|

市场调查报告书

商品编码

1685780

农药:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

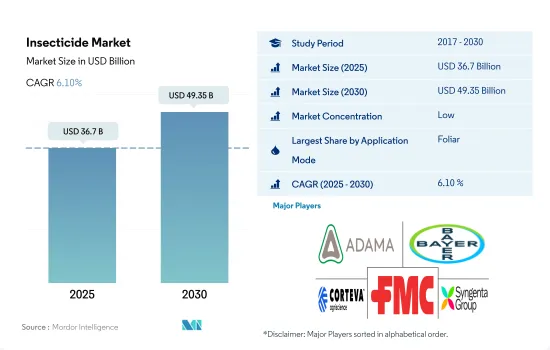

杀虫剂市场规模预计在 2025 年为 367 亿美元,预计到 2030 年将达到 493.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.10%。

害虫压力的增加以及保护作物免受害虫侵害的需求推动了对农药的需求

- 随着使用方法的多样化,农药的使用量不断增加,以保护作物免受虫害。 2022 年,叶面喷布领域将占据主要份额,占整个杀虫剂市场的 56.9%。这归因于害虫防治压力的增加以及害虫防治的有效性、快速性和针对性。

- 从以金额为准来看,全球杀虫剂市场的种子处理方法预计在 2023 年至 2029 年期间的复合年增长率为 4.5%。这种方法之所以主要被使用,是因为它可以在作物生命週期的早期控制许多种子和幼苗害虫,例如蚜虫、蓟马、甘蓝夜蛾和介壳虫。

- 农药市场中的土壤处理部分预计在 2023 年至 2029 年期间的复合年增长率为 4.1%。影响小麦、大豆、油棕榈、可可和咖啡等重要经济作物根部生长的主要害虫是蛞蝓、金针虫、船虫和土壤蛀虫。因此,预计土壤处理方面对农药的需求将会增加,以保护作物免受这些害虫的侵害。

- 农民对化学灌溉方法的认识越来越深入。将农药施用与灌溉结合起来可以为农民节省时间和精力,这对于管理大型农业经营的农民来说是一个方便的选择。受这些因素的推动,预计预测期内(2023-2029年),该应用模式杀虫剂的市场价值将以 3.7% 的复合年增长率增长。

- 预计这些施用方法的全球杀虫剂市场将经历显着成长,2023 年至 2029 年的复合年增长率为 4.2%。

由于气候条件变化导致的种植面积扩大促进了市场成长。

- 世界人口不断增长以及生产更多粮食的需求导致农业产量增加,这反过来又推动了对用于保护作物免受害虫侵害的农药的需求。在过去一段时期(2017-2022 年),杀虫剂市场成长了 84.498 亿美元3。

- 南美洲是农业生产的主要地区之一,2022 年占了 24.9% 的市场。大豆、玉米、甘蔗和其他作物的大量产量对有效控制害虫的杀虫剂产生了巨大的需求。南方树皮甲虫(Spodoptera eridania)等昆虫的侵扰日益增多,推动着市场的成长。

- 金额,亚太地区是杀虫剂市场占有最大份额的地区,预计将成为成长最快的市场,预测期内(2023-2029 年)的复合年增长率为 3.9%。由于气候变化,破坏农作物的害虫变得越来越普遍。因此,杀虫剂的需求预计会增加,因为它们是防治害虫和确保作物产量的有效手段。

- 预计预测期内(2023-2029 年)北美的复合年增长率将达到 4.7%。保护作物的需要,加上入侵害虫的引入或扩散,可能会增加对用于管理和控制这些新威胁的杀虫剂的需求。

- 然而,欧洲和非洲拥有强劲的农业部门,在全球农药市场中发挥关键作用。预计在此期间这两个地区的复合年增长率分别为 4.6% 和 3.7%。

- 预计 2023-2029 年全球杀虫剂市场复合年增长率为 4.2%。由于气候变化,农业部门的快速扩张正在推动市场成长。

全球杀虫剂市场趋势

全球暖化导致害虫增多,农药使用量增加

- 全球平均每公顷农地化学农药消费量为918.7公克。由于农业集约化、害虫增加以及为确保全球粮食安全而对高产量和作物生产力的需求等因素,这一情况多年来一直在增加。根据联合国粮食及农业组织的资料,全球每年有40%的农作物产量因病虫害而损失,平均造成700亿美元左右的经济损失。

- 欧洲使用的杀虫剂比世界上任何其他地区都多,其中德国使用的杀虫剂最多,达到每公顷 3,028.0 克。这可能是由于高度集约的农业实践注重最大限度地提高作物产量。集约农业通常使用大量投入,包括杀虫剂,来控制害虫并确保最佳作物产量。紧随欧洲之后的是亚太地区,平均杀虫剂施用率为每公顷 975.1 克。

- 在北美国家中,美国每公顷杀虫剂消费量最高,2022 年为 791.7 克。这是因为作物种植面积大,不断变化的气候条件增加了遭受虫害的机会。

- 全球暖化导致的气候条件变化为某些害虫的滋生创造了有利条件,从而引发严重的疫情。例如,2020年蝗虫严重影响了23个国家,其中中东9个国家、东北和非洲11个国家、南亚3个国家,造成的损失估计达85亿美元。这种情况迫使农民在农业生产中使用大量农药。

Imidacloprid是最经济的杀虫剂,且杀虫剂频谱广。

- Lambda-Cyhalothrin属于拟除虫菊酯类杀虫剂,是一种以菊花中天然除虫菊酯为原型的合成化学物质。Lambda-Cyhalothrin用于防治棉花、玉米、大豆、蔬菜和水果作物中的蚜虫、蓟马、叶蝉、粉蝨和各种毛虫等害虫。活性成分可作为神经毒素,针对昆虫的神经系统。它会抑制神经细胞的正常功能,导致害虫瘫痪并最终死亡。 2022 年的价格为每吨 22,700 美元。

- Cypermethrin是一种非合成拟除虫菊酯,用于控制跳甲、果子狸、蟑螂、白蚁、瓢虫、蝎子和黄蜂。 2022年的价格为21,000美元。巴西是全球三大Cypermethrin进口国之一,根据欧盟-南方共同市场协议,欧盟是巴西的主要出口国。

- Emamectin benzoate是一种属于阿维菌素类化学杀虫剂。它透过攻击神经系统来杀死害虫。它与神经细胞上的特定受体结合,使害虫麻痹并最终杀死它们。欧洲国家使用Emamectin benzoate来防治农业中的各种害虫。价格为每吨17,300美元。

- Imidacloprid是一种新烟碱类杀虫剂,可有效控制多种害虫,包括蚜虫、叶蝉、粉蝨、蓟马和某些甲虫。 2022 年该活性成分的价格为每吨 17,170 美元。Malathion是农药中最便宜的化学物质。 2022 年的价格为每吨 12,500 美元。

农药业概况

农药市场较为分散,前五大企业的市占率为33.15%。该市场的主要企业是:ADAMA Agricultural Solutions Ltd.、Bayer AG、Corteva Agriscience、FMC Corporation和Syngenta Group(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 有效成分价格分析

- 法律规范

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 智利

- 中国

- 法国

- 德国

- 印度

- 印尼

- 义大利

- 日本

- 墨西哥

- 缅甸

- 荷兰

- 巴基斯坦

- 菲律宾

- 俄罗斯

- 南非

- 西班牙

- 泰国

- 乌克兰

- 英国

- 美国

- 越南

- 价值链与通路分析

第五章 市场区隔

- 如何使用

- 化学灌溉

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

- 地区

- 非洲

- 按国家

- 南非

- 非洲其他地区

- 亚太地区

- 按国家

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 缅甸

- 巴基斯坦

- 菲律宾

- 泰国

- 越南

- 其他亚太地区

- 欧洲

- 按国家

- 法国

- 德国

- 义大利

- 荷兰

- 俄罗斯

- 西班牙

- 乌克兰

- 英国

- 其他欧洲国家

- 北美洲

- 按国家

- 加拿大

- 墨西哥

- 美国

- 北美其他地区

- 南美洲

- 按国家

- 阿根廷

- 巴西

- 智利

- 其他南美国家

- 非洲

第六章 竞争格局

- 重大策略倡议

- 市场占有率分析

- 业务状况

- 公司简介

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 47401

The Insecticide Market size is estimated at 36.7 billion USD in 2025, and is expected to reach 49.35 billion USD by 2030, growing at a CAGR of 6.10% during the forecast period (2025-2030).

The rising pest pressure and the need to protect crops from damaging insects are driving the demand for insecticides

- Insecticide use is increasing through different application modes to protect crops from insect pests. In 2022, the foliar segment held the major share, accounting for 56.9% of the overall insecticide market. This could be attributed to increasing pest pressure and its effectiveness in controlling insects, rapid action, and targeted control.

- In terms of value, the seed treatment method in the global insecticide market is expected to record a CAGR of 4.5% between 2023 and 2029. This method is being majorly adopted because it protects against many pests that attack seeds or seedlings, such as aphids, thrips, wireworms, and beetles, at the very beginning of a crop's life cycle.

- Soil treatment in the insecticide market is expected to record a 4.1% CAGR between 2023 and 2029. The main pests affecting the root growth of economically significant crops such as wheat, soybean, oil palm, cocoa, and coffee are slugs, wireworms, fungi gnats, and soil mealybugs. Therefore, to protect crops from these pests, the demand for insecticides in terms of soil treatment is expected to increase.

- Farmers are becoming more and more aware of the chemigation method. By combining insecticide application with irrigation, farmers can save time and labor, making it a convenient choice for farmers managing large-scale agricultural operations. Due to these factors, the insecticide market value in this application mode is projected to record a 3.7% CAGR during the forecast period (2023-2029).

- The global insecticide market in these application methods is expected to witness significant growth and is projected to record a 4.2% CAGR from 2023 to 2029.

The expansion of cropland areas with changes in climate conditions is contributing to the growth of the market

- The increase in global population and the need for higher food production have led to the expansion of agricultural production, which, in turn, boosted the demand for insecticides to protect the crops from damaging pests. During the historical period (2017-2022), the insecticide market grew by USD 8,449.8 million.3

- South America was one of the major regions in agriculture production, with a 24.9% market value in 2022. The vast production of soybeans, corn, sugarcane, and other crops creates a significant demand for insecticides to manage pests effectively. The rise of infestation of insects such as southern armyworm (Spodoptera eridania) has driven the growth of the market.

- Asia-Pacific holds the largest insecticide market value share, and the market is anticipated to grow fastest in the region, registering a CAGR of 3.9% during the forecast period (2023-2029). Insect pests that could damage crops are spreading due to the changing climate. Consequently, the demand for insecticides is expected to rise as they are efficient tools for addressing these pests and ensuring crop productivity.

- North America is projected to register a CAGR of 4.7% during the forecast period (2023-2029). The need to protect the crops, coupled with the introduction or spread of invasive pests, could lead to increased demand for insecticides to manage and control these new threats.

- However, Europe and Africa have a substantial agricultural sector and play a vital role in the global insecticide market. These regions are projected to register CAGRs of 4.6% and 3.7%, respectively, during the period.

- The global insecticide market is projected to register a CAGR of 4.2% during 2023-2029. The rapidly expanding agriculture sector with a changing climate is driving the growth of the market.

Global Insecticide Market Trends

Increased pest proliferation due to global warming is increasing the usage of insecticides

- The average global consumption of chemical insecticides is 918.7 g per hectare of agricultural land. It has been increasing over the years owing to factors like the intensification of agriculture, increasing pest populations, and the need for higher yield and crop productivity to ensure global food security. According to the data provided by the Food and Agriculture Organization, 40% of global crop production is lost to pests annually, resulting in an average economic loss of around USD 70.0 billion.

- Europe witnessed higher insecticide applications compared to other regions of the world, with Germany having a higher per-hectare consumption of 3,028.0 g, which may be attributed to its highly intensive agricultural practices, with a significant focus on maximizing crop yields. Intensive agriculture often involves the use of higher inputs, including insecticides, to manage pests and ensure optimal crop production. Europe is followed by Asia-Pacific, with an average insecticide application of 975.1 g per hectare.

- Among the North American countries, the United States witnessed the largest consumption of insecticides per hectare, with 791.7 g in 2022, attributed to the large area under the cultivation of crops and increased exposure to insect pest infestations due to constantly changing climatic conditions.

- Changing climatic conditions due to global warming have created favorable conditions for certain pests, resulting in severe outbreaks. For instance, a locust outbreak in 2020 severely affected 23 countries, i.e., nine in East Africa, 11 in North Africa and the Middle East, and three in South Asia, causing an estimated loss of USD 8.5 billion. These circumstances necessitate farmers to use higher amounts of insecticides in agriculture.

Imidacloprid is the most affordable insecticide with a broad spectrum of activity

- Lambda-cyhalothrin belongs to the class of pyrethroid insecticides, which are synthetic chemicals modeled after natural pyrethrins found in chrysanthemum flowers. Lambda-cyhalothrin is used to control pests such as aphids, thrips, leafhoppers, whiteflies, and various caterpillar species in crops like cotton, corn, soybean, vegetables, and fruits. This active ingredient acts as a neurotoxin, targeting the nervous system of insects. It disrupts the normal functioning of nerve cells, leading to paralysis and, ultimately, the death of the pests. In 2022, it was priced at USD 22.7 thousand per metric ton.

- Cypermethrin is a non-synthetic pyrethroid used to control flea beetles, boxelder bugs, cockroaches, termites, ladybugs, scorpions, and yellow jackets. It was priced at USD 21.0 thousand in 2022. Brazil ranks among the top three importers of cypermethrin globally, with the European Union being a major exporter to Brazil under the EU-Mercosur deal.

- Emamectin benzoate is an insecticide belonging to the chemical class of avermectins. It kills the pests by targeting the nervous system. It binds to specific receptors in nerve cells, leading to paralysis and the eventual death of the pests. Emamectin benzoate is majorly used in European countries to control various insect pests in agriculture. It was priced at USD 17.3 thousand per metric ton.

- Imidacloprid is a neonicotinoid insecticide used to effectively manage various pests, including aphids, leafhoppers, whiteflies, thrips, and certain beetle species. This active ingredient was priced at USD 17.17 thousand per metric ton in 2022. Malathion is the most affordable chemical among the insecticides. It was valued at USD 12.5 thousand per metric ton in 2022.

Insecticide Industry Overview

The Insecticide Market is fragmented, with the top five companies occupying 33.15%. The major players in this market are ADAMA Agricultural Solutions Ltd., Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

Buprofezin市场:2026-2032年全球市场预测(按剂型、作物、应用方法、最终用户和销售管道)克百威市场:按剂型、作物类型、最终用户、分销管道和应用划分-2026-2032年全球预测高效能Cypermethrin市场:按製剂类型、销售管道和应用划分-2026-2032年全球预测二唑唑市场:依作物类型、剂型、应用方法、最终用户和分销管道划分-2026-2032年全球预测

Buprofezin市场:2026-2032年全球市场预测(按剂型、作物、应用方法、最终用户和销售管道)克百威市场:按剂型、作物类型、最终用户、分销管道和应用划分-2026-2032年全球预测高效能Cypermethrin市场:按製剂类型、销售管道和应用划分-2026-2032年全球预测二唑唑市场:依作物类型、剂型、应用方法、最终用户和分销管道划分-2026-2032年全球预测 美国农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球农药市场规模、份额、趋势和成长分析报告(2026-2034年)

全球农药市场规模、份额、趋势和成长分析报告(2026-2034年) 全球农药市场报告(2026 年)

全球农药市场报告(2026 年) 农药市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年技术级多杀菌素市场依製剂类型、作物类型、害虫类型和应用方法划分-2026-2032年全球预测杀虫剂种子处理市场-2026-2031年预测

农药市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年技术级多杀菌素市场依製剂类型、作物类型、害虫类型和应用方法划分-2026-2032年全球预测杀虫剂种子处理市场-2026-2031年预测

▼