|

市场调查报告书

商品编码

1641865

入门 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Primer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

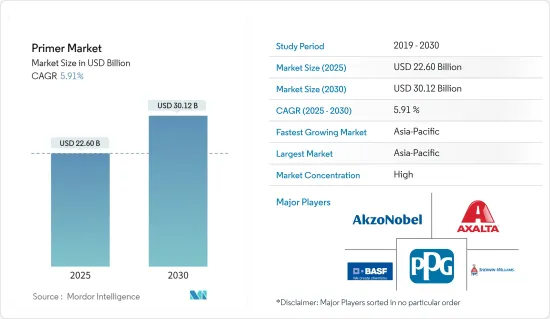

预计 2025 年底漆市场规模为 226 亿美元,到 2030 年将达到 301.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.91%。

COVID-19 疫情对市场产生了负面影响,因为建筑和汽车製造活动已暂时停止,以遏制新的 COVID-19 病例的传播,从而减少了这些终端用户行业的底漆消耗。不过,这种情况在2021年开始有所改善。预计这将在预测期内增加对产品的需求。

关键亮点

- 短期内,亚太地区建设活动的增加和汽车产业的不断发展预计将推动市场成长。

- 另一方面,有关底漆使用的规定可能会阻碍市场成长。

- 生物性底漆使用方面的技术创新有望成为市场成长的机会。

- 亚太地区是全球最大的市场,其中印度、中国和其他国家的需求和消费量最高,预计将主导全球市场。

底漆市场趋势

建筑和施工领域占据市场主导地位

- 底漆广泛用于建筑和施工领域。它可用作墙壁和其他基材上涂漆前的底漆。

- 底漆是一种有色涂料,在涂Undercoats底漆或面漆之前涂在新表面或旧表面上。建筑业的成长在增加油漆和被覆剂的需求方面发挥着重要作用。随着建设活动数量的增加,对油漆和被覆剂的需求也随之增加,最终促进底漆市场的发展。

- 过去几年,由于人口成长、新城市开发、都市区移民增加以及成熟城市老化基础设施更新等因素,建筑和建筑业一直保持成长势头。美元。

- 美国占据北美建筑业的很大份额。美国、加拿大和墨西哥也对建筑业投资做出了重大贡献。

- 根据美国人口普查局的数据,2023年美国年度建筑价值为19,787亿美元,较2022年增加约7.03。

- 亚太地区的建筑业是世界上最大的。由于人口成长、中产阶级的壮大和都市化,中国正经历健康的成长率。

- 受中国和印度住宅建筑市场扩张的推动,预计亚太地区将出现最高成长。预计到2030年,这些国家将占全球中阶的43.3%以上。

- 因此,预计上述因素将在未来几年对市场产生重大影响。

亚太地区占市场主导地位

- 预计亚太地区将在预测期内经历最大的成长。这是由于该地区建筑业和汽车生产的不断发展。

- 亚太地区拥有许多新兴经济体,如印度、中国、印尼和越南。这使得它成为投资者感兴趣的市场。

- 到2030年,全球建筑市场规模预计将达到8兆美元。预计印度、中国和美国等国家将推动大部分成长。

- 中国正经历建筑热潮。中国拥有全球最大的建筑市场,占全球建筑投资总额的20%。到2030年,预计光是中国就在建筑领域投资约13兆美元。

- 根据中国国家统计局预测,2023年中国建筑业总产值将成长1.99%,达到人民币712847.2亿元(108,678亿美元)。

- 此外,印度的住宅产业正在成长,政府的支持和倡议进一步刺激了需求。在 2022-2023 年预算中,住房与城市发展部(MoHUA) 已拨款约 98.5 亿美元用于住宅建设和筹集资金以完成停滞的计划。

- 除了建筑业之外,汽车业也是该地区的主要产业,对底漆的需求很大。

- 亚太地区是全球最有价值汽车製造商的所在地。中国、印度、日本和韩国等国家正致力于加强製造地和发展高效的供应链以提高盈利。

- 根据中国工业协会(CAAM)统计,中国是全球最重要的汽车生产基地,预计2023年汽车总产量将达到3,016万辆,较去年的2,702万辆成长11.6%。根据国际贸易管理局(ITA)预测,2025年国内汽车产量将达3,500万辆。

- 此外,印度的汽车工业是世界第五大汽车工业,预计2030年将成为世界第三大汽车工业。根据国际汽车结构组织(OICA)的数据,到 2023 年,印度的汽车产量预计将成长约 7%,达到 585 万辆。

- 预计上述因素将在未来几年对市场产生重大影响。

底漆产业概览

底漆市场本质上呈现整合状态。主要企业(不分先后顺序)包括 AkzoNobel NV、宣威公司、Axalta Coating Systems LLC、PPG Industries Inc. 和BASF SE。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 亚太地区建设活动不断增加

- 不断发展的汽车产业

- 其他驱动因素

- 限制因素

- 有关底漆使用的严格环境法规

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 按组件

- 树脂

- 丙烯酸纤维

- 环氧树脂

- 聚醋酸乙烯酯

- 醇酸

- 其他树脂(马来酸、聚酯、聚酰胺等)

- 按添加剂

- 分散剂

- 除生物剂

- 表面改质剂

- 其他添加物(防銹剂、盐害抑制剂、乳化剂、稳定剂等)

- 其他成分(溶剂、颜料等)

- 树脂

- 按最终用户产业

- 车

- 建筑和施工

- 家具

- 工业的

- 包装

- 其他终端用户产业(金属加工、塑胶、橡胶)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧的

- 土耳其

- 俄罗斯

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- AkzoNobel NV

- Asian Paints

- Axalta Coating Systems LLC

- BASF SE

- Berger Paints India Limited

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd

- Masco Corporation

- NIPSEA Group

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

- Tikkurila

第七章 市场机会与未来趋势

- 生物性底漆的创新

- 其他机会

The Primer Market size is estimated at USD 22.60 billion in 2025, and is expected to reach USD 30.12 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market as construction and automotive manufacturing activities were temporarily halted to reduce the spread of new COVID-19 cases, thereby decreasing the consumption of primer in these end-user industries. However, the condition started recovering in 2021. This is expected to increase the demand for the product during the forecast period.

Key Highlights

- Over the short term, the growth of the market is likely driven by increasing construction activities in Asia-Pacific and the growing automotive industry.

- On the flip side, regulations regarding the use of primers are likely to hinder market growth.

- Innovations in the use of bio-based primers are expected to act as opportunities for market growth.

- Asia-Pacific is the largest market in the world and is expected to dominate the global market, with the highest demand and consumption from India, China, and other countries.

Primer Market Trends

Building and Construction Segment to Dominate the Market

- Primer is extensively used in the building and construction sectors. It is used as a preparatory coat on walls and other substrates before applying the paint.

- Primers are pigmented coatings that are applied to new or old surfaces prior to the application of undercoats or topcoats. The growing construction industry plays a keen role in the increasing demand for paints and coatings. The greater the increase in the number of construction activities, the greater the demand for paints and coatings, which will eventually boost the market for primers.

- The building and construction industry has been growing for the past few years, owing to factors such as increasing population, development of new cities, growing migration in urban areas, renewal of old infrastructure in established cities, and others, and it is expected to reach a revenue of USD 4.4 trillion by 2030.

- The United States includes a significant share of the construction industry in North America. The United States, Canada, and Mexico also contribute significantly to the construction sector investments.

- According to the US Census Bureau, the annual value for construction in the United States accounted for USD 1,978.7 billion in 2023, which was an increase of about 7.03 compared to 2022.

- The construction sector in Asia-Pacific is the largest in the world. It is growing at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization.

- The highest growth for housing is expected to be registered in Asia-Pacific, owing to the expanding housing construction markets in China and India. These countries are expected to represent over 43.3% of the global middle class by 2030.

- Therefore, the factors mentioned above are expected to have a significant impact on the market in the coming years.

Asia-Pacific to Dominate the Market

- During the forecast period, Asia-Pacific is expected to witness the maximum growth. This is because the construction industry and automotive production in the region are growing.

- Asia-Pacific has a lot of countries with emerging economies, like India, China, Indonesia, and Vietnam. This has made it a market that investors are interested in.

- By 2030, the global construction market is expected to be worth USD 8 trillion. Countries like India, China, and the United States are expected to drive most of this growth.

- China is amid a construction boom. The country has the world's largest building market, accounting for 20% of all construction investment globally. The country alone is expected to spend nearly USD 13 trillion on buildings by 2030.

- According to the National Bureau of Statistics of China, the gross output value of the construction industry in China in 2023 increased by 1.99%, accounting for CNY 71,284.72 billion (USD 10,086.78 billion).

- In addition, the residential sector in India is growing, and government support and initiatives are further boosting demand. In the budget of 2022-2023, the Ministry of Housing and Urban Development (MoHUA) allocated about USD 9.85 billion to construct houses and create funds to complete the halted projects.

- Along with the construction industry, the automotive industry is another major industry in the region contributing to significant demand for primers.

- Asia-Pacific is home to some of the world's most valuable vehicle manufacturers. Countries like China, India, Japan, and South Korea have been working hard to strengthen their manufacturing bases and develop efficient supply chains for greater profitability.

- According to the China Association of Automobile Manufacturers (CAAM), China has the most significant automotive production base in the world, with a total vehicle production of 30.16 million units in 2023, registering an increase of 11.6% compared to 27.02 million units produced last year. As per the International Trade Administration (ITA), domestic automotive production is expected to reach 35 million units by 2025.

- Further, the Indian automotive industry is the fifth largest in the world and is projected to become the third largest by 2030. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), Indian automotive production in 2023 increased by about 7% and was valued at 5.85 million units.

- The above factors are likely to have a significant effect on the market in the coming years.

Primer Industry Overview

The primer market is consolidated in nature. The major players (not in any particular order) include AkzoNobel NV, The Sherwin-Williams Company, Axalta Coating Systems LLC, PPG Industries Inc., and BASF SE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Construction Activities in the Asia-Pacific Region

- 4.1.2 Growing Automotive Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding the Use of Primers

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Ingredient

- 5.1.1 Resin

- 5.1.1.1 Acrylic

- 5.1.1.2 Epoxy

- 5.1.1.3 Poly Vinyl Acetate

- 5.1.1.4 Alkyd

- 5.1.1.5 Other Resins (Maleic, Polyester, Polyamide, etc.)

- 5.1.2 By Additives

- 5.1.2.1 Dispersant

- 5.1.2.2 Biocides

- 5.1.2.3 Surface Modifier

- 5.1.2.4 Other Additives (Rust Inhibitors, Salt Inhibitors, Emulsifiers, Stabilizers, etc)

- 5.1.3 Other Ingredients (Solvent, Pigments, etc.)

- 5.1.1 Resin

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Furniture

- 5.2.4 Industrial

- 5.2.5 Packaging

- 5.2.6 Other End-user Industries (Metalworking, Plastic, and Rubber)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AkzoNobel NV

- 6.4.2 Asian Paints

- 6.4.3 Axalta Coating Systems LLC

- 6.4.4 BASF SE

- 6.4.5 Berger Paints India Limited

- 6.4.6 Hempel A/S

- 6.4.7 Jotun

- 6.4.8 Kansai Paint Co. Ltd

- 6.4.9 Masco Corporation

- 6.4.10 NIPSEA Group

- 6.4.11 PPG Industries Inc.

- 6.4.12 RPM International Inc.

- 6.4.13 The Sherwin-Williams Company

- 6.4.14 Tikkurila

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation of Bio-based Primers

- 7.2 Other Opportunities

2026年全球环氧底漆市场报告

2026年全球环氧底漆市场报告 无溶剂密封剂市场:全球预测(2026-2032 年),按类型、形态、固化机制、应用和分销管道划分自流平底漆市场按技术、包装类型、最终用途、应用类型和分销管道划分,全球预测(2026-2032年)

无溶剂密封剂市场:全球预测(2026-2032 年),按类型、形态、固化机制、应用和分销管道划分自流平底漆市场按技术、包装类型、最终用途、应用类型和分销管道划分,全球预测(2026-2032年) 底漆市场规模、份额和成长分析(按材料、应用、最终用途和地区划分)—2026-2033年产业预测环氧底漆市场按应用、终端用户产业、树脂类型、形态、技术和分销管道划分-2025-2032年全球预测

底漆市场规模、份额和成长分析(按材料、应用、最终用途和地区划分)—2026-2033年产业预测环氧底漆市场按应用、终端用户产业、树脂类型、形态、技术和分销管道划分-2025-2032年全球预测 2030 年包装底漆市场预测:按类型、功能、应用、最终用户、地区进行全球分析

2030 年包装底漆市场预测:按类型、功能、应用、最终用户、地区进行全球分析 全球环氧底漆市场规模(按技术、基材、应用、地区、范围和预测)

全球环氧底漆市场规模(按技术、基材、应用、地区、范围和预测)