|

市场调查报告书

商品编码

1645150

电视与机上盒:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Television And Set Top Box - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

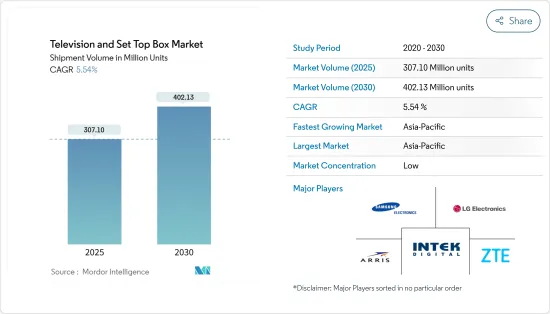

电视和机上盒市场规模(基于出货量)预计将从 2025 年的 3.071 亿台扩大到 2030 年的 4.0213 亿台,预测期内(2025-2030 年)的复合年增长率为 5.54%。

关键亮点

- 机上盒中人工智慧(AI)的采用激增、新兴市场中互联网和宽频普及率的提高以及基于作业系统的设备的持续部署,正在推动市场发展发挥重要作用。

- 政府法规要求安装机上盒、机上盒供应商推出基于可用作业系统的设备以及新兴国家的模拟切换迁移,这些都推动了市场对机上盒的需求。例如,印度政府透过修改《有线电视网络(监管)法》规定强制安装机上盒。由于采用了数位讯号,机上盒可以提供更好的观看体验,并有助于防止非法频道在印度播放。

- 此外,去年第四季度,印度资讯和广播部(MIB)设立了一个由四人组成的委员会,负责审查印度电视评级机构的指导方针,并建议将回传路径数据(RPD)规定为分销平台运营商(DPO)今后部署的所有机上盒(STB)的强制性功能,使 RPD 成为与加密、有条件接收和其他重要的普遍条件。

- 此外,各种技术创新的兴起也带动了具有各种创新功能的机上盒的发展。受此影响,机上盒企业之间的竞争日益激烈。此外,数位录影是最理想的功能之一,观众可以观看和录製自己喜欢的节目。

- 此外,市场正在见证数位娱乐服务和IPTV的融合。例如今年第二季度,亚洲首家4K RDK IPTV盒子供应商创维数位宣布,印度多系统营运商Bhimavaram Community Network(BCN)已选择创维数位作为BCN数位娱乐服务提供来源。

- 此外,根据 Conviva 的数据,截至 2021 年第一季,Roku 是最受欢迎的 OTT 电视设备,占北美电视观看时间的 37%。此外,随着 4K 等技术的出现,观看体验的改善,加上基础设施和设备的改进,催生了捆绑的音讯视讯和资料服务。此外,根据电视测量机构 BARC India(印度广播观众研究委员会)的报告,疫情期间电视收视率持续飙升。预计这些趋势将进一步推动所研究市场的成长。

- COVID-19 疫情导致政府采取封锁措施,以遏制病毒传播。各国的封锁措施影响了各通讯服务供应商的供应链。去年第三季度,Airtel 的 DTH 部门宣布计划在去年年底前停止进口高清机上盒,并生产本地开发的机上盒,以应对新冠疫情造成的供应链中断。然而,COVID-19 疫情也导致了Over-The-Top(OTT) 服务的兴起。 Hulu、Prime Video 和 Netflix 等 OTT 平台都报告用户数量增加。向 OTT 服务的转变促使服务供应商提供可提供直播和Over-the-Top内容的混合机上盒。

电视和机上盒市场趋势

卫星技术预计将实现显着的市场成长

- 卫星电视是机上盒市场最重要的应用之一。卫星电视的创新之一是引入了节目录製功能,这使得消费者可以即时录製节目并在稍后观看。

- 卫星机上盒也开始包含各种互动功能,包括随选视讯和电子节目指南。除了基本功能外,更先进的机上盒设备还提供一系列互动式多媒体服务,如网路浏览、电子邮件和即时通讯软体,这些服务直接透过使用者的电视系统提供。

- 世界各国政府一直在寻求扩大其太空计划,以增加其国内外直接到户(DTH)服务的覆盖范围。今年第二季度,印度太空研究组织宣布发射通讯GSAT-24。该卫星由新太空印度有限公司(NSIL)发射,这是第一个由需求主导的通讯任务。 GSAT-24 所搭载卫星的全部容量将租赁给塔塔集团的 DTH 业务 Tata Play,以满足其应用需求。

- 此外,卫星/DTH 机上盒市场的供应商正在推出有吸引力的优惠来吸引该市场的客户群。例如,在 2021 年最后一个季度,Dish TV 向印度八个邦(马哈拉斯特拉邦、北方邦、西孟加拉邦、东北部、阿萨姆邦、奥里萨邦、旁遮普邦、奥里萨邦、哈里亚纳邦、古吉拉突邦、喜马偕尔邦、恰蒂斯加尔邦和查谟和克什米尔邦)的用户提供了免费的 MPEG4 盒子。您的升级将包括机上盒、遥控器、HDMI 电缆、A/V 电缆和转接器。用户还将获得新机上盒的 12 个月保固期。此外,混合DTH机上盒的推出在机上盒市场的卫星领域越来越受欢迎。

- 根据印度电讯监理局(TRAI)统计,去年上半年,塔塔集团旗下营运商Tata Sky占据印度DTH市场最大份额,约占33%。在测量期间,该公司的表现优于 Airtel,其次是 Dish TV 和 Sun Direct。除 Dish TV 的市场占有率有所下降外,其余 DTH 营运商在年内进一步巩固了其市场主导地位。因此,如果这些运营商的市场占有率增加,则市场可能会在整个预测期内扩大。

亚太地区占主要市场占有率

- 亚太地区也是技术采用值得关注的地区之一。付费电视市场饱和状态且竞争激烈,促使亚太地区供应商在其 Android TV 产品中添加网关功能、安全性、应用程式、高清功能等。

- 此外,亚洲国家强制安装机上盒的政府法规正在推动亚太地区机上盒市场的成长。据资讯和广播部 (MIB) 称,共有 1,726 家 MSO。此外,还有 12 家 MSO 和 1 家空中头端 (HITS) 营运商,每家都有超过 100 万的用户群。目前,印度有四家优质DTH营运商,为6,957万用户提供电视服务。

- 此外,由于该地区对更高品质电影和强大的技术介面的日益重视,以及该国因资源和劳动力丰富而导致的低生产成本,该地区的市场正在不断扩大。特艺彩色 (Technicolor) 等公司正在印度等亚洲国家扩大生产能力。此外,去年第三季度,Tata Sky推出了首款印度製造的机上盒。该机上盒是与 Technicolor Connected Home 和 Flextronics 合作生产的。

- 此外,该地区已出现从Over-The-Top到 OTT 的明显转变。这种转变的主要原因是为了阻止新冠病毒传播而实施的封锁。根据影片广告和收益平台 SpotX 去年发布的报告,亚太地区有超过 4 亿人使用 OTT影片串流服务,超过 69% 的影片观众每周至少观看一次串流影片。此外,OTT观看排名前三大的市场包括新加坡(91%)、澳洲(81%)和印尼(76%)。此外,OTT串流媒体在东南亚呈指数级增长。

- 此外,根据 TRAI 发布的资料,由于 Netflix、Amazon Prime Video 和 AltBalaji的用户数量大幅增加,有线电视和 DTH 电视服务供应商在疫情期间将市场拱手让给了串流媒体服务。同样,通讯业者DTH 供应商也在与 OTT参与企业合作,提供完整的娱乐内容。去年第三季度,沃达丰 Idea 曾表示,由于 OTT 平台消费的成长和物联网 (IoT) 的加速发展,通讯业正在经历数位变革时期。该公司已与 Voot Select 和 Sun NXT 等本地 OTT 平台合作。

电视和机上盒产业概况

过去几年,电视产业发生了无数变化,变得更加多元化。 ARRIS International PLC、Intek Digital Inc.、中兴通讯股份有限公司、三星电子和 LG 电子等主要企业正在不断创新,并透过策略併购和联盟寻求市场扩张。

2022 年 3 月,Technicolor Connected Home 与法国着名网路服务供应商之一、拥有超过 2,620 万固定和行动用户的 Bouygues Telecom 合作,开发和部署面向未来的高级 Android 4K 超高清 (UHD) STB,该 STB 整合了一流的 Wi-Fi,为整个法国市场的消费者提供更好的视讯体验。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 相关人员分析

- COVID-19 市场影响评估

- 技术简介

第五章 市场动态

- 市场驱动因素

- 先进技术创新

- 新兴市场采用率不断提高

- 基于作业系统的设备部署

- 市场限制

- 生产成本上升和供应商整合是成长放缓的关键因素

- 市场正走向成熟

第六章 市场区隔:机上盒

- 依技术分类

- 卫星/DTH

- IPTV

- 电缆

- 其他类型(DTT 和 OTT)

- 按决议

- SD

- HD

- 超高清以上

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

7. 市场区隔-电视

- 按决议

- HD/FHD

- 4K

- 8K

- 尺寸(英吋)

- 32 或更少

- 39~43

- 48~50

- 55~60

- 65 岁以上

- 依技术分类

- LCD

- 有机发光二极体

- QLED

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

8.供应商市场占有率分析

- 供应商市场占有率机上盒市场

- 供应商市场占有率电视市场

第九章 竞争格局

- 公司简介

- ARRIS International PLC(CommScope Inc.)

- Technicolor SA

- Intek Digital Inc.

- HUMAX Electronics Co. Ltd

- ZTE Corporation

- Skyworth Digital Ltd

- Sagemcom SAS

- Gospell Digital Technology Co. Limited

- Kaon Media Co. Limited

- Shenzhen Coship Electronics Co. Ltd

- Evolution Digital LLC.

- Shenzhen SDMC Technology Co. Ltd

- Samsung Electronics Co. Ltd

- LG Electronics

- TCL

- Hisense

- Xiaomi

第十章 投资分析

第 11 章:投资分析市场的未来

The Television And Set Top Box Market size in terms of shipment volume is expected to grow from 307.10 Million units in 2025 to 402.13 Million units by 2030, at a CAGR of 5.54% during the forecast period (2025-2030).

Key Highlights

- The surge in the adoption of artificial intelligence (AI) in set-top boxes, the rising internet penetration and broadband adoption in emerging markets, continuous deployment of OS-based devices is playing a very significant role in driving the market.

- The government regulations mandating the installation of set-top boxes, deployment of available OS-based devices by STB vendors, and analog switch-off transition in emerging countries are driving the demand for the STB market. For instance, the Government of India has made STBs compulsory through an amendment to the Cable Television Networks (Regulation) Act. STBs provide a better viewing experience because of digital signals and help prevent illegal channels from being broadcasted in India.

- Moreover, in the last quarter of the previous year, the four-member committee formed by the Ministry of Information and Broadcasting (MIB) to review guidelines for TV rating agencies in India recommended that the provision for Return Path Data (RPD) be made a mandatory capability in all future set-top boxes (STBs) deployed by Distribution Platform Operators (DPOs) so that the RPD becomes a ubiquitous capability on par with encryption, conditional access, and other such mandatory STB-level capabilities.

- Also, the rise in various technological innovations led to development a wide range of STBs with various innovative features. This, in turn, has made the competition fierce among the set-top box companies. Moreover, digital video recording is one of the most desired features, enabling viewers to watch and record their favorite shows.

- Additionally, the market is witnessing the integration of digital entertainment services and IPTV. For instance, in the second quarter of this year, Asia's first 4K RDK IPTV box provider Skyworth Digital announced that Bhimavaram Community Network (BCN), India's multi-system operator, had selected Skyworth Digital as the source of BCN's digital entertainment offerings.

- Also, according to Conviva, the most popular OTT TV device as of Q1 2021 was Roku, with a 37% share of TV viewing time in North America. Moreover, enhanced viewer experience, owing to the advent of technologies such as 4K, coupled with better infrastructure and devices, has led to the emergence of bundled voice video and data services. Further, TV viewership continued to surge during the pandemic, as reported by the television viewership measurement agency Broadcast Audience Research Council of India (BARC India). Such trends are further expected to act as catalysts for the growth of the studied market.

- The COVID-19 pandemic led to lockdowns imposed by the government to curb the spread of the virus. The lockdown across countries has affected the supply chains of various telecom service providers. In the 3rd quarter of the last year, Airtel DTH arm announced plans to stop imports of high-definition set-top boxes by the end of last year to tackle the COVID-19-induced supply chain disruption and make locally developed set-top boxes. However, the COVID-19 pandemic also led to an increase in over-the-top (OTT) services. OTT platforms, such as Hulu, Prime Video, Netflix, and more, have all announced their increase in subscriber rates. The shift toward OTT services has led service providers to offer hybrid set-top boxes that provide live streaming and over-the-top content.

TV Set Top Box Market Trends

Satellite Technology is Expected to Witness Significant Market Growth

- Satellite television is one of the most significant applications of the set-top box market. One of the innovations in satellite TV is introducing a show-recording facility, which enables consumers to record their shows in real-time and watch them later at their convenience.

- Also, the satellite STB units are increasingly equipped with various interactive features, like video-on-demand, electronic program guides, etc. More advanced STB units also provide a suite of interactive and multimedia services directly through a user television system, such as internet browsing, email, and instant messaging, in addition to basic functionality.

- The governments have been looking to expand their space programs to increase the range of respective direct-to-home (DTH) offerings within and outside their borders. In the 2nd quarter of this year, ISRO announced the launch of the communication satellite GSAT-24. The satellite was launched by NewSpace India Limited (NSIL) in its first demand-driven communication satellite mission. The total satellite capacity on board GSAT-24 will be leased to its committed customer Tata Play, the DTH business of Tata Group, to meet their application requirements.

- Moreover, satellite/DTH set-top box market vendors are coming up with attractive offers to lure the customer base in this market. For instance, in the last quarter of 2021, Dish TV offered a free MPEG4 box upgrade offer for users in Maharashtra, Uttar Pradesh, West Bengal, North East, and Assam, and eight more states, including Orissa, Punjab, Rajasthan, Haryana, Gujarat, Himachal Pradesh, Chhattisgarh and Jammu & Kashmir in India. The set-top box, remote, HDMI, or A/V cable and adapter would be provided upon upgrading. Subscribers will also get 12 monthly warranty on the new STB. Furthermore, the launch of Hybrid DTH set-top boxes is gaining popularity in the satellite segment of the STB market.

- As per Telecom Regulatory Authority of India (TRAI), in India's DTH market during the first half of the last year, Tata Sky, a business under the Tata Group, had the most significant share with around 33% of the market. During the measured time, the operator was ahead of Airtel, followed by Dish TV and Sun Direct. The remaining DTH operators further solidified their control of the market that year, except for Dish TV, which suffered a fall in its market shares. Hence, the rise in such market shares of these operators will amplify the market throughout the forecasted period.

Asia Pacific to Hold Major Market Share

- The Asia-Pacific region is also one of the prominent regions in terms of technology adoption. Due to the market saturation of Pay-TV consumers and stiff competition, vendors in the Asia Pacific region are constantly trying to add features to their Smart android-based televisions, such as gateway abilities, security, applications, and HD functionality.

- Moreover, the supportive government regulations mandating the installation of set-top boxes in Asian countries are driving the growth of the Asia Pacific set-top box market. According to the Ministry of Information and Broadcasting (MIB), there are 1726 MSOs. Further, there is 12 MSOs and one Headend-in-the-Sky (HITS) operator with a subscriber base greater than one million each. There are currently 4 Pay DTH operators in India, providing television services to 69.57 million users.

- Additionally, the region's market is expanding due to the growing emphasis on higher-quality movies and potent technological interfaces and the nation's low production costs brought on by the availability of plentiful resources and labor. Companies such as Technicolor, and others, have been expanding their manufacturing capabilities in Asian countries such as India. Moreover, in the 3rd quarter of the last year, Tata sky also unveiled its first batch of India-made set-top boxes. The set-top boxes were manufactured in partnership with Technicolor Connected Home and Flextronics.

- Additionally, the region has clearly seen the transition from cable to over-the-top (OTT). The main cause of the transition was the lockdowns implemented to stop the COVID-19 pandemic from spreading. According to last year's report by SpotX, a video advertising and monetization platform, more than 400 million people use OTT video streaming services across the Asia Pacific region, with over 69% of video viewers watching a streaming video at least once a week. Furthermore, the top three markets for OTT viewing included Singapore (91%), Australia (81%), and Indonesia (76%). Also, OTT streaming has increased drastically in Southeast Asia.

- Also, according to the data released by the TRAI, cable and DTH television service providers ceded ground to streaming services during the pandemic, as Netflix, Amazon Prime Video, and AltBalaji reached a significant number of subscribers. On similar lines, telecom DTH providers are also partnering with OTT players to offer complete entertainment content. In the third quarter of the last year, Vodafone Idea announced that the telecom industry is undergoing a digital transformation due to the growing consumption of OTT platforms and the Internet of Things (IoT) acceleration. The company partnered with local OTT platforms such as Voot Select and Sun NXT.

TV Set Top Box Industry Overview

The television industry has witnessed myriad changes over the past several years and has become more diverse. The major players, such as ARRIS International PLC, Intek Digital Inc., ZTE Corporation, Samsung Electronics Co. Ltd., and LG Electronics, continuously innovate and seek market expansion through strategic mergers, acquisitions, and partnerships.

In March 2022, Technicolor Connected Home partnered with Bouygues Telecom, one of France's prominent network service providers with over 26.2 million fixed and mobile subscribers, to develop and deploy a futureproof and premium Android 4K ultra high-definition (UHD) STB integrated with best-in-class Wi-Fi that delivers video experiences to consumers throughout the French market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Stakeholder Analysis

- 4.4 An Assessment of Impact of COVID-19 on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Levels of Technological Innovations

- 5.1.2 Growing Adoption in the Emerging Markets

- 5.1.3 Deployment of OS-based Devices

- 5.2 Market Restraints

- 5.2.1 Growing Production Costs and Vendor Consolidation Cited as the Key Reasons for Slow Growth Forecast

- 5.2.2 Given that the Market is on the Verge of Reaching Maturity

6 MARKET SEGMENTATION - SET-TOP BOX

- 6.1 By Technology

- 6.1.1 Satellite/DTH

- 6.1.2 IPTV

- 6.1.3 Cable

- 6.1.4 Other Types (DTT and OTT)

- 6.2 By Resolution

- 6.2.1 SD

- 6.2.2 HD

- 6.2.3 Ultra-HD and Higher

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 MARKET SEGMENTATION - TELEVISION

- 7.1 By Resolution

- 7.1.1 HD/FHD

- 7.1.2 4K

- 7.1.3 8K

- 7.2 By Size (in inches)

- 7.2.1 32 and below

- 7.2.2 39-43

- 7.2.3 48-50

- 7.2.4 55-60

- 7.2.5 65 and above

- 7.3 By Technology

- 7.3.1 LCD

- 7.3.2 OLED

- 7.3.3 QLED

- 7.4 By Geography

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia

- 7.4.4 Australia and New Zealand

- 7.4.5 Latin America

- 7.4.6 Middle East and Africa

8 VENDOR MARKET SHARE ANALYSIS

- 8.1 Vendor Market Share Set-top box Market

- 8.2 Vendor Market Share Television Market

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 ARRIS International PLC (CommScope Inc.)

- 9.1.2 Technicolor SA

- 9.1.3 Intek Digital Inc.

- 9.1.4 HUMAX Electronics Co. Ltd

- 9.1.5 ZTE Corporation

- 9.1.6 Skyworth Digital Ltd

- 9.1.7 Sagemcom SAS

- 9.1.8 Gospell Digital Technology Co. Limited

- 9.1.9 Kaon Media Co. Limited

- 9.1.10 Shenzhen Coship Electronics Co. Ltd

- 9.1.11 Evolution Digital LLC.

- 9.1.12 Shenzhen SDMC Technology Co. Ltd

- 9.1.13 Samsung Electronics Co. Ltd

- 9.1.14 LG Electronics

- 9.1.15 TCL

- 9.1.16 Hisense

- 9.1.17 Xiaomi

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET

机上盒市场-全球产业规模、份额、趋势、机会和预测,依产品类型、内容品质、服务、最终用户、地区和竞争格局划分,2020-2030年预测

机上盒市场-全球产业规模、份额、趋势、机会和预测,依产品类型、内容品质、服务、最终用户、地区和竞争格局划分,2020-2030年预测 4K 机上盒市场(按应用类型、分销管道、最终用户和连接性)- 全球预测,2025 年至 2032 年机上盒市场按分销管道、技术、应用、连接方式、平台和销售管道划分-2025-2032年全球预测

4K 机上盒市场(按应用类型、分销管道、最终用户和连接性)- 全球预测,2025 年至 2032 年机上盒市场按分销管道、技术、应用、连接方式、平台和销售管道划分-2025-2032年全球预测 机上盒市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

机上盒市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2025年全球4K机上盒市场报告2025年全球Android机上盒(STB)和电视市场报告2025年全球机上盒市场报告

2025年全球4K机上盒市场报告2025年全球Android机上盒(STB)和电视市场报告2025年全球机上盒市场报告 2032 年 4K 机上盒市场预测:按产品类型、解析度/功能、分销管道、最终用户和地区进行的全球分析

2032 年 4K 机上盒市场预测:按产品类型、解析度/功能、分销管道、最终用户和地区进行的全球分析 机上盒市场规模及预测 2021-2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:依产品类型、内容品质(标准画质、高画质和 4K)及地理

机上盒市场规模及预测 2021-2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:依产品类型、内容品质(标准画质、高画质和 4K)及地理 机上盒(STB)的全球市场

机上盒(STB)的全球市场