|

市场调查报告书

商品编码

1687470

RF GaN-市场占有率分析、产业趋势与统计、成长预测(2025-2030)RF GaN - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

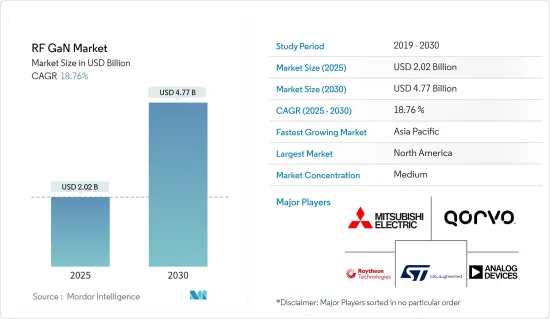

预计 2025 年 RF GaN 市场规模为 20.2 亿美元,预计 2030 年将达到 47.7 亿美元,在市场估计和预测期(2025-2030 年)内复合年增长率为 18.76%。

随着越来越多的行业采用物联网 (IoT) 技术,在广泛的即时连接设备和应用中使用 RF GaN 的优势预计将推动市场的成长。随着 GaN 技术的不断发展,GaN 在更复杂的应用中能够实现更高的频率,例如相位阵列、雷达、有线电视 (CATV)、甚小孔径终端 (VSAT) 和国防通讯的基地台收发器。

主要亮点

- RF GaN 在无线基础设施中发挥着至关重要的作用,它可以提高效率并增加频宽以支援不断增长的资料传输。 RF GaN 市场将主要受到 5G 日益普及和无线通讯进步的推动。电讯营运商也可能受益于 GaN 功率电晶体的使用增加。

- 电动车对射频 GaN 的采用日益增多也是推动该市场需求的主要因素之一。碳化硅元件用于电动公车、计程车、货车和乘用车的车载电池充电器。此外,政府对电动车市场的支持立法不断增加也刺激了射频 GaN 市场的需求。

- 自动驾驶汽车和无人机发展所需的基础设施也是推动RF GaN技术需求的因素之一。因此,预计在预测期内,自动驾驶汽车和无人机在各种应用(尤其是军事和国防应用)中的采用和发展将进一步增加 RF GaN 设备的采用。

- GaN 固有的材料优势也带来了一些相关的製造挑战,包括成本以及装置加工和封装的最佳化。为了扩大这些设备的采用,需要解决其他问题,包括电荷捕获和电流崩塌。儘管基于 GaN 的射频 (RF) 装置已经有了显着的改进(性能和产量比率),但仍有几个障碍阻碍 GaN-on-SiC(碳化硅上氮化镓)进入主流应用(即无线通讯基地台和 CATV)。

- 新冠疫情影响了供应链和电讯业。新冠疫情影响了供应链和通讯业,严重阻碍了通讯领域5G的推广。预计消费者将在此次危机期间继续使用行动电话,但大多数人可能无法进一步投资于仍处于起步阶段的技术。

- 资料消费的迅猛增长推动了商业网路的成长,并鼓励网路供应商采用 4G 和 5G 等下一代网路。根据思科可视化网路指数,预计到 2022 年全球行动资料流程量将以 46% 的复合年增长率成长,达到每月 77.5 Exabyte。

- 世界各地的组织都在创新产品并扩展业务。例如,2022 年 6 月,创新射频和微波功率解决方案供应商 Integra 宣布已开始向美国和欧洲客户出货其突破性的 100V RF GaN 技术。该公司还宣布将扩大其 100V RF GaN产品系列,推出七款新产品,单一电晶体可提供高达 5kW 的功率水平,适用于航空电子、定向能、电子战、雷达和科学市场。

高频氮化镓市场趋势

5G实施进展带动通讯基础设施领域需求强劲

- 通讯业作为全球数位化的关键驱动力和市场环境全面变化的产业,被视为数位转型技术的主要用户。通讯业对互通性和技术的投资正在推动全球经济中资本和资讯流的模式转移,为各产业全新经营模式的出现奠定了基础。

- 5G技术可望改变各种宽频服务的格局,并增强各种终端用户的垂直连接。推动 GaN市场占有率的主要因素是行动用户、线上视讯内容串流、5G 基础设施以及利用 5G 的各种物联网应用的成长。 5G可望支援多种场景的多种业务及相关服务需求。

- 目前,5G行动用户数估值为42万,预计到2022年将达到4亿人。随着全球5G技术部署的显着增加,预计对RF GaN技术的需求将会增加。

- 2022 年 5 月,义法半导体 (ST) 和通讯、工业、国防和资料中心产业半导体产品供应商 MACOM Technology Solutions Holdings (MACOM) 宣布生产硅基射频 GaN 原型。凭藉着此次成功,ST 和 MACOM 很高兴能继续并扩大合作。 ST 和 MACOM 正在开发的 GaN-on-Si 技术预计在整合到标准半导体製程流程时将提供具有竞争力的性能和显着的规模经济。

- Qorvo 是 2G、3G 和 4G基地台製造商 RF 解决方案的主要供应商之一。 Qorvo 在市场上具有独特的优势,支援 6GHz 以下和 cmWave/mmWave 无线基础架构的开发。为了实现 5G,Qorvo 正在投资并提供涵盖相关 5G 频段(包括 3.5、4.8、28 和 39 GHz)的产品解决方案来服务市场。

- 5G 基础设施需要高密度、小型天线阵列,这给射频 (RF) 系统的电源和温度控管带来了重大挑战。 GaN 装置凭藉其改进的宽频性能、效率和功率密度,提供了能够应对这些挑战的更紧凑的解决方案的潜力。

预计亚太地区将出现显着成长

- 亚太离散半导体市场以中国大陆、日本、台湾和韩国为主导,约占全球离散半导体市场的65%。相较之下,越南、泰国、马来西亚和新加坡等其他司法管辖区也为该地区的市场主导地位做出了贡献。

- 根据印度电子和半导体协会的数据,印度半导体元件市场预计将实现 10.1% 的复合年增长率(2018-2025),到 2025 年达到 323.5 亿美元。该国是全球研发中心的重要目的地。因此,印度政府正在进行的「印度製造」倡议预计将为半导体市场带来大量投资。印度政府的此类倡议可能会推动射频 GaN 市场的发展。

- 2022年2月,氮化镓积体电路(IC)供应商纳微半导体(Navitas Semiconductor)宣布参加中国国际金融股份有限公司(CICC)投资者会议。该公司专有的 GaN 功率 IC 将 GaN 功率与 GaN 驱动、控制和保护整合在单一 SMT 封装中。这些市场参与企业将推动该地区的 GaN 市场的发展。

- 由于投资者对支持 5G 技术的基础设施建设的兴趣增加,预计全部区域对 RF GaN 的需求将会增加。例如,根据GSMA的预测,到2025年,亚太地区行动电话营运商预计将花费超过4,000亿美元,其中3,310亿美元将用于5G部署。

- 随着中国经济从製造业主导向创新主导转型,中国射频 GaN 公司的成长是更广泛趋势的一部分。中国市场对商业无线通讯应用的需求正在激增,中国企业已开始开发下一代通讯网路。

- 此外,2021 年 12 月,印度理工学院坎普尔分校的研究人员开发了一种高性能、行业标准的铝氮化镓 (AlGaN)高电子移动性电晶体(HEMT) 模型。该模型提供了一种简单的设计方法,可用于製造高功率射频电路。射频电路包括用于无线传输的放大器和开关,可用于航太和国防应用。研究人员的持续技术创新有望推动该地区射频 GaN 市场的成长。

高频氮化镓产业概况

由于雷神科技公司、意法半导体微电子公司等主要企业的存在,RF GaN 市场竞争非常激烈。持续的创新使他们比其他人拥有竞争优势。透过研发、策略伙伴关係和併购,这些公司在市场上确立了强势地位。

2022 年 6 月,Qorvo,一家致力于连接世界的创新 RF 解决方案的知名供应商,被美国国防部 (DoD) 选中,推动国内最先进 (SOTA) RF GaN 计划的高级集成互连和蓝图,也称为 STARRY NITE,作为国防部研究与工程副部长办公室 (OUSD R&E) 微电子路线的一部分。该计划旨在开发和完善国内开放的 SOTA RF GaN 代工厂,以与国防部先进封装生态系统保持一致。

2022 年 5 月,义法半导体和工业、通讯、国防和资料中心产业半导体产品的主要供应商 MACOM Technology Solutions Holdings Inc. 宣布成功生产硅基射频氮化镓原型。凭藉这一成就,ST 和 MACOM 将继续合作并加强彼此关係。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 技术简介

- COVID-19 产业影响评估

第五章市场动态

- 市场驱动因素

- 5G实施进展带动通讯基础设施领域需求强劲

- 高性能、小外形规格等优势特性

- 市场限制

- 成本和营运挑战

第六章市场区隔

- 按应用

- 军队

- 通讯基础设施(回程传输、RRH、大规模MIMO、小型基地台)

- 卫星通讯

- 有线宽频

- 商用雷达和航空电子设备

- 射频能量

- 依材料类型

- GaN-on-Si

- GaN-on-SiC

- 其他材料类型(GaN-on-GaN、GaN-on-Diamond)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

第七章竞争格局

- 公司简介

- Aethercomm Inc.

- Analog Devices Inc.

- Wolfspeed Inc.(Cree Inc.)

- Integra Technologies Inc.

- MACOM Technology Solutions Holdings Inc.

- Microsemi Corporation(Microchip Technology Incorporated)

- Mitsubishi Electric Corporation

- NXP Semiconductors NV

- Qorvo Inc.

- STMicroelectronics NV

- Sumitomo Electric Device Innovations Inc.

- HRL Laboratories

- Raytheon Technologies

- Mercury Systems, Inc

第八章投资分析

第九章 市场机会与未来趋势

The RF GaN Market size is estimated at USD 2.02 billion in 2025, and is expected to reach USD 4.77 billion by 2030, at a CAGR of 18.76% during the forecast period (2025-2030).

Due to the benefits of RF GaN usage across a wide range of real-time linked devices and applications, more industries are expected to use the Internet of Things (IoT) technology, which is expected to drive market growth. With the continuously evolving GaN technology, GaN enables higher frequencies in more complex applications, such as phased arrays, radar, and base transceiver stations for cable TV (CATV), very small aperture terminal (VSAT), and defense communications.

Key Highlights

- RF GaN plays a key role in wireless infrastructure, improving efficiency and expanding bandwidth to support ever-increasing data transmission speeds. The market for RF GaN is primarily driven by increasing 5G adoption and advances in wireless communications. Telecom operators could also benefit from increased use of GaN power transistors.

- The increasing adoption of RF GaN in electric automotive is also one of the major factors driving demand in this market. Silicon carbide devices are used in the onboard battery chargers of electric buses, taxis, lorries, and passenger cars. Further, increasing government laws favoring the electric vehicles market stimulates demand in the RF GaN market.

- The infrastructure needed to create autonomous vehicles and drones is another factor that increases demand for RF GaN technologies. Hence, growth in the adoption and development of autonomous vehicles and drones for various applications, especially military and defense, is expected to increase further the adoption of RF GaN devices over the forecast period.

- The inherent material advantages of GaN come with some associated manufacturing challenges that include the cost and optimization of device processing and packaging. Other issues include charge trapping and current collapse, which need to be resolved for increased adoption of these devices. Although significant improvements have been made in RF GaN-based devices (performance and yields), there are still some barriers preventing the gallium nitride on silicon carbide (GaN-on-SiC) from entering mainstream applications (i.e., in wireless telecom base-stations or CATV).

- The COVID-19 pandemic impacted supply lines and the telecoms industry. It considerably hindered the penetration of 5G in the telecommunications sector. In this critical situation, consumers are expected to continue using mobile phones, but most of them may not be able to invest more in a technology that is still in a nascent stage.

- Rapidly increasing data consumption has resulted in the growth of commercial networks and is encouraging network providers to adopt next-generation networks, such as 4G and 5G. According to the Cisco Visual Networking Index, global mobile data traffic is expected to register a CAGR of 46%, reaching 77.5 exabytes per month by 2022.

- Organizations across the world are innovating new products and expanding their business. For instance, in June 2022, Integra, a provider of innovative RF and microwave power solutions, announced that it had begun shipping its breakthrough 100V RF GaN technology to customers in the United States and Europe. The company also announced the expansion of its 100V RF GaN product portfolio with the launch of seven new products for the avionics, directed energy, electronic warfare, radar, and scientific market segments, delivering power levels of up to 5kW in a single transistor.

Radiofrequency Gallium Nitride Market Trends

Strong Demand from Telecom Infrastructure Segment Driven by Advancements in 5G Implementation

- As a primary driver of global digitization and an industry undergoing comprehensive changes in the market environment, the telecommunications industry is regarded as a major user of digital transformation technologies. The telecommunications industry's investment in interoperability and technology has facilitated a paradigm shift in the flow of capital and information throughout the global economy, providing the building blocks for the emergence of entirely new business models across the industry.

- The 5G technology is expected to revolutionize the domain of various broadband services and empower connectivity across different end-user verticals. The major factors boosting the market share of GaN are increasing mobile subscriptions, streaming of online video content, 5G infrastructure, and various IoT applications using 5G. 5G is anticipated to support different services and associated service requirements across multiple scenarios.

- Currently, the number of 5G mobile subscriptions is valued at 0.42 million, and it is expected to reach 400 million subscriptions by 2022. With the substantial growth in the rollouts of 5G technology globally, the demand for RF GaN technology is expected to increase.

- In May 2022, STMicroelectronics (ST) and MACOM Technology Solutions Holdings (MACOM), a supplier of semiconductor products for the telecommunications, industrial, defense, and data center industries, announced the production of RF GaN on silicon (RF Gan-on-Si) prototypes. With this success, ST and MACOM will continue to work together and expand their relationship. GaN-on-Si technology under development by ST and MACOM is anticipated to offer competitive performance and significant economies of scale enabled by integration into standard semiconductor process flows.

- Qorvo is one of the suppliers of RF solutions to the 2G, 3G, and 4G base station manufacturers. It is uniquely positioned in the market to support the development of sub-6 GHz and cmWave/mmWave wireless infrastructure. Qorvo has been investing in product solutions covering relevant 5G bands, such as 3.5, 4.8 and 28, and 39GHz, to service the market, mainly to enable 5G.

- The need for dense, small-scale antenna arrays in 5G infrastructure results in key challenges with power and thermal management in radio frequency (RF) systems. With their improved wideband performance, efficiency, and power density, GaN devices offer the potential for more compact solutions that can address these challenges.

Asia-Pacific is Expected to Experience Significant Growth

- The Asia-Pacific region's discrete semiconductor industry is driven by China, Japan, Taiwan, and South Korea, constituting around 65% of the global discrete semiconductor market. In contrast, others, like Vietnam, Thailand, Malaysia, and Singapore, contribute to the region's dominance in the market.

- According to the Electronics and Semiconductors Association of India,the Indian market for semiconductor components would register a 10.1% CAGR (2018-2025) to reach USD 32.35 billion by 2025. The country is a vital destination for global research and development centers. Therefore, the ongoing 'Make in India' initiative by the Government of India is expected to result in significant investment in the semiconductor market. Such initiatives by the government of India will leverage the RF GaN market.

- In February 2022, Navitas Semiconductor, a provider of GaN integrated circuits (ICs), announced its participation in the China International Capital Corporation Limited (CICC) Investor Conference. The company's proprietary GaN power IC integrates GaN power and GaN drive, control, and protection in a single SMT package. Such participation will leverage the GaN market in the region.

- Demand for RF GaN across the APAC region is expected to increase due to growing investor interest in developing infrastructure to support 5G technology. For instance, according to the GSMA, the Asia-Pacific mobile operator is expected to spend more than USD 400 billion by 2025, of which USD 331 billion will be expended on 5G deployments.

- The growth of RF GaN companies in China is part of a broader trend as the nation shifts from a manufacturing- to an innovation-driven economy. The Chinese market is witnessing an exploding demand for commercial wireless telecom applications, and Chinese companies are already developing next-gen telecom networks.

- Moreover, in December 2021, researchers from IIT Kanpur in India developed a high-performance, industry-standard model of aluminum GaN (AlGaN) high electron mobility transistor (HEMT). This model provides a simple design method that can be used to manufacture high-power RF circuits. RF circuits include amplifiers and switches used in wireless transmissions and are useful in aerospace and defense applications. Constant innovations by researchers will drive the market growth of RF GaN in the region.

Radiofrequency Gallium Nitride Industry Overview

The competitive rivalry among the players in the RF GaN market is high owing to the presence of some key players such as Raytheon Technologies, STM microelectronics, amongst others. Their ability to continually innovate their offerings has allowed them to gain a competitive advantage over other players. Through research and development, strategic partnerships, and mergers and acquisitions, these players have been able to gain a strong foothold in the market.

In June 2022, Qorvo, a prominent provider of innovative RF solutions that connect the world, was selected by the US Department of Defense (DoD) to proceed with the Advanced Integration Interconnection and Fabrication Growth for Domestic State-of-the-Art (SOTA) RF GaN program, also known as STARRY NITE, as part of the Office of Undersecretary of Defense Research & Engineering's (OUSD R&E) microelectronics roadmap. The program seeks to develop and mature domestic, open SOTA RF GaN foundries in alignment with the DoD's advanced packaging ecosystem.

In May 2022, STMicroelectronics and MACOM Technology Solutions Holdings Inc., a significant supplier of semiconductor products for the industrial, telecommunications, defense, and data center industries, announced the successful production of RF Gan on Silicon (RF Gan-on-Si) prototypes. With this achievement, ST and MACOM would continue to work together and enhance their relationship.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

- 4.5 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Strong Demand from Telecom Infrastructure Segment Driven by Advancements in 5G Implementation

- 5.1.2 Favorable Attributes Such As High-performance and Small Form Factor to

- 5.2 Market Restraints

- 5.2.1 Cost & Operational Challenges

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Military

- 6.1.2 Telecom Infrastructure (Backhaul, RRH, Massive MIMO, Small Cells)

- 6.1.3 Satellite Communication

- 6.1.4 Wired Broadband

- 6.1.5 Commercial Radar and Avionics

- 6.1.6 RF Energy

- 6.2 By Material Type

- 6.2.1 GaN-on-Si

- 6.2.2 GaN-on-SiC

- 6.2.3 Other Material Types (GaN-on-GaN, GaN-on-Diamond)

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Aethercomm Inc.

- 7.1.2 Analog Devices Inc.

- 7.1.3 Wolfspeed Inc. (Cree Inc.)

- 7.1.4 Integra Technologies Inc.

- 7.1.5 MACOM Technology Solutions Holdings Inc.

- 7.1.6 Microsemi Corporation (Microchip Technology Incorporated)

- 7.1.7 Mitsubishi Electric Corporation

- 7.1.8 NXP Semiconductors NV

- 7.1.9 Qorvo Inc.

- 7.1.10 STMicroelectronics NV

- 7.1.11 Sumitomo Electric Device Innovations Inc.

- 7.1.12 HRL Laboratories

- 7.1.13 Raytheon Technologies

- 7.1.14 Mercury Systems, Inc

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

GaN射频元件市场规模、份额和成长分析(按元件类型、应用、频宽、技术和地区划分)-产业预测(2026-2033年)

GaN射频元件市场规模、份额和成长分析(按元件类型、应用、频宽、技术和地区划分)-产业预测(2026-2033年) 射频氮化镓半导体市场-全球产业规模、份额、趋势、机会和预测,按材料、应用、最终用户、地区和竞争格局划分,2020-2030年预测

射频氮化镓半导体市场-全球产业规模、份额、趋势、机会和预测,按材料、应用、最终用户、地区和竞争格局划分,2020-2030年预测 射频氮化镓 (RF GaN) 市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测 (2024-2032)射频氮化镓(RF GaN)市场-2025-2030年预测

射频氮化镓 (RF GaN) 市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测 (2024-2032)射频氮化镓(RF GaN)市场-2025-2030年预测 射频氮化镓市场分析与预测(至2034年):类型、产品、服务、技术、组件、应用、材料类型、设备、最终用户与能力

射频氮化镓市场分析与预测(至2034年):类型、产品、服务、技术、组件、应用、材料类型、设备、最终用户与能力 氮化镓射频半导体装置:市场份额分析、产业趋势、统计数据和成长预测(2025-2030 年)

氮化镓射频半导体装置:市场份额分析、产业趋势、统计数据和成长预测(2025-2030 年) 全球通讯基础设施中 RF GAN 设备市场卫星通讯中 RF GAN 设备的全球市场

全球通讯基础设施中 RF GAN 设备市场卫星通讯中 RF GAN 设备的全球市场 2032 年 RF GaN 市场预测:按材料类型、装置类型、晶圆尺寸、应用、最终用户和地区进行的全球分析全球 GaN基板和 GaN 晶圆市场规模(按类型、应用、地区、范围和预测)

2032 年 RF GaN 市场预测:按材料类型、装置类型、晶圆尺寸、应用、最终用户和地区进行的全球分析全球 GaN基板和 GaN 晶圆市场规模(按类型、应用、地区、范围和预测)