|

市场调查报告书

商品编码

1683983

中国杀菌剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)China Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

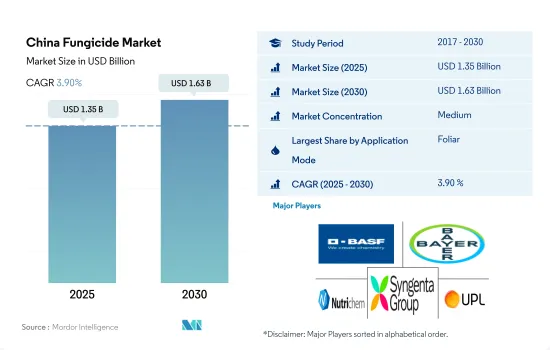

预计 2025 年中国杀菌剂市场规模将达到 13.5 亿美元,预计到 2030 年将达到 16.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.90%。

叶面喷布因其快速起效的特性而占据中国杀菌剂市场的主导地位

- 中国拥有成熟的杀菌剂製造业,国内有多家公司生产杀菌剂製剂及活性成分。我国使用的杀菌剂主要有三唑类、甲氧基丙烯酸酯类、苯并咪唑酮、二硫代氨基甲酸、醌类外抑制剂(QoIs)等。这些杀菌剂具有不同的作用方式并针对特定的真菌病原体。 2022年中国将占亚太杀菌剂市场的31.5%。

- 叶面喷布占据中国杀菌剂市场的主导地位,2022 年的份额为 60.1%。叶面喷布杀菌剂可以快速对抗真菌病原体。杀菌剂通常被配製成能够在植物内快速吸收和转移。这使得杀菌剂能够到达受影响的组织并抑製或杀死真菌,从而减缓疾病的进展并防止进一步的损害。

- 2022 年,种子处理占中国杀菌剂市场的 14.1%。真菌感染会削弱植物并阻碍其发育。杀菌剂种子处理有助于预防或减少疾病的侵袭,维持植物的健康和活力。这使得植物能够将更多的能量用于生长发育,产生更健康、更高产的作物。 2017 年至 2022 年,种子处理市场价值将增加 9,190 万美元。

- 预计到 2026 年,中国杀菌剂出口量也将增加。 2021 年,中国出口了 1.102 亿公斤杀菌剂。预计2026年出口量将达1.256亿公斤。这一因素可能会进一步推动杀菌剂市场的发展,预计预测期内复合年增长率将达到 3.7%。

中国杀菌剂市场趋势

最大残留量规定的製定和疾病控制其他替代方法的采用已导致每公顷杀菌剂消费量大幅减少。

- 过去一段时间,中国每公顷杀菌剂消费量下降了约16%。中国政府已经推出了管理杀菌剂使用的法规和政策。这包括对农产品中杀菌剂的最大残留量设定限制,并制定安全和负责任使用杀菌剂的指南。透过实施这些法规,中国旨在确保杀菌剂合理使用并采取适当的预防措施。

- 中国积极鼓励实施综合虫害管理(IPM)策略,包括预防措施、生物防治技术和杀菌剂等农药的适当使用。这种综合方法已成功降低杀菌剂的使用率。

- 中国政府也探索了疾病控制的替代方案,例如透过传统育种和基因工程技术开发抗病作物品种。透过注重提高作物对疾病的天然抵抗力,中国减少了对杀菌剂的依赖。

- 中国一直在使用生物防治剂来取代杀菌剂。这些生物防治剂包括有益微生物,如细菌和真菌,它们可以抑製或阻止植物病原体的生长。将这些生物防治剂应用于作物可以减少杀菌剂的使用。

- 农民采用轮作和土壤管理等技术来有效地预防和控制疾病。这些技术减少了中国每公顷杀菌剂的消费量。

Mancozeb、丙森锌、福美锌是我国最常使用的杀菌剂成分。

- Mancozeb、丙森锌、福美锌是我国最常使用的杀菌剂成分。 2021年,中国杀菌剂出口量达1,1,025万公斤,位居德国、法国、中国之后,位居第四。自1997年以来,出口与前一年同期比较%。预计到2026年将达到1.2564亿公斤。

- 代森锰锌是一种频谱接触性杀菌剂,用于控製油菜、生菜、小麦、苹果、番茄、鲜食葡萄、酿酒葡萄、洋葱、胡萝卜、欧洲防风草、青葱和硬粒小麦中的多种真菌疾病,包括炭疽病、腐霉菌、叶斑病、白粉病、灰霉病、銹病和多种真菌疾病。 2022 年的价格为每吨 7,700 美元。

- 丙森锌是一种Dithiocarbamate接触性杀菌剂,2022 年的价格为每吨 3,500 美元。丙森锌适用于番茄、大白菜、黄瓜、芒果和花卉等作物。用于防治芒果早疫病、晚疫病,白菜炭疽病,马铃薯霜霉病,黄瓜霜霉病,番茄晚疫病。

- 福美锌是一种氨基甲酸酯类农业杀菌剂。它可以施叶面喷布,也可以用作土壤或种子处理。可用于仁果、核果、坚果、攀缘植物、蔬菜和观赏植物,特别适用于防治苹果、梨的黑星病,以及其他作物上的黑星病、斑枯病、桃叶病、穿孔病、銹病、黑腐病和炭疽病。 2022 年 Ziram 的价格为每吨 3,300 美元。

- 活性成分价格受到当地天气、疾病爆发、能源价格和人事费用等因素的显着影响。

中国杀菌剂产业概况

中国杀菌剂市场格局适度整合,前五大企业市占率合计为63.77%。市场的主要企业有:BASF公司、拜耳公司、颖泰化工、先正达集团和联合磷化有限公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 活性成分价格分析

- 法律规范

- 中国

- 价值炼和通路分析

第五章 市场区隔

- 执行模式

- 化学喷涂

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

第六章 竞争格局

- 重大策略倡议

- 市场占有率分析

- 商业状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nutrichem Co. Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001685

The China Fungicide Market size is estimated at 1.35 billion USD in 2025, and is expected to reach 1.63 billion USD by 2030, growing at a CAGR of 3.90% during the forecast period (2025-2030).

Foliar application dominated the Chinese fungicide market owing to its quick action

- China has a well-established fungicide manufacturing industry, with several domestic companies producing fungicide formulations and active ingredients. Major fungicide classes used in China include triazoles, strobilurins, benzimidazoles, dithiocarbamates, and quinone outside inhibitors (QoIs). These fungicides have different modes of action and target specific fungal pathogens. China accounted for 31.5% of the Asia-Pacific fungicide market in 2022.

- Foliar application dominated the Chinese fungicide market and accounted for a share of 60.1% in 2022. Fungicides applied in foliar can provide rapid action against fungal pathogens. They are typically formulated to have quick absorption and translocation properties within the plant. This allows the fungicide to reach the affected tissues and inhibit or kill the fungi, reducing disease progression and preventing further damage.

- Seed treatment accounted for 14.1% of the Chinese fungicide market in 2022. Fungal infections can weaken and stunt the development of plants. Fungicide seed treatments can help plants maintain their health and vigor by preventing or lowering disease damage. This allows the plants to allocate more energy toward growth and development, leading to healthier and more productive crops. The market value of seed treatment between 2017 and 2022 increased by USD 91.9 million.

- Exports of fungicides from China are also projected to increase by 2026. In 2021, the country exported 110.2 million kg of fungicides. By 2026, exports are projected to reach 125.6 million kg. This factor may further drive the fungicide market, which is anticipated to register a CAGR of 3.7% during the forecast period.

China Fungicide Market Trends

Setting regulations for controlling maximum residue levels and adopting other alternatives for disease control significantly reduced per-hectare fungicide consumption

- During the historical period, China witnessed a notable decrease of approximately 16% in the consumption of fungicides per hectare, attributed to several reasons. The Chinese government has implemented regulations and policies to control the use of fungicides. These include setting limits on the maximum residue levels of fungicides in agricultural products and establishing guidelines for their safe and responsible use. By enforcing these regulations, China aims to ensure that fungicides are used judiciously and with proper precautions.

- China has actively encouraged the implementation of integrated pest management (IPM) strategies, which encompass preventive measures, biological control techniques, and judicious application of pesticides, such as fungicides. This comprehensive approach has successfully led to a decrease in the rate of fungicide usage.

- The Chinese government has also explored alternative methods of disease control, including the development of disease-resistant crop varieties through traditional breeding or genetic modification techniques. By focusing on enhancing the natural resistance of crops to diseases, China has reduced the reliance on fungicides.

- China has been utilizing biological control agents as an alternative to fungicides. These agents include beneficial microorganisms, such as bacteria and fungi, which can suppress or inhibit the growth of plant pathogens. Applying these biocontrol agents to crops could lead to a reduction in the rate of fungicide usage.

- The farmers adopted techniques, such as crop rotation and soil management, to prevent and manage diseases effectively. These techniques reduced the consumption of fungicide per hectare in China.

Mancozeb, propineb, and ziram are the most commonly used fungicide ingredients in China

- Mancozeb, propineb, and ziram are the most commonly used fungicide ingredients in China. In 2021, the country exported 110,250,000 kg of fungicides and was fourth behind Germany, France, and China. On average, exports have grown by 2.2% Y-o-Y since 1997. Exports are projected to reach 125,640,000 kg by 2026.

- Mancozeb is a broad-spectrum contact fungicide that is used to control a number of fungal diseases, such as anthracnose, pythium blight, leaf spot, downy mildew, botrytis, rust, and scab, in oilseed rape, lettuce, wheat, apples, tomatoes, table grapes, wine grapes, bulb onions, carrots, parsnip, shallots, and durum wheat. It was priced at USD 7.7 thousand per metric ton in 2022.

- Propineb is a dithiocarbamate contact fungicide, priced at USD 3.5 thousand per metric ton in 2022. Propineb is applicable to tomato, Chinese cabbage, cucumber, mango, flowers, and other crops. It is used in preventing and treating early late blight of mango, anthracnose of Chinese cabbage, potato downy mildews, cucumber downy mildew, and tomato late blight.

- Ziram is a carbamate, agricultural fungicide. It can be applied to the foliage of plants, but it is also used for soil and/or seed treatment. It can be used in pome fruit, stone fruit, nuts, vines, vegetables, and ornamentals, particularly to control scabs in apples and pears, as well as Alternaria, Septoria, peach leaf curl, shot-hole, rusts, black rot, and anthracnose in other fruit crops. Ziram was priced at USD 3.3 thousand per metric ton in 2022.

- The active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country.

China Fungicide Industry Overview

The China Fungicide Market is moderately consolidated, with the top five companies occupying 63.77%. The major players in this market are BASF SE, Bayer AG, Nutrichem Co. Ltd, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Nutrichem Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2032年作物杀菌剂市场预测:按产品类型、作物类型、剂型、应用、最终用户和地区进行的全球分析

2032年作物杀菌剂市场预测:按产品类型、作物类型、剂型、应用、最终用户和地区进行的全球分析 甲氧基丙烯酸酯类系杀菌剂市场,规模,占有率,趋势,分析报告:类别,各製剂,各用途,各终端用户,各地区,2025年~2034年的市场预测化学杀菌剂市场:依产品种类、依应用、按杀菌剂类型、依配方、按地区

甲氧基丙烯酸酯类系杀菌剂市场,规模,占有率,趋势,分析报告:类别,各製剂,各用途,各终端用户,各地区,2025年~2034年的市场预测化学杀菌剂市场:依产品种类、依应用、按杀菌剂类型、依配方、按地区 2025年杀菌剂全球市场报告2025年杀菌剂全球市场报告

2025年杀菌剂全球市场报告2025年杀菌剂全球市场报告 种子处理杀菌剂市场报告:趋势、预测与竞争分析(至2031年)

种子处理杀菌剂市场报告:趋势、预测与竞争分析(至2031年) 亚太杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)北美杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)南美杀菌剂:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年)印尼杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)

亚太杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)北美杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)南美杀菌剂:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年)印尼杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)

▼