|

市场调查报告书

商品编码

1693659

电动公车:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Electric Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

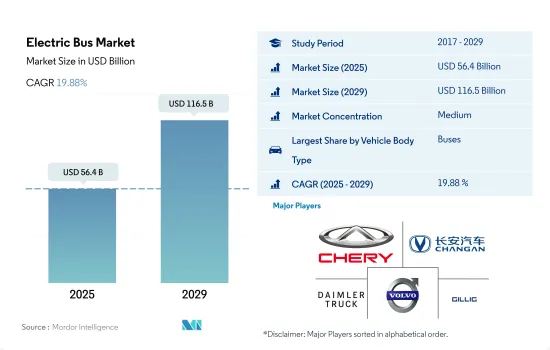

电动公车市场规模预计在 2025 年为 564 亿美元,预计到 2029 年将达到 1,165 亿美元,预测期内(2025-2029 年)的复合年增长率为 19.88%。

由于环境问题、燃料成本上升以及更严格的绿色汽车法规,全球对电动公车的需求正在强劲增长。

- 近年来,全球对电动公车的需求大幅成长。这种激增是由于二氧化碳排放、燃料成本上升、营运成本高以及世界各国政府实施严格的绿色汽车法规所导致的对环境问题的日益关注。因此,2022 年全球对电动公车的需求与 2021 年相比显着增加。

- 多个国家的公共交通管理部门正在积极支持电动公车的推广。例如,印度最大的公共交通巴士营运商班加罗尔都市运输公司(BMTC)宣布了雄心勃勃的电动巴士计画。卡纳塔克邦政府的目标是到 2030 年将所有 6,500 辆 BMTC 公车转变为零排放汽车。这些倡议可望提振全球对电动公车的需求和销售量。

- 世界各地的政府机构越来越多地采用电动公车。在美国,这一趋势很明显,越来越多的城市和大学正在引入电动公车。值得注意的是,加州已成为这项转型中的领跑者,实施了创新清洁交通规则(ICTR)。该规定要求,新购公车的25%必须是零排放公车,并设定目标到2029年从加州交通机构订单100%零排放公车的订单。加州的目标是到2040年,所有12,000辆城市公车都实现电动化。其他国家也正在采取类似倡议,预计2024年至2030年间,电动公车的需求将会成长。

全球电动公车市场趋势

全球需求成长和政府支持将推动电动车市场成长

- 电动车(EV)已成为汽车产业的重要组成部分,因为它具有提高能源效率、减少温室气体和污染排放的潜力。这种快速成长背后的主要因素是日益增长的环境问题和政府的支持。其中,电动车全球销售呈现强劲成长势头,2022年较2021年成长10.82%。据预测,2025年底,电动乘用车年销量将超过500万辆,约占汽车总销量的15%。

- 领先的製造商和组织(例如伦敦警察厅和消防队)正在积极推行电动车策略。例如,该公司设定了在 2025 年实现零排放汽车、在 2030 年实现 40% 货车电气化、到 2040 年实现全电动化的目标。预计全球也将出现类似的趋势,2024 年至 2030 年间电动车的需求和销售量将急剧成长。

- 在电池技术和汽车电气化进步的推动下,亚太地区和欧洲有望主导电动车生产。 2020年5月,起亚汽车欧洲公司公布“S计划”,宣布转向电动化策略。这项决定是在起亚电动车在欧洲创下销售纪录之际做出的。起亚雄心勃勃地计划在 2025 年之前在全球推出 11 款电动车,涵盖轿车、SUV 和 MPV 等各个领域。该公司的目标是到 2026 年实现全球电动车年销量达到 50 万辆。

电动公车产业概况

电动公车市场适度整合,前五大企业占48.55%。市场的主要企业有:奇瑞汽车、重庆长安汽车股份有限公司、戴姆勒卡车控股股份公司、沃尔沃集团和浙江吉利控股集团(按字母顺序排列)

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 人口

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 人均GDP

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 消费者汽车购买支出(cvp)

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 通货膨胀率

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 汽车贷款利率

- 共乘

- 共乘

- 电气化的影响

- 电动车充电站

- 电池组价格

- 非洲

- 亚太地区

- 欧洲

- 中东

- 北美洲

- 南美洲

- 新款 Xev 车型发布

- 燃油价格

- OEM生产统计

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 燃料类别

- BEV

- FCEV

- HEV

- PHEV

- 地区

- 非洲

- 南非

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 欧洲

- 法国

- 德国

- 义大利

- 西班牙

- 英国

- 其他欧洲国家

- 中东

- 阿拉伯聯合大公国

- 其他中东地区

- 北美洲

- 加拿大

- 墨西哥

- 美国

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地区

- 非洲

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Anhui Ankai Automobile Co. Ltd.

- Ashok Leyland Limited

- Byd Auto Industry Company Limited

- Chery Automobile Co. Ltd.

- Chongqing Changan Automobile Company Limited

- CRRC Electric Vehicle Co. Ltd.

- Daimler Truck Holding AG

- King Long United Automotive Industry Co. Ltd.

- NFI Group Inc.

- Proterra INC.

- Tata Motors Limited

- Volvo Group

- Zhejiang Geely Holding Group Co. Ltd

- Zhengzhou Yutong Bus Co. Ltd.

- Zhongtong Bus Holding Co. Ltd.

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 93052

The Electric Bus Market size is estimated at 56.4 billion USD in 2025, and is expected to reach 116.5 billion USD by 2029, growing at a CAGR of 19.88% during the forecast period (2025-2029).

The global demand for electric buses is experiencing significant growth due to environmental concerns, rising fuel costs, and stringent green vehicle regulations

- The global demand for electric buses has surged significantly in recent years. This uptick can be attributed to mounting environmental concerns stemming from carbon emissions, escalating fuel costs, the burden of high operational expenses, and the imposition of stringent green vehicle regulations by governments worldwide. Consequently, the global demand for electric buses saw a notable increase in 2022 compared to 2021.

- Public transit agencies in several nations are actively championing the adoption of electric buses. For instance, the Bangalore Metropolitan Transport Corporation (BMTC), India's largest public transit bus operator, has unveiled ambitious plans for battery electric buses. It has committed to procuring up to 1,800 electric buses in the coming years, while the Karnataka state government aims to transition BMTC's entire fleet of 6,500 buses to zero-emission vehicles by 2030. Such initiatives are poised to bolster the global demand and sales of electric buses.

- Government bodies worldwide are increasingly embracing electric buses. In the United States, the trend is evident as more cities and universities are incorporating electric bus fleets. Notably, California emerged as a frontrunner in this transition, introducing the Innovative Clean Transit Rule (ICTR). This rule mandates that 25% of new bus purchases be zero-emission buses, with a subsequent target of 100% zero-emission orders from California transport agencies by 2029. California aims to electrify its entire fleet of 12,000 city buses by 2040. Similar endeavors in other nations are poised to fuel the demand for electric buses from 2024 to 2030.

Global Electric Bus Market Trends

The rising global demand and government support propel electric vehicle market growth

- Electric vehicles (EVs) have become indispensable in the automotive industry, driven by their potential to enhance energy efficiency and reduce greenhouse gas and pollution emissions. This surge is primarily attributed to growing environmental concerns and supportive government initiatives. Notably, global EV sales witnessed a robust 10.82% growth in 2022 compared to 2021. Projections indicate that annual sales of electric passenger cars will surpass 5 million by the end of 2025, accounting for approximately 15% of total vehicle sales.

- Leading manufacturers and organizations, like the London Metropolitan Police & Fire Service, have been actively pursuing their electric mobility strategies. For instance, they have set a target of a zero-emission fleet by 2025, with a goal of electrifying 40% of their vans by 2030 and achieving full electrification by 2040. Similar trends are expected globally, with the period from 2024 to 2030 witnessing a surge in demand and sales of electric vehicles.

- Asia-Pacific and Europe are poised to dominate electric vehicle production, driven by their advancements in battery technology and vehicle electrification. In May 2020, Kia Motors Europe unveiled its "Plan S," signaling a strategic shift toward electrification. This decision came on the heels of record-breaking sales of Kia's EVs in Europe. Kia has ambitious plans to introduce 11 EV models globally by 2025, spanning various segments like passenger vehicles, SUVs, and MPVs. The company aims to achieve annual global EV sales of 500,000 by 2026.

Electric Bus Industry Overview

The Electric Bus Market is moderately consolidated, with the top five companies occupying 48.55%. The major players in this market are Chery Automobile Co. Ltd., Chongqing Changan Automobile Company Limited, Daimler Truck Holding AG, Volvo Group and Zhejiang Geely Holding Group Co. Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.1.1 Africa

- 4.1.2 Asia-Pacific

- 4.1.3 Europe

- 4.1.4 Middle East

- 4.1.5 North America

- 4.1.6 South America

- 4.2 GDP Per Capita

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.3.1 Africa

- 4.3.2 Asia-Pacific

- 4.3.3 Europe

- 4.3.4 Middle East

- 4.3.5 North America

- 4.3.6 South America

- 4.4 Inflation

- 4.4.1 Africa

- 4.4.2 Asia-Pacific

- 4.4.3 Europe

- 4.4.4 Middle East

- 4.4.5 North America

- 4.4.6 South America

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Shared Rides

- 4.8 Impact Of Electrification

- 4.9 EV Charging Station

- 4.10 Battery Pack Price

- 4.10.1 Africa

- 4.10.2 Asia-Pacific

- 4.10.3 Europe

- 4.10.4 Middle East

- 4.10.5 North America

- 4.10.6 South America

- 4.11 New Xev Models Announced

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Fuel Category

- 5.1.1 BEV

- 5.1.2 FCEV

- 5.1.3 HEV

- 5.1.4 PHEV

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 South Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 China

- 5.2.2.2 India

- 5.2.2.3 Japan

- 5.2.2.4 South Korea

- 5.2.3 Europe

- 5.2.3.1 France

- 5.2.3.2 Germany

- 5.2.3.3 Italy

- 5.2.3.4 Spain

- 5.2.3.5 UK

- 5.2.3.6 Rest-of-Europe

- 5.2.4 Middle East

- 5.2.4.1 UAE

- 5.2.4.2 Rest-of-Middle East

- 5.2.5 North America

- 5.2.5.1 Canada

- 5.2.5.2 Mexico

- 5.2.5.3 US

- 5.2.6 South America

- 5.2.6.1 Argentina

- 5.2.6.2 Brazil

- 5.2.6.3 Rest-of-South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Anhui Ankai Automobile Co. Ltd.

- 6.4.2 Ashok Leyland Limited

- 6.4.3 Byd Auto Industry Company Limited

- 6.4.4 Chery Automobile Co. Ltd.

- 6.4.5 Chongqing Changan Automobile Company Limited

- 6.4.6 CRRC Electric Vehicle Co. Ltd.

- 6.4.7 Daimler Truck Holding AG

- 6.4.8 King Long United Automotive Industry Co. Ltd.

- 6.4.9 NFI Group Inc.

- 6.4.10 Proterra INC.

- 6.4.11 Tata Motors Limited

- 6.4.12 Volvo Group

- 6.4.13 Zhejiang Geely Holding Group Co. Ltd

- 6.4.14 Zhengzhou Yutong Bus Co. Ltd.

- 6.4.15 Zhongtong Bus Holding Co. Ltd.

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

电池驱动电动巴士市场:机会、成长要素、产业趋势分析以及 2026 年至 2035 年的预测。

电池驱动电动巴士市场:机会、成长要素、产业趋势分析以及 2026 年至 2035 年的预测。 欧洲电动巴士:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲电动巴士:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球电动巴士市场规模、份额、趋势和成长分析报告(2026-2034年)全球电池驱动电动巴士市场规模、份额、趋势和成长分析报告(2026-2034)燃料电池电动巴士全球市场规模、份额、趋势和成长分析报告(2026-2034)

全球电动巴士市场规模、份额、趋势和成长分析报告(2026-2034年)全球电池驱动电动巴士市场规模、份额、趋势和成长分析报告(2026-2034)燃料电池电动巴士全球市场规模、份额、趋势和成长分析报告(2026-2034) 日本电动巴士市场规模、份额、趋势及预测(按动力方式、电池类型、车身长度、续航里程、电池容量和地区划分,2026-2034年)

日本电动巴士市场规模、份额、趋势及预测(按动力方式、电池类型、车身长度、续航里程、电池容量和地区划分,2026-2034年) 全球电动巴士市场:依电池类型、动力系统、应用、巴士尺寸、车身类型、充电方式、电池容量和地区划分 - 市场规模、市场动态、主要参与者、机会分析和预测(2026-2035年)

全球电动巴士市场:依电池类型、动力系统、应用、巴士尺寸、车身类型、充电方式、电池容量和地区划分 - 市场规模、市场动态、主要参与者、机会分析和预测(2026-2035年) 全球电动铰接式城市公车市场:按推进技术、电池化学成分、充电方式、车辆长度和最终用户分類的预测(2026-2032年)按动力来源、传动方式、铰接长度、车门配置、应用和最终用户分類的铰接式城市公车市场,全球预测,2026-2032年按动力类型、车辆类型、服务类型、购买类型和最终用户分類的学前校车市场-全球预测(2026-2032 年)

全球电动铰接式城市公车市场:按推进技术、电池化学成分、充电方式、车辆长度和最终用户分類的预测(2026-2032年)按动力来源、传动方式、铰接长度、车门配置、应用和最终用户分類的铰接式城市公车市场,全球预测,2026-2032年按动力类型、车辆类型、服务类型、购买类型和最终用户分類的学前校车市场-全球预测(2026-2032 年)

▼