|

市场调查报告书

商品编码

1687948

半导体设备:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Semiconductor Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

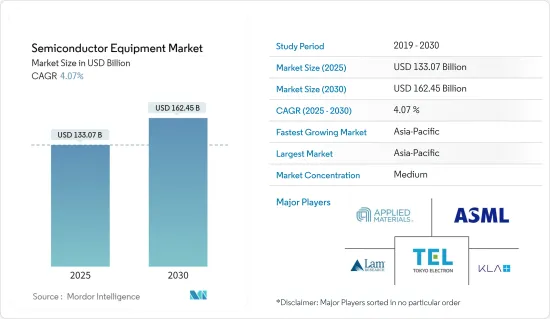

预计 2025 年半导体设备市场规模为 1,330.7 亿美元,到 2030 年将达到 1,624.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.07%。

全球半导体产业受到智慧型手机和高级家用电器等设备的同步成长以及汽车产业的成长所推动。

主要亮点

- 这些产业受到无线技术(5G)和人工智慧等技术转型的推动。多种因素,包括对高性能、低成本半导体的需求稳定成长,正在推动市场发展,并在短期、中期和长期产生各种影响。

- 5G的推出预计将成为推动市场发展的关键因素之一。 5G的扩展将加速无线产业的发展,实现扩增实境、关键任务服务、固定无线存取和物联网等创新。

- 此外,随着节点、晶圆尺寸不断缩小等半导体产业的逐步变革,超大规模整合技术对晶圆尺寸增加的需求正推动半导体设备的成长。此外,由于晶圆小型化带来的成本上升和测试挑战,晶圆製造商正在将其製程监视器从裸晶圆转变为生产晶圆。

- 全球对300mm硅晶片的需求旺盛,近年来对200mm硅晶片的需求也大幅增加。据 SEMI 称,2017 年至 2022 年期间,200 毫米晶圆厂准备在全球每月增加 60 万多片晶圆。预计此类趋势将进一步成为研究市场成长的催化剂。

- 2020 年上半年,新冠疫情扰乱了全球半导体供应链和生产流程,尤其是在中国。主要原因是劳动力短缺,导致多家半导体公司暂停营运。这给依赖半导体的最终产品公司带来了压力。

半导体设备市场趋势

消费性电子产品需求不断成长

- 消费性电子产品是成长最快的领域,对市场扩张贡献巨大。智慧型手机的成长是该市场的主要推动力,预计其成长将随着人口的成长而增加。由于对平板电脑、智慧型手机、笔记型电脑和穿戴式装置等产品的需求不断增加,消费性电子产品正在推动该产业的发展。随着半导体技术的进步,机器学习等新的细分市场正在迅速整合。

- 随着汽车、医疗设备、智慧型装置、智慧家庭、穿戴式装置等的不断进步,半导体整合已成为一种普遍现象。此外,由于消费者对小型化的需求,单晶片半导体的趋势日益增长。製造半导体的机器正在蓬勃发展,使得将半导体整合到单晶片上成为可能。

- 到2021年终,行动用户数量将达到约82亿。预计到 2027年终将达到约 91 亿。同期行动宽频用户份额可能会从 84% 上升到 93%。到预测期结束时,独立行动客户数量预计将从年终的 61 亿增加到 67 亿。

- 智慧型手机相关合约仍在增加。截至年终年底,合约数量为63亿,占全部行动电话合约的近77%。到 2027 年,预计这一数字将成长至 78 亿,占所有行动电话用户的 87%。

- 半导体设备市场受到对更快、更有效率的记忆体解决方案的需求的推动。这些半导体变得越来越复杂,能够处理密集型记忆体操作。总体而言,由于对 IP 解决方案提供者的依赖增加,市场投资大量涌入。

亚太地区预计将占据主要市场占有率

- 半导体设备高度集中在少数国家,少数主要国家以外的销售非常有限或根本不存在。中国已成为成熟半导体技术的重要生产国。同时,中国政府继续将半导体产业视为经济成长和技术领先地位的驱动力。预计到2030年全球半导体产能将增加约40%。

- 此外,2022年4月,领先的自动化测试设备供应商泰瑞达宣布向中国领先的微控制器单元(MCU)和安全集成电路(IC)晶片製造商国信科技发货其第7,000台J750半导体测试平台。

- 智慧电子设备的日益普及提高了製造机会,且电子设备在各种应用中的整合度更高,这是推动日本半导体设备成长的主要因素。此外,物联网、人工智慧和连网型设备与各个终端用户产业的结合预计将推动该国半导体设备市场的发展。

- 国际产业组织国际半导体产业协会 (SEMI) 称,由于汽车和高效能运算设备所使用的晶片需求强劲,预计台湾今年将成为全球最大的前端晶片製造设备支出地区。台湾在製造设备上的支出预计每年将增加52%,达到340亿美元。

- 包括韩国在内的主要铸造中心正在加强投资并鼓励本国工业影响力的成长。此外,韩国贸易、工业和能源部宣布,到2030年,晶片出口额预计将翻倍,达到2,000亿美元。政府还计划在首尔以南数十公里处建造一条“K半导体带”,将晶片设计人员、製造商和供应商聚集在一起。这些工厂旨在在全球晶片短缺的情况下将主要半导体公司及其供应商聚集在一起,增强韩国在全球半导体行业的竞争力,并实现关键半导体材料和设备的本地化供应。

半导体设备产业概况

半导体设备市场竞争对手之间的敌意较高。企业专业化是由小型企业产业竞争所需的高额研发投入和资本支出所推动的。主要参与者包括应用材料公司、阿斯麦控股半导体公司和 KLA 公司。该市场的一些最新发展包括:

- 2022年5月:SCREEN Holdings加大力度减少半导体产业对环境的影响。然而,随着我们对半导体装置的依赖性不断增加,製造过程对环境的影响已成为通用。在这项挑战背景下,SCREEN SPE 同意参与由世界领先的创新者 IMEC主导的永续半导体技术和系统调查计画。该计划旨在为减少整个半导体产业对环境的影响做出贡献。

- 2022 年 2 月:总部位于台湾的全球半导体代工厂联华电子 (UMC) 宣布计划在新加坡建立新的先进製造工厂。新工厂将建在该公司位于巴西立的现有工厂 Fab12i 旁。总投资额50亿美元。新晶圆厂月产能为3万片晶圆,预定2024年下半年开始生产。联华电子称,该工厂将成为新加坡最先进的半导体代工厂之一,将生产22nm和28nm晶片。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- COVID-19 产业影响评估

第五章 市场动态

- 市场驱动因素

- 家用电子电器需求不断成长

- 人工智慧、物联网和连网型设备的产业分布

- 市场限制

- 此技术的动态特性使得製造设备必须进行多项变革

第六章 市场细分

- 依设备类型

- 前端装置

- 光刻设备

- 蚀刻设备

- 成膜设备

- 测量/检测设备

- 材料去除及清洗设备

- 光阻剂处理设备

- 其他设备

- 后端设备

- 测试设备

- 组装包装设备

- 前端装置

- 按供应链进入

- IDM

- OSAT

- 晶圆代工厂

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 中国

- 日本

- 台湾

- 韩国

- 世界其他地区

第七章 竞争格局

- 公司简介

- Applied Materials Inc.

- ASML Holding Semiconductor Company

- Tokyo Electron Limited

- Lam Research Corporation

- KLA Corporation

- Veeco Instruments Inc.

- Screen Holdings Co. Ltd

- Teradyne Inc.

- Hitachi High-Technologies Corporation

第八章投资分析

第九章 市场机会与未来趋势

The Semiconductor Equipment Market size is estimated at USD 133.07 billion in 2025, and is expected to reach USD 162.45 billion by 2030, at a CAGR of 4.07% during the forecast period (2025-2030).

The global semiconductor industry is driven by the simultaneous growth of smartphones and other devices, such as advanced consumer electronics, and the growth of the automotive industry.

Key Highlights

- These industries are driven by technology transitions such as wireless technologies (5G) and artificial intelligence. Several factors, including a steady rise in the demand for high-performance and low-cost semiconductors, drive the market with varying impacts over the short, medium, and long term.

- The deployment of 5G is expected to be one of the key factors driving the market. This is because the expansion of 5G would lead to the expansion of the wireless industry and enable innovations like augmented reality, mission-critical services, fixed wireless access, and the Internet of Things.

- Furthermore, with the gradual transitions in the semiconductor industry, such as the miniaturization of nodes and wafer sizes, the demand for increasing the wafer sizes for ultra-large-scale integration technologies has fostered the growth of semiconductor equipment. Moreover, fab manufacturers are shifting process monitors from bare wafers to production wafers due to the higher cost and inspection challenges faced by wafer miniaturization.

- The global demand for 300 mm silicon wafers is strong, and the demand for 200 mm has also seen a surge in recent years. According to SEMI, 200 mm fabs are gearing up to add over 600,000 wafers per month across the world during 2017-2022. Such trends are further expected to act as catalysts for the growth of the market studied.

- The COVID-19 pandemic disrupted the supply chains and production processes of semiconductors worldwide, especially in China, during the first half of 2020. The primary reason was a labor shortage, during which several semiconductor companies suspended operations. This created a crunch for end-product companies that depend on semiconductors.

Semiconductor Equipment Market Trends

Increasing Demand for Consumer Electronic Devices

- Consumer electronics is the fastest-growing segment and contributes significantly to market expansion. The growth of smartphones, which is predicted to increase with population growth, is the key driving force for this market. Consumer electronics drive the industry due to the increased demand for products such as tablets, smartphones, laptop computers, and wearable gadgets. As semiconductor technology advances, new market areas, such as machine learning, are rapidly being integrated.

- Due to ongoing improvements in items, including cars, medical equipment, smart devices, smart homes, and wearables, semiconductor integration has become a widespread phenomenon. Additionally, the trend of combining semiconductors into a single chip is expanding due to the consumers' desire for small-sized devices. The machinery used to manufacture semiconductors is gaining momentum since it makes it possible to assemble semiconductors on a single chip.

- There were approximately 8.2 billion mobile subscriptions by the end of 2021. This is anticipated to reach nearly 9.1 billion by the end of 2027. The percentage of mobile broadband subscriptions may rise from 84% to 93% at the same time. By the end of the forecast period, there are expected to be 6.7 billion unique mobile customers, up from 6.1 billion at the end of 2021.

- Smartphone-related subscriptions are still increasing. There were 6.3 billion at the end of 2021, making up nearly 77% of all mobile phone subscriptions. By 2027, this is anticipated to increase to 7.8 billion, or 87% of all mobile subscribers.

- The semiconductor equipment market is driven by the demand for quicker and more effective memory solutions. These semiconductors are becoming more complicated and can handle intensive memory operations. Overall, the market is seeing significant investments due to the increased reliance on IP solution providers.

Asia-Pacific Expected to Hold Significant Market Share

- The semiconductor equipment is highly concentrated in a few countries, and sales of this equipment are very limited or non-existent outside some major countries. China has grown significantly as an essential producer of mature semiconductor technologies. On the other hand, the Chinese government continues to prioritize the semiconductor industry as a driver of economic growth and technological leadership. It is expected to add roughly 40% of the new global capacity by 2030.

- Further, in April 2022, Teradyne Inc., a leading supplier of automated test equipment, announced the shipment of the 7,000th unit of its J750 semiconductor test platform to Nations Technologies, a leading microcontroller unit (MCU) and security integrated circuit (IC) chip maker in China.

- The growing adoption of smart electronic devices that improve manufacturing opportunities and the significant integration of electronics into various applications are the key factors driving the growth of semiconductor equipment in Japan. Moreover, the incorporation of IoT, artificial intelligence, and connected devices into various end-user industries are expected to drive the semiconductor equipment market in the Country.

- Due to the robust demand for chips used in vehicles and high-performance computing devices, Taiwan is expected to become the world's largest spender on front-end chip manufacturing equipment this year, according to the international trade group SEMI. Taiwanese fab equipment spending is expected to rise by 52% yearly to USD 34 billion.

- South Korea and other major hubs for foundries are increasingly investing and incentivizing to expand the industry presence of their respective countries. In addition, the Ministry of Trade, Industry, and Energy announced that chip exports are expected to double to USD 200 billion by 2030. Furthermore, the government seeks to build a "K-Semiconductor belt" that stretches dozens of kilometers south of Seoul and brings together chip designers, manufacturers, and suppliers. These plants aim to sharpen South Korea's competitive edge in the global semiconductor industry and localize major semiconductor materials and equipment supplies with key semiconductor companies and their suppliers working in clusters amid a global chip shortage.

Semiconductor Equipment Industry Overview

The intensity of competitive rivalry is moderately high in the semiconductor equipment market. Firm specialization is driven by the high R&D investments and capital expenditures required to compete in the SME industry. Some key players are Applied Materials Inc., ASML Holding Semiconductor Company, and KLA Corporation. A few recent developments in this market are:

- May 2022: SCREEN Holdings increased its efforts to reduce the environmental impact of the semiconductor industry. However, as reliance on semiconductor devices has grown, the environmental impact created by the manufacturing processes has become a shared concern for the semiconductor industry. With this challenge in mind, SCREEN SPE agreed to join the Sustainable Semiconductor Technologies and Systems research program led by IMEC, a world-leading innovator. The program is designed to help the semiconductor industry reduce its overall environmental impact.

- February 2022: United Microelectronics Corporation (UMC), a Taiwanese global semiconductor foundry, announced its plans to build a new advanced manufacturing facility in Singapore. The new facility would be built next to its existing plant, known as Fab12i, in Pasir Ris. The total investment for the planned project was USD 5 billion. The new wafer fab facility would have a monthly capacity of 30,000 wafers, with production expected to start in late 2024. According to UMC, it would also be one of the most advanced semiconductor foundries in Singapore and will produce 22 nm and 28 nm chips.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes Products

- 4.3 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Consumer Electronic Devices

- 5.1.2 Proliferation of AI, IoT, And Connected Devices Across Industry Verticals

- 5.2 Market Restraints

- 5.2.1 Dynamic Nature of Technologies Requires Several Changes in Manufacturing Equipment

6 MARKET SEGMENTATION

- 6.1 By Equipment Type

- 6.1.1 Front-end Equipment

- 6.1.1.1 Lithography Equipment

- 6.1.1.2 Etch Equipment

- 6.1.1.3 Deposition Equipment

- 6.1.1.4 Metrology/Inspection Equipment

- 6.1.1.5 Material Removal/Cleaning Equipment

- 6.1.1.6 Photoresist Processing Equipment

- 6.1.1.7 Other Equipment Types

- 6.1.2 Back-end Equipment

- 6.1.2.1 Test Equipment

- 6.1.2.2 Assembly and Packaging Equipment

- 6.1.1 Front-end Equipment

- 6.2 By Supply Chain Participants

- 6.2.1 IDM

- 6.2.2 OSAT

- 6.2.3 Foundry

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Taiwan

- 6.3.3.4 Korea

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Applied Materials Inc.

- 7.1.2 ASML Holding Semiconductor Company

- 7.1.3 Tokyo Electron Limited

- 7.1.4 Lam Research Corporation

- 7.1.5 KLA Corporation

- 7.1.6 Veeco Instruments Inc.

- 7.1.7 Screen Holdings Co. Ltd

- 7.1.8 Teradyne Inc.

- 7.1.9 Hitachi High -Technologies Corporation