|

市场调查报告书

商品编码

1692538

无线连接晶片组:市场占有率分析、行业趋势和成长预测(2025-2030 年)Wireless Connectivity Chipset - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

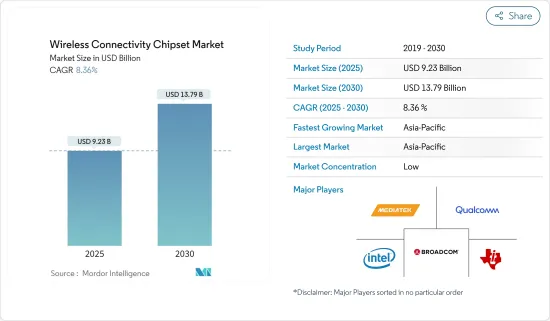

预计到 2025 年无线连接晶片组市场规模将达到 92.3 亿美元,到 2030 年将达到 137.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.36%。

关键亮点

- 随着高速网路的普及,连网型设备和智慧家庭应用的采用率正在增加,尤其是在欧洲、北美和亚太等地区。主要解决方案包括语音助理、智慧恆温器、智慧照明、安全摄影机和智慧家用电子电器。

- 此外,2024 年 5 月,联发科宣布推出两款新晶片组,它们将提供强大的性能并支援多个垂直领域的最新 AI 增强功能。其中包括用于高阶 Chromebook 的 Kompanio 838 SoC 和用于 4K 高阶智慧型电视和显示器的 Pentonic 800 SoC。该公司重点介绍了人工智慧、汽车、物联网、电视、Chromebook 和无线连接等产品类型的重大发展。

- 例如,中国成立了IMT-2030(6G)推进组,加速6G技术研发。预计2030年左右全球将实现6G商用,中国率先支持5G商用,将为6G发展奠定坚实基础。

- 增加多个设备(例如在物联网中)会增加网路的表面积,并在此过程中增加潜在的攻击媒介。即使连接到网路的单一不安全设备也可能成为针对网路的主动攻击的入口点。

- 根据经济合作暨发展组织(OECD)的研究,到2025年,拥有电脑的家庭数量预计将增加到1,262,470,000个。拥有至少一台电脑的家庭称为电脑家庭。电脑普及率的显着提高为市场参与企业创造了机会,使他们能够拓宽 Wi-Fi 晶片组产品系列、扩大在不同地区的影响力并增加市场占有率。

- 市场上的各种参与企业都在开发新产品以保持竞争力,这可能会进一步促进市场成长。例如,Wi-Fi 7 技术的早期先驱联发科于 2023 年 11 月推出最新产品 Filogic 860 和 Filogic 360,巩固了其市场领导地位。这些新增产品大大扩展了联发科的尖端产品线,专注于提供卓越性能和坚如盘石的可靠性的最新连接技术。

- Filogic 860 晶片组具有双频网路基地台和先进的网路处理器,专为企业网路基地台、服务供应商网关、网状节点以及各种零售和物联网路由器量身定制。同时,Filogic 360 将 Wi-Fi 7 2x2 功能和双蓝牙 5.4 无线电整合到单一晶片中。该设计经过专门设计,旨在为边缘和串流媒体设备以及各种家用电子电器产品带来下一代 Wi-Fi 7 连接。

- 开发和製造先进 Wi-Fi 晶片组的高成本对市场构成了重大挑战。製造这些晶片组所需的复杂且昂贵的技术可能会增加最终产品的成本并阻碍其采用,尤其是对于对价格敏感的消费者而言。

- 新冠疫情过后,人们更加重视采用协作工具,同时选择采用数位模式进行相关会议与讨论。此外,新兴的 5G使用案例(例如支援增加上学和在家工作的需求)预计将推动 5G 投资。此外,许多职场正在采用混合工作模式,透过部署 5G 连线可以增强这种模式。儘管供应链短缺造成中断,但此类情况仍对市场产生积极推动作用。

无线连接晶片组市场趋势

Wi-Fi 独立组网占据最大市场份额

- Wi-Fi网路技术的进步使用户体验到更快的速度和更低的通讯。这鼓励了数据密集型服务和应用程式的使用。透过 Wi-Fi 网路传输的资料量大幅增加,主要原因是客户对视讯的需求以及企业和消费者向云端服务的转变。预计此因素将推动对高速、大容量网路的无线 5G 连线的需求。

- 网路在现代世界的普及率正在不断提高。根据通讯预测,到 2023 年,全球网路用户数将由去年的 51 亿增加到 54 亿。这占世界人口的67%。

- 根据 Snapchat 的报告,到 2025 年,全球约 75% 的人口和几乎所有智慧型手机用户都将成为 AR 技术的频繁用户,其中超过 15 亿是千禧世代。根据GSMA《中国移动经济》预测,到2025年,中国大陆将新增约3.4亿个智慧型手机连接,占全球连接数的90%,其中中国当地的普及率将达到15亿,香港为1230万,澳门为190万,台湾为2570万。

- 2024年2月,韩国Stage X公司宣布取得频谱,成为韩国第四大行动营运商,并计画在2025年上半年推出全国性行动网路服务。该公司计划投资4.62亿美元(6,128亿韩元)兴建6,000个基地台,在韩国全国推出28GHz的5G网路。

- 根据爱立信行动报告,到 2026 年,北美智慧型手机的平均每月行动数据使用量预计将达到 49GB。智慧型手机的消费者群体、丰富的影片使用和大资料方案正在推动流量成长。虽然每部智慧型手机的流量在短期内可能会强劲成长,但预计采用由 AR 和 VR 驱动的身临其境型5G 消费者连线将在长期内推动更高的成长率。

- 此外,低延迟为高速虚拟和扩增实境影像奠定了基础,不会故障或延迟。小型基地台基础设施将增强行动连线,它可以增强 5G 无线讯号并改善穿过混凝土建筑物和墙壁的移动。小型基地台天线还可以加强无线连接,支援在同一网路上同时连接更多设备。预计此类发展将推动市场发展。

亚太地区可望成为成长最快的市场

- 5G在亚太地区的出现加速了用于高速网路连接的无线连接晶片组的部署。日本政府已批准在全国20.8万个交通号誌上安装5G基地台。地方政府和通讯业者共同承担5G部署使用交通号誌的成本。这将允许在更短的时间内部署更多的解决方案,并更快地将5G连线带到全国各地。

- 像 Biju 这样的印度跨国教育科技公司正在向学生提供平板电脑作为其教育课程的一部分,并透过数位方法和传统教学方法对他们进行教育。预计市场公司的这些倡议将进一步推动对平板电脑、智慧型手机和其他家用电子电器产品的需求,从而在预测期内推动该地区平板电脑无线连接晶片组市场的发展。

- 此外,亚太地区对网路服务的需求不断增长也有望推动该地区无线连接晶片组的采用。总理表示,印度推出5G网路服务预计将为该国释放新的经济潜力和社会效益。

- 此外,中国正引领全球5G的发展。全国已建成超过254万个5G基地台,超过5.75亿人拥有5G智慧型手机。中国也计划在2025年投资1.2兆元人民币(1742亿美元)建设5G网路。对稳定的5G网路日益增长的需求正在加速中国小型基地台解决方案的部署。

- 随着 5G 智慧型手机的普及和价格的不断下降,以及大都会圈和农村地区智慧型手机的快速普及,预计 5G 用户数量将快速增长,到 2023 年底该地区将达到约 5,000 万。

- 2023年2月,新加坡网路营运商M1与StarHub组成名为Antina的联盟。两家公司已延长与诺基亚的协议,以改善全国范围内的室内和室外 5G 覆盖范围。为了提供具有高频宽、极快速度和最小延迟的更好的 5G 用户体验,诺基亚将安装小型基地台解决方案,以使用 MIMO(多输入、多输出)自适应天线覆盖新建筑。

无线连接晶片组产业概览

无线连接晶片组市场较为分散,参与的公司众多,包括博通公司、高通公司、联发科公司、英特尔公司和德州仪器公司。此外,公司还透过推出新产品、业务扩张、策略合併、联盟和收购来扩大其市场影响力。

- 2023 年 6 月:博通推出第二代 Wi-Fi 7 晶片组。 BCM47722 是一款住宅Wi-Fi 7网路基地台晶片,具有双物联网无线电,支援低功耗蓝牙 (BLE)、Zigbee、 网路基地台和 Matter通讯协定操作;BCM4390是一款专为行动装置设计的低功耗Wi-Fi 7、蓝牙和802.15.4复合晶片。 BCM47722 企业 Wi-Fi 7网路基地台SoC 规格支援无线连线。

- 2023 年 4 月:德州仪器推出其最新的 SimpleLink 系列,这是一系列 Wi-Fi 6伴同性积体电路 (IC)。这些 IC 旨在帮助设计人员创建强大、安全且高效的 Wi-Fi 连接,特别适合高密度或高达 105 度C的高温环境中的应用。 TI CC33xx 系列的首批成员在单一 IC 上同时支援 Wi-Fi 6 和低功耗蓝牙 5.3。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 评估宏观经济趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 透过家庭自动化实现连网家庭的需求不断增加

- 家庭和企业的网路普及率不断提高

- 市场问题

- 与资料安全和隐私、设备连接和互通性相关的问题

- 部分行动装置需求低迷

第六章市场区隔

- 按类型

- Wi-Fi 独立

- 蓝牙独立

- Wifi 和蓝牙组合

- 低功耗无线IC

- 按最终用户应用程式

- 消费者

- 企业

- 行动装置

- 车

- 工业的

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Broadcom Inc.

- Qualcomm Incorporated

- Mediatek Inc.

- Intel Corporation

- Texas Instruments Incorporated

- STMicroelectronics NV

- NXP Semiconductors NV

- On Semiconductor Corporation

- Infineon Technologies AG

- Microchip Technology Inc.

- Qorvo Inc.

- Skyworks Solutions Inc.

- Hisilicon Technologies Co. Ltd

- Tsinghua Unigroup Co. Ltd(unisoc(Shanghai)Technologies Co. Ltd)

8.供应商市场占有率分析

第九章投资分析

第十章:投资分析市场的未来

The Wireless Connectivity Chipset Market size is estimated at USD 9.23 billion in 2025, and is expected to reach USD 13.79 billion by 2030, at a CAGR of 8.36% during the forecast period (2025-2030).

Key Highlights

- With the growing penetration of high-speed internet, the adoption of connected devices and smart home applications is increasing, especially in regions such as Europe, North America, and Asia-Pacific. Some major solutions include voice assistants, smart thermostats, smart lighting, security cameras, and smart appliances.

- Further, in May 2024, MediaTek announced the debut of two new chipsets with powerful performance and support for the latest AI enhancements across multiple verticals. These included the Kompanio 838 SoC for premium Chromebooks and the Pentonic 800 SoC for 4K premium smart TVs and displays. The company highlighted major developments in product categories such as AI, automotive, IoT, TVs, Chromebooks, and wireless connectivity.

- For instance, the IMT-2030 (6G) Promotion Group was formed in China to speed up the R&D of 6G technology. Around 2030, the world is anticipated to witness the commercialization of 6G. China is leading the charge in supporting the commercialization of 5G, which will provide a solid basis for developing 6G.

- Adding several devices, such as in IoT, increases the surface area of a network, creating more potential attack vectors in the process. Even a single unsecured device connected to a network may serve as a point of entry for an active attack on the network.

- According to the Organisation for Economic Co-operation and Development survey, by 2025, the number of households with computers is anticipated to increase to 1,262.47 million. Homes with at least one computer are referred to as computer households. Such a massive boost in computer adoption will create an opportunity for the market players to expand their Wi-Fi chipset product portfolio, expand their presence in different regions, and advance their market share.

- Various players in the market are developing new products to stay competitive, which may further propel market growth. For instance, in November 2023, MediaTek, an early pioneer in Wi-Fi 7 technology, solidified its position as a market leader with the launch of its latest offerings, the Filogic 860 and Filogic 360. These additions significantly expanded MediaTek's cutting-edge product line, emphasizing the latest connectivity technologies for superior performance and unwavering reliability.

- The Filogic 860 chipsets, featuring a dual-band access point and an advanced network processor, are tailored for enterprise access points, service provider gateways, mesh nodes, and various retail and IoT router applications. On the other hand, the Filogic 360 facilitates Wi-Fi 7 2x2 capabilities and dual Bluetooth 5.4 radios in a single chip. This design is specifically crafted to bring next-gen Wi-Fi 7 connectivity to edge and streaming devices, as well as a wide range of consumer electronics.

- High costs associated with developing and producing advanced Wi-Fi chipsets pose a significant challenge in the market. The sophisticated and expensive technology needed for manufacturing these chipsets inflates the final product's cost, potentially hindering adoption, especially among price-sensitive consumers.

- Post-COVID-19, there was a shift to opting for digital modes for relevant meetings and discussions while focusing more on adopting collaborative tools. Furthermore, emerging use cases for 5G, including the need to support increasing numbers of individuals schooling and working from home, are expected to drive 5G investment. In addition, many workplaces have adopted a hybrid model of working, for which 5G connections can be deployed for better connectivity. Such cases have positively driven the market despite the disruptions caused due to shortages in the supply chain.

Wireless Connectivity Chipset Market Trends

Wi-Fi Standalone Holds the Maximum Share of the Market

- The evolution of Wi-Fi network technology allows users to experience faster speeds and lower latency. It boosted the use of data-heavy services and applications. The significant rise in the volume of data carried by Wi-Fi networks has been primarily driven by customer demand for video and business and consumer moves to cloud services. This factor is expected to drive the need for a wireless 5G connection with fast and high-capacity networks.

- Internet penetration has scaled up in the modern world. According to the International Telecommunication Union, as of 2023, the estimated number of internet users worldwide was 5.4 billion, up from 5.1 billion in the previous year. This share represented 67% of the global population.

- According to a report from Snapchat, by 2025, around 75% of the global population and almost all smartphone users will be frequent AR technology users, out of which more than 1.5 billion are anticipated to be millennials. According to GSMA's Mobile Economy China, China will add around 340 million smartphone connections by 2025, with adoption rising to 9 in 10 connections, 1.5 billion in Mainland China, 12.3 million in Hong Kong, 1.9 million in Macao, and 25.7 million in Taiwan.

- In February 2024, Stage X, a South Korean company, announced that it was awarded a spectrum that will enable it to be the nation's fourth mobile carrier and planned to launch nationwide mobile network services in the first half of 2025. The company invested USD 462 million (KRW 612.8 billion) to deploy its 28 GHz 5G network across South Korea with a plan to build 6,000 base stations; it also involved the mandated installation standard for the 28 GHz frequency network.

- According to Ericsson's Mobility Report, the monthly average usage of mobile data in North America is expected to reach 49 GB per month for smartphones in 2026. A smartphone-savvy consumer base, video-rich applications, and large data plans will drive traffic growth. While there may be robust growth in traffic per smartphone in the near term, the adoption of immersive consumer 5G connections utilizing AR and VR is expected to lead to an even better growth rate in the long term.

- Lower latency is also poised to enable high-speed virtual and augmented reality video without glitches or delays. Mobile connectivity can be strengthened with small cell infrastructure, densifying 5G wireless signals and improving their movement through concrete buildings and walls. Small-cell antennas will also enhance wireless connection, supporting more devices on the same network simultaneously. Such developments are expected to drive the market.

Asia-Pacific is Expected to be the Fastest-growing Market

- The advent of 5G in the Asia-Pacific region accelerated wireless connectivity chipset deployment for high-speed network connectivity. Japan's government granted permission to install 5G base stations on 208,000 traffic lights across the country. Local administrations and operators shared the costs of using the traffic lights for 5G deployments. This will help with more solution deployment in less time, thereby circulating 5G connectivity faster throughout the country.

- Various Indian multinational educational technology companies, such as Byju's, provide their students with a tablet as a part of their educational curriculum to educate the students via digital methods along with the traditional methods of teaching. Such initiatives by the companies in the market are expected to promote further the demand for tablets, smartphones, and other consumer electronics in the market, thereby driving the market for wireless connectivity chipsets for tablets in the region during the forecast period.

- The increasing demand for internet services in the Asia-Pacific region is also expected to promote the adoption of wireless connectivity chipsets in the region. As per the prime minister of India, the launch of 5G internet services in India is expected to bring new economic possibilities and societal benefits to the nation.

- In addition, China is leading 5G development on a worldwide scale. More than 2.54 million 5G base stations have been built nationwide, and more than 575 million people now own 5G smartphones. The country further plans to invest CNY 1.2 trillion (USD 174.2 billion) in 5G network construction by 2025. This growing demand for a 5G stable network is accelerating the deployment of small-cell solutions in the country.

- Due to the increasing availability and affordability of 5G smartphones and the rapid adoption of smartphones in metropolitan and rural areas, 5G subscriptions are expected to rapidly increase to reach approximately 50 million in the region by the end of 2023.

- In February 2023, Network operators M1 and StarHub in Singapore formed an alliance named Antina. They extended their contract with Nokia to improve indoor and outdoor 5G coverage nationwide. To provide a better 5G user experience with high bandwidth, breakneck speeds, and minimal latency, Nokia will install its small cell solution called airscale indoor radio (ASiR), covering new buildings with multiple input, multiple outputs (MIMO) adaptive antennas.

Wireless Connectivity Chipset Industry Overview

The wireless connectivity chipset market is fragmented, with many players like Broadcom Inc., Qualcomm Incorporated, Mediatek Inc., Intel Corporation, and Texas Instruments Incorporated. The companies are also increasing their market presence by introducing new products, expanding their operations, and entering strategic mergers, partnerships, and acquisitions.

- June 2023: Broadcom unveiled its second-generation Wi-Fi 7 chipsets: the BCM6765 residential Wi-Fi 7 access point chip, the BCM47722 enterprise Wi-Fi 7 access point chip with dual IoT radios that support operation for Bluetooth Low Energy (BLE), Zigbee, Thread, and Matter protocols, and the BCM4390 low-power Wi-Fi 7, Bluetooth, and 802.15.4 combo chip designed for use in mobile devices. BCM47722 enterprise Wi-Fi 7 access point SoC specifications allow wireless connectivity.

- April 2023: Texas Instruments unveiled its latest SimpleLink family, a line of Wi-Fi 6 companion integrated circuits (ICs). These ICs are designed to empower designers to create robust, secure, and efficient Wi-Fi connections, particularly for applications in high-density or high-temperature settings, reaching up to 105 °C. The initial offerings from TI's CC33xx family cater to both Wi-Fi 6 and Bluetooth Low Energy 5.3, all within a single IC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Connected Homes Through Home Automation

- 5.1.2 Increasing Internet Penetration into Homes and Enterprises

- 5.2 Market Challenges

- 5.2.1 Issues Related to Security and Privacy of Data and Connectivity of Devices and Interoperability

- 5.2.2 Slow Demand for Some Mobile Handset Types

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Wi-Fi Standalone

- 6.1.2 Bluetooth Standalone

- 6.1.3 Wifi and Bluetooth Combo

- 6.1.4 Low-power Wireless IC

- 6.2 By End-user Application

- 6.2.1 Consumer

- 6.2.2 Enterprise

- 6.2.3 Mobile Handsets

- 6.2.4 Automotive

- 6.2.5 Industrial

- 6.2.6 Other End-user Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Broadcom Inc.

- 7.1.2 Qualcomm Incorporated

- 7.1.3 Mediatek Inc.

- 7.1.4 Intel Corporation

- 7.1.5 Texas Instruments Incorporated

- 7.1.6 STMicroelectronics NV

- 7.1.7 NXP Semiconductors NV

- 7.1.8 On Semiconductor Corporation

- 7.1.9 Infineon Technologies AG

- 7.1.10 Microchip Technology Inc.

- 7.1.11 Qorvo Inc.

- 7.1.12 Skyworks Solutions Inc.

- 7.1.13 Hisilicon Technologies Co. Ltd

- 7.1.14 Tsinghua Unigroup Co. Ltd (unisoc (Shanghai) Technologies Co. Ltd

8 VENDOR MARKET SHARE ANALYSIS

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

无线连接市场:按技术类型、组件、应用和最终用户划分 - 2026-2032年全球市场预测

无线连接市场:按技术类型、组件、应用和最终用户划分 - 2026-2032年全球市场预测 2026年全球无线连接市场报告

2026年全球无线连接市场报告 无线连接市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形式、设备、部署类型及最终用户划分

无线连接市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形式、设备、部署类型及最终用户划分 日本无线接取市场报告:按技术、网路类型、最终用户和地区划分(2026-2034年)

日本无线接取市场报告:按技术、网路类型、最终用户和地区划分(2026-2034年) 无线连接市场规模、份额和成长分析(按类型、最终用途和地区划分)—2026-2033年产业预测

无线连接市场规模、份额和成长分析(按类型、最终用途和地区划分)—2026-2033年产业预测 无线连接市场-全球产业规模、份额、趋势、机会及预测(按技术、终端用户产业、地区和竞争格局划分,2020-2030 年预测)

无线连接市场-全球产业规模、份额、趋势、机会及预测(按技术、终端用户产业、地区和竞争格局划分,2020-2030 年预测) 无线连接晶片组市场-2025-2030年预测

无线连接晶片组市场-2025-2030年预测 无线物联网连接晶片组市场:2025-2030

无线物联网连接晶片组市场:2025-2030 无线连线的市场资料概要:2025年第3季

无线连线的市场资料概要:2025年第3季 2032 年桥接晶片市场预测:按类型、功能、配置、技术、应用、最终用户和地区进行的全球分析

2032 年桥接晶片市场预测:按类型、功能、配置、技术、应用、最终用户和地区进行的全球分析