific value of more than 7 MJ/kg.

- Regarding technology, thermal processing is among the most popular in the WtE market. Under thermal conditions, incineration is the most prevalent and approved technology. According to the Federal Statistical Office (Destatis), over 156 waste incineration plants were operational in Germany as of 2021. However, due to the lower initial investment, capital cost, and O&M cost per ton, co-processing and gasification are economical options. Future waste streams in Germany are determined by considering the emergence and availability of wastes and residues potentially usable for thermal treatment and the connected capacity developments of energy recovery facilities.

- At present, incineration is the most well-known WtE technology for MSW processing. The gasification and pyrolysis processes produce a combustible synthetic gas (syngas) that can either be used to generate electricity or further refined and upgraded for direct generation in a gas turbine or engine.

- According to International Renewable Energy Agency, in 2022, Germany's total bioenergy installed capacity accounted for 9880 MW, more significant than 9825 MW in 2021. Thus, with increasing bioenergy capacity, Germany's waste-to-energy market is expected to grow.

- On the flip side, Germany has significantly shifted its focus with respect to municipal waste disposal methods from disposal to prevention and recycling. Although municipal waste represents only around 10% of total waste generated in the country, its prevention can reduce the environmental impact during the waste conversion phase and through the life cycle of the products consumed.

- A life-cycle assessment of different waste management options indicates that three to five times more energy can be saved through alternative strategies, such as waste prevention, reuse, recycling, and composting, compared to generating energy by combustion.

- For instance, an incinerator can burn one ton of paper and generate about 8,200 megajoules of energy. However, recycling the same material saves about 35,200 megajoules of energy. As a result, several European countries, including Germany, have started to focus more on recycling, which is restraining the studied market.

- However, the increase in energy generation through waste in Germany could be primarily attributed to the banning of landfills in 2005 due to the rise in methane emissions. The ban on landfills will likely increase demand for waste-to-energy plants to accommodate the waste initially going into landfills.

- Thus, owing to the above points thermal based waste-to-energy conversion is expected to dominating the Market.

Increasing Recycling Rate of Waste in Germany Expected to Restrain the Market

- Germany has high % recycling rates of 67.6% for household waste and around 70% for industrial and commercial waste. In addition, there are only over 156 thermal waste incineration plants operational in Germany, with a capacity of over 25 million tons, while waste generation is increasing exponentially. Furthermore, there is the limited energy efficiency of waste incineration plants, which is expected to hinder the growth of the waste-to-energy market in the country.

- The recycling rate of waste in Germany remains among the highest in the world and offers more excellent economics than waste incineration, which has affected market growth in the country.

- In addition, the adoption of the resolution by the European Commission to turn Europe into a more circular economy and boost the recycling of municipal solid waste to more than 65% by 2035 is expected to affect the market for incineration as well.

- Moreover, the eventually difficult and expensive disposal of solid combustion residues raises severe environmental concerns. Besides, the insecurity and partly even the lack of long-term stable market conditions for the waste-to-energy market are expected to restrain the growth during the forecast period.

- Thus, owing to the above points, the increasing recycling rate of waste in Germany is expected to restrain the market.

Waste to Energy Germany Industry Overview

The German waste-to-energy market is moderately fragmented. Some of the key players (not in any particular order) include Tana Oy, Martin GmbH, Envi Con & Plant Engineering GmbH, EEW Energy from Waste, and STEAG Energy Services GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition and Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecasts in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 MARKET DYNAMICS

- 4.5.1 Drivers

- 4.5.1.1 The High Amount of Waste Generation in the Country

- 4.5.1.2 The growing Focus on Non-Fossil Fuel Sources

- 4.5.2 Restraints

- 4.5.2.1 The Recycling Rate of Waste in Germany

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Physical

- 5.1.2 Thermal

- 5.1.3 Biological

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Tana Oy

- 6.3.2 Martin GmbH

- 6.3.3 Envi Con & Plant Engineering GmbH

- 6.3.4 STEAG Energy Services GmbH

- 6.3.5 EEW Energy from Waste GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Emerging Waste-to-Energy Technologies, Such as Dendro Liquid Energy (DLE)

亚太地区废弃物製氢(WtH)市场:按应用、技术、废弃物类型和国家分類的分析和预测(2025-2035 年)

亚太地区废弃物製氢(WtH)市场:按应用、技术、废弃物类型和国家分類的分析和预测(2025-2035 年) 欧洲废弃物氢气市场按应用、技术、垃圾类型和国家划分-分析与预测(2025-2035 年)

欧洲废弃物氢气市场按应用、技术、垃圾类型和国家划分-分析与预测(2025-2035 年) 2026-2030年全球废弃物发电市场

2026-2030年全球废弃物发电市场 垃圾焚化发电市场-全球产业规模、份额、趋势、机会及预测(依技术、废弃物类型、应用、地区及竞争格局划分,2021-2031年)

垃圾焚化发电市场-全球产业规模、份额、趋势、机会及预测(依技术、废弃物类型、应用、地区及竞争格局划分,2021-2031年) 全球废弃物发电用炉排锅炉市场(按燃料类型、技术类型、容量、安装类型、运作模式、应用和最终用户划分)预测(2026-2032年)

全球废弃物发电用炉排锅炉市场(按燃料类型、技术类型、容量、安装类型、运作模式、应用和最终用户划分)预测(2026-2032年) 废弃物技术及应用趋势:2032 年市场预测-按废弃物类型、技术、最终用户和地区划分:全球分析

废弃物技术及应用趋势:2032 年市场预测-按废弃物类型、技术、最终用户和地区划分:全球分析 日本垃圾发电市场报告(按技术(物理、热力、生物)和地区划分,2026-2034年)

日本垃圾发电市场报告(按技术(物理、热力、生物)和地区划分,2026-2034年) 垃圾焚化发电(WtE) 市场规模、份额和成长分析(按技术、废弃物类型、应用和地区划分)—产业预测 (2026-2033)

垃圾焚化发电(WtE) 市场规模、份额和成长分析(按技术、废弃物类型、应用和地区划分)—产业预测 (2026-2033) 全球废弃物氢气市场:按应用、技术、废弃物类型和国家分類的分析和预测(2025-2035 年)

全球废弃物氢气市场:按应用、技术、废弃物类型和国家分類的分析和预测(2025-2035 年) 垃圾发电市场:依能源产出、垃圾类型、技术、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

垃圾发电市场:依能源产出、垃圾类型、技术、最终用户、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测