|

市场调查报告书

商品编码

1473282

应用材料公司:目标市场竞争分析Applied Materials: Competitive Analysis of Served Markets |

||||||

介绍

应用材料公司凭藉其技术领先地位、战略市场定位以及应对现代半导体製造课题的全面方法,在竞争激烈的半导体製造设备行业中脱颖而出。随着半导体产业朝向更小的节点和更复杂的装置架构发展,应用材料公司在蚀刻、沉积、CMP、计量和离子注入设备方面的创新将在实现下一代电子装置方面发挥重要作用。透过持续创新和策略远见,应用材料公司正在引领半导体技术和製造的未来,使我们在每个市场都拥有无与伦比的领导地位。

蚀刻/沉积技术

应用材料公司在作为半导体装置製造基础的蚀刻和沈积过程方面表现出色。该公司的蚀刻设备精确控制等离子体工艺,这对于在硅基板上定义奈米级特征至关重要。

在气相沉积方面,我们提供化学气相沉积 (CVD)、物理气相沉积 (PVD) 和原子层沉积 (ALD) 解决方案。这些技术对于形成半导体装置的各种薄膜层至关重要,并且重点关注精度、製程效率以及对不断变化的行业要求的适应性。

化学机械研磨设备

CMP(化学机械抛光)设备也是应用材料公司重点关注的领域,可确保製造步骤之间的晶圆表面平整度。应用材料公司的 CMP 设备整合到製造工作流程中,以优化产量并降低废品率。这有助于提高製造产量和成本效率,并实现半导体产业的目标。

测量/检测设备

计量和检测设备提供有关晶圆特性的关键数据,促进製程调整和缺陷的早期检测。此类设备对于品质控制至关重要,使製造商能够在设备变得更加复杂的情况下保持高产品产量和营运效率。

离子注入机

应用材料公司也专注于离子注入技术,这对于掺杂半导体材料至关重要。

该公司的注入机对于精确控制掺杂剂种类、能量和剂量以实现半导体装置所需的电气性能至关重要。

关于本报告

本报告分析了应用材料公司在全球半导体製造设备市场的表现趋势,包括整体技术开发、製造和供应趋势(2012-2023)、依产品类型划分的市场规模和占有率以及主要竞争对手。产品和业务成果。

目录

第一章简介

第二章 应用材料战略

- 市场策略

- 推动製造设备需求

- 国际存在

- 满足客户需求

- 新任CEO的策略

- 经营策略

- Silicon Systems Group

- Applied Global Services

- 展示

- 能源和环境解决方案

- 技术战略

- 产品策略

- 收购策略

- 法律策略

- 财务分析

第三章市场预测

- 市场驱动力

- 半导体市场

- 技术趋势

- 经济趋势

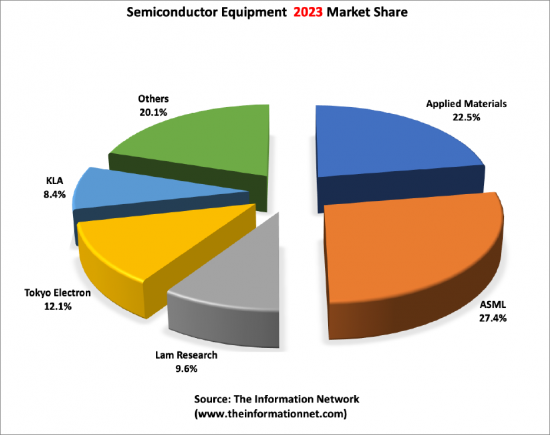

- Applied Materials:全球市场领导者(截至 2019 年)

- 市场规模及市占率

- 化学气相沉积

- 物理气相沉积

- 干蚀刻

- 快速热处理/氧化/扩散

- 硅外延

- CMP(化学机械平坦化)

- 测量/检查

- 离子注入

第四章竞争环境

- 介绍

- Lam Research

- Tokyo Electron Limited

- KLA

- ASM International

- Axcelis

- Canon Anelva

- Ebara

- Eugene Technology

- Hitachi High-Technologies

- Hitachi Kokusai Electric

- Jusung Engineering

- KC Tech

- Lasertec

- Nissin Ion Equipment

- NuFlare Technology

- Screen Semiconductor Solutions

- SEMES

- SEN

- TES

- Ulvac

- Wonik IPS

Introduction

In the competitive realm of semiconductor manufacturing equipment, Applied Materials stands out for its technological leadership, strategic market positioning, and comprehensive approach to addressing the challenges of modern semiconductor fabrication. As the industry moves towards smaller nodes and more complex device architectures, Applied Materials' innovations in etch, deposition, CMP, metrology, and ion implant equipment will continue to play a critical role in enabling the next generation of electronic devices. Through continuous innovation and strategic foresight, Applied Materials is not just competing but leading in the markets it serves, shaping the future of semiconductor technology and manufacturing.

Applied Materials' market leadership is supported by continuous innovation and a strategic approach to addressing semiconductor manufacturing challenges. The company's investment in research and development ensures its technologies meet current demands and anticipate future industry shifts.

As semiconductor fabrication evolves towards more advanced nodes and explores novel materials and architectures, Applied Materials is poised to play a central role. Its comprehensive technology portfolio, covering etch, deposition, CMP, metrology/inspection, and ion implant, positions the company as a key enabler of next-generation semiconductor devices.

Etch and Deposition Technologies

Applied Materials excels in etch and deposition processes, foundational to semiconductor device fabrication. The company's etch systems offer precise control over plasma processes, crucial for defining nanoscale features on silicon substrates. These systems enable the creation of intricate device structures required for current computing and memory applications.

In deposition, Applied Materials provides solutions across Chemical Vapor Deposition (CVD), Physical Vapor Deposition (PVD), and Atomic Layer Deposition (ALD). These technologies are critical for forming the various thin-film layers in semiconductor devices, with a focus on precision, process efficiency, and adaptability to evolving industry requirements.

CMP Systems

CMP equipment is another area of focus for Applied Materials, ensuring the planarity of wafer surfaces between fabrication steps. The company's CMP systems integrate with fabrication workflows, optimizing throughput and reducing defectivity. This contributes to improved manufacturing yields and cost efficiencies, aligning with the semiconductor industry's goals.

Metrology/Inspection Equipment

Metrology and inspection equipment from Applied Materials provides critical data on wafer properties, facilitating process adjustments and early defect identification. This category of equipment is vital for quality control, enabling manufacturers to uphold high standards of product yield and operational efficiency amid increasing device complexity.Ion Implant Equipment

Applied Materials also specializes in ion implantation technology, essential for doping semiconductor materials. The company's implanters deliver high precision in dopant species, energy, and dose control, critical for achieving desired electrical characteristics in semiconductor devices.

About This Report

This report addressed the Served Available Markets that Applied Materials competes. Namely:

- Chemical Vapor Deposition

- Physical Vapor Deposition

- Dry Etch

- Rapid Thermal Processing/Oxidation/Diffusion

- Silicon Epitaxy

- Chemical Mechanical Planarization

- Metrology and Inspection

- Ion Implantation

It presents forecasts for each sector and market shares for each equipment type between 2012 and 2023.

Table of Contents

Chapter 1. Introduction

Chapter 2. Applied's Strategies

- 2.1. Market Strategies

- 2.1.1. Driving Demand for Processing Equipment

- 2.1.2. A Global Presence

- 2.1.3. Meeting Customer Needs

- 2.1.4. New CEO's Strategy

- 2.2. Business Strategies 2.

- 2.2.1. Silicon Systems Group

- 2.2.2. Applied Global Services

- 2.2.3. Display

- 2.2.4. Energy and Environmental Solutions

- 2.3. Technology Strategies

- 2.4. Product Strategies

- 2.5. Acquisition Strategies

- 2.6. Legal Strategies

- 2.7. Financial Analysis

Chapter 3. Market Forecast

- 3.1. Market Drivers

- 3.1.1. Semiconductor Market

- 3.1.2. Technical Trends

- 3.1.3. Economic Trends

- 3.2. Applied Materials - Global Market Leader Until 2019

- 3.3. Market Size and Market Shares

- 3.3.1. Chemical Vapor Deposition

- 3.3.2. Physical Vapor Deposition

- 3.3.3. Dry Etch

- 3.3.4. Rapid Thermal Processing/Oxidation/Diffusion

- 3.3.5. Silicon Epitaxy

- 3.3.6. Chemical Mechanical Planarization

- 3.3.7. Metrology and Inspection

- 3.3.8. Ion Implantation

Chapter 4. Competitive Environment

- 4.1. Introduction

- 4.2. Lam Research

- 4.2.1. Strategies

- 4.2.2. Products

- 4.2.3. Financial Analysis

- 4.3. Tokyo Electron Limited

- 4.3.1. Strategies

- 4.3.2. Products

- 4.3.3. Financial Analysis

- 4.4. KLA

- 4.4.1. Strategies

- 4.4.2. Products

- 4.4.3. Financial Analysis

- 4.5. ASM International

- 4.5.1. Strategies

- 4.5.2. Products

- 4.5.3. Financial Analysis

- 4.6. Axcelis

- 4.6.1. Strategies

- 4.6.2. Products

- 4.6.3. Financial Analysis

- 4.7. Canon Anelva

- 4.7.1. Business Sectors Covered In The Market Analysis Chapter

- 4.7.2. Company Profile

- 4.7.3. Company Financials

- 4.8. Ebara

- 4.8.1. Business Sectors Covered In The Market Analysis Chapter

- 4.8.2. Company Profile

- 4.8.3. Company Financials

- 4.9. Eugene Technology

- 4.9.1. Business Sectors Covered In The Market Analysis Chapter

- 4.9.2. Company Profile

- 4.9.3. Company Financials

- 4.10. Hitachi High-Technologies

- 4.10.1. Business Sectors Covered In The Market Analysis Chapter

- 4.10.2. Company Profile

- 4.10.3. Company Financials

- 4.11. Hitachi Kokusai Electric

- 4.11.1. Business Sectors Covered In The Market Analysis Chapter

- 4.11.2. Company Profile

- 4.11.3. Company Financials

- 4.12. Jusung Engineering

- 4.12.1. Business Sectors Covered In The Market Analysis Chapter

- 4.12.2. Company Profile

- 4.12.3. Company Financials

- 4.13. KC Tech

- 4.13.1. Business Sectors Covered In The Market Analysis Chapter

- 4.13.2. Company Profile

- 4.13.3. Company Financials

- 4.14. Lasertec

- 4.14.1. Business Sectors Covered In The Market Analysis Chapter

- 4.14.2. Company Profile

- 4.14.3. Company Financials

- 4.15. Nissin Ion Equipment

- 4.15.1. Business Sectors Covered In The Market Analysis Chapter

- 4.15.2. Company Profile

- 4.15.3. Company Financials

- 4.16. NuFlare Technology

- 4.16.1. Business Sectors Covered In The Market Analysis Chapter

- 4.16.2. Company Profile

- 4.16.3. Company Financials

- 4.17. Screen Semiconductor Solutions

- 4.17.1. Business Sectors Covered In The Market Analysis Chapter

- 4.17.2. Company Profile

- 4.17.3. Company Financials

- 4.18. SEMES

- 4.18.1. Business Sectors Covered In The Market Analysis Chapter

- 4.18.2. Company Profile

- 4.18.3. Company Financials

- 4.19. SEN

- 4.19.1. Business Sectors Covered In The Market Analysis Chapter

- 4.19.2. Company Profile

- 4.19.3. Company Financials

- 4.20. TES

- 4.20.1. Business Sectors Covered In The Market Analysis Chapter

- 4.20.2. Company Profile

- 4.20.3. Company Financials

- 4.21. Ulvac

- 4.21.1. Business Sectors Covered In The Market Analysis Chapter

- 4.21.2. Company Profile

- 4.21.3. Company Financials

- 4.22. Wonik IPS

- 4.22.1. Business Sectors Covered In The Market Analysis Chapter

- 4.22.2. Company Profile

- 4.22.3. Company Financials

List of Tables

- 3.1. Worldwide Capital Spending

- 3.2. Wafer Front End (WFE) Market By Device Type

- 3.3. Top Semiconductor Equipment Revenues

- 3.4. Worldwide CVD Market Forecast

- 3.5. Worldwide CVD Market Shares

- 3.6. Worldwide PVD Market Forecast

- 3.7. Worldwide PVD Market Shares

- 3.8. Worldwide Dry Etch Market Forecast

- 3.9. Worldwide Dry Etch Market Shares

- 3.10. Worldwide RTP/Oxidation/Diffusion Market Forecast

- 3.11. Worldwide RTP/Oxidation/Diffusion Market Shares

- 3.12. Worldwide Silicon Epitaxy Market Forecast

- 3.13. Worldwide Silicon Epitaxy Market Shares

- 3.14. Worldwide CMP Market Forecast

- 3.15. Worldwide CMP Market Shares

- 3.16. Worldwide M&I Market Forecast

- 3.17. Worldwide M&I Market Shares

- 3.18. Worldwide Ion Implantation Market Forecast

- 3.19. Worldwide Ion Implantation Market Shares

List of Figures

- 3.1. Semiconductor vs Equipment vs GDP

- 3.2. Recession Cycle

- 3.3. Semiconductor Equipment Share

- 3.4. Worldwide CVD Market Shares

- 3.5. Worldwide PVD Market Shares

- 3.6. Worldwide Dry Etch Market Shares

- 3.7. Worldwide RTP/Oxidation/Diffusion Market Shares

- 3.8. Worldwide Silicon Epitaxy Market Shares

- 3.9. Worldwide CMP Market Shares

- 3.10. Worldwide M&I Market Shares

- 3.11. Worldwide Ion Implantation Market Shares

半导体製造设备市场:2026-2032年全球预测(按设备类型、封装尺寸、应用产业、最终用户、分销和应用划分)

半导体製造设备市场:2026-2032年全球预测(按设备类型、封装尺寸、应用产业、最终用户、分销和应用划分) 半导体製造设备市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、装置、製程、最终用户及製造阶段划分扫描电子显微镜维修服务市场:按服务类型、应用和最终用户划分,全球预测(2026-2032年)显微镜目镜筒市场:按类型、材料、分销管道、应用和最终用户划分,全球预测,2026-2032年

半导体製造设备市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、装置、製程、最终用户及製造阶段划分扫描电子显微镜维修服务市场:按服务类型、应用和最终用户划分,全球预测(2026-2032年)显微镜目镜筒市场:按类型、材料、分销管道、应用和最终用户划分,全球预测,2026-2032年 中国大陆半导体及设备市场:分析及製造趋势

中国大陆半导体及设备市场:分析及製造趋势 全球半导体製造设备:市场、市场占有率、市场预测等离子切割系统市场:按设备类型、晶圆尺寸、晶圆厚度、最终用户和应用划分,全球预测,2026-2032年生物洁净作业台市场按产品类型、应用和最终用户划分,全球预测(2026-2032年)冷冻肉切丁机市场按机器类型、自动化程度、产能、终端用户产业、应用和销售管道划分,全球预测(2026-2032年)人工智慧市场分析及产量比率(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和设备划分

全球半导体製造设备:市场、市场占有率、市场预测等离子切割系统市场:按设备类型、晶圆尺寸、晶圆厚度、最终用户和应用划分,全球预测,2026-2032年生物洁净作业台市场按产品类型、应用和最终用户划分,全球预测(2026-2032年)冷冻肉切丁机市场按机器类型、自动化程度、产能、终端用户产业、应用和销售管道划分,全球预测(2026-2032年)人工智慧市场分析及产量比率(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和设备划分