|

市场调查报告书

商品编码

1637895

日本纸包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Japan Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

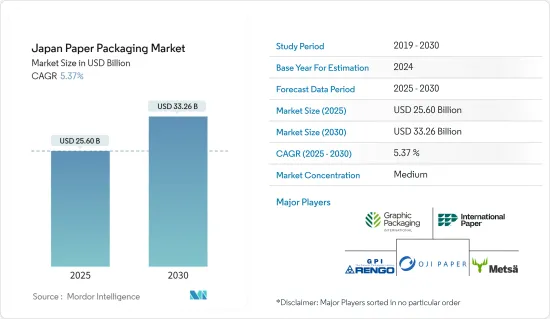

日本纸包装市场规模预计在 2025 年将达到 256 亿美元,预计到 2030 年将达到 332.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.37%。

主要亮点

- 日本是世界上人均塑胶废弃物排放第二大的国家,仅次于美国。预计日本更严格的国际法规将促使製造商满足各行各业对永续包装材料(尤其是纸质包装材料)日益增长的需求。

- 日本是纸製品的重要消费国,其消费领域涵盖报纸纸张、包装、印刷和通讯、卫生和其他用途等多个行业。该地区的食品製造商开始意识到塑胶包装的缺点,并准备改用纸质包装。

- 该地区的大型塑胶购物袋供应商,如工业,已经经历了杂货店对塑胶购物袋的需求下降。下降的原因是法律明确要求顾客为行李支付费用。该公司预计近期订单将下降三分之一。工业宣布投资材料开发,以减少对环境的影响和生产成本。

- 日本製纸等日本主要造纸公司正打算利用塑胶需求下降的机会。日本製纸工业公司宣布扩大其纸基阻隔材料的应用,以保护产品免受空气和水的侵害。据该公司介绍,作为塑胶替代品的纸和纸板包装材料的需求逐年增加。纸质包装材料占日本製纸总销售额的70%。

- 儘管人们越来越关注永续性和减少废弃物,但纸包装产业仍面临挑战。由于人们认为纸质包装不如替代材料环保,因此对纸质包装的需求可能会下降。它们还面临塑胶、金属和玻璃等具有耐用性和成本优势的材料的竞争。此外,纸浆和纸张等原料价格的波动也会影响纸包装製造商的盈利。

日本纸包装市场的趋势

纸板有望实现强劲增长

- 日本的纸和纸板包装市场正在健康成长。食品饮料和加工食品的成长正在推动日本对瓦楞包装的需求。日本加工食品产业的成长预计也将成为纸板包装市场的主要驱动力之一。

- 为了减少塑胶的使用以及相应的策略开发,纸质包装的采用大幅增加,从而推动了市场的发展。此外,该地区的主要纸张製造商正在扩大其市场占有率,预计这将支持市场成长。

- 雀巢日本也推出了其着名套件巧克力棒的新微型包装,并宣布计划在 2025 年使用 100% 可回收包装。新的纸质包装也将获得森林管理委员会的认证,并且完全可回收。

- 据有机贸易协会称,2021 年日本有机包装食品市场的零售额为 4.166 亿美元。预计到 2025 年市场规模将达到 4.271 亿美元。

- 有机食品通常需要符合其环保形象的包装。此类产品通常使用可回收、生物分解性的纸板。随着有机包装食品市场的成长,预计将有更多公司使用纸板来满足消费者对永续包装的偏好。

零售业大幅成长

- 日本是全球成长最快的电子商务市场之一,发展稳定,拥有乐天、亚马逊等全球大型公司的存在。伊藤洋华堂等超级市场电商平台也大力推广使用纸质包装。

- 电子商务的成长导致对包装材料的需求大幅增加。许多电子商务企业更喜欢纸质包装,因为它环保且具有成本效益。

- 纸包装的回收成本通常比塑胶和玻璃等材料低。此外,再生纸市场规模庞大,包装是广泛使用再生纸产品的众多产业之一。

- 再生纸的需求量很大,因此它比替代材料更便宜。纸质包装的回收成本低,对于希望降低包装成本同时支持永续实践的电子商务和零售企业来说,这是一个有吸引力的选择。

- 根据经济产业省统计,2023年12月零售业销售额为1,106.7亿美元,较2023年4月的940.1亿美元略有成长。销售额的成长可能导致零售商扩大其产品供应,从而可能产生对更多样化包装解决方案的需求,包括专门的纸质包装选择,例如客製化设计的盒子和环保材料。

日本纸包装产业概况

市场呈现半分散状态,Graphic Packaging、International Paper Company 和 Rengo 等公司利用塑胶包装需求下降和客户对纸质包装的偏好来推动需求成长,发挥重要作用。为了获得市场占有率,供应商正在加强其产品线,并透过合作和收购来制定经营模式策略,并专注于永续性。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场动态

- 市场驱动因素

- 食品和饮料行业的需求增加

- 对塑胶包装产品的限制将促进需求增加

- 市场限制

- 原材料成本上涨和外包

第六章 市场细分

- 按产品

- 纸板

- 箱板纸

- 纸板

- 其他产品

- 按最终用户产业

- 饮食

- 个人护理

- 居家护理

- 卫生保健

- 零售

- 其他最终用户产业

第七章 竞争格局

- 公司简介

- Graphic Packaging International Corporation

- International Paper Company

- Rengo Co. Ltd

- Oji Paper Co. Ltd

- Metsa Group

- Amcor Group GmbH

- Daio Paper Corporation

- THE PACK CORPORATION

第八章 市场机会与未来趋势

The Japan Paper Packaging Market size is estimated at USD 25.60 billion in 2025, and is expected to reach USD 33.26 billion by 2030, at a CAGR of 5.37% during the forecast period (2025-2030).

Key Highlights

- Japan ranks as the world's second-largest producer of plastic waste per capita, following the United States. Stringent international regulations in Japan are expected to drive manufacturers toward meeting the increasing demand for environmentally sustainable packaging materials, particularly paper packaging, across various industries.

- Japan is a significant consumer of paper-based products across multiple industries, including newsprint, packaging, printing and communication, sanitary, and other miscellaneous applications. Food manufacturers in the region have begun to recognize the disadvantages of plastic wrapping and are preparing to transition to paper packaging.

- Major plastic bag suppliers in the region, such as Fukusuke Kogyo, are experiencing decreased demand for plastic bags at grocery stores. This decline is attributed to customers being legally required to pay explicitly for bags. The company anticipates a one-third decrease in orders in the near future. Fukusuke Kogyo has announced investments in materials development to reduce environmental impacts and production costs.

- Leading paper manufacturing companies in Japan, such as Nippon Paper, are aiming to capitalize on the decreasing demand for plastic. Nippon Paper has announced the expansion of paper-based barrier materials that protect products from air and water. According to the company, the demand for paper and paperboard packaging materials has increased over the years as a replacement for plastics. Paper-based packaging materials account for 70% of Nippon Paper's total sales.

- While sustainability and waste reduction have gained prominence, the paper packaging industry faces challenges. There is a potential decline in demand due to perceptions of paper packaging being less environmentally friendly than alternative materials. The industry also faces competition from materials like plastic, metal, and glass, which offer advantages in durability and cost. Additionally, fluctuating prices of raw materials such as pulp and paper potentially impact the profitability of paper packaging producers.

Japan Paper Packaging Market Trends

Paperboard is Anticipated to Witness Significant Growth

- The paper and paperboard packaging market in Japan is experiencing healthy growth. Beverages and packaged food growth have fueled the demand for corrugated packaging in the country. Japan's growing processed food industry is also expected to act as one of the critical drivers for the paperboard packaging market.

- The market is led by the massively growing adoption of paper packaging in response to reduced plastic usage and the respective strategic developments. Furthermore, major paper manufacturing companies in the region aiming to capitalize on developments to cater to the market are expected to support market growth.

- Also, in line with the announcement of Nestle Japan's plan to use 100% recyclable packaging by 2025, Nestle Japan released new packaging for its famous miniature KitKat Chocolate bars featuring origami paper instead of plastic materials. Also, the new paper packaging is set to receive the Forest Stewardship Council certification and is fully recyclable.

- According to the Organic Trade Association, in 2021, the retail value of the organic packaged food market in Japan accounted for USD 416.6 million. The market size is expected to reach USD 427.1 million in 2025.

- Organic food products often require packaging that aligns with their eco-friendly image. Recyclable and biodegradable paperboard is a popular choice for such products. As the organic packaged food market grows, more companies are expected to use paperboard to meet consumer preferences for sustainable packaging.

Retail is Observing Notable Growth

- Japan boasts one of the world's fastest-growing e-commerce markets, with consistent development and the presence of global giants like Rakuten and Amazon. The country also hosts supermarket e-commerce platforms such as Ito-Yokado and Markets, which promote paper packaging use.

- The growth of e-commerce has significantly increased demand for packaging materials. Many e-commerce businesses prefer paper packaging due to its environmental friendliness and cost-effectiveness.

- Paper packaging typically has lower recycling costs than materials like plastics and glass. Additionally, there is a substantial market for recycled paper, with packaging being one of many industries extensively using recycled paper products.

- The high demand for recycled paper makes it less expensive than alternative materials. Paper packaging's lower recycling cost makes it an attractive option for e-commerce and retail businesses aiming to reduce packaging expenses while supporting sustainable practices.

- According to the Ministry of Economy, Trade and Industry, commercial sales in the retail industry accounted for USD 110.67 billion in December 2023, a slight increase from USD 94.01 billion in April 2023. This rise in sales may lead retailers to expand their product ranges, potentially increasing demand for diverse packaging solutions, including specialized paper packaging options such as custom-designed boxes and eco-friendly materials.

Japan Paper Packaging Industry Overview

The market is semi-fragmented, with the presence of players like Graphic Packaging, International Paper Company, and Rengo Co. Ltd, which play vital roles in upscaling the rise in the demand, leveraging the declining demand for plastic packaging and customers' preference for paper-based packaging. To capture the market share, vendors are strategizing their business models by enhancing their product lines and engaging in collaborations and acquisitions, with a core focus on sustainability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand from the Food and Beverage Sector

- 5.1.2 Regulations on Plastic-based Packaging Products Contributes to Higher Demand

- 5.2 Market Restraints

- 5.2.1 Increasing Raw Material Costs and Outsourcing

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Paperboard

- 6.1.2 Container Board

- 6.1.3 Corrugated Board

- 6.1.4 Other Products

- 6.2 By End-user Industry

- 6.2.1 Food and Beverage

- 6.2.2 Personal Care

- 6.2.3 Home Care

- 6.2.4 Healthcare

- 6.2.5 Retail

- 6.2.6 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Graphic Packaging International Corporation

- 7.1.2 International Paper Company

- 7.1.3 Rengo Co. Ltd

- 7.1.4 Oji Paper Co. Ltd

- 7.1.5 Metsa Group

- 7.1.6 Amcor Group GmbH

- 7.1.7 Daio Paper Corporation

- 7.1.8 THE PACK CORPORATION

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球纸和纸板包装市场(按等级、类型、原料、纸浆、应用和地区划分)- 预测至 2030 年

全球纸和纸板包装市场(按等级、类型、原料、纸浆、应用和地区划分)- 预测至 2030 年 全球纸和纸板包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球纸和纸板包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 宣纸包装市场规模、份额、趋势分析报告:按产品、应用、地区、细分市场预测,2025-2030 年

宣纸包装市场规模、份额、趋势分析报告:按产品、应用、地区、细分市场预测,2025-2030 年 包装纸市场:按材料、按产品类型、按最终用户、按分销管道、按地区全球纸和纸板包装市场规模:等级、类型、应用、区域范围和预测

包装纸市场:按材料、按产品类型、按最终用户、按分销管道、按地区全球纸和纸板包装市场规模:等级、类型、应用、区域范围和预测 日本纸包装市场报告(按类型(折迭纸盒、瓦楞纸箱等)、最终用途行业(食品饮料、医疗保健、个人护理和家庭护理、工业等)和地区)2025-2033再生纸包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测3D 印刷纸及纸板包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测纸包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测软纸包装市场机会、成长动力、产业趋势分析及2025-2034年预测

日本纸包装市场报告(按类型(折迭纸盒、瓦楞纸箱等)、最终用途行业(食品饮料、医疗保健、个人护理和家庭护理、工业等)和地区)2025-2033再生纸包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测3D 印刷纸及纸板包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测纸包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测软纸包装市场机会、成长动力、产业趋势分析及2025-2034年预测