|

市场调查报告书

商品编码

1692494

视讯编码器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Video Encoder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

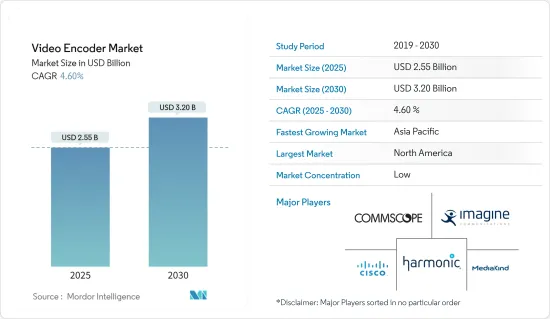

预计 2025 年视讯编码器市场规模为 25.5 亿美元,预计到 2030 年将达到 32 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.6%。

主要亮点

- 由于各种平台对高品质视讯串流和广播的需求不断增加,视讯编码器市场正在经历强劲增长。视讯编码器将视讯讯号转换为适合透过网际网路和其他网路传输的数位格式。这项市场扩张的推动力包括线上影片内容消费的增加、 Over-The-Top服务的普及以及直播活动的激增。社群媒体平台的兴起,影片内容是其中重要的参与工具,进一步推动了对先进影片编码解决方案的需求。

- 技术进步对于塑造视讯编码器市场至关重要。 H.265(HEVC)和新兴的 AV1转码器等压缩演算法的创新在保持视讯品质的同时提高了压缩比,促进了高效的资料传输和储存。这些进步将满足对 4K 和 8K 视讯解析度日益增长的需求,这需要更多的频宽和储存容量。

- 此外,整合人工智慧(AI)和机器学习(ML)的硬体编码器的发展代表着一个重要趋势。这些整合提高了即时视讯处理能力并优化了网路资源。

- 此外,Cisco、Harmonic 和 Axis Communications(Canon)等大公司在视讯编码器市场处于领先地位。除了这些产业巨头之外,新兴企业也凭藉其创新解决方案掀起波澜。这些参与者正在积极推行合併、收购、合作和产品发布等策略,以加强其市场地位。特别是,许多公司正在与 OTT服务供应商和广播公司建立策略联盟,以利用协同效应并扩大客户范围。

- 视讯编码器市场前景十分光明,具有巨大的成长机会。视讯标准的不断发展、5G 网路的全球部署以及对虚拟实境 (VR) 和扩增实境(AR) 等身临其境型体验日益增长的需求正在推动进一步的创新和应用。重视研发并对技术变化做出快速反应的公司将能够更好地利用新兴趋势并保持竞争优势。

- 儘管视讯编码器市场拥有许多成长动力,但硬体视讯编码器的高前期成本也带来了明显的障碍。这些设备对于将原始影像转换为广播和串流媒体的数位格式至关重要,通常需要大量的前期投资。这样的财务支出可能是一个重大障碍,尤其是对于小型企业和新兴企业。由此产生的高成本可能会阻碍潜在客户采用新技术或更新现有设置,从而阻碍市场扩张和创新。此外,这些费用会直接影响公司的整体投资收益,凸显了製造商考虑节约成本措施和提供弹性资金筹措选择以促进更广泛采用的重要性。

视讯编码器市场趋势

视讯串流平台的普及正在推动市场成长

- Netflix、Amazon Prime 和 YouTube 等影片串流服务的日益普及,带来了对高品质、低延迟串流媒体的需求。因此,这种趋势正在推动对先进视讯编码器的需求。这些编码器的任务是高效压缩影片、保持品质并确保无缝的观看体验,尤其是在 4K 和 8K 等要求苛刻的解析度下。根据 Inplayer 统计,18.4% 的 OTT 使用者年龄在 25-29 岁之间,11.5% 的 OTT 使用者年龄在 30-36 岁之间。值得注意的是,约有 15% 的 OTT 用户年龄在 17 岁以下。

- 用户生成内容和专业内容的兴起正在推动串流影片製作的繁荣。因此,对高效影片编码解决方案的需求日益增加。这些解决方案对于增加内容量、快速上传以及确保无缝的串流体验至关重要。这一趋势是视讯编码器市场的主要推动力。

- 此外,活动、游戏、体育和社交媒体直播的激增推动了对即时视讯编码解决方案的需求,从而推动了视讯编码器市场的发展。能够快速处理即时内容并最大限度地减少延迟的编码器对于提供流畅且引人入胜的观看体验至关重要。

- 此外,智慧型手机、平板电脑和智慧型电视上影片串流使用量的快速成长凸显了自我调整视讯编码的必要性。编码器对于根据不同的萤幕大小和网路速度缩放影片至关重要,它正在推动影片编码器市场的发展。

预计亚太地区将占据最大市场占有率

- 中国地面电波位地面电视广播的出现改善了现有的服务,为新的应用铺平了道路。 DTT广播标准允许广域固定接收高画质电视和多个标准画质电视节目。新服务还包括行动、穿戴和高速应用。

- 中国政府也致力于改善人们的观看体验,并鼓励主要城市开始免费提供地面电波高清电视广播内容。这将有助于推动地面数位广播市场和整个高清电视行业的成长,包括高清平板、晶片组、发送器、软体和内容创作。

- 随着 Netflix、亚马逊和 Disney+Hotstar 等 OTT 服务对原创和收购内容的投资,订阅视讯点播将占 OTT 总收入的 93%,到 2024 年将上升至 30.7%,在印度达到 27 亿美元。截至2024年1月,YouTube用户数已达4.62亿,观看人数远超美国,成为印度领先的影片平台。

- 韩国公司正在开发视讯编码器解决方案,以引领广播和串流媒体市场。例如,KT公司凭藉其在DTH领域的垄断地位和在IPTV领域的强势地位,在韩国付费电视服务行业中,在订阅量和监督处于领先地位,占有最大的市场份额。

- 近年来,技术的进步使得能够录製和显示 4K影像的相机、显示器、平板电脑和其他设备的迅速普及,4K 视讯的解析度高于高清电视 (HDTV)。随着此类设备越来越普及,日本对透过广播和网路分发传输高清影像的下一代影像编码的期望也越来越高。 4K电视在一般家庭中越来越普及,各大电视厂商纷纷推出多种型号。

视讯编码器产业概况

视讯编码器市场竞争激烈,Harmonic Inc.、CommScope Holding Company Inc. 和 MediaKind 等主要参与者不断增强自身能力以保持竞争力。这些公司策略性地专注于产品创新、合併、收购和伙伴关係,以实现产品系列多样化并扩大全球影响力。

- 2024 年 1 月,主要企业Arcturus 宣布更新其 HoloSuite 工具组。此次更新引入了一种新方法,可以将轻量级、可扩展的体积影像无缝传送到游戏引擎。 Arcturus 为虚拟製作团队和游戏开发者提供支援。使用者可以使用更多的体积特征来丰富他们的数位景观,而不会牺牲资料品质。

- 2023 年 11 月,影像和音讯转码器技术专家 MainConcept 宣布发布用于 OTT 和电视广播工作流程的即时编码应用程式的最新版本。 Live Encoder 的新版本 3.4 支援 VVC/H.266 和 MPEG-5 LCEVC转码器。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 视讯转码器分析及其发展

- VVC核准的公司和企业名单

- 为 VVC 标准做出贡献的公司列表

- COVID-19对市场的影响

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场动态

- 市场驱动因素

- 视讯串流平台日益普及

- 轻鬆整合硬体编码器和摄影机

- 云端视讯编码技术推动需求

- 市场挑战

- 硬体视讯编码器的初始成本高

第六章市场区隔

- 按应用

- 付费电视

- 有线视讯编码器

- 卫星视讯编码器

- IPTV视讯编码器

- 广播与数位地面电视(DTT)

- 贡献视讯编码器

- 回程传输和分发视讯编码器

- DTT视讯编码器

- 安全与监控

- 付费电视

- 按地区

- 美洲

- 美国

- 加拿大

- 巴西

- 墨西哥

- 其他地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 波兰

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 韩国

- 日本

- 其他亚太地区

- 中东和非洲

- 土耳其

- 以色列

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 美洲

第七章竞争格局

- 公司简介

- Harmonic Inc.

- Commscope Holding Company Inc.

- MediaKind

- Cisco Systems Inc.

- Imagine Communications

- Z3 Technology

- ATEME

- Adtec Digital

- Telairity(VITEC)

- Axis Communications AB(Canon Inc.)

第八章投资分析

第九章:市场的未来

The Video Encoder Market size is estimated at USD 2.55 billion in 2025, and is expected to reach USD 3.20 billion by 2030, at a CAGR of 4.6% during the forecast period (2025-2030).

Key Highlights

- The video encoder market is witnessing strong growth, driven by the rising demand for high-quality video streaming and broadcasting across various platforms. Video encoders convert video signals into digital formats suitable for transmission over the Internet or other networks. This market's expansion is fueled by the increasing consumption of online video content, the proliferation of over-the-top (OTT) services, and the surge in live-streaming activities. The widespread adoption of social media platforms, where video content is a key engagement tool, further propels the demand for advanced video encoding solutions.

- Technological advancements are pivotal in shaping the video encoder market. Innovations in compression algorithms, such as H.265 (HEVC) and the emerging AV1 codec, enhance compression rates while maintaining video quality, facilitating efficient data transmission and storage. These advancements support the increasing demand for 4K and 8K video resolutions, which require significantly more bandwidth and storage capacity.

- Additionally, the development of hardware encoders that integrate artificial intelligence (AI) and machine learning (ML) represents a significant trend. These integrations improve real-time video processing capabilities and optimize network resources.

- Moreover, major players such as Cisco Systems Inc., Harmonic Inc., and Axis Communications AB (Canon Inc.) lead the pack in the video encoder market. Alongside these industry stalwarts, newer firms are making waves with innovative solutions. These players are actively pursuing strategies like mergers, acquisitions, partnerships, and product launches to bolster their market positions. Notably, many are forging strategic ties with OTT service providers and broadcasters, seeking to tap into synergies and broaden their customer reach.

- The video encoder market exhibits a highly promising outlook with significant growth opportunities. The ongoing evolution of video standards, the global deployment of 5G networks, and the increasing demand for immersive experiences, such as virtual reality (VR) and augmented reality (AR), are set to drive further innovations and applications. Companies prioritizing research and development and swiftly adapting to technological shifts will be well-positioned to capitalize on emerging trends and maintain their competitive advantage.

- While the video encoder market boasts numerous growth drivers, a notable hurdle emerges in the form of the steep initial costs associated with hardware video encoders. These devices, pivotal for transforming raw video into digital formats for broadcasting and streaming, often demand a significant upfront investment. This financial outlay can pose a formidable obstacle, especially for smaller enterprises and startups. The resulting high costs may dissuade potential customers from embracing new technologies or modernizing their existing setups, constraining market expansion and stifling innovation. Moreover, these expenses can directly impact a company's overall return on investment, underscoring the importance for manufacturers to explore cost-cutting measures or offer flexible financing options to spur wider adoption.

Video Encoder Market Trends

Increasing Popularity of Video Streaming Platforms is Expected to Drive the Market Growth

- The rising popularity of video streaming services such as Netflix, Amazon Prime, and YouTube has heightened the appetite for high-quality, low-latency streaming. Consequently, this trend drives the demand for advanced video encoders. These encoders are tasked with compressing videos efficiently, maintaining quality, and guaranteeing seamless viewing, especially at resolutions as demanding as 4K and 8K. According to Inplayer, among OTT users, 18.4% fall in the 25 - 29 age bracket, with 11.5% in the 30 - 36 range. Notably, approximately 15% of OTT users are under 17 years old.

- The rise of user-generated and professional content has led to a boom in video production for streaming. Consequently, there is a growing demand for efficient video encoding solutions. These solutions are crucial for increasing content volume, ensuring swift uploads, and seamless streaming experiences. This trend serves as a significant driver of the video encoder market.

- Moreover, the surge in live streaming across events, gaming, sports, and social media has heightened the need for real-time video encoding solutions, driving the video encoder market. Encoders that can process live content swiftly, ensuring minimal delays, are pivotal for delivering a smooth and engaging viewer experience.

- Also, the surge in smartphone, tablet, and smart TV usage for video streaming has underscored the necessity for adaptive video encoding. Encoders, pivotal for tailoring videos to diverse screen sizes and network speeds, are driving the video encoder market.

Asia-Pacific is Expected to Hold the Largest Market Share

- The advent of terrestrial digital television broadcasting in China has improved existing services and paved the way for new applications. The DTT broadcast standard enables wide-area fixed reception on HDTV and multiple SDTV programs. New services also include mobile, wearable, and high-speed applications.

- The Chinese government is also working to improve people's viewing experience, and China encouraged major cities to start offering free terrestrial HDTV broadcast content. This helps drive growth in the digital terrestrial market and the HDTV industry as a whole, including high-definition flat panels, chipsets, transmitters, software, and content creation.

- Investments by OTT services like Netflix, Amazon, and Disney+ Hotstar in original and acquired content will enable subscription video-on-demand to make up 93% of the total OTT revenue, increasing to 30.7% by 2024, amounting to USD 2.7 billion in India. By January 2024, YouTube emerged as the leading video platform in India, attracting 462 million users, significantly outpacing the United States in viewership.

- South Korean organizations are developing video encoder solutions to drive the broadcasting and streaming market. For example, KT Corp. is driving the pay TV services industry in South Korea regarding subscriptions and supervision, owing to its monopoly in the DTH segment and strong position in the IPTV segment, where it has the greatest share.

- In recent years, technological advances have led to the rapid spread of devices such as cameras, displays, and tablets that can record and display 4K video in higher resolution than high-definition televisions (HDTVs). With the proliferation of these devices, expectations are rising for next-generation video encoding for delivering HD video over broadcast and network delivery in Japan. 4K TVs are becoming increasingly popular in the home, and many models are available from major TV manufacturers.

Video Encoder Industry Overview

The video encoder market is highly competitive, with major players like Harmonic Inc., CommScope Holding Company Inc., and MediaKind continuously enhancing their capabilities to maintain a competitive edge. These companies strategically focus on product innovations, mergers, acquisitions, and partnerships to diversify their product portfolios and expand their global footprint.

- In January 2024, Arcturus, a key player in volumetric video technology, unveiled an update for its HoloSuite toolset. This update introduces a novel approach, enabling the seamless delivery of lightweight, scalable volumetric video to game engines. Arcturus empowers not just virtual production teams but also game developers. Users can now enrich their digital landscapes with more volumetric characters without compromising on data quality.

- In November 2023, MainConcept, a video and audio codec technology specialist, announced the release of the latest version of its real-time encoding application for OTT and TV broadcasting workflows. The new version, Live Encoder 3.4, supports VVC/H.266 and MPEG-5 LCEVC codecs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Analysis of Video Codecs and Their Evolution

- 4.3 List of VVC-approved and Incorporated Companies

- 4.4 List of Companies Contributing to the VVC Standard

- 4.5 Impact of COVID-19 on the Market

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Popularity of Video Streaming Platforms

- 5.1.2 Easy Integration of Hardware Encoders with Video Cameras

- 5.1.3 Cloud Video Encoding Technology to Drive the Demand

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Hardware Video Encoder

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Pay TV

- 6.1.1.1 Cable Video Encoder

- 6.1.1.2 Satellite Video Encoder

- 6.1.1.3 IPTV Video Encoder

- 6.1.2 Broadcast and Digital Terrestrial Television (DTT)

- 6.1.2.1 Contribution Video Encoder

- 6.1.2.2 Backhaul and Distribution Video Encoder

- 6.1.2.3 DTT Video Encoder

- 6.1.3 Security and Surveillance

- 6.1.1 Pay TV

- 6.2 By Geography

- 6.2.1 Americas

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.1.3 Brazil

- 6.2.1.4 Mexico

- 6.2.1.5 Rest of the Americas

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Russia

- 6.2.2.5 Poland

- 6.2.2.6 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 South Korea

- 6.2.3.4 Japan

- 6.2.3.5 Rest of Asia-Pacific

- 6.2.4 Middle East and Africa

- 6.2.4.1 Turkey

- 6.2.4.2 Israel

- 6.2.4.3 United Arab Emirates

- 6.2.4.4 Saudi Arabia

- 6.2.4.5 South Africa

- 6.2.4.6 Rest of Middle East and Africa

- 6.2.1 Americas

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Harmonic Inc.

- 7.1.2 Commscope Holding Company Inc.

- 7.1.3 MediaKind

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Imagine Communications

- 7.1.6 Z3 Technology

- 7.1.7 ATEME

- 7.1.8 Adtec Digital

- 7.1.9 Telairity (VITEC)

- 7.1.10 Axis Communications AB (Canon Inc.)