|

市场调查报告书

商品编码

1690722

北美汽车物流:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)North America Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

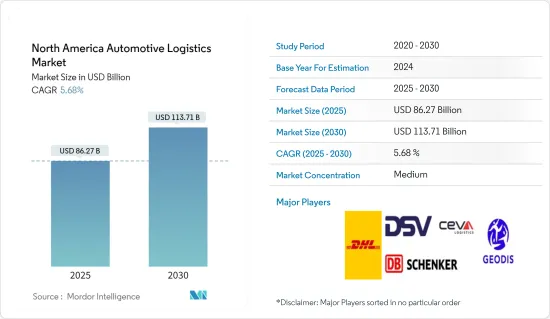

北美汽车物流市场规模预计在 2025 年为 862.7 亿美元,预计到 2030 年将达到 1,137.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.68%。

北美汽车物流从未像现在这样准备好迎接巨大的变革和机会。然而,与整个汽车产业一样,汽车物流的经济和贸易风险、新法规、消费行为和投资回报率几乎没有不不确定性。

凭藉前所未有的可视性和灵活性,汽车物流行业必须在竞争中保持领先。OEM、物流和技术提供者必须合作共用资料、制定计划和升级技术,以保持供应链高效流动。

汽车供应链的未来物流服务提供者以及从宏观层面来说整个经济都至关重要。汽车供应链结构的变化可能会影响全球贸易的性质和各国经济的动态。

全球汽车生产设施数量的不断增加正在推动汽车物流市场的成长。此外,随着汽车製造商为物流供应商创造巨大的商机,预计未来几年市场成长将会加速。自经济衰退以来,新兴经济体一直保持稳定成长,消费者的可支配收入增加。

北美汽车物流市场趋势

小型车生产需求

- 在北美,消费者的偏好正在转向运动型多功能车和卡车,汽车製造商正在增加产量以满足不断增长的需求。例如福特探险者 (Ford Explorer) 和雪佛兰 Silverado 等车款的受欢迎程度。

- 电动车产量的成长是由于人们对混合动力汽车和电动车的兴趣日益浓厚。例如,特斯拉的超级工厂于2023年12月在德克萨斯建成,旨在满足北美日益增长的电动车需求。

- 北美汽车产业正在调整和投资技术以满足更严格的排放法规,从而影响轻型车辆的设计和生产。 2022年8月,美国政府将签署具有历史意义的《通膨控制法案》,这可能是美国史上最重要的经济和气候相关法案。 《通膨削减法案》协助推动了美国製造业产能的復苏,为清洁能源技术的开发和生产提供了广泛的奖励。

- 随着小型车生产需求的增加,汽车物流公司的运输量将会增加。更多的车辆和零件必须从製造厂运送到配送中心和经销店。

美国电动车发展

- 联邦和州级的奖励对于电动车的广泛应用至关重要。联邦政府为购买符合条件的电动车提供税额扣抵。例如,合格插电式电动车信贷额度最高可达 7,500 美元。

- 各大汽车厂商也都在积极布置电动车。通用汽车和福特等公司已宣布投资电动车研发和生产的计画。 2024 年 1 月,福特马达与这家总部位于明尼苏达州的公司签署协议,购买 1,000 辆全电动汽车,具体为 F-150 Lightning 和 Mustang Mach-E。

- 2023 年前 11 个月,电动车註册量预计将超过 100 万辆,约占整个市场的 7.4%(高于 2022 年同期的 5.4%)。专家也表示,2023 年电池电动车 (BEV) 的销量将达到约 110 万辆。特斯拉在 2023 年销售了 1,739,707 辆 Model 3/Y。

- 此外,鑑于联邦政府和国家相关人员正在就取消 2025 年燃油经济性标准和《清洁空气法》规定的州政府权力进行讨论,持续的市场成长将取决于监管发展。

北美汽车物流行业概况

北美汽车物流市场比较分散。预计未来几年电动车需求的不断增长、轻型汽车数量的增加以及其他一些因素将推动市场成长。竞争格局以以下主要企业为特征:DHL Supply Chain、Ryder System 和 CH Robinson。这些公司利用其全球网路和先进技术,提供全面的物流和供应链解决方案。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提条件

- 研究范围

第二章调查方法

- 分析方法

- 研究阶段

第三章执行摘要

第四章 市场洞察

- 市场概况

- 政府法规和倡议

- 价值链/供应链分析

- 产业技术趋势

- 聚焦:电子商务对传统汽车物流供应链的影响

- 深入了解汽车售后市场及其物流活动

第五章 市场动态

- 市场驱动因素

- 环境问题和法规

- 汽车技术的进步

- 市场限制

- 经济不确定性

- 市场机会

- 电动车的普及

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第六章 市场细分

- 按服务

- 运输

- 仓储、配送和库存管理

- 其他服务

- 按类型

- 整车

- 汽车零件

- 其他的

- 按国家

- 美国

- 加拿大

- 墨西哥

第七章 竞争格局

- 市场集中度概览

- 公司简介

- CEVA Logistics AG

- DB Schenker

- DHL

- DSV

- GEODIS

- KUEHNE+NAGEL International AG

- Nippon Express Co. Ltd

- Ryder System Inc.

- XPO Logistics Inc.

- United Parcel Service Inc.*

- 其他公司

第八章 市场机会与未来趋势

第 9 章 附录

- 各活动国内生产毛额分布

- 资本流动洞察

- 经济统计-运输和仓储业对经济的贡献

The North America Automotive Logistics Market size is estimated at USD 86.27 billion in 2025, and is expected to reach USD 113.71 billion by 2030, at a CAGR of 5.68% during the forecast period (2025-2030).

North American automotive logistics has rarely been on the verge of much change and opportunity. Yet, as in the broader automotive industry, there are few uncertainties about economic and trade risks, new regulations, consumer behavior, or returns on investment faced by vehicle logistics.

With greater visibility and more flexibility than ever before, the vehicle logistics sector must be able to compete. OEMs, logistics, and technology providers must collaborate to share data, plan, and upgrade technology to keep the supply chain flowing efficiently.

The future of automotive supply chains is vital to logistics service providers in the automotive sector and, at the macro level, whole economies. The nature of global trade and the dynamics of different national economies can be affected by any change in the supply chain structure for vehicles.

An increasing number of vehicle production facilities worldwide compels the growth of the automotive logistics market. In addition, the market growth is expected to accelerate in the coming years due to automobile manufacturers' significant business opportunities for logistics providers. In the post-recession era, emerging economies have seen steady growth, leading to a rise in disposable income for consumers.

North America Automotive Logistics Market Trends

Demand for Light Vehicle Production

- In North America, consumer preferences have shifted to sport utility vehicles and trucks, driving auto manufacturers to adapt their production to meet rising demand. Instances include the popularity of models like Ford Explorer and Chevrolet Silverado.

- Increased production of electric vehicles results from the increasing interest in hybrids and EVs. For example, in December 2023, Tesla's Gigafactory in Texas aimed to meet North America's growing demand for electric vehicles.

- The automotive industry in North America has been adapting to and investing in technologies to meet stringent emission standards, influencing the design and production of light vehicles. In August 2022, the US government signed the historic Inflation Reduction Act into law, which could prove to be the most critical economic and climate legislation in American history. The Act to reduce inflation, which has driven a revival in US manufacturing capacity, offers broad incentives for developing and manufacturing clean energy technologies.

- As the demand for light vehicle production rises, automotive logistics companies experience increased shipping volumes. More vehicles and components must be transported from manufacturing facilities to distribution centers and dealerships.

EV Boost in United States

- Federal and state-level incentives have been crucial in promoting EV adoption. The federal government offers tax credits for the purchase of qualifying electric vehicles. For instance, the Qualified Plug-In Electric Drive Motor Vehicle Credit provides a credit of up to USD 7,500.

- Major automakers have made substantial commitments to electric vehicles. Companies like General Motors (GM), Ford, and others have announced plans to invest in developing and producing electric vehicles. In January 2024, Ford Motor Co. inked a deal with a Minnesota-based company to buy a fleet of 1,000 all-electric vehicles, specifically the F-150 Lightning and Mustang Mach-E.

- During the first 11 months of 2023, EV registrations exceeded 1 million units, which is about 7.4% of the total market (up from 5.4% at this same time in 2022). Experts also stated that around 1.1 million battery-electric vehicles (BEVs) were sold in 2023. Tesla sold 1,739,707 Model 3/Y cars in 2023.

- The market's sustainable growth also depends on regulatory developments, given ongoing discussions among federal and national parties regarding the rollback of 2025 fuel-economy standards and state authority under the Clean Air Act.

North America Automotive Logistics Industry Overview

The North American Automotive Logistics Market is fragmented. The increasing demand for EVs, an increase in lighter vehicles, and several other factors are likely to drive the market's growth over the coming years. The competitive landscape is marked by key players such as DHL Supply Chain, Ryder System, and C.H. Robinson. These companies offer a comprehensive range of logistics and supply chain solutions, leveraging their global networks and advanced technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Government Regulations and Initiatives

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Technological Trends in the Industry

- 4.5 Spotlight - Effect of E-commerce on Traditional Automotive Logistics Supply Chain

- 4.6 Insights into Automotive Aftermarket and its Logistics Activities

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Environmental Concerns and Regulations

- 5.1.2 Technological Advancements in Automotive Technology

- 5.2 Market Restraints

- 5.2.1 Economic Uncertainty

- 5.3 Market Opportunities

- 5.3.1 Electric Vehicle Adoption

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Transportation

- 6.1.2 Warehousing, Distribution and Inventory Management

- 6.1.3 Other Services

- 6.2 By Type

- 6.2.1 Finished Vehicle

- 6.2.2 Auto Components

- 6.2.3 Other types

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

- 6.3.3 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 CEVA Logistics AG

- 7.2.2 DB Schenker

- 7.2.3 DHL

- 7.2.4 DSV

- 7.2.5 GEODIS

- 7.2.6 KUEHNE + NAGEL International AG

- 7.2.7 Nippon Express Co. Ltd

- 7.2.8 Ryder System Inc.

- 7.2.9 XPO Logistics Inc.

- 7.2.10 United Parcel Service Inc.*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 GDP Distribution, by Activity

- 9.2 Insights into Capital Flows

- 9.3 Economic Statistics-Transport and Storage Sector, Contribution to Economy

电动物流车辆马达市场(按马达类型、额定功率、车辆类型、应用和最终用户产业划分)-全球预测,2026-2032年

电动物流车辆马达市场(按马达类型、额定功率、车辆类型、应用和最终用户产业划分)-全球预测,2026-2032年 全球汽车物流市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车物流市场规模、份额、趋势和成长分析报告(2026-2034) 汽车物流市场规模、份额、趋势及预测(按类型、活动、运输方式、物流解决方案、分销和地区划分),2026-2034年

汽车物流市场规模、份额、趋势及预测(按类型、活动、运输方式、物流解决方案、分销和地区划分),2026-2034年 2026-2030年全球汽车OEM厂商厂内物流市场

2026-2030年全球汽车OEM厂商厂内物流市场 欧洲汽车物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲汽车物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 汽车物流市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

汽车物流市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 工厂内物流自动化:全球市场份额和排名、总收入和需求预测(2025-2031 年)汽车物流市场按模式、服务类型、车辆类型和最终用户划分-2025-2032 年全球预测按类型、操作类型、控制模式、容量、安装类型、应用、最终用途产业和分销管道分類的厂内升降机市场 - 2025-2030 年全球预测

工厂内物流自动化:全球市场份额和排名、总收入和需求预测(2025-2031 年)汽车物流市场按模式、服务类型、车辆类型和最终用户划分-2025-2032 年全球预测按类型、操作类型、控制模式、容量、安装类型、应用、最终用途产业和分销管道分類的厂内升降机市场 - 2025-2030 年全球预测 2025年全球汽车物流市场报告

2025年全球汽车物流市场报告