|

市场调查报告书

商品编码

1644608

通讯专用逻辑积体电路:市场占有率分析、产业趋势与成长预测(2025-2030 年)Communication Special Purpose Logic IC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

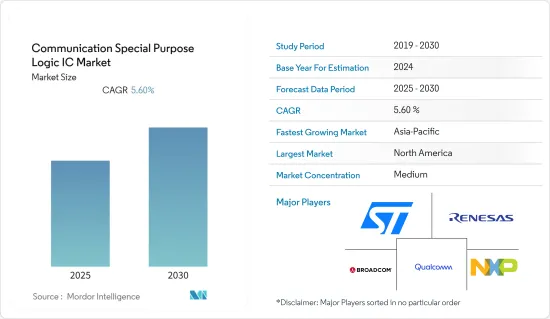

预计预测期内通讯专用逻辑积体电路市场复合年增长率为 5.6%。

专用积体电路 (IC) 旨在解决实现闭合迴路运动和马达速度控制所需的任务。专用积体电路 (IC) 也被设计用于解决实现闭合迴路运动和马达速度控制所需的任务。

开发人员越来越注重打造能够以小封装提供所需效能并最大限度降低功耗的小元件。因此,预计在预测期内,专用逻辑积体电路市场将受到对设备整合日益关注的推动。

随着网路普及率的提高以及对手机、笔记型行动电话和平板电脑等消费性设备的需求不断增长,通讯积体电路市场正在扩大。由于全球对高频段连接服务的需求不断增加,COVID-19 疫情对市场成长产生了积极影响。此外,医疗设备产量的增加也促进了市场的扩大。

由于车辆连网服务的不断增加,汽车产业的快速扩张对市场成长产生了积极影响。此外,预计连网汽车市场将在整个预测期内推动市场成长。

通讯专用逻辑 IC 的市场趋势

汽车产业推动市场成长

通用积体电路用于多种任务,包括计算和资料传输。通用积体电路(IC)存在于电脑处理器中。温度控制、速度控制和其他各种业务由专用 IC 执行。专用IC广泛应用于空调、智慧电视、马达工厂设备、行动电话等。

由于消费者对环境污染意识的增强和油价的飙升,全球对电动车的需求不断扩大,这也扩大了通讯逻辑IC的市场。车对车 (V2V)通讯的潜力在于,它可以透过无线方式传输附近车辆的速度和位置信息,有望帮助缓解交通拥堵、防止碰撞并改善环境。

由于车辆连接选项的增加而导致的汽车销售增加对行业成长产生了积极影响。此外,由于汽车行业的快速成长,预计预测期内市场将继续发展。

该地区拥有强大的汽车製造基础设施和庞大的消费市场。亚太地区是本田、现代、丰田和塔塔等主要汽车製造商的所在地。该地区也是一个巨大的汽车行业市场,拥有各行各业的消费者。根据OICA 2022年的资料,中国2021年生产了约2,140万辆乘用车,而日本生产了约660万辆,印度生产了约360万辆。中国与全球汽车製造商建立了合作伙伴关係,成为该地区最大的汽车生产国,超过韩国、日本和印度,这些国家的国内汽车产业都实力雄厚。随着该地区汽车工业的崛起,研究市场的需求也预计将成长。

中国占很大市场份额

中国拟成立专门机构,鼓励国内企业与英特尔等国际半导体巨头合作,共建软体、材料及製造设备开发中心。北京正加紧发展不受美国制裁的国内半导体供应链。同时,外国政府可能对该倡议持怀疑态度,担心关键技术转移到中国。

2015年,北京推出了「中国製造2025」策略,将半导体列为优先事项。中国透过国家投资平台支持 NAND 快闪记忆体公司长江储存科技等公司,并向晶片产业投入了超过 200 亿美元的资金。在习近平的领导下,政府部门正准备投资中芯国际的新设施,并向材料和製造设备投入资金,以增强供应链。但考虑到中国的技术不足,新建立的海外合作论坛可能对这项努力至关重要。

2021年9月,中国最大的晶片代工製造商中芯国际(SMIC)宣布将在上海自贸区的临港特区建立新工厂。拟建的投资 88.7 亿美元的晶圆厂每月将生产 10 万片 12 吋晶圆。中芯国际将持有合资公司至少 51% 的股份,其余 25% 由上海市政府指定的投资公司持有。今年3月,中芯国际宣布将与深圳市政府合作,投资23.5亿美元建造月产4万片28奈米以上积体电路12吋晶圆的计划。

中国针对半导体和软体产业制定了许多有利法规,包括免税、优惠贷款、智慧财产权保护以及对研发、进出口和人力资源开发的支援。对积体电路製造企业以及积体电路设计、设备、材料、封装、测试、软体等企业给予税务减免或优惠。

随着与美国的技术竞争加剧,中国正加强支持本土软体公司。此趋势涵盖晶片存取、5G网路建置、社群媒体应用、网路监管等多个领域。北京认为科技产业具有战略重要性,预计未来几年政府资金将会增加。

通讯专用逻辑积体电路 (IC) 产业概况

通讯专用逻辑积体电路市场竞争激烈,有多家製造商存在。产品创新、併购是市场参与企业采用的一些技巧。此外,随着积体电路製造流程的改进以适应更多的应用,新的市场参与企业正在扩大其市场占有率并扩大其在新兴国家的足迹。

2021年11月,先进半导体技术供应商瑞萨电子株式会社宣布推出通讯(PLC) 数据机 IC R9A06G061。 R9A06G061无需使用继电器即可在1公里以上的远距上实现高达1Mbps的高速通讯,扩大了PLC的应用范围。

2021 年 8 月 - 领先的先进半导体解决方案提供商瑞萨电子株式会社和领先的电池和电源管理、Wi-Fi、蓝牙、低功耗和工业边缘运算解决方案提供商 Dialog Semiconductor Plc 宣布瑞萨完成对 Dialog 全部已发行和即将发行股本的收购。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响

第五章 市场区隔

- 按地区

- 中国

- 日本

- 台湾

- 印度

- 其他亚太地区

第六章 竞争格局

- 公司简介

- STMicroelectronics

- Renesas Electronics

- ADI

- Broadcom Inc.

- Qualcomm Inc.

- NXP Semiconductors NV

- Marvell Semiconductor, Inc.

- Mediatek, Inc.

- Intel Corporation

- Toshiba Corporation

第七章投资分析

第 8 章:市场的未来

The Communication Special Purpose Logic IC Market is expected to register a CAGR of 5.6% during the forecast period.

Special-purpose ICs are designed to tackle the duties required to accomplish closed-loop motion and motor speed control. Special-purpose ICs have also been designed to tackle the duties required to accomplish closed-loop motion and motor speed control.

Manufacturers are increasingly focusing on developing gadgets that minimize power consumption while delivering the desired performance in a small package. Consequently, the market for Special Purpose Logic ICs is expected to be driven by the increased focus on device integration over the forecast period.

The communication ICs market is expanding due to rising internet penetration and demand for consumer devices such as mobile phones, laptops, and tablets. Because of the rising need for high-band connectivity services around the world, the COVID-19 pandemic is positively impacting the market's growth. Furthermore, the increased production of medical equipment contributed to the market's expansion.

Rapid expansion in the automotive industry is favorably influencing market growth due to the increasing deployment of connection services in cars. Furthermore, the connected automobiles market is expected to drive the market's growth throughout the forecast period.

Communication Special Purpose Logic IC Market Trends

Automotive Industry to drive the Market Growth

While general-purpose ICs are used for various tasks like calculation, data transfer, and other comparable tasks. General-purpose integrated circuits (ICs) are found in computer processors. Temperature control, speed control, and various other duties are performed by special purpose ICs. Specific purpose ICs can be found in air conditioners, smart televisions, factory devices with motors, and mobile phones.

Because of rising consumer awareness about environmental pollution and rising oil prices, the demand for electric vehicles is expanding globally, driving the market for communication logic IC to rise. The potential of vehicle-to-vehicle (V2V) communication to wirelessly transmit information on the speed and position of nearby cars holds enormous promise for reducing traffic congestion, avoiding crashes, and improving the environment.

Increased sales of autos due to increased connectivity options in vehicles are positively impacting the industry growth. Furthermore, the market is expected to develop in the forecast period due to the rapid growth of the automotive sector.

The region has a strong infrastructure for automobile manufacturing and a huge consumption market. Asia-Pacific is the home of major automobile manufacturers such as Honda, Hyundai, Toyota, TATA, etc. The region is also a huge market for the automobile industry, with consumers of all classes. According to the 2022 data by OICA, in 2021, China produced approximately 21.4 million passenger cars, while Japan and India produced approx. 6.6 and 3.6 million cars. While China has partnerships and collaborations with global automobile manufacturers, making it the biggest auto producer in the region, ahead of South Korea, Japan, and India, these countries enjoy a strong domestic automotive sector. With the rise of the auto industry in the region, the demand for the studied market will also grow.

China to hold a significant share in the Market

China intends to create a special agency to encourage collaboration between domestic enterprises and international semiconductor powerhouses like Intel to build software, material, and manufacturing equipment development centers. Beijing is rushing to develop a domestic supply chain for semiconductors that is not subject to US sanctions. On the other hand, foreign governments are likely to be suspicious of this initiative, fearing the transfer of vital technology to China.

In 2015, Beijing introduced the "China Manufacturing 2025" strategy, prioritizing semiconductors. China has supported enterprises like Yangtze Memory Technologies, a NAND flash memory company, through government-backed investment institutions with a war chest of more than USD 20 billion committed to the chip industry. Under Xi's instructions, government-backed institutions are preparing to invest in new SMIC facilities and pump money into materials and manufacturing equipment to strengthen the supply chain. Given the lack of Chinese technology, however, the newly developed forum for foreign collaboration could be critical to the attempt.

In September 2021 - Semiconductor Manufacturing International Corp. (SMIC), China's largest contract chipmaker, announced the establishment of a new plant in the Lin-Gang Special Area, which is part of Shanghai's free trade zone. The proposed USD 8.87 billion foundry is expected to produce 100,000 12-inch wafers monthly. SMIC will own at least 51 % of the joint venture, with a 25% interest held by a Shanghai, government-designated investment company. SMIC stated in March that it would partner with the Shenzhen government to invest USD 2.35 billion in a project to produce 40,000 12-inch wafers per month using 28nm and higher integrated circuits.

China has enacted plenty of beneficial regulations for the semiconductor and software industries, including tax rebates, attractive financing, IP protection, and support for R&D, import and export, and talent development, among other things. Tax exemptions and discounts will be available to IC manufacturing companies and IC design, equipment, materials, packaging, testing, and software companies.

Due to the escalating technology standoff with the United States, China is strengthening its efforts to strengthen local software companies. This trend has touched many sectors, including chip access, 5G network construction, social media applications, and internet regulation. Beijing considers the technology industry strategically important, and government funding is projected to grow in the coming years.

Communication Special Purpose Logic IC Industry Overview

The Communication Special Purpose Logic IC Market is highly competitive, with multiple manufacturers. Product innovation, mergers, and acquisitions are some of the techniques used by market players. Furthermore, as the IC manufacturing process improves, allowing for more applications, new industry participants are extending their market presence and expanding their corporate footprint in emerging nations.

In November 2021 - The R9A06G061 power line communication (PLC) modem IC was introduced by Renesas Electronics Corporation, a leading provider of sophisticated semiconductor technologies. The R9A06G061 provides high-speed communication of up to 1 Mbps across extended distances of a kilometre or more without the use of relays, broadening the scope of PLC applications.

In August 2021 - Renesas Electronics Corporation, a leading provider of advanced semiconductor solutions, and Dialog Semiconductor Plc, a leading provider of battery and power management, Wi-Fi, Bluetooth, low energy, and Industrial edge computing solutions, have announced the completion of Renesas' acquisition of Dialog's entire issued and to be issued share capital.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Value Chain / Supply Chain Analysis

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 COVID-19 Impact on the Market

5 MARKET SEGMENTATION

- 5.1 By Geography

- 5.1.1 China

- 5.1.2 Japan

- 5.1.3 Taiwan

- 5.1.4 India

- 5.1.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 STMicroelectronics

- 6.1.2 Renesas Electronics

- 6.1.3 ADI

- 6.1.4 Broadcom Inc.

- 6.1.5 Qualcomm Inc.

- 6.1.6 NXP Semiconductors N.V.

- 6.1.7 Marvell Semiconductor, Inc.

- 6.1.8 Mediatek, Inc.

- 6.1.9 Intel Corporation

- 6.1.10 Toshiba Corporation

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

全球逻辑积体电路市场规模、份额、产业分析报告:按类型、通用逻辑积体电路类型、按技术、按应用、按地区划分,展望与预测(2025-2032年)

全球逻辑积体电路市场规模、份额、产业分析报告:按类型、通用逻辑积体电路类型、按技术、按应用、按地区划分,展望与预测(2025-2032年) 逻辑 IC 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

逻辑 IC 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 标准逻辑积体电路的全球市场

标准逻辑积体电路的全球市场 2025-2029年全球标准逻辑IC市场

2025-2029年全球标准逻辑IC市场 逻辑 IC 市场规模、份额和趋势分析报告:按类型、技术、应用、地区和细分市场预测,2025 年至 2033 年

逻辑 IC 市场规模、份额和趋势分析报告:按类型、技术、应用、地区和细分市场预测,2025 年至 2033 年 逻辑IC(积体电路) -市场占有率分析、产业趋势与统计、成长预测(2025-2030)全球消费标准逻辑IC-市场占有率分析、产业趋势与统计、成长预测(2025-2030)标准逻辑 IC:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)消费性专用逻辑IC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)用于电脑和周边设备的标准逻辑 IC -市场占有率分析、行业趋势和统计、成长预测 (2025-2030)

逻辑IC(积体电路) -市场占有率分析、产业趋势与统计、成长预测(2025-2030)全球消费标准逻辑IC-市场占有率分析、产业趋势与统计、成长预测(2025-2030)标准逻辑 IC:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)消费性专用逻辑IC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)用于电脑和周边设备的标准逻辑 IC -市场占有率分析、行业趋势和统计、成长预测 (2025-2030)