|

市场调查报告书

商品编码

1684043

工业MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Industrial MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

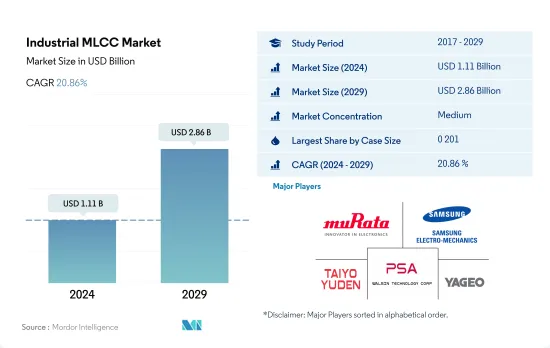

工业 MLCC 市场规模预计在 2024 年为 11.1 亿美元,预计到 2029 年将达到 28.6 亿美元,预测期内(2024-2029 年)的复合年增长率为 20.86%。

先进的电子元件和工业应用之间存在着动态的相互作用。

- 工业 MLCC 市场按外壳尺寸细分,呈现以先进电子元件和工业应用之间的相互作用为特征的动态格局。其中,0 201、0 402、0 603、1 210 和 1 005 等特定外壳尺寸体现了 MLCC 在确保各种应用的最佳性能和可靠性方面发挥的重要作用。

- 外壳尺寸 0 201 在交流伺服马达中很重要,对于机器人、半导体设备和飞机系统等精密驱动应用至关重要。这些 MLCC 提高了效率、可靠性和降噪效果,对于在不同工业环境中实现无缝运作至关重要。

- 0402 外壳尺寸类别在追求节能解决方案中发挥核心作用,并符合减少排放和实现永续工业实践的全球措施。此类 MLCC 可促进高效配电和讯号完整性,支援采用节能技术。协作机器人和自动化正在推动 1210 MLCC 的需求,确保密闭空间内的稳定性。这些 MLCC 与OMRON的 TM20 和 Doosan Robotics 的 E-SERIES 协作机器人相容。

- 随着工业自动化的发展,对 0603 MLCC 的需求也不断增长。全球工业生产的成长正在加强市场并满足对紧凑和可靠的 MLCC 的需求。 1005 MLCC与精密机械相容,符合自动化趋势,特别体现在中国协作机器人安装趋势。随着功率半导体和电子产品满足电动车需求和能源效率计划,0 805、1 812、2 220、1 218 和 1 813 等外壳尺寸的 MLCC 将推动 MLCC 和半导体市场的成长。

技术进步和经济动态正在塑造市场格局并推动全球工业 MLCC 市场的发展

- 在快速的技术进步和不断变化的经济状况的共同推动下,全球工业 MLCC 市场正处于关键的十字路口。在北美,自动化和对製造卓越的不懈追求正在推动 MLCC 的采用。强劲的工业机器人市场,尤其是美国和加拿大的市场,正在催化需求的稳定成长。本部分不仅强调了 MLCC 在工业机器人中的日益普及,还强调了 MLCC 在服务机器人中的作用不断扩大,以适应该地区的医疗保健和老化挑战。

- 以日本和中国主导的亚太地区正在崛起成为科技强国。自动化、机器人、人工智慧和物联网解决方案的蓬勃发展正在推动该地区向前发展。本分析深入探讨了 MLCC 如何实现日本复杂机器人的稳定性以及如何推动中国 5G工业IoT(IIoT) 设备的崛起。该地区的技术先驱将塑造 MLCC 需求的未来。

- 在欧洲,工业 4.0 的曙光正在彻底改变製造业和机器人技术。探索了工业机器人和 MLCC 之间的复杂相互作用,强调了 MLCC 在电源管理和稳健性能方面的关键作用。随着欧洲机器人的快速普及,MLCC的需求日益受到关注,因为它可以提高业务效率,并有望成为变革性成长的舞台。

- 包括拉丁美洲、中东和非洲在内的世界其他地区则呈现多样化的经济转变和技术期望。

全球工业MLCC市场趋势

为了满足自动化应用不断变化的需求,不断进步,对控制 PLC 的销售需求也在增加。

- MLCC 是 PLC 的重要组成部分,与处理器、电源和输入/输出 (I/O) 单元一样。 MLCC在PLC中的关键作用是确保微处理器和积体电路等敏感元件的稳定电源供应和滤除杂讯。

- 透过提供可靠的去耦或旁路功能,MLCC 可提高 PLC 效能、降低故障或资料损坏的可能性,并确保在工业环境中的无缝运作。因此,由于工业自动化需要强大且可靠的电源管理解决方案,PLC 市场对 MLCC 的需求持续成长。

- 工业可程式逻辑控制器 (PLC) 的需求受到持续进步的推动,以满足自动化应用不断变化的需求。 PLC 现在提供增强的程式功能,从而实现更大的灵活性、扩充性和易用性。 PLC 提供更大的记忆体容量、紧凑的尺寸,并允许整合高速(Gigabit)乙太网路连接和内建无线功能。此功能有助于高效监控和控制分散式伺服器/多用户应用程式。具有高电容值的小型 MLCC 的出现使 PLC 製造商能够设计紧凑但功能强大的系统,有助于满足对节省空间、高性能 PLC 解决方案的需求。

智慧工厂的出现推动了对MLCC的需求

- 工业机器人产量将从2021年的41万台增加到2022年的43万台。工业机器人在製造业的工业自动化中发挥着至关重要的作用,工业中的许多核心业务都由机器人管理。在工业机器人中,MLCC主要用于滤波和去耦用途。 MLCC 有助于稳定和调节电源,确保机器人电子元件平稳可靠地运作。工业机器人对 MLCC 的要求取决于机器人的尺寸和复杂性、功率需求以及所需的精度和可靠性等级等因素。

- 工业机器人市场细分为关节机器人、线性机器人、圆柱形机器人、并联机器人和SCARA机器人,用于汽车、化学和製造、建筑、电气和电子、食品和饮料、机械和金属、製药等各种终端用户行业。汽车产业整体产量从 2021 年的 1.332 亿辆成长到 2022 年的 1.3987 亿辆。汽车需求的成长需要增加产量,这导致工业机器人在汽车製造过程中的使用增加以及人工智慧数位化的参与。

- 在新冠疫情期间,对机器人的需求增加,因为它们被用来帮助遏制感染疾病的传播。机器人的引入使得医疗专业人员能够以最高的精度进行手术。

工业MLCC产业概况

工业MLCC市场适度整合,前五大企业占57.14%。该市场的主要企业有:村田製作所、三星电机、太阳诱电、华新科技和国巨集团(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 工业自动化全球销售

- 控制PLC的全球销售

- 全球工业机器人销售

- 服务机器人全球销售

- 伺服马达全球销售

- 太阳能逆变器和优化器的全球销售

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 錶壳尺寸

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- 其他的

- 电压

- 600V~1100V

- 小于600V

- 1100V以上

- 电容

- 10μF至100μF

- 小于10μF

- 100μF 以上

- 介电类型

- 1级

- 2级

- 地区

- 亚太地区

- 欧洲

- 北美洲

- 世界其他地区

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第 7 章 CEO 的关键策略问题CEO 的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001986

The Industrial MLCC Market size is estimated at 1.11 billion USD in 2024, and is expected to reach 2.86 billion USD by 2029, growing at a CAGR of 20.86% during the forecast period (2024-2029).

There is a dynamic interplay between advanced electronic components and industrial applications in the market

- The industrial MLCC market, categorized by case size, showcases a dynamic landscape characterized by the interplay between advanced electronic components and industrial applications. Within this context, the specific case sizes 0 201, 0 402, 0 603, 1 210, 1 005, and others exemplify the pivotal role of MLCCs in ensuring optimal performance and reliability across various sectors.

- The 0 201 case size is critical in AC servo motors and is essential for precision-driven applications like robotics, semiconductor equipment, and aircraft systems. These MLCCs enhance efficiency, reliability, and noise reduction, which is vital for seamless operation in diverse industrial settings.

- The 0 402 case size category takes center stage in the pursuit of energy-efficient solutions, aligning with global initiatives to reduce emissions and achieve sustainable industrial practices. MLCCs in this category facilitate efficient power distribution and signal integrity, supporting the adoption of energy-efficient technologies. Cobots and automation drive the demand for 1 210 MLCCs, ensuring stability in confined spaces. These MLCCs align with OMRON's TM20 and Doosan Robotics' E-SERIES cobots.

- The demand for 0 603 MLCCs is growing with industrial automation. Global industrial production growth strengthens the market, aligning with compact, reliable MLCC requirements. The 1 005 MLCCs cater to precision machinery and align with automation trends, mirroring cobot installations, especially in China. MLCCs in case sizes like 0 805, 1 812, 2 220, 1 218, and 1 813 power semiconductors and electronics meet EV demands and energy efficiency initiatives, thus driving the growth of the MLCC and semiconductor market.

Technological advancements and economic dynamics are shaping the landscape, propelling the global industrial MLCC market

- The global industrial MLCC market stands at a critical juncture, propelled by the confluence of rapid technological advancements and the ever-evolving economic landscape. In North America, a relentless pursuit of automation and manufacturing excellence drives the adoption of MLCCs. Robust industrial robotics markets, particularly in the United States and Canada, are catalysts for the steady rise in demand. This segment not only explores the increasing integration of MLCCs in industrial robots but also uncovers the expanding role of these components in service robots, aligning with the region's healthcare and aging population challenges.

- Asia-Pacific is emerging as a technological powerhouse, with Japan and China leading the charge. A vibrant landscape of automation, robotics, AI, and IoT solutions propels the region forward. This analysis dives deep into how MLCCs enable stability in Japan's intricate robotics while facilitating the rise of 5G-powered industrial IoT (IIoT) devices in China. The region's technological pioneers are poised to shape the future of MLCC demand.

- In Europe, the dawn of Industry 4.0 revolutionized manufacturing and robotics. The intricate interplay between industrial robots and MLCCs is explored, emphasizing their pivotal role in power management and robust performance. As Europe experiences a surge in robotic installations, the demand for MLCCs is expected to enhance operational efficiency and gain prominence, setting the stage for transformative growth.

- The Rest of the World, encompassing Latin America and Middle East & Africa, unveils a tapestry of diverse economic shifts and technological aspirations.

Global Industrial MLCC Market Trends

Continuous advancements to meet the evolving requirements of automation applications are increasing the demand for control PLC sales

- MLCCs are essential components in PLCs, alongside the processor, power supply, and input/output (I/O) section. An important role of MLCCs in PLCs is to ensure a stable power supply and filter out noise for sensitive components like microprocessors and integrated circuits.

- By providing reliable decoupling or bypassing capabilities, MLCCs enhance the performance of PLCs, reducing the potential for malfunctions and data corruption, thus ensuring seamless operation in industrial environments. As a result, the demand for MLCCs in the PLC market continues to grow, driven by the need for robust and reliable power management solutions in industrial automation.

- The demand for industrial programmable logic controllers (PLCs) is fueled by their continuous advancements to meet the evolving requirements of automation applications. PLCs now offer enhanced programming capabilities, enabling greater flexibility, scalability, and ease of use. They are equipped with larger memory capacities and compact sizes, allowing for the integration of high-speed (gigabit) Ethernet connectivity and built-in wireless features. This feature facilitates efficient monitoring and control of distributed server/multi-user applications. The availability of compact MLCCs with high capacitance values enables PLC manufacturers to design smaller yet highly functional systems, meeting the demand for space-efficient and high-performance PLC solutions.

The emergence of smart factories is propelling the demand for MLCCs

- The industrial robots' production volume increased from 0.41 million units in 2021 to 0.43 million units in 2022. Industrial robots play a crucial role in manufacturing industrial automation, with many core operations in industries being managed by robots. In industrial robots, MLCCs are primarily used for filtering and decoupling purposes. They help stabilize and regulate the power supply, ensuring smooth and reliable operation of the robot's electronic components. MLCC requirements in industrial robots can vary depending on factors such as the size and complexity of the robot, the power requirements, and the level of precision and reliability needed.

- The industrial robotics market is segmented into articulated robots, linear robots, cylindrical robots, parallel robots, and SCARA robots, which can be used in various end-user industries such as automotive, chemical and manufacturing, construction, electrical and electronics, food and beverage, machinery and metal, and pharmaceutical. The overall automotive industry witnessed growth in terms of production volume, from 133.20 million units in 2021 to 139.87 million units in 2022. The rising demand for automobiles necessitates increased production, resulting in the increased use of industrial robots in the automotive manufacturing process and the involvement of AI and digitalization.

- During the COVID-19 pandemic, there was an increase in demand for robots since they could be used to curb the spread of infectious diseases. With the introduction of robots, healthcare professionals were able to perform surgery with maximum precision.

Industrial MLCC Industry Overview

The Industrial MLCC Market is moderately consolidated, with the top five companies occupying 57.14%. The major players in this market are Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd, Walsin Technology Corporation and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Global Industrial Automation Sales

- 4.1.1 Global Control PLC Sales

- 4.1.2 Global Industrial Robots Sales

- 4.1.3 Global Service Robots Sales

- 4.1.4 Global Servo Motor Sales

- 4.1.5 Global Solar PV Inverters and Optimizers Sales

- 4.2 Regulatory Framework

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Case Size

- 5.1.1 0 201

- 5.1.2 0 402

- 5.1.3 0 603

- 5.1.4 1 005

- 5.1.5 1 210

- 5.1.6 Others

- 5.2 Voltage

- 5.2.1 600V to 1100V

- 5.2.2 Less than 600V

- 5.2.3 More than 1100V

- 5.3 Capacitance

- 5.3.1 10 μF to 100 μF

- 5.3.2 Less than 10 μF

- 5.3.3 More than 100 μF

- 5.4 Dielectric Type

- 5.4.1 Class 1

- 5.4.2 Class 2

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

用于MLCC内电极的镍浆-2026年至2032年全球市占率及排名、总收入及需求预测

用于MLCC内电极的镍浆-2026年至2032年全球市占率及排名、总收入及需求预测 用于MLCC电极的镍浆(<200nm)—全球市场份额和排名、总收入和需求预测(2025-2031年)MLCC镍内电极膏:2025-2031年全球市占率排名、总销售额及需求预测

用于MLCC电极的镍浆(<200nm)—全球市场份额和排名、总收入和需求预测(2025-2031年)MLCC镍内电极膏:2025-2031年全球市占率排名、总销售额及需求预测 MLCC-市场占有率分析、产业趋势与统计、成长预测(2024-2029)个人电脑和笔记型电脑用 MLCC——市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中压MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)中国MLCC市场占有率分析、产业趋势与统计、成长预测(2025-2030年)亚太地区MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)北美MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)印度MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

MLCC-市场占有率分析、产业趋势与统计、成长预测(2024-2029)个人电脑和笔记型电脑用 MLCC——市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中压MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)中国MLCC市场占有率分析、产业趋势与统计、成长预测(2025-2030年)亚太地区MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)北美MLCC:市场占有率分析、产业趋势与成长预测(2025-2030年)印度MLCC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

▼