|

市场调查报告书

商品编码

1687351

东协商用车:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)ASEAN Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

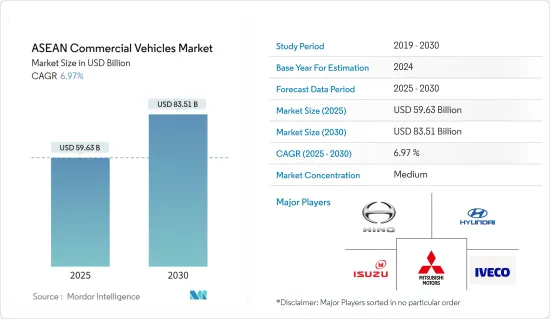

2025年东协商用车市场规模预估为596.3亿美元,预估至2030年将达835.1亿美元,预测期间(2025-2030年)复合年增长率为6.97%。

随着基础设施建设的改善、电子商务活动的增加对物流车辆的需求以及该地区电子商务热潮带来的经济復苏,东协商用车市场预计将在 2023 年实现强劲成长。快速的都市化和大规模货物运输的需求改善了市场条件。

从长远来看,严格的车辆排放法规、车辆安全性的提高、新车采用ADAS(驾驶辅助系统)以及东协零售和电子商务领域物流的快速成长预计将主要推动对新型和先进商用车的需求。随着物流和电子商务行业的快速扩张,对轻型商用车的需求预计会增加。

东协各国政府都在向汽车製造商施压,要求他们减少燃烧柴油产生的碳排放并解决温室气体排放,迫使OEM投资开发电动卡车。

自1998年以来,泰国污染控制部(PCD)要求所有新型重型卡车必须符合欧盟6排放标准,以抑制车辆污染。这刺激了人们对新型改装商用车的购买。

整体而言,由于经济发展、私人消费以及持续的排放气体相关政策调整,预测期内东协商用车市场预计将持续成长。

东协商用车市场趋势

轻型商用车市场占据主导地位

- 轻型商用车主要用于近距离运输。电子商务导致的商品需求不断增长,推动了轻型商用车在物流领域的应用,为市场成长铺平了道路。众多电商、物流公司纷纷进入东协地区,带动当地商用车市场发展。因此,该地区的主要企业正在以更低的价格推出改良产品来提高销售量。

- 在道路狭窄、交通拥挤的东南亚国协都市区中,小型车辆被证明能够帮助无缝应对这些基础设施挑战。

- 此外,轻型商用车在采集费用和营运成本方面都具有成本效益,这对该地区的中小企业 (SME) 和新创新兴企业来说提案。认识到这一潜力,一些东协政府正在积极实施政策,包括税收优惠和贷款计划,以鼓励企业采用轻型商用车。

- 总体而言,轻型商用车正在成为东协地区最主要的商用车型,这与城市经济状况和青睐较小、更灵活的交通工具的经营模式一致。

印尼的复合年增长率最高

近年来,印尼已崛起成为东协商用车市场的领先国家。这种成长归功于几个关键因素。

中国强劲的经济成长和日益发展的基础建设正推动各领域对商用车的庞大需求。政府雄心勃勃的基础设施建设计划,包括建造新的收费公路、港口和交通枢纽,需要部署大型重型卡车和工程车辆。

此外,印尼快速发展的物流和电子商务行业极大地推动了对轻型商用车(LCV)的需求,以促进最后一英里的交付。此外,印尼的商用车市场也受惠于政府旨在促进国内製造和汽车普及的优惠政策。

此外,印尼致力于实现主要经济体能源与气候论坛 (MEF) 的目标,即到 2030 年使全球中型和重型汽车销售的 30% 成为零排放汽车 (ZEV)。这项承诺反映了印尼对交通运输领域永续性和碳中和的关注。

印尼市场的主要企业正在加快引进创新和先进的商用车,以满足该国的需求。

- 2023 年 8 月,三菱扶桑卡客车公司宣布将在印尼推出全电动式eCanter 卡车。 eCanter 配备了电力传动系统,零排放气体,噪音极小,预计将为改善雅加达的生活品质做出贡献。

东协商用车产业概况

东协商用车市场处于中等整合状态,仅有少数几家企业占据明显的市场主导地位。东协商用车市场的主要企业包括丰田汽车公司、五十铃汽车公司、工业和日野汽车公司。合资企业、伙伴关係、工业部门不断增长的需求以及新兴国家的政府发展计划等因素显着推动了这一市场的发展。

例如,2022 年 9 月,Nex Point PLC (NEX) 宣布将与 Energy Absolute (EA) PCL 合作建立泰国首家商用电动车製造和组装工厂 Absolute Assembly (AAB),年生产能力高达 9,000 辆。该公司订单,其中200辆已成功交付。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 基础设施支出和贸易活动增加

- 市场限制

- 满足严格的汽车废气排放法规是一项挑战

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按车型

- 轻型商用车

- 中型商用车

- 重型商用车

- 透过推进力

- 内燃机

- 纯电动车

- 插电式混合动力汽车

- 燃料电池电动车

- 按国家

- 印尼

- 泰国

- 越南

- 新加坡

- 马来西亚

- 菲律宾

- 其他东南亚国协

第六章 竞争格局

- 供应商市场占有率

- 公司简介

- Isuzu Motors Limited

- Mitsubishi Motors Corporation

- Honda Motor Co. Ltd

- Daihatsu Motor Co. Ltd

- Ford Motor Company

- UD Trucks Corp.

- Scania

- FCA US LLC

- Hyundai Motor Company

- IVECO

- Hino Motors Ltd

- Tata Motors

第七章 市场机会与未来趋势

- 随着物流和电子商务行业的快速扩张,对轻型商用车的需求预计将增加

第八章商用车区域法规分析

The ASEAN Commercial Vehicles Market size is estimated at USD 59.63 billion in 2025, and is expected to reach USD 83.51 billion by 2030, at a CAGR of 6.97% during the forecast period (2025-2030).

The ASEAN commercial vehicle market saw robust growth in 2023, driven by rising infrastructure development, an increase in e-commerce activities requiring more logistics vehicles, and economic recovery from the COVID-19 pandemic in the region. Rapid urbanization and the need for mass material movement improved the market conditions.

Over the long term, stringent vehicle emission regulations, advancements in vehicle safety, the introduction of driver-assist systems in new vehicles, and rapidly growing logistics in the retail and e-commerce sectors across ASEAN are primarily expected to drive demand for new and advanced commercial vehicles. LCV demand is expected to rise as the logistics and e-commerce industries expand rapidly.

Governments throughout the ASEAN region are putting pressure on vehicle manufacturers to reduce carbon emissions from diesel fuel combustion and address greenhouse gas emissions, compelling OEMs to invest in developing electric trucks.

As per regulations of the Pollution Control Department (PCD) in Thailand since 1998, all new heavy trucks must meet Euro 6 emission standards to curb vehicular pollution. This spurred purchases of newer, compliant commercial vehicles.

Overall, the ASEAN commercial vehicle market is projected to continue its growth curve during the forecast period owing to economic development, consumer spending, and ongoing policy adjustments related to emissions.

ASEAN Commercial Vehicles Market Trends

Light Commercial Vehicle Segment Dominates the Market

- Light commercial vehicles are mainly used to transport goods over short distances. The increased demand for goods via e-commerce is driving the use of LCV in logistics, paving the way for the market's growth. Many e-commerce and logistics companies are expanding in the ASEAN region, driving the commercial vehicles market in the region. Thus, key players in the region are coming up with revised products at lower prices to improve sales.

- With urban areas across ASEAN nations grappling with narrow streets and traffic congestion, these compact vehicles have proven instrumental in navigating such infrastructural challenges seamlessly.

- Moreover, the cost advantages associated with LCVs, both in terms of acquisition and operational expenses, have rendered them an attractive proposition for small and medium-sized enterprises (SMEs) and start-ups operating in the region. Recognizing their potential, several ASEAN governments have proactively implemented policies, such as tax incentives and lending programs, to stimulate LCV adoption among businesses.

- Overall, LCVs emerge as the preeminent commercial vehicle type in the ASEAN region, aligning with the urban economic landscape and business models that favor smaller, more agile modes of transportation.

Indonesia to Register Highest CAGR

Indonesia has emerged as the leading nation in the ASEAN commercial vehicle market in recent years. This growth can be attributed to several key factors.

The nation's robust economic growth and increasing infrastructure development have fueled significant demand for commercial vehicles across various segments. The government's ambitious infrastructure push, including the construction of new toll roads, ports, and transportation hubs, has necessitated the deployment of a vast array of heavy-duty trucks and construction vehicles.

Furthermore, Indonesia's burgeoning logistics and e-commerce sectors have driven substantial demand for light commercial vehicles (LCVs) to facilitate last-mile deliveries. Additionally, Indonesia's commercial vehicle market has also benefited from favorable government policies aimed at promoting domestic manufacturing and vehicle adoption.

Moreover, Indonesia has also pledged to the Major Economies Forum on Energy and Climate (MEF) objective of achieving 30% of global medium and heavy-duty vehicle sales as zero-emission vehicles (ZEVs) by 2030. This commitment reflects the country's focus on sustainability and carbon neutrality in its transportation sector.

The key players operating in the Indonesian market are increasingly launching innovative and advanced commercial vehicles to cater to the country's requirements.

- In August 2023, Mitsubishi Fuso Truck and Bus Corporation announced the launch of its all-electric eCanter trucks in Indonesia. The eCanter, with its locally emission-free and nearly noiseless electric drivetrain, is expected to contribute to a better quality of life in Jakarta.

ASEAN Commercial Vehicles Industry Overview

The ASEAN commercial vehicle market is moderately consolidated, with few players having a significant hold of the market. Some of the key players in the ASEAN commercial vehicles market are Toyota Motor Corporation, ISUZU, Mitsubishi Motor Corporation, and Hino Motors. The market studied is highly driven by factors like joint ventures, partnerships, and growing demand from the industrial sector and government development initiatives across ASEAN countries.

For instance, in September 2022, Nex Point PLC (NEX) announced a collaboration with Energy Absolute (EA) PCL to establish Thailand's first commercial EV manufacturing and assembly plant, Absolute Assembly Co. Ltd (AAB), with an annual production capacity of up to 9,000 cars. The company received orders to produce 3,195 electric buses, with 200 units successfully delivered.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Higher Infrastructure Spending and Trade Activities

- 4.2 Market Restraints

- 4.2.1 Complying to the Stringent Vehicle Emission Regulations is a Challenge

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value and Volume)

- 5.1 By Vehicle Type

- 5.1.1 Light Commercial Vehicles

- 5.1.2 Medium-duty Commercial Vehicles

- 5.1.3 Heavy-duty Commercial Vehicles

- 5.2 By Propulsion

- 5.2.1 Internal Combustion Engine

- 5.2.2 Battery Electric Vehicle

- 5.2.3 Plug-in Hybrid Electric Vehicle

- 5.2.4 Fuel Cell Electric Vehicle

- 5.3 By Country

- 5.3.1 Indonesia

- 5.3.2 Thailand

- 5.3.3 Vietnam

- 5.3.4 Singapore

- 5.3.5 Malaysia

- 5.3.6 Philippines

- 5.3.7 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Isuzu Motors Limited

- 6.2.2 Mitsubishi Motors Corporation

- 6.2.3 Honda Motor Co. Ltd

- 6.2.4 Daihatsu Motor Co. Ltd

- 6.2.5 Ford Motor Company

- 6.2.6 UD Trucks Corp.

- 6.2.7 Scania

- 6.2.8 FCA US LLC

- 6.2.9 Hyundai Motor Company

- 6.2.10 IVECO

- 6.2.11 Hino Motors Ltd

- 6.2.12 Tata Motors

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 LCV Demand is Expected to Rise as the Logistics and E-Commerce Industries Expand Rapidly

8 ANALYSIS OF REGIONAL REGULATORY COMPLIANCES REGARDING COMMERCIAL VEHICLES

2025年全球商用车市场报告

2025年全球商用车市场报告 2025-2029年全球商用车市场

2025-2029年全球商用车市场 2025 年至 2033 年商用车市场规模、份额、趋势及预测(按车型、推进类型、最终用途和地区划分)2025 年至 2033 年日本商用车市场报告,按车辆类型(客车、重型商用卡车、轻型商用皮卡、轻型商用厢式货车、中型商用卡车)、发动机类型(混合动力和电动车、内燃机)和地区划分

2025 年至 2033 年商用车市场规模、份额、趋势及预测(按车型、推进类型、最终用途和地区划分)2025 年至 2033 年日本商用车市场报告,按车辆类型(客车、重型商用卡车、轻型商用皮卡、轻型商用厢式货车、中型商用卡车)、发动机类型(混合动力和电动车、内燃机)和地区划分 商用车市场:按类型、燃料类型、推进系统、变速箱类型、最终用途、分销管道 - 2025-2030 年全球预测

商用车市场:按类型、燃料类型、推进系统、变速箱类型、最终用途、分销管道 - 2025-2030 年全球预测 商用车市场:依产品、最终用途及地区划分

商用车市场:依产品、最终用途及地区划分 亚太商用车:市场占有率分析、产业趋势与成长预测(2025-2030 年)印度商用车市场:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)商用车-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)日本商用车市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

亚太商用车:市场占有率分析、产业趋势与成长预测(2025-2030 年)印度商用车市场:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)商用车-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)日本商用车市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)