|

市场调查报告书

商品编码

1687874

全球汽车物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Global Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

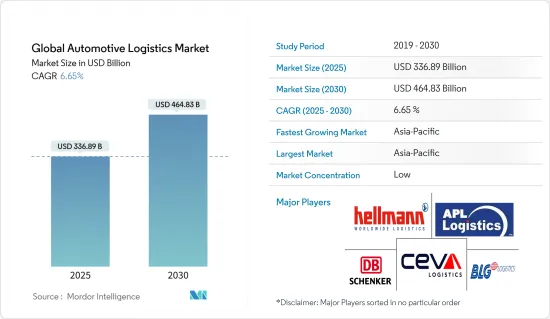

2025 年全球汽车物流市场规模估计为 3,368.9 亿美元,预计到 2030 年将达到 4,648.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.65%。

关键亮点

- 受全球汽车产量和销量不断增长的推动,全球汽车物流市场正在经历显着增长。这种扩张主要归因于新兴市场的需求不断增长、汽车行业的技术进步以及电子商务的激增。预测显示,在汽车製造全球化、向电动和自动驾驶汽车的转变以及全球供应链的持续演变的支持下,汽车产业将呈现稳定的成长轨迹。

- 汽车物流市场的成长与整个汽车产业的健康密切相关。随着汽车产量和销售量的增加,对高效物流解决方案的需求也随之成长。新兴市场在这一扩张中发挥关键作用,为物流供应商提供了新的机会。技术进步不仅增强了车辆的性能,而且还改变了物流业务,使其更有效率、更安全。向电动和自动驾驶汽车的转变正在带来新的物流挑战和机会,尤其是在处理专用零件和电池方面。此外,对永续性的关注正在鼓励公司采用更环保的物流实践,这也将节省成本并提高品牌声誉。

- 儘管如此,亚洲国家在汽车零件进口方面仍占据主导地位,占63%,其次是欧洲(27%)和北美(9%)。来自欧洲的进口量增加了 8%,来自北美的进口量增加了 2.5%,而来自亚洲的进口量则增加了 2%。此外,专注于售后服务和产品的售后市场部分在2024财年上半年大幅成长了7.5%,达到55亿美元。

- 印度汽车零件製造商在 2024 财年上半年的收益为 361 亿美元,主要受到汽车目标商标产品製造商 (OEM ) 强劲需求的推动。预计OEM需求的激增将成为汽车零件物流市场的主要动力。

- 物联网、人工智慧和区块链等技术的采用正在彻底改变供应链视觉性、优化营运并提高安全性和效率。例如,2023年5月,韩国贸易、工业和能源部承诺投入超过14兆韩元(110亿美元),与当地汽车製造商合作,加强国内汽车供应链,促进出口,并促进向下一代技术的过渡。

- 向电动车 (EV) 的转变和自动驾驶汽车的兴起正在重塑物流,并需要对零件和电池进行专门处理。同时,人们也越来越重视物流的环境永续性。越来越多的公司采用环保做法,例如优化运输路线、使用节能车辆和采用永续包装解决方案。

- 随着物流技术的不断创新,它将使供应链更有效率、透明和更具适应性。特别是亚太地区快速成长的市场预计将对全球汽车物流市场的扩张做出重大贡献。此外,向线上汽车销售的转变以及对客户体验的重视正在重塑物流策略和营运。

汽车物流市场的全球趋势

特定服务运输服务未来将占据最大市场占有率

- 车辆主要透过公路、铁路、海运和空运运输。由于即时追踪、RFID 技术和物联网设备等技术的进步,提高了供应链的可视性,预计道路产业将在全球市场上实现成长。

- 特别是在欧洲,低成本和智慧交通系统的引入正在刺激公路产业的发展。这些系统将促进先进的连接、车队行驶并为自动驾驶铺平道路。同时,在高效能港口服务和优质基础设施兴起的推动下,海运业可望大幅成长,进而降低企业、托运人和消费者的成本。

- 2023年12月,中国知名第三方汽车物流公司长久物流采取引人注目的倡议,承接上汽通用五菱的跨国道路运输。约500车陆续从柳州工厂出发,经中国新疆维吾尔自治区喀什口岸驶往乌兹别克塔什干。这种跨境道路运输因其速度快、成本效益高和灵活性而受到重视。在上汽通用五菱柳州工厂,长久物流团队精心将一辆五菱乘用车装载到开往乌兹别克的双层汽车运输拖车上。随着这项发展,亚太地区汽车物流市场将享有更大的跨境连通性和营运效率。

- 2023年5月,CEVA物流了横跨中国-吉尔吉斯斯坦-乌兹别克斯坦和中国-巴基斯坦走廊的新国际道路运输(TIR)路线,成为头条新闻。这些航线旨在加强贸易并造福该地区,并举行了剪綵仪式。这支由六辆卡车组成的车队满载着工业零件、汽车零件和消费品,从中国西部的喀什出发,进入吉尔吉斯斯坦,行驶约1100公里,抵达乌兹别克的撒马尔罕。该倡议将开闢新的贸易路线并促进物流业务,从而显着增强亚太汽车物流市场。

- 铁路客运2023财年1-3月汽车运输量较上年同期增加33%,达到约2.7万辆。

- 中央铁路公司报告称,2023 财年第一季火车车辆负载容量与 2022 财年同期相比大幅增加了 33%。

- 马恆达、塔塔汽车和马鲁蒂乌迪奥格等主要汽车製造商一直依赖铁路服务来满足其车辆运输需求。

- 2023 年 6 月,DMN 物流采取策略性措施收购 JLL 汽车分销,彰显其致力于加强电动车 (EV) 和通用汽车物流业务的决心。 JLL 汽车分销公司总部位于阿尔维彻奇,成立于 2010 年,是一家家族企业,专门提供精品和电动汽车运输服务,为 Inchcape、Autorola、奥迪和其他主要经销商集团和品牌等客户提供服务。

- 此外,JLL 汽车分销还为企业客户和经销商提供送货和车辆运输服务以及客户交接服务。 DMN 物流与 JLL 的董事总经理进行了讨论,最终达成了全面收购。此次收购充分利用了中国新兴OEM对打入英国汽车物流市场日益增长的兴趣。

亚太地区可望维持市场占有率

- 亚太地区包括中国、日本、印度和韩国,是世界汽车强国。汽车产销量的激增、汽车出口的良好趋势以及消费者对新车和二手车的需求不断增长,推动了市场的快速扩张。

- 电子商务的出现和网上汽车销售的快速成长正在重塑汽车物流。这种转变凸显了精简物流网路和创新最后一哩路交付解决方案的必要性。此外,人们对电动车日益增长的兴趣不仅改变了汽车产业,也彻底改变了物流。这包括专用零件和电池的复杂运输要求,为新颖的物流解决方案铺平了道路。

- 例如,2023年,中国汽车出口强劲。光是2023年12月,中国就售出了49.9万辆汽车。根据中国工业协会的资料,2023年中国汽车出口创下新纪录,飙涨57.9%,达491万辆。这一成长主要得益于新能源汽车出口的大幅成长,出口量激增 77.6%,超过 120 万辆。其中,纯电动汽车出口成长80.9%,混合动力汽车成长47.8%。

- 中国汽车整体市场销量与前一年同期比较增12%,突破3,000万辆大关。产量同样令人印象深刻,突破3000万辆,比2022年增长11.6%。新能源汽车发挥了重要作用,产销分别达到958万辆和949万辆,年比大幅增加35.8%和与前一年同期比较%。值得注意的是,到 2023 年,新能源汽车将占据 31.6% 的市场占有率。汽车出口和新能源汽车产量的成长极大地推动了亚太汽车物流市场的发展,促进了对高效运输和配送解决方案的需求。

- 汽车产业是日本经济的重要组成部分。丰田、本田、日产等全球大型公司不仅引领国内市场,在全球也占有重要地位。值得注意的是,汽车出口(主要是轿车)占日本出口总额的很大一部分,凸显了该产业在经济状况中所扮演的关键角色。根据日本海关的资料,2023年日本乘用车出口总量约527万辆,与前一年同期比较增加20%。这些出口额约为15.54兆日圆(1056.7亿美元)。展望2024年,日本汽车工业协会报告称,日本1月汽车出口量为295,133辆。其中,乘用车263981辆,货车22755辆,客车8397辆。高出口量需要先进的物流解决方案来管理车辆的有效运输,从而加强该地区的汽车物流市场。

- 印度是全球第三大汽车市场,汽车业对该国GDP的贡献率为7.1%。最近的一份报告也强调,该国在过去 14 年减少了 33% 的温室气体排放。

- 在汽车产业经历重大转型的同时,印度依然坚定地履行《联合国气候变迁公约》(UNFCCC)的承诺。依照全球永续性目标,我们的目标是到 2030 年将排放强度在 2005 年的基础上降低 45%。这项承诺加上汽车产业的成长,推动了对支持高效汽车和零件分销的创新物流解决方案的需求,从而进一步推动亚太汽车物流市场的发展。

全球汽车物流产业概览

汽车物流市场较为分散,有大型全球参与企业、中小型本地参与企业以及少数占据市场占有率的少数参与企业。大多数全球物流参与企业都设有汽车物流部门来满足市场需求。此外,本地参与企业在库存处理、服务提供、处理产品和技术方面的能力也日益增强。

市场上的第三方物流(3PL)服务供应商正在根据其可靠性和供应链能力展开激烈竞争。每家公司都试图透过提供高附加价值的服务来实现其服务的差异化。电子商务销售的兴起为物流公司在速度、配送等方面创造了机会和挑战。

拥有大量资产和资本资源的全球公司可以投资先进的技术和物流中心,以从上述场景中获益。同时,地区和本地参与企业正在提出更好的行业解决方案来满足製造商、零售商和经销商的需求。该行业的一些主要参与者包括 Hellmann Worldwide Logistics、APL Logistics、BLG Logistics Group、CEVA Logistics 和 DB Schenker。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

- 分析方法

- 研究阶段

第三章执行摘要

第四章 市场洞察

- 当前市场状况

- 产业价值链分析

- 政府法规和倡议

- 全球物流业(概况、LPI 评分、主要货运统计等)

- 聚焦全球汽车产业(概况、发展趋势、统计等)

- 聚焦-电子商务对传统汽车物流供应链的衝击

- 逆向物流的回顾与说明(概述、与正向物流的比较问题等)

- 深入了解汽车售后市场及其物流活动

- 物流与综合物流需求聚焦

- 地缘政治与疫情将如何影响市场

第五章市场动态

- 市场驱动因素

- 汽车产销售成长

- 电子商务与全通路物流

- 市场限制

- 供应链中断

- 基础设施限制

- 市场机会

- 技术创新

- 投资永续性计划

- 产业吸引力-波特五力分析

- 买家/消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第六章市场区隔

- 按服务

- 运输

- 仓储、配送和库存管理

- 其他的

- 按类型

- 整车

- 汽车零件

- 其他的

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 义大利

- 俄罗斯

- 法国

- 其他欧洲国家

- 拉丁美洲

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中东和非洲

- 南非

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东和非洲地区

- 亚太地区

第七章竞争格局

- 公司简介

- Hellmann Worldwide Logistics SE & Co. KG

- APL Logistics Ltd

- BLG Logistics Group AG & Co. KG

- CEVA Logistics

- DB Schenker

- DHL Group

- GEFCO SA

- Kerry Logistics Network Ltd

- Kuehne+Nagel International AG

- Penske Logistics Inc.

- Ryder System Inc.

- DSV Panalpina AS

- Expeditors

- Panalpina

- XPO Logistics Inc.

- Tiba Group

- Bollore Logistics

- CFR Rinkens*

- 其他公司

第八章:市场的未来

第九章 附录

- GDP 分布(依活动 - 主要国家)

- 资本流动洞察 – 主要国家

- 经济统计-运输和仓储业对经济的贡献(主要国家)

- 全球汽车产业统计数据

The Global Automotive Logistics Market size is estimated at USD 336.89 billion in 2025, and is expected to reach USD 464.83 billion by 2030, at a CAGR of 6.65% during the forecast period (2025-2030).

Key Highlights

- The global automotive logistics market is witnessing substantial growth, propelled by increased vehicle production and sales worldwide. This expansion is primarily fueled by heightened demand in emerging markets, technological advancements in the automotive sector, and the surge of e-commerce. Projections indicate a steady growth trajectory, underpinned by the globalization of automotive manufacturing, the pivot towards electric and autonomous vehicles, and the continual evolution of global supply chains.

- The automotive logistics market's growth is closely tied to the overall health of the automotive industry. As vehicle production and sales rise, the demand for efficient logistics solutions increases. Emerging markets are playing a crucial role in this expansion, offering new opportunities for logistics providers. Technological advancements are not only enhancing vehicle features but also transforming logistics operations, making them more efficient and secure. The shift towards electric and autonomous vehicles is creating new logistics challenges and opportunities, particularly in the handling of specialized components and batteries. Additionally, the emphasis on sustainability is driving companies to adopt greener logistics practices, which can also lead to cost savings and improved brand reputation.

- Despite this, Asian nations retained their dominance in auto components imports, accounting for 63%, with Europe at 27% and North America at 9%. While imports from Europe and North America saw modest growth rates of 8% and 2.5% respectively, those from Asia increased by a more conservative 2%. Furthermore, the aftermarket segment, focusing on post-sales services and products, saw a notable 7.5% expansion, reaching USD 5.5 billion in H1 FY24.

- India's auto parts manufacturers raked in a revenue of USD 36.1 billion in the first half of the 2024 fiscal year, largely driven by robust demand from automotive original equipment manufacturers (OEMs). This surge in demand from OEMs is poised to be a key driver for the auto components logistics market.

- Technological adoptions, such as IoT, AI, and blockchain, are revolutionizing supply chain visibility, operational optimization, and enhancing security and efficiency. For instance, in May 2023, South Korea's Ministry of Trade, Industry, and Energy, in collaboration with local automakers, pledged over KRW 14 trillion (USD 11 billion) to fortify the nation's automotive supply chain, boost exports, and facilitate the transition to next-gen technologies.

- The transition to electric vehicles (EVs) and the rise of autonomous vehicles are reshaping logistics, necessitating specialized handling of components and batteries. Simultaneously, there's a growing emphasis on environmental sustainability in logistics. Companies are increasingly adopting green practices, including optimizing transportation routes, using energy-efficient vehicles, and embracing sustainable packaging solutions.

- As logistics technology continues to innovate, it's poised to further enhance supply chain efficiency, transparency, and adaptability. The burgeoning markets, especially in the Asia-Pacific region, are set to be significant contributors to the global automotive logistics market's expansion. Moreover, the shift towards online vehicle sales and an amplified focus on customer experience are reshaping logistics strategies and operations.

Global Automotive Logistics Market Trends

By Service Transportation Service Occupies the Largest Market Share in the Future

- Automotive vehicles primarily utilize roadways, railways, maritime, and airways for transportation. The roadways segment is poised for global market growth, driven by advancements like real-time tracking, RFID technology, and IoT devices, enhancing supply chain visibility.

- Low costs and the adoption of intelligent transport systems, particularly in Europe, are fueling the roadways segment. These systems facilitate high-level connectivity, platooning, and pave the way for automated driving. Meanwhile, the maritime segment is set for significant growth, attributed to the rise of high-performing port services and quality infrastructure, which reduce costs for operators, shippers, and consumers.

- In a notable move in December 2023, Changjiu Logistics, a prominent third-party automotive logistics firm in China, took on SAIC-GM-Wuling's cross-border road transport. The journey saw nearly 500 vehicles leaving sequentially from Liuzhou plant, traveling from Kashgar port in Xinjiang, China, to Tashkent, Uzbekistan. This cross-border road transport is lauded for its speed, cost-efficiency, and flexibility. Changjiu Logistics' team meticulously handled operations at SAIC-GM-Wuling's Liuzhou plant, loading Wuling passenger cars onto double-deck car carrier trailers destined for Uzbekistan. This development boosts the automotive logistics market in the Asia-Pacific region by enhancing cross-border connectivity and operational efficiency.

- CEVA Logistics made headlines in May 2023 with the launch of new international road transport (TIR) routes spanning China-Kyrgyzstan-Uzbekistan and China-Pakistan corridors. These routes, aimed at bolstering trade and reaping regional benefits, were inaugurated with a ribbon-cutting ceremony. The convoy, comprising six trucks laden with industrial components, auto parts, and consumer goods, set off from Kashgar in western China, crossed into Kyrgyzstan, and successfully reached Samarkand in Uzbekistan after a journey of about 1,100 kilometers. This initiative significantly enhances the automotive logistics market in the Asia-Pacific region by opening new trade routes and facilitating smoother logistics operations.

- Central Railway saw a commendable 33% surge in car transportation, moving around 27,000 cars in the first three months of FY 2023, compared to the same period in FY 2022.

- Central Railway reported a significant uptick of 33% in car loading via trains in the first quarter of FY 2023, compared to the corresponding period in FY 2022.

- Leading automobile manufacturers like Mahindra & Mahindra, Tata Motors, and Maruti Udyog have been relying on railway services for their vehicle transportation needs.

- In a strategic move in June 2023, DMN Logistics acquired JLL Vehicle Distribution, emphasizing its commitment to bolstering its electric vehicle (EV) and general vehicle logistics operations. JLL Vehicle Distribution, based in Alvechurch and founded in 2010 as a family business, specializes in boutique and EV transport services, catering to clients like Inchcape, Autorola, and Audi, as well as other major dealer groups and brands.

- Besides, JLL Vehicle Distribution offers delivery and vehicle transfer services to corporate clients, dealers, and handles customer handovers. DMN Logistics initiated discussions with JLL's managing director, eventually culminating in a full acquisition. The acquisition is poised to capitalize on the growing interest from emerging Chinese OEMs eyeing expansion into the UK's vehicle logistics market.

Asia-Pacific is Poised to Maintain its Dominance in Market Share

- The Asia-Pacific region, encompassing countries like China, Japan, India, and South Korea, stands out as a global automotive powerhouse. This market's rapid expansion is fueled by surging vehicle production and sales, a buoyant trend in automotive exports, and an escalating appetite for both new and pre-owned vehicles among consumers.

- The advent of e-commerce and the surge in online vehicle sales are reshaping automotive logistics. This shift underscores the need for streamlined distribution networks and innovative last-mile delivery solutions. Additionally, the mounting interest in electric vehicles is not just transforming the automotive landscape but also revolutionizing logistics. This includes the intricate transportation requirements for specialized components and batteries, paving the way for novel logistics solutions.

- For example, in 2023, China's automotive exports painted a robust picture. In December 2023 alone, China shipped out a staggering 499,000 automobiles. Data from the China Association of Automobile Manufacturers (CAAM) revealed that China's auto exports hit a milestone in 2023, surging by 57.9% to a record 4.91 million vehicles. This surge was largely driven by a remarkable uptick in new energy vehicle (NEV) exports, which leaped by 77.6% to over 1.2 million units. Specifically, pure electric vehicle exports soared by 80.9%, while hybrid variants saw a 47.8% uptick.

- The broader auto market in China saw a 12% year-on-year sales increase, crossing the 30 million mark. Production figures were equally impressive, surpassing 30 million units, marking an 11.6% rise from 2022. NEVs played a significant role, with production and sales exceeding 9.58 million and 9.49 million units, respectively, marking a robust 35.8% and 37.9% year-on-year surge. Notably, NEVs captured a market share of 31.6% in 2023. This growth in automotive exports and NEV production significantly boosts the automotive logistics market in the Asia-Pacific region, driving demand for efficient transportation and distribution solutions.

- Japan's automotive sector is a cornerstone of its economy. Global giants like Toyota, Honda, and Nissan not only lead the domestic market but also command a significant presence worldwide. Notably, automotive exports, predominantly automobiles, make up a substantial portion of Japan's total exports, underscoring the sector's pivotal role in the nation's economic landscape. Data from Japan Customs for 2023 highlights that Japan exported around 5.27 million passenger cars, marking a robust 20% increase from the previous year. These exports were valued at approximately 15.54 trillion Japanese yen (USD 105.67 billion). Moving into 2024, January saw Japan exporting 295,133 motor vehicles, as reported by the Japan Automobile Manufacturers Association. The breakdown includes 263,981 passenger cars, 22,755 trucks, and 8,397 buses. The substantial volume of exports necessitates advanced logistics solutions to manage the efficient movement of vehicles, thereby enhancing the automotive logistics market in the region.

- India, the world's third-largest automotive market, sees its automotive sector contributing a notable 7.1% to the nation's GDP. Recent reports also highlight a commendable 33% reduction in the country's greenhouse gas emissions over the past 14 years.

- Amidst a sweeping transformation in the automotive landscape, India is steadfast in its commitment to the United Nations Convention on Climate Change (UNFCCC). The nation aims to slash emissions intensity by 45% from 2005 levels by 2030, aligning with global sustainability goals. This commitment, coupled with the growth of the automotive sector, drives the need for innovative logistics solutions to support the efficient distribution of vehicles and components, further boosting the automotive logistics market in the Asia-Pacific region.

Global Automotive Logistics Industry Overview

The automotive logistics market is fragmented in nature, with large global players, small- and medium-sized local players, and few players who occupy the market share. Most global logistics players have an automotive logistics division to meet the market needs and demand. Additionally, local players are increasingly enhancing their capabilities in terms of inventory handling, service offerings, products handled, and technology.

The third-party logistics (3PL) service providers in the market compete intensely based on reliability and supply chain capacity. By offering value-added services, companies would differentiate their service offerings. The growing e-commerce sales are creating opportunities and challenges for logistics firms in terms of speed, delivery, etc.

Global companies with high assets and capital can invest in advanced technology and distribution centers and benefit from the scenario mentioned above. On the other hand, regional and local players are coming up with better sector solutions to support the needs of manufacturers, retailers, as well as dealers. This industry's major players include Hellmann Worldwide Logistics, APL Logistics, BLG Logistics Group, CEVA Logistics, and DB Schenker.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Industry Value Chain Analysis

- 4.3 Government Regulations and Initiatives

- 4.4 Global Logistics Sector (Overview, LPI Scores, Key Freight Statistics, etc.)

- 4.5 Focus on the Global Automotive Industry (Overview, Development and Trends, Statistics, etc.)

- 4.6 Spotlight - Effect of E-commerce on Traditional Automotive Logistics Supply Chain

- 4.7 Review and Commentary on Reverse Logistics (Overview, Challenges in Comparison with Forwards Logistics, etc.)

- 4.8 Insights on Automotive Aftermarket and its Logistics Activities

- 4.9 Spotlight on the Demand for Contract Logistics and Integrated Logistics

- 4.10 Impact of Geopolitics and Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Vehicle Production and Sales

- 5.1.2 E-commerce and Omnichannel Distribution

- 5.2 Market Restraints

- 5.2.1 Supply Chain Disruptions

- 5.2.2 Infrastructure Limitations

- 5.3 Market Opportunities

- 5.3.1 Technological Innovations

- 5.3.2 Investing in Sustainability Initiatives

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Powers of Buyers/Consumers

- 5.4.2 Bargaining Power of Suppliers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Transportation

- 6.1.2 Warehousing, Distribution, and Inventory Management

- 6.1.3 Other Services

- 6.2 By Type

- 6.2.1 Finished Vehicle

- 6.2.2 Auto Components

- 6.2.3 Other Types

- 6.3 Geography

- 6.3.1 Asia-Pacific

- 6.3.1.1 China

- 6.3.1.2 Japan

- 6.3.1.3 India

- 6.3.1.4 South Korea

- 6.3.1.5 Rest of Asia-Pacific

- 6.3.2 North America

- 6.3.2.1 United States

- 6.3.2.2 Canada

- 6.3.2.3 Mexico

- 6.3.3 Europe

- 6.3.3.1 United Kingdom

- 6.3.3.2 Germany

- 6.3.3.3 Italy

- 6.3.3.4 Russia

- 6.3.3.5 France

- 6.3.3.6 Rest of Europe

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East & Africa

- 6.3.5.1 South Africa

- 6.3.5.2 United Arab Emirates

- 6.3.5.3 Saudi Arabia

- 6.3.5.4 Rest of Middle East & Africa

- 6.3.1 Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 Hellmann Worldwide Logistics SE & Co. KG

- 7.2.2 APL Logistics Ltd

- 7.2.3 BLG Logistics Group AG & Co. KG

- 7.2.4 CEVA Logistics

- 7.2.5 DB Schenker

- 7.2.6 DHL Group

- 7.2.7 GEFCO SA

- 7.2.8 Kerry Logistics Network Ltd

- 7.2.9 Kuehne + Nagel International AG

- 7.2.10 Penske Logistics Inc.

- 7.2.11 Ryder System Inc.

- 7.2.12 DSV Panalpina AS

- 7.2.13 Expeditors

- 7.2.14 Panalpina

- 7.2.15 XPO Logistics Inc.

- 7.2.16 Tiba Group

- 7.2.17 Bollore Logistics

- 7.2.18 CFR Rinkens*

- 7.3 Other Companies

8 FUTURE OF THE MARKET

9 APPENDIX

- 9.1 GDP Distribution (by Activity - Key Countries)

- 9.2 Insights on Capital Flows - Key Countries

- 9.3 Economic Statistics - Transport and Storage Sector, Contribution to Economy (Key Countries)

- 9.4 Global Automotive Industry Statistics

汽车物流市场按模式、服务类型、车辆类型和最终用户划分-2025-2032 年全球预测按类型、操作类型、控制模式、容量、安装类型、应用、最终用途产业和分销管道分類的厂内升降机市场 - 2025-2030 年全球预测

汽车物流市场按模式、服务类型、车辆类型和最终用户划分-2025-2032 年全球预测按类型、操作类型、控制模式、容量、安装类型、应用、最终用途产业和分销管道分類的厂内升降机市场 - 2025-2030 年全球预测 全球厂内物流市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测全球汽车物流市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球厂内物流市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测全球汽车物流市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 2025年全球汽车物流市场报告

2025年全球汽车物流市场报告 汽车物流市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、解决方案、模式汽车OEM厂内物流市场(按零件、服务模式类型、自动化程度、物流模式、汽车零件类型和最终用户划分)- 全球预测,2025 年至 2030 年

汽车物流市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、解决方案、模式汽车OEM厂内物流市场(按零件、服务模式类型、自动化程度、物流模式、汽车零件类型和最终用户划分)- 全球预测,2025 年至 2030 年 北美汽车物流:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

北美汽车物流:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 全球汽车物流市场:市场规模、份额、趋势分析(按类型、分布、活动和解决方案)、区域展望和未来预测(2024-2031 年)汽车物流市场规模、份额、趋势分析报告:按活动、类型、分布、物流解决方案、地区、细分市场、预测,2025-2030 年

全球汽车物流市场:市场规模、份额、趋势分析(按类型、分布、活动和解决方案)、区域展望和未来预测(2024-2031 年)汽车物流市场规模、份额、趋势分析报告:按活动、类型、分布、物流解决方案、地区、细分市场、预测,2025-2030 年