|

市场调查报告书

商品编码

1683999

南美杀菌剂:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年)South America Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

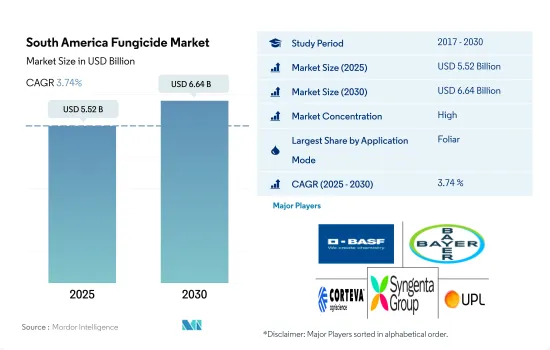

南美杀菌剂市场规模预计在 2025 年达到 55.2 亿美元,预计到 2030 年将达到 66.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.74%。

叶面喷布是施用杀菌剂最重要的主要方法。

- 在南美洲,人们使用多种杀菌剂施用方法来有效控制农业中的真菌病害。选择正确的施用方法可以为农民提供经济有效的解决方案,使他们能够精确覆盖特定区域并最大限度地减少不必要的使用。功效的提高优化了杀菌剂的利用率并降低了农民的投入成本。

- 在农业中各种杀菌剂使用方法中,叶面喷布是主流,占2022年杀菌剂总使用量的59.8%。此方法主要应用于豆类和油籽,占市场占有率最大,为42.1%。叶面喷布的针对性和高效吸收特性有助于控制疾病,从而有可能提高产量并降低农民的成本。

- 2022年,种子治疗方法将占据第二大市场占有率,占总量的14.2%。随着农民越来越意识到使用杀菌剂种子处理产品保护幼苗和提高生产力的好处,其采用率显着增加。因此,预计南美杀菌剂种子处理市场在 2023-2029 年预测期内的复合年增长率将达到 4.0%。

- 在南美洲,杀菌剂主要用于农业,以最大限度地提高作物产量并提高整体盈利。预计应用领域将大幅成长,2023-2029 年预测期内的复合年增长率为 4.0%。

真菌病害对作物的威胁日益严重,巴西占据市场主导地位

- 许多作物生长在南美洲的热带气候中。巴西、阿根廷、巴拉圭是南美洲三大农业生产国。这些国家是大豆、玉米、糖、咖啡、水果和蔬菜的主要出口国。

- 巴西占据市场主导地位,2022 年占 59.4% 的市场占有率。随着巴西农业的扩大和多样化,真菌病害对作物的威胁越来越大。真菌病原体对多种作物不利影响,导致产量下降、品质下降并给农民带来经济损失。

- 2022年智利占南美洲杀菌剂市场的4.8%。智利北部的阿塔卡马沙漠属温带气候,中部肥沃的中央谷地地区属于地中海气候,南部的低矮沿海山区和东部崎岖的安地斯山脉属凉爽湿润气候。这些气候条件有利于该国真菌疾病的传播。剋菌丹和福美双是智利广泛使用的杀菌剂。研究发现,剋菌丹与有机质含量高的天然土壤最容易相互作用,而福美双则更适合与黏土含量高的土壤相互作用。

- 推动杀菌剂市场发展的因素包括可耕地面积减少、人口成长、提高作物产量的需求。各种真菌对现有杀菌剂的抗药性以及植物中新疾病的出现促使主要企业寻找新产品来对抗新的真菌突变并减少农民的损失。预计预测期内对抗作物疾病杀菌剂的需求不断增加将推动市场发展。

南美洲杀菌剂市场趋势

增加种植密度等强化农业实践创造了有利于真菌病原体快速繁殖的环境。

- 真菌感染疾病会削弱植物的整体健康并导致生长不良。受感染的植物可能会高度降低、叶子变小、分枝减少,直接导致产量下降。这种真菌也会破坏植物内的荷尔蒙平衡,影响植物的发育和整体生产力。

- 南美洲南锥体是疾病爆发最重要的地区之一。该地区包括阿根廷、玻利维亚、智利、巴西、巴拉圭和乌拉圭。严重的疾病包括銹病、白粉病和真菌叶枯病(叶枯病、叶斑病)。这些疾病每年都会发生,因为正常条件有利于疾病的发展和传播。

- 智利是南美洲最大的杀菌剂消费国,2022 年的消费量为 4.1 公斤/公顷。这是因为智利某些地区的气候条件较高,湿度大,降雨多,气温波动大,有利于真菌病害的发生。为了预防和控制这些疾病,农民经常使用杀菌剂。

- 巴西南部的气候条件非常适合几种重要的真菌叶面疾病的发展。经过12年的调查,喷洒杀菌剂的小麦平均产量增加了40%。 2022年,巴西杀菌剂消费量排名第二,为0.9公斤/公顷。

- 增加种植密度等农业实践的强化创造了有利于真菌病原体快速繁殖和定居的环境,从而推动了预测期内对杀菌剂的需求。

Mancozeb是南美洲使用最广泛的杀菌剂。

- 代森锰锌是一种二硫代氨基甲酸盐类杀菌剂。它在南美洲被广泛用于控制各种作物的真菌病害。Mancozeb可有效治疗马铃薯、番茄、葡萄和香蕉等作物的多种真菌疾病,包括晚疫病、霜霉病、早疫病和炭疽病。代森锰锌透过抑制真菌的代谢过程来发挥作用,阻止其生长和繁殖。代森锰锌的活性频谱也比其他杀菌剂更广,可作用于真菌细胞内的多个部位,因此更有效。 2022年南美代森锰锌价格为7,800美元。

- 与Mancozeb一样,丙森锌是一种二硫代氨基甲酸盐类杀菌剂。丙森锌在农业中用于控制各种真菌疾病。丙森锌可有效治疗多种作物的霜霉病、晚疫病、叶斑病和晚疫病等真菌疾病。与Mancozeb一样,丙森锌也透过多位点活性发挥作用,减少真菌群体中抗药性的发生。 2022年南美丙森锌的价格为3,540美元。

- 与代森锰锌和丙森锌一样,福美锌属于Dithiocarbamate化学品类,2022 年的价格为每公尺 3,300 美元。福美锌通常用于控制农业中的真菌疾病,已知可以有效控制纹枯病、霜霉病、叶斑病和炭疽病等真菌疾病。福美锌能抑制真菌细胞内的几种关键酶,破坏各种代谢过程,阻碍病原体的生长和繁殖能力。它作用于多个区域,可长期有效控制疾病。

南美洲杀菌剂产业概况

南美洲杀菌剂市场相当集中,前五大公司占据了70.48%的市场。市场的主要参与者有:BASF公司、拜耳公司、科迪华农业科技公司、先正达集团和联合磷化有限公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 活性成分价格分析

- 法律规范

- 阿根廷

- 巴西

- 智利

- 价值炼和通路分析

第五章市场区隔

- 执行模式

- 化学灌溉

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

- 原产地

- 阿根廷

- 巴西

- 智利

- 南美洲其他地区

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ADAMA Agricultural Solutions Ltd.

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Rainbow Agro

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001701

The South America Fungicide Market size is estimated at 5.52 billion USD in 2025, and is expected to reach 6.64 billion USD by 2030, growing at a CAGR of 3.74% during the forecast period (2025-2030).

The foliar application holds the utmost significance as the primary mode of fungicide application

- In South America, numerous methods of fungicide applications are utilized to effectively control fungal diseases in agriculture. By choosing suitable application methods, farmers can attain cost-efficient solutions, ensuring accurate coverage of specific areas and minimizing unnecessary usage. This improved efficacy optimizes fungicide utilization, resulting in decreased input costs for farmers.

- Among various fungicide application methods in agriculture, foliar application is the dominant mode, accounting for 59.8% of the total fungicide usage in 2022. This approach is primarily utilized in pulses and oilseeds, which hold the largest market share at 42.1%. The targeted and efficient absorption properties of foliar application contribute to its effectiveness in controlling diseases, potentially resulting in increased yields and saving costs for farmers.

- In 2022, the seed treatment method held the second-largest market share, comprising 14.2% of the total. The rise in farmers' awareness about the benefits of using fungicide seed treatment products to protect seedlings and boost productivity has resulted in a significant rise in their adoption. As a result, it is projected that the South American fungicide seed treatment market may experience a CAGR of 4.0% during the forecast period from 2023 to 2029.

- In the agricultural sector of South America, fungicides are utilized with the primary aim of maximizing crop yields and improving overall profitability. The mode of the application segment is anticipated to experience substantial growth, with a CAGR of 4.0% during the forecast period from 2023 to 2029.

Brazil dominated the market as the threat of fungal diseases to crops became increasingly significant

- Many crops thrive in the tropical climates of South America. Brazil, Argentina, and Paraguay are the three major agricultural producers in South America. These countries are major exporters of soybeans, maize, sugar, coffee, fruits, and vegetables.

- Brazil dominated the market, accounting for a market share of 59.4% in 2022. As Brazil's agriculture expands and diversifies, the threat of fungal diseases to crops becomes increasingly significant. Fungal pathogens can adversely impact a wide range of crops, leading to yield losses, reduced quality, and economic losses for farmers.

- Chile accounted for 4.8% of the South American fungicide market in 2022. Chile has a temperate climate in the Atacama Desert in the north, a Mediterranean climate in the central and fertile central valley region, and a cool and damp climate in the southern low coastal mountains and rugged Andes in the east. These climatic conditions favor the proliferation of fungal diseases in the country. Captan and thiram are two fungicides widely used in Chile. Captan is found to have the greatest interaction with natural soils with high organic matter content, while thiram showed a preference for soils with high clay content.

- Factors driving the market for fungicides include decreasing arable land, increasing population, and the need to improve crop yields. Resistance of various fungi to the existing fungicides and the emergence of new diseases in plants led the companies to find novel products for fighting the new fungus mutations and reducing the loss to farmers. The increasing demand for fungicides to fight crop diseases is expected to drive the market during the forecast period.

South America Fungicide Market Trends

Intensification of agricultural practices, such as increased planting densities, creates a conducive environment for the rapid proliferation of fungal pathogens

- Fungal infections can weaken the overall health of plants, leading to stunted growth. Infected plants may exhibit reduced height, smaller leaves, and fewer branches, which can directly translate into lower crop yields. Fungi can also disrupt the hormonal balance within plants, affecting their development and overall productivity.

- The Southern Cone of South America is one of the most critical regions for disease epidemics. The region is comprised of Argentina, Bolivia, Chile, Brazil, Paraguay, and Uruguay. Serious diseases that cause epidemics and production losses include leaf rusts, powdery mildew, and fungal leaf blights (Septoria leaf blotch, spot blotch). These diseases are present every year since normal conditions are conducive to their appearance and dissemination.

- Chile is the largest consumer of fungicides in South America, with a consumption of 4.1 kg/ha in the year 2022. This is because certain regions in Chile have climatic conditions, such as high humidity, rainfall, and temperature fluctuations, which can create a conducive environment for fungal disease development. To prevent and manage these diseases, farmers often rely on fungicides as a proactive measure.

- Climatic conditions prevailing in southern Brazil are highly conducive to the development of several important fungal foliar diseases. A twelve-year study demonstrated that wheat plants sprayed with fungicide showed a mean yield increase of 40%. Brazil accounted for the second most fungicide consumption rate of 0.9 kg/ha in 2022.

- The intensification of agricultural practices, such as increased planting densities, creates a conducive environment for the rapid proliferation and establishment of fungal pathogens, thereby fueling the demand for fungicides during the forecast period.

Mancozeb is the most popularly used fungicide in South America

- Mancozeb is a fungicide belonging to the chemical class of dithiocarbamates. It is commonly used in South America to control fungal diseases in various crops. Mancozeb is effective in managing a wide range of fungal diseases, including late blight, downy mildew, early blight, and anthracnose, in crops like potatoes, tomatoes, grapes, and bananas. Mancozeb works by interfering with the metabolic processes of the fungi, preventing their growth and reproduction. In addition, Mancozeb has a broad spectrum of activity compared to other fungicides and acts on multiple sites within the fungal cell, making it more effective. Mancozeb was priced at USD 7.8 thousand in South America in 2022.

- Propineb is also a fungicide belonging to the chemical class of dithiocarbamates, similar to Mancozeb. It is used to control various fungal diseases in agriculture. Propineb is effective in managing fungal diseases such as downy mildew, late blight, leaf spot, and blight in various crops. Like Mancozeb, Propineb also works through multi-site activity, making it less prone to resistance development in fungal populations. Propineb was priced at USD 3.54 thousand in South America in the year 2022.

- Similar to Mancozeb and Propineb, Ziram belongs to the chemical class of dithiocarbamates, priced at USD 3.3 thousand per metric in 2022. It is commonly used to control fungal diseases in agriculture and is known to effectively manage fungal diseases such as common blight, downy mildew, leaf spot, and anthracnose. Ziram inhibits several key enzymes in the fungal cell, disrupting various metabolic processes and interfering with the pathogens' ability to grow and reproduce. The multi-site activity makes it an effective tool for disease control over the long term.

South America Fungicide Industry Overview

The South America Fungicide Market is fairly consolidated, with the top five companies occupying 70.48%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Chile

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Rainbow Agro

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

杀菌剂市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、地区和竞争细分,2020-2030 年)种子处理杀菌剂市场-全球产业规模、份额、趋势、机会及预测(按类型、作物类型、形态、应用、地区和竞争细分,2020-2030 年)

杀菌剂市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、地区和竞争细分,2020-2030 年)种子处理杀菌剂市场-全球产业规模、份额、趋势、机会及预测(按类型、作物类型、形态、应用、地区和竞争细分,2020-2030 年) 2025-2030 年全球甲氧基丙烯酸酯类杀菌剂市场预测(按类型、剂型、作物类型、施用方法和分销管道)

2025-2030 年全球甲氧基丙烯酸酯类杀菌剂市场预测(按类型、剂型、作物类型、施用方法和分销管道) 农作物杀菌剂市场(按类型、应用、作物类型、国家/地区)-2024 年至 2032 年产业分析、市场规模、市场份额及预测

农作物杀菌剂市场(按类型、应用、作物类型、国家/地区)-2024 年至 2032 年产业分析、市场规模、市场份额及预测 全球农业杀菌剂市场

全球农业杀菌剂市场 2025年全球三唑类杀菌剂市场报告2025年全球化学杀菌剂市场报告2025年种子处理杀菌剂全球市场报告

2025年全球三唑类杀菌剂市场报告2025年全球化学杀菌剂市场报告2025年种子处理杀菌剂全球市场报告 全球甲氧基丙烯酸酯类市场(至 2030 年)按产品类型、作物类型、剂型、应用方法和地区划分

全球甲氧基丙烯酸酯类市场(至 2030 年)按产品类型、作物类型、剂型、应用方法和地区划分 2032年作物杀菌剂市场预测:按产品类型、作物类型、剂型、应用、最终用户和地区进行的全球分析

2032年作物杀菌剂市场预测:按产品类型、作物类型、剂型、应用、最终用户和地区进行的全球分析

▼