|

市场调查报告书

商品编码

1683199

自动驾驶卡车:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Autonomous Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

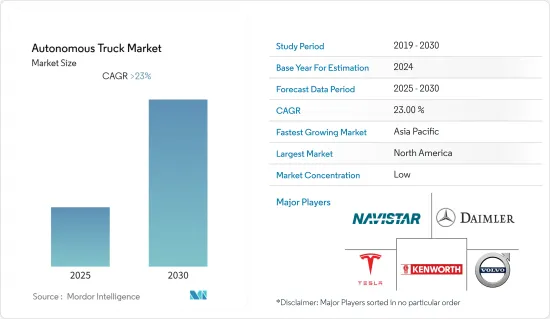

预测期内,自动驾驶卡车市场预计将以超过 23% 的复合年增长率成长。

与整个产业相比,COVID-19 疫情对汽车产业这一领域的影响相对较小。疫情封锁和全球交通停顿在一定程度上阻碍了自动驾驶卡车的需求。不过,随着市场和贸易的逐步开放,以及对自动化的需求不断增加,自动驾驶卡车市场有望实现经济復苏。

主要亮点

- 推动市场成长的关键因素包括新兴市场工业部门的扩张、物流行业的需求增加以及建筑业的需求增加(由于建设活动增加)。由于新兴经济体和已开发经济体的经济成长,预计未来几年市场将会成长。

- 自动驾驶卡车在便利性方面具有取代传统卡车的巨大潜力,但生产成本、缺乏适当的基础设施、政府法规和政策不足以及通勤者和行人的安全问题阻碍因素了它们的发展。已报告 36 起涉及自动驾驶汽车的事故。

- 对车辆安全的需求不断增长以及严格的政府法规正在推动 ADAS 市场的成长。美国公路交通安全管理局 (NHTSA) 要求到 2022 年 9 月 1 日,所有重量在 8,501 至 10,000 磅之间的卡车都必须配备自动紧急煞车系统。英国还建立了网联和自动驾驶汽车中心(CAV),并致力于制定允许在高速公路和道路上进行车辆测试的法律法规。

自动驾驶卡车市场趋势

ADAS 需求不断上升

消费者意识的不断增强推动了对具有自动驾驶功能和先进安全功能的车辆的需求。 90% 为车辆选择 ADAS 系统的客户会成为回头客。政府的规范和政策也在推动 ADAS 市场的销售。美国和欧洲当局计划在 2022 年强制实施汽车紧急煞车 (AEB),并在 2020 年正面防撞/警告系统。

只有昂贵的豪华车才配备完整的 ADAS 系统。许多卡车OEM正在与 ADAS 製造商合作生产低成本的 ADAS 系统。然而,虽然汽车(商用车和乘用车)的价格以每年 1% 的微不足道的平均速度增长,但 ADAS 系统的製造成本很高。由于OEM不愿意提高中小型汽车领域的价格,ADAS 公司可能无法获得预期的回报。这一因素可能会阻碍 ADAS 市场的成长。

各大OEM供应商均采取与科技公司合作开发ADAS的策略。 Nvidia 等科技公司已进入该领域,为Volvo和 Paccar 等公司提供服务。亚马逊使用 Embark 自动驾驶卡车运送货物。

过去几十年来,被动安全领域经历了许多创新,但新兴市场仍然没有太多改进空间。开发商目前专注于在新兴市场提供最佳的被动安全性。主动式安全(预测和避免碰撞)尚处于起步阶段,还有很多需要改进的地方。 ADAS技术已获得多数参与者的早期核准,很可能在未来全自动驾驶汽车的发展中发挥关键作用。

北美引领自动驾驶卡车市场

虽然自动驾驶卡车在欧洲和亚太等地区处于应用的早期阶段,但由于基础设施的完善和大量科技公司进入自动驾驶领域,北美目前是最大的市场。

新兴市场的汽车电气化,以及特斯拉等公司开拓基础建设,也推动了北美市场的发展。电动车中线控技术的引进有助于改善自动驾驶。

2021 年 9 月,PACCAR 与主要企业的自动驾驶技术公司 Aurora 合作,开始在华盛顿对用于运输业务的自动驾驶卡车进行商业测试。该技术预计将被联邦快递采用。

2019 年,戴姆勒北美卡车公司与 Torc Robotics 合作,开始在维吉尼亚81 号州际公路上测试自动驾驶卡车。在 2020 年国际消费电子展 (CES) 上,肯沃斯卡车发布了基于其 T680 卡车的自动驾驶卡车技术。自动驾驶卡车将在行驶过程中使用感测器和光达每小时收集多达Terabyte的资料。

自动驾驶卡车行业概况

自动驾驶卡车市场主要由以下参与者主导:戴姆勒、沃尔沃、特斯拉等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 市场限制

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按类型

- 小型货车

- 中型卡车

- 大型卡车

- 按自动化程度

- 半自动驾驶

- 完全自主

- 透过ADAS功能

- 主动式车距维持定速系统

- 车道偏离警示

- 智慧停车辅助

- 高速公路导航

- 自动紧急制动

- 盲点侦测

- 交通壅塞辅助

- 车道维持辅助系统

- 依组件类型

- 骑士

- 雷达

- 相机

- 感应器

- 按驱动类型

- 内燃机

- 电动式的

- 杂交种

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东和非洲

- 北美洲

第六章 竞争格局

- 供应商市场占有率

- 公司简介

- AB Volvo

- Mercedes Benz Group

- Traton SE

- TuSimple

- Fabu Technology

- Tesla Inc.

- Paccar Inc

- BYD Co. Ltd.

- Einride

- Embark

第七章 市场机会与未来趋势

The Autonomous Truck Market is expected to register a CAGR of greater than 23% during the forecast period.

The COVID-19 pandemic had a relatively more minor impact on this automotive industry segment compared to the whole. The demand for autonomous trucks was slightly hindered due to the lockdown and global transportation halt due to the pandemic. However, with market and trade gradually opening up and the increased need for automation, the autonomous truck market is hoping for an economic revival.

Key Highlights

- Some major factors driving the growth of the market are the expansion of industrial sectors in the emerging market, growing demand from the logistics industry, and rising demand from the construction sector (owing to growing construction activities). The market is expected to witness growth in the coming years due to growing economies across developing and developed counties.

- Although autonomous/driverless trucks have a great potential to replace conventional trucks in terms of convenience-high, cost of manufacturing, lack of proper infrastructures, inadequate regulations and policies of governments, and safety of commuters and pedestrians are some of the reasons are acting as a hindrance in the growth. There have been 36 reported accidents involving autonomous vehicles.

- The rising demand for vehicle safety and stringent government rules drive the ADAS market growth. National Highway Traffic Safety Administration (NHTSA) makes it mandatory for all trucks with weights ht range from 8501 lb. to 10000 lb. to be equipped with Automatic Emergency Braking by September 1, 2022. United Kingdom has also set up a Centre for Connected and Autonomous Vehicles (CAV) that is working towards establishing laws and regulations to allow vehicle testing on highways and roads.

Autonomous Truck Market Trends

ADAS demand is on the rise

Rising awareness among customers is leading to growth in demand for vehicles with autonomous and advanced safety features. 90% of the customers who opt for any ADAS system in their vehicle become repeat purchasers. Government norms and policies are also boosting the sales of the ADAS market. US and European authorities will make the installation of Automotive Emergency Braking (AEB) mandatory by 2022 and the Forward Collision Avoidance/Warning System by 2020.

The complete ADAS systems are featured in expensive luxury segment vehicles only. Many truck OEMs collaborate with ADAS manufacturing companies to produce low-cost ADAS systems. However, vehicles (commercial and passenger) register a minute average annual growth of 1% in their prices, while ADAS systems are expensive due to their high manufacturing cost. OEMs may show reluctance in increasing the prices of small and mid-sized vehicle segments, and ADAS companies might not get the expected return. This factor might hinder the growth of the ADAS market.

Top OEM suppliers have adopted the strategy of partnering with technology companies to develop ADAS. Tech companies like Nvidia have entered this space to provide services to companies such as Volvo and Paccar. Amazon is using Embark's self-driving trucks to deliver its cargo.

Passive safety (safety measures to prevent drivers from injuries during or after the crash) has seen a lot of innovations in the past decades, andminimale scope for improvement is left to make in the markets of developed geographies. Companies are now focusing on providing the best passive safety in developing markets. Active Safety (to predict and avoid crashes) is in its initial stage and has a lot to offer. Any ADAS technology that gets early approval from a majority of players will play a crucial role in the development of fully autonomous vehicles in the future.

North America is leading the autonomous truck market

Although Autonomous trucks are in the early stage of adoption across the globe in geographies such as Europe and the Asia Pacific, North America is currently the largest market due to the availability of infrastructure and significant technology companies that are entering autonomous driving segment.

The rising electrification of vehicles due to infrastructure development by companies such as Tesla is also propelling the market in North America. The induction of x-by-wire technology in electric vehicles is helping in the improvement of autonomous driving.

In Sep 2021, PACCAR teamed up with Aurora, a leading autonomous driving technology company, to launch a commercial pilot of autonomous trucks in hauling operations in Washington. The technology is expected to be used by FedEx.

In 2019, Daimler Trucks North America partnered with Torc Robotics and started testing autonomous trucks at Interstate 81 in Virginia. At CES 2020, Kenworth Truck Co. unveiled its autonomous truck technology based on the T680 truck. The autonomous truck uses sensors and LiDAR and collects up to 1 terabyte of data per hour during driving.

Autonomous Truck Industry Overview

The autonomous truck market is firmly consolidated by players such as Daimler, Volvo, Tesla, etc. The primary strategy players adopt collaborating with technology companies to integrate services such as artificial intelligence (AI), robotics, advanced analytics, Internet of Things, Cloud technology, etc., in the production and operation of autonomous trucks.

- In Sep 2021, Volvo Autonomous Solutions revealed a prototype long-haul autonomous truck for the North America application.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Light-duty Trucks

- 5.1.2 Medium-duty Trucks

- 5.1.3 Heavy-duty Trucks

- 5.2 Level of Autonomy

- 5.2.1 Semi-Autonomonus

- 5.2.2 Fully Autonomoys

- 5.3 ADAS Features

- 5.3.1 Adaptive Cruise Control

- 5.3.2 Lane Departure Warning

- 5.3.3 Intelligent Park Assist

- 5.3.4 Highway Pilot

- 5.3.5 Automatic Emergency Braking

- 5.3.6 Blind Spot Detection

- 5.3.7 Traffic Jam Assist

- 5.3.8 Lane Keeping Assist System

- 5.4 Component Types

- 5.4.1 LIDAR

- 5.4.2 RADAR

- 5.4.3 Camera

- 5.4.4 Sensors

- 5.5 Drive Type

- 5.5.1 IC Engine

- 5.5.2 Electric

- 5.5.3 Hybrid

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.4.1 South America

- 5.6.4.2 Middle-East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 AB Volvo

- 6.2.2 Mercedes Benz Group

- 6.2.3 Traton SE

- 6.2.4 TuSimple

- 6.2.5 Fabu Technology

- 6.2.6 Tesla Inc.

- 6.2.7 Paccar Inc

- 6.2.8 BYD Co. Ltd.

- 6.2.9 Einride

- 6.2.10 Embark

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2032 年自动驾驶卡车市场预测:按卡车类型、自动化程度、零件、推进系统、应用、最终用户和地区进行的全球分析

2032 年自动驾驶卡车市场预测:按卡车类型、自动化程度、零件、推进系统、应用、最终用户和地区进行的全球分析 自动驾驶卡车市场规模、份额和趋势分析报告:按推进系统、车辆类型、感测器类型、应用、ADAS 功能、自主等级、地区和细分市场预测,2025 年至 2033 年B2B 互联车队服务的全球市场

自动驾驶卡车市场规模、份额和趋势分析报告:按推进系统、车辆类型、感测器类型、应用、ADAS 功能、自主等级、地区和细分市场预测,2025 年至 2033 年B2B 互联车队服务的全球市场 全球自动驾驶卡车市场按自动驾驶等级、推进类型、最终用途产业、卡车类型、地区和预测划分2030 年自动驾驶卡车市场预测:按卡车类型、推进类型、组件、自动化程度、应用和地区进行的全球分析

全球自动驾驶卡车市场按自动驾驶等级、推进类型、最终用途产业、卡车类型、地区和预测划分2030 年自动驾驶卡车市场预测:按卡车类型、推进类型、组件、自动化程度、应用和地区进行的全球分析 自动驾驶卡车的全球市场:市场规模·占有率·趋势,产业分析 (各自动驾驶等级·感测器类别·各最终用途·各地区),未来预测 (2025年~2034年)自动驾驶卡车市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

自动驾驶卡车的全球市场:市场规模·占有率·趋势,产业分析 (各自动驾驶等级·感测器类别·各最终用途·各地区),未来预测 (2025年~2034年)自动驾驶卡车市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 自动卡车市场规模、份额和成长分析:按 ADAS 功能、自动化程度、推进类型、感测器类型、卡车类别、应用和地区 - 2025-2032 年行业预测

自动卡车市场规模、份额和成长分析:按 ADAS 功能、自动化程度、推进类型、感测器类型、卡车类别、应用和地区 - 2025-2032 年行业预测 自动驾驶卡车市场评估:自动驾驶层级·推动因素·各地区的机会及预测 (2018-2032年)

自动驾驶卡车市场评估:自动驾驶层级·推动因素·各地区的机会及预测 (2018-2032年) 全球自动驾驶卡车市场,2024-2028

全球自动驾驶卡车市场,2024-2028