|

市场调查报告书

商品编码

1687228

穿戴式感测器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Wearable Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

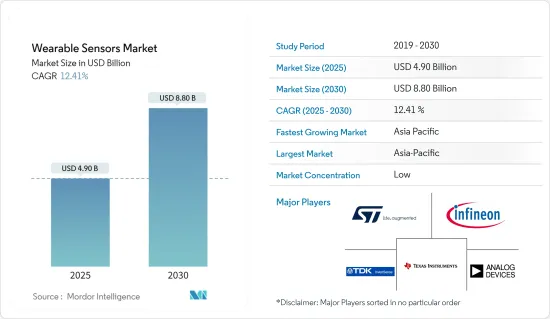

穿戴式感测器市场规模预计在 2025 年为 49 亿美元,预计到 2030 年将达到 88 亿美元,预测期内(2025-2030 年)的复合年增长率为 12.41%。

电子产业因数数位化而蓬勃发展,推动了对广泛用于自我健康监测应用的可穿戴技术设备的需求。

主要亮点

- 由于消费者对追踪步数和步行距离等即时运动感应活动的兴趣日益浓厚,可穿戴感测器对于穿戴式装置至关重要。使用者可以透过分析产生的资料来获得切实的结果来确定健身和健康目标。穿戴式科技完全依靠感测器来监测消费者的健康和资料并帮助他们做出有意义的决策。不断发展的感测器技术使穿戴式装置变得更加智能,也越来越受消费者欢迎。

- 消费性电子产品的支出也刺激了穿戴式装置的成长。此外,由于人口成长和生活方式的改变而导致的都市化不断加快,人们的健康和安全意识也不断增强。这是刺激健身追踪器、耳戴式装置和智慧型手錶等穿戴式装置成长的主要因素。

- 智慧型穿戴装置上高性能感测器的成长、电池尺寸和效率的改进以及感测器和相关组件的小型化是推动穿戴式动作感测器市场的主要因素。

- 随着消费者转向智慧穿戴设备,零件成本的上升推高了设备价格,限制了市场采用。智慧型手錶和健身追踪器拥有低价市场,吸引了大量消费者的注意。然而,随着技术变得越来越普及,其他设备(如鞋类、眼镜产品和内衣产品)变得更加昂贵,采用率较低。目前大多数穿戴式科技价格昂贵,这对市场采用产生了负面影响。

- COVID-19 疫情对穿戴式感测器市场产生了积极影响,并凸显了利用数位基础设施进行远端患者监控的必要性。由于目前的病毒检测和疫苗需要时间来开发,可穿戴感测器可以帮助检测疾病并追踪个人和人群的健康状况。

穿戴式感测器市场趋势

体育健身产业占大部分市场占有率

- 对健康监测器和健身追踪器的需求不断增长是推动全球穿戴式感测器出货量成长的关键因素。随着消费者越来越意识到这些设备所提供的功能(例如远端健康和健身监测),全球对基于感测器的设备的需求正在增长。根据Cisco预测,2022年北美将拥有最多的使用穿戴式装置的5G连线。 2022年北美和亚洲的穿戴式装置合计将占全球穿戴式5G连线的约70%。

- 穿戴式性能设备正逐渐向一般大众和运动队伍推出。如今,技术的进步使得个人耐力运动员、运动团队和医生能够监测功能性动作、工作量和生物特征标记,以提高运动表现。不断成长正在推动市场的发展。

- 科技组织在开发和推广运动团队穿戴装置方面取得了长足的进步。 Zephyr Technology、Viperpod、Smartlife、miCoach 和 Catapult 等公司正在重塑运动教练的决策方式、体育活动的进行方式以及职业运动员的表现、健康和安全。这些技术也正从专业运动界迅速转向消费市场。

- 2022 年 6 月,Garmin 发布了 Forerunner 955 Solar,这是其首款具有太阳能充电功能的跑步专用智慧型手錶。 Forerunner 955 Solar 配备 Power Glass 太阳能充电镜片,在智慧型手錶模式下可为运动员提供长达 20 天1 的电池续航时间,在 GPS 模式下可为运动员提供长达 49 小时2 的电池续航时间。这款智慧型手錶具有常亮的全彩显示屏,即使在阳光直射下也清晰可见。灵敏的触控萤幕加上传统的五键设计,可以快速存取标准健康功能、更轻鬆的地图导航等。

- 此外,2021 年 9 月,Whoop 为其以健身为中心的健身穿戴装置筹集了 2 亿美元。 F 轮融资使 Whoop 的公开投资总额达到约 4.05 亿美元。Softbank Corporation愿景基金二期融资后,该公司的估值达到 36 亿美元。其他投资者包括 IVP、Cavu Venture Partners、GP Bullhound、Accomplice、NextView Ventures 和 Animal Capital。他们都是日益增多的前赞助商名单中的一部分,其他支持者还有国家橄榄球联盟球员协会、杰克·多尔西和几名职业运动员。

亚太地区发展迅速

- 中国长期以来在晶片产业扮演关键角色,目前正成为晶片小型化领域的领导者。中国晶片小型化的关键驱动因素之一是奈米技术等先进製造技术的发展,这使得生产更小、更有效率的晶片成为可能。这刺激了更小、更有效率的晶片产量激增,这对于穿戴式感测器的发展至关重要。此外,中国政府也推出了多项倡议,推动数位医疗保健和医疗技术的发展,其中包括穿戴式感测器。

- 日本近年来数位化进程迅速,预计穿戴式感测器市场将大幅成长。这一趋势受到多种因素推动,包括政府加速采用数位技术的措施、数位原民消费者的增加以及提高各行业生产力和效率的需求。

- 印度的可穿戴感测器市场正在迅速增长,这归因于多种因素,包括数位技术的采用日益广泛、人们对健康和健身的兴趣日益浓厚以及对穿戴式装置优势的认识日益加深。

- 过去几年,随着人们对健身和健康的兴趣日益浓厚、人口老化以及科技和医疗保健的进步,亚太其他地区对穿戴式感测器的需求一直稳步增长。

- 根据东协邮政报道,仅靠养老院不足以满足日益增长的老年人口的需求。这些设施提供的服务也不足,影响了生活品质并让居民产生孤立感。房地产开发商在为居住者建造住宅时也会考虑老龄化社会的问题,这为穿戴式感测器带来了一个潜在的尚未开发市场。

穿戴式感测器产业概况

穿戴式感测器市场竞争激烈,主要参与者包括意法半导体公司 (STMicroelectronics NV)、德州仪器公司 (Texas Instruments Incorporated)、英飞凌科技股份公司 (Infineon Technologies AG)、ADI 公司 (Analog Devices Inc.) 和 InvenSense Inc. (TDK Corporation)。市场参与者正在采用伙伴关係、协作、创新和收购等策略来加强其产品供应并获得永续的竞争优势。

- 2022 年 12 月 - ADI 公司与奥勒冈健康与科学大学 (OHSU) 合作开发了智慧型手錶,以应对青少年日益严重的心理健康危机。面对日益严重的全球精神健康危机,OHSU 旨在利用 ADI 的创新技术和产品来拯救、改善和丰富人们的生活。

- 2022 年 12 月——Panasonic推出了其着名的 Grid-Eye 感测器系列的新成员,配备 90° 镜头。 Grid-Eye 90° 以及其他应用程式对用于追踪和计算个人动作的系统进行了改进。注重隐私的设计师会喜欢 Grid-Eye 系列的 64 像素解析度。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- COVID-19 产业影响评估

第五章 市场动态

- 市场驱动因素

- 增强健康和健身意识

- 智慧穿戴装置日益流行

- 市场挑战

- 设备成本增加

第六章 市场细分

- 按类型

- 化学品和气体

- 压力

- 成像/光学

- 运动

- 其他感测器

- 按应用

- 健康与福祉

- 安全监控

- 运动与健身

- 其他用途

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章 竞争格局

- 公司简介

- STMicroelectronics NV

- Texas Instruments Incorporated

- Infineon Technologies AG

- Analog Devices Inc.

- InvenSense Inc.(TDK Corporation)

- AMS OSRAM AG

- Panasonic Corporation

- NXP Semiconductors NV

- TE Connectivity Ltd

- Bosch Sensortec GmbH(Robert Bosch GmbH)

第八章投资分析

第九章:市场的未来

The Wearable Sensors Market size is estimated at USD 4.90 billion in 2025, and is expected to reach USD 8.80 billion by 2030, at a CAGR of 12.41% during the forecast period (2025-2030).

The electronics industry has thrived significantly, primarily due to digitalization, which drives the demand for wearable technology devices widely used for self-health monitoring applications.

Key Highlights

- Wearable sensors are crucial to wearable devices due to consumers' growing interest in tracking real-time motion-sensing activities, such as step counting and walking distance covered. Users can define their goals for fitness and health using the specific results provided by analyzing the generated data. Wearable technology completely relies on sensors to monitor consumers' health and data and helps make meaningful decisions. With evolving sensor technology, wearables are becoming smart and gaining popularity among consumers.

- Spending on consumer electronic products is also stimulating the growth of wearable devices. Further, the growing population's increasing urbanization and changing lifestyle have raised its health and safety awareness. This has been the major factor stimulating the growth of wearable devices, such as fitness trackers, ear wears, and smartwatches.

- With the ongoing miniaturization of sensors and related components, the growth of the advanced function sensors in smart wearables, the improvement in the battery sizes, and efficiency are the key drivers boosting the wearable motion sensors market.

- With consumers' growing propensity toward smart wearables, the prices of devices are also soaring along with the growing cost of components, thus limiting adoption in the market. Smartwatches and fitness trackers have low-cost segments that drive significant attention from consumers. However, with the proliferation of technology, other devices such as footwear, eyewear, and body wear products are highly priced and have lower adoption rates. Most wearable technologies are currently highly-priced, which is negatively impacting adoption in the market.

- The COVID-19 pandemic had a favorable effect on the market for wearable sensors and highlighted the necessity of utilizing digital infrastructure for remote patient monitoring. Wearable sensors could help with disease detection and tracking individual and population health since current viral tests and vaccines take a while to develop.

Wearable Sensors Market Trends

Sports and Fitness Segment to Hold Major Market Share

- The increasing demand for wellness monitors and fitness trackers is a crucial factor driving the growth of shipments of wearable sensors globally. Globally, demand for sensor-based devices is increasing as consumers become more aware of the features that these devices provide, such as remote monitoring of wellness and fitness. According to Cisco Systems, North America had the most 5G connections made using wearable devices in 2022. Together, wearables in North America and Asia accounted for around 70% of the wearable 5G connections worldwide in 2022.

- Wearable performance devices are significantly available to the general population and athletic teams. Advancements in technology have allowed individual endurance athletes, sports teams, and physicians to monitor functional movements, workloads, and biometric markers to increase performance. The increased growth is driving the market.

- Technology organizations are making significant strides in growing and advertising wearable gadgets for athletic teams. Companies like Zephyr Technology, Viperpod, Smartlife, miCoach, and Catapult are remodeling how athletic coaches make decisions, how sports activities are played, and professional sports players' performance, health, and safety. These technologies are also moving rapidly from the professional sports arena into markets for the general public.

- In June 2022, Garmin Ltd introduced the Forerunner 955 Solar, the company's first dedicated running smartwatch featuring solar charging. The Forerunner 955 Solar features a Power Glass solar charging lens, providing athletes with up to 20 days of battery life in smartwatch mode1 and up to 49 hours in GPS mode2. The smartwatch features an always-on, full-color display that is easy to read in direct sunlight. The responsive touchscreen, coupled with the traditional 5-button design, allows fast access to standard health features, easier map control, etc.

- Further, in September 2021, Whoop raised USD 200 million for athlete-focused fitness wearables. The Series F spherical brings Whoop's general investment to nearly USD 405 million. The spherical series, with the aid of using SoftBank's Vision Fund 2, places the valuation at USD 3.6 billion valuations. Additional investors include IVP, Cavu Venture Partners, GP Bullhound, Accomplice, NextView Ventures, and Animal Capital. They have all been part of an extended listing of former backers, together with the National Football League Players Association, Jack Dorsey, and some expert athletes.

Asia-Pacific to Register Fastest Growth

- China has been a significant player in the chip industry for many years, and the country is now emerging as a leader in chip miniaturization. One of the critical drivers of chip miniaturization in China is the development of advanced manufacturing techniques, such as nanotechnology, which enable the production of more minor and more efficient chips. This has led to a surge in the production of smaller and more efficient chips, which are essential for developing wearable sensors. In addition, the Chinese government has launched several initiatives to promote the development of digital healthcare and medical technologies, including wearable sensors.

- Japan is expected to observe significant growth in the wearable sensors market as it has experienced increasing digitization in recent years. This trend has been driven by several factors, including government initiatives to promote the adoption of digital technologies, a growing number of digital-native consumers, and the need to improve productivity and efficiency in various industries.

- The market for wearable sensors is rapidly growing in India, driven by several factors, including the increasing adoption of digital technologies, a growing focus on health and fitness, and a rising awareness of the benefits of wearable devices.

- The demand for wearable sensors in the Rest of Asia-Pacific has steadily increased over the past few years, driven by a growing interest in fitness and wellness, a rising aging population, and advancements in technology and healthcare.

- According to the ASEAN Post, nursing homes are not enough to meet the ever-growing aged population. The services provided at these homes are also inadequate, impacting the quality of life and creating isolation among residents. Property developers are also considering the issue of an aging society when creating housing for urban dwellers, thus presenting an untapped potential market for wearable sensors.

Wearable Sensors Industry Overview

The wearable sensors market is competitive with the presence of major players like STMicroelectronics NV, Texas Instruments Incorporated, Infineon Technologies AG, Analog Devices Inc., and InvenSense Inc. (TDK Corporation). Players in the market are adopting strategies such as partnerships, collaborations, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2022 - Analog Devices Inc. collaborated with Oregon Health & Science University (OHSU) to develop a smartwatch that detects key mental health indicators to help address the rising mental health crisis in teens. As per the collaboration on the first and one-of-a-kind project, OHSU would leverage ADI's innovative technology and products for the burgeoning worldwide mental health crisis to save, improve, and enrich human lives.

- December 2022 - Panasonic Industries introduced a new member of its famous Grid-Eye sensor family with a 90° lens that provides a broader field of vision (FoV) and reduces the number of sensors needed to cover a given area, enabling people to count and track applications. Grid-Eye 90° will improve systems built to track and count the movement of individuals as well as other applications. Privacy-conscious designers have praised the Grid-Eye family's 64-pixel resolution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Awareness of Health and Fitness

- 5.1.2 Increasing Trend of Smart Wearable Devices

- 5.2 Market Challenges

- 5.2.1 Higher Costs Associated with Gadgets

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Chemical and Gas

- 6.1.2 Pressure

- 6.1.3 Image/Optical

- 6.1.4 Motion

- 6.1.5 Other Types of Sensors

- 6.2 By Application

- 6.2.1 Health and Wellness

- 6.2.2 Safety Monitoring

- 6.2.3 Sports and Fitness

- 6.2.4 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 STMicroelectronics NV

- 7.1.2 Texas Instruments Incorporated

- 7.1.3 Infineon Technologies AG

- 7.1.4 Analog Devices Inc.

- 7.1.5 InvenSense Inc. (TDK Corporation)

- 7.1.6 AMS OSRAM AG

- 7.1.7 Panasonic Corporation

- 7.1.8 NXP Semiconductors NV

- 7.1.9 TE Connectivity Ltd

- 7.1.10 Bosch Sensortec GmbH (Robert Bosch GmbH)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

穿戴式装置市场中的 HMI 感测器,按感测器类型、穿戴式装置类型、应用、技术、国家和地区划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

穿戴式装置市场中的 HMI 感测器,按感测器类型、穿戴式装置类型、应用、技术、国家和地区划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 穿戴式装置中的 HMI 感测器市场规模、份额、趋势分析报告:按感测器类型、装置类型、应用、最终用途、地区、细分市场预测,2025 年至 2030 年

穿戴式装置中的 HMI 感测器市场规模、份额、趋势分析报告:按感测器类型、装置类型、应用、最终用途、地区、细分市场预测,2025 年至 2030 年 2026 年至 2032 年穿戴式感测器市场类型、装置、应用和地区分布

2026 年至 2032 年穿戴式感测器市场类型、装置、应用和地区分布 穿戴式感测器市场规模、份额和成长分析(按应用、感测器类型、最终用户、外形规格和地区)- 产业预测 2025-2032

穿戴式感测器市场规模、份额和成长分析(按应用、感测器类型、最终用户、外形规格和地区)- 产业预测 2025-2032 中东和非洲穿戴式感测器市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)北美穿戴式感测器:市场占有率分析、产业趋势和成长预测(2025-2030)拉丁美洲穿戴式感测器:市场占有率分析、产业趋势、产业趋势、成长预测(2025-2030)欧洲穿戴式感测器 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)美国穿戴式感测器:市场占有率分析、产业趋势、成长预测(2025-2030)

中东和非洲穿戴式感测器市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)北美穿戴式感测器:市场占有率分析、产业趋势和成长预测(2025-2030)拉丁美洲穿戴式感测器:市场占有率分析、产业趋势、产业趋势、成长预测(2025-2030)欧洲穿戴式感测器 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)美国穿戴式感测器:市场占有率分析、产业趋势、成长预测(2025-2030) 穿戴式感测器市场,规模,占有率,趋势,行业分析报告:按感测器类型、技术、设备、最终用户、地区 - 2025-2034 年市场预测

穿戴式感测器市场,规模,占有率,趋势,行业分析报告:按感测器类型、技术、设备、最终用户、地区 - 2025-2034 年市场预测