|

市场调查报告书

商品编码

1844646

中东和非洲的雷射雷达:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Middle East And Africa LiDAR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

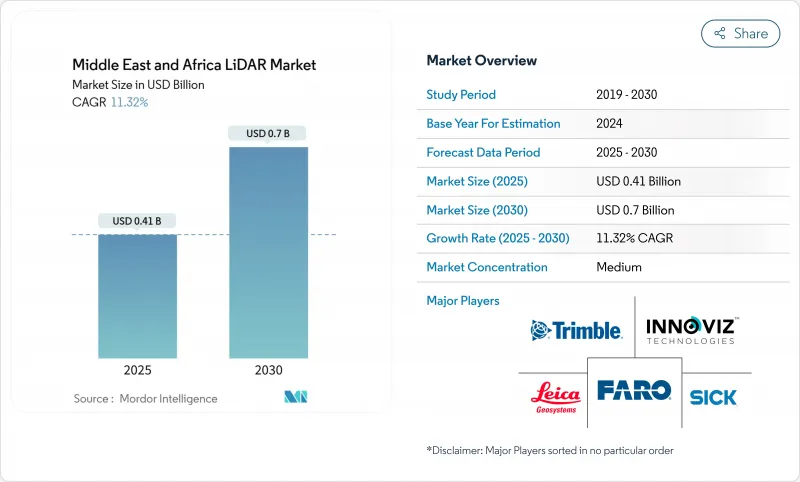

中东和非洲雷射雷达市场预计到 2025 年将达到 4.1 亿美元,到 2030 年将达到 7 亿美元,复合年增长率为 11.32%。

沙乌地阿拉伯「2030愿景」下计划的快速推进、海湾地区智慧城市计画的扩张以及南部非洲持续的基础设施支出,正在推动对高精度3D空间数据的需求。雷射雷达正越来越多地与人工智慧相结合,用于自动特征提取,从而缩短了施工监控和资产检查的计划週期。盖格模式感测器等固态技术的进步正在减小尺寸、重量、功耗和成本,使其能够部署在能够承受沙漠酷热和尘土的无人机上。汽车製造商正在将雷射雷达纳入高级驾驶辅助系统 (ADAS),以支持阿联酋到2030年将25%的城市出行转向自动驾驶汽车的计画。

中东和非洲 LiDAR 市场趋势与洞察

海湾合作委员会 (GCC) 智慧城市数位双胞胎强制使用光达

海湾国家政府目前要求对城市资产进行亚厘米级数位复製,这使得雷射雷达成为地下公用设施测绘、交通流量优化和碳足迹分析的关键技术。杜拜市政府正在利用行动扫描器对地下管道和电缆进行建模,以减少计划外停电和挖掘返工。在卡达,卢萨尔市政府耗资6000万美元的智慧城市平台处理持续的雷射雷达数据,以管理45万居民的服务。公共计划正在强制采用建筑资讯模型(BIM),其中雷射雷达点云资料直接流入标准化施工模型,从而消除资料格式瓶颈。由此产生的统一规划方法可以加快核准并减少生命週期成本超支。海湾合作委员会(GCC)当局也将雷射雷达采购与云端分析捆绑在一起,并鼓励当地资料中心遵守主权法规。

沙乌地阿拉伯计划中基于无人机的线路测量製图激增

像 NEOM 长达 170 公里的「线状城市」这样备受瞩目的项目,需要每週对大片区域进行地形更新,而传统测绘技术根本无法及时覆盖。配备中程光达的旋翼无人机现在每天可以绘製多达 100 英亩的地图,精度可达 1-3 厘米,将进度追踪週期缩短了 70%。像 Aeromotus 这样的专业承包商提供承包即服务套餐,将飞行计划、扫描和云端处理融为一体。由此产生的数位双胞胎使承包商能够将设计意图与竣工状况进行比较,从而能够及早发现土方工程的偏差。对于高速铁路支线和海水淡化管道等线性基础设施,快速的走廊更新可以减少变更单的频率,并满足交付里程碑。

缺乏本地校准实验室延长了前置作业时间

由于利雅德和约翰尼斯堡之间仅有少数几家获得认证的实验室,大多数业者被迫将感测器送往欧洲进行年度重新校准。物流延误可能长达12週,导致施工高峰期的车队运转率降低。大型承包商的应对措施是从ClearSkies Geomatics等供应商租用预校准设备。瓶颈问题也阻碍了先进固态雷射雷达的普及,这类设备通常需要较短的服务週期才能保持保证的规格。一些海湾自由区已宣布为外国称重设备製造商开设分店提供激励措施,但预计要到2027年才能实现有效产能。

細項分析

到2024年,机载平台将占据中东和非洲雷射雷达市场规模的55%,这得益于其能够勘测干旱地区大型计划的足迹。沙乌地阿拉伯的工程公司使用直升机和固定翼宣传活动每週更新挖填工程量,并透过仪表板标记进度延误。倾斜摄影测量结合密集点云数据,可视觉化影响道路走向的岩壁和沙漠干谷。航空扫描技术也有助于监测纳米比亚的海岸侵蚀,利用绿色波长雷射脉衝测量旅游海滩沿岸的流动沙丘。

地面扫描仪的市占率较小,但随着市政当局对下水道、桥樑和历史建筑建筑幕墙数位化,其复合年增长率将达到14.11%。穿戴式系统无需GPS即可绘製多层隧道地图,使检查员能够检测瓷砖后面剥落的混凝土。中东和非洲的雷射雷达市场正受益于即时记录扫描数据的SLAM演算法,这使得碰撞检测报告能够在一夜之间发布,而之前需要一周时间。微型硬体现在允许两名工人在一夜之间捕捉整个地铁站,从而使顶级承包商以外的人也能获得高精度文件。

飞行时间(ToF) 相机占 2024 年销售额的 63%,这得益于其在阿拉伯半岛尘土飞扬的风和强烈阳光下的出色表现。电力公司正在采用 ToF 设备进行电力线路走廊的间隙检查,以避免因植被相关的停电而导致炼油厂停产。此外,供应商的蓝图还包括推出人眼安全的 1550 nm 雷射器,其作用距离超过 3 公里,从而扩大其在露天矿边坡分析中的应用。

盖格模式感测器的预期复合年增长率为 13.11%,而超高点密度技术则加速了环境建模。加蓬森林碳计划利用此技术来优化生物量估算。高空作业支援 366 平方公里/小时的覆盖范围,只需一次飞机飞行即可完成全国范围的 DEM 更新。正在进行的压缩感知研究预计将在不增加资料量的情况下将解析度提高 64 倍,使其适用于即时洪水模拟。

中东和非洲光达市场份额报告按产品(机载光达、地基光达、其他)、技术(飞行时间、盖格模式、其他)、组件(雷射扫描仪、GPS、其他)、部署平台(基于无人机、其他)、测量范围(短程、其他)、终端行业(工程、其他)和国家(沙乌地阿拉伯、其他)细分。市场规模和预测以美元计算。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 海湾合作委员会 (GCC) 智慧城市数位双胞胎强制使用光达

- 沙乌地阿拉伯计划中基于无人机的线路测量製图激增

- 纳米比亚和南非离岸风力发电的水深测量需求

- 阿联酋关键地点的安全主导週边监控

- 铜金露天矿高解析度地形测量

- 尼罗河流域气候变迁适应洪氾区模型

- 市场限制

- 缺乏本地校准实验室会增加前置作业时间

- 非海湾合作委员会非洲国家 3B 类雷射进口关税

- 海湾国家以外的 GNSS 参考站密度低

- 北非衝突后公共部门资本支出低

- 价值/供应链分析

- 监管和技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 投资分析

第五章市场规模及成长预测

- 按产品

- 机载光达

- 机械扫描

- 固体扫描

- 依技术

- 地基光达

- 飞行时间

- 盖格模式

- 相移

- 闪光雷射雷达

- 按组件

- 雷射扫描仪

- GPS/GNSS接收器

- 惯性测量单元

- 摄影机和 MEMS 镜

- 其他组件

- 按部署平台

- 地面型静力三脚架

- 基于无人机/无人驾驶飞机

- 移动式製图(车载)

- 水深测量/航空水文测量

- 按距离

- 短距离

- 中距离

- 远距

- 按行业

- 工程与建筑

- 石油和天然气

- 航太/国防

- 汽车和ADAS

- 采矿和采石业

- 农业/林业

- 按国家

- 沙乌地阿拉伯

- 卡达

- 科威特

- 阿拉伯聯合大公国

- 南非

- 肯亚

- 其他中东和非洲地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Leica Geosystems AG

- Sick AG

- Ouster Inc.

- Cepton Technologies Inc.

- Hexagon AB

- MENA 3D

- Sandvik Mining and Rock Solutions

- Trimble Inc.

- FARO Technologies Inc.

- RIEGL Laser Measurement Systems

- Quanergy Systems Inc.

- LightWare LiDAR LLC

- GlobalScan Technologies LLC

- Microdrones GmbH

- Innoviz Technologies Ltd

- Velodyne Lidar Inc.

- Teledyne Optech

- Topcon Positioning Group

- Falcon-3D

- Sitech Gulf

- DJI Enterprise

第七章 市场机会与未来展望

The Middle East and Africa LiDAR market stands at USD 0.41 billion in 2025 and is projected to reach USD 0.7 billion by 2030, reflecting an 11.32% CAGR.

Rapid rollout of giga-projects under Saudi Vision 2030, expanding smart-city programs across the Gulf, and sustained infrastructure spending in Southern Africa are intensifying demand for high-precision, three-dimensional spatial data. Increased pairing of LiDAR with artificial intelligence for automated feature extraction is shortening project cycles in construction monitoring and asset inspection. Solid-state advances such as Geiger-mode sensors are reducing size, weight, power, and cost, enabling deployment on drones that can tolerate harsh desert heat and dust. Automotive original-equipment manufacturers are incorporating LiDAR into advanced driver assistance systems, supported by the UAE plan that requires 25% of city journeys to shift to autonomous vehicles by 2030.

Middle East And Africa LiDAR Market Trends and Insights

LiDAR Mandate for Smart-City Digital Twins in GCC

Gulf governments now require sub-centimeter digital replicas of city assets, making LiDAR indispensable for underground-utility mapping, traffic-flow optimisation, and carbon-footprint analysis. Dubai Municipality is applying mobile scanners to model buried pipes and cables, cutting unplanned outages and excavation re-works. In Qatar, a USD 60 million smart-city platform for Lusail City processes continuous LiDAR feeds to manage 450,000 residents' services. Mandatory BIM adoption in public projects ensures that LiDAR point clouds flow directly into standardised construction models, removing data-format bottlenecks. The result is a unified planning approach that speeds permit approvals and reduces lifecycle cost overruns. GCC authorities also bundle LiDAR procurement with cloud analytics, encouraging local data-centres that comply with sovereignty rules.

Surge in UAV-Borne Corridor Mapping for Saudi Giga-Projects

High-profile programmes such as NEOM's 170 km linear city require weekly topographic updates over vast tracts that conventional surveys cannot cover in time. Rotary-wing drones equipped with medium-range LiDAR now map up to 100 acres per day at 1-3 cm accuracy, slashing progress-tracking cycles by 70%. Specialist operators like Aeromotus supply turnkey drone-as-a-service packages that combine flight planning, scanning, and cloud processing. Resulting digital twins allow contractors to compare design intent with as-built conditions, catching earthwork deviations early. For linear infrastructure such as high-speed rail spines and desalination pipelines, rapid corridor updates reduce change-order frequency and safeguard delivery milestones.

Scarcity of Regional Calibration Labs Inflating Lead-Times

Only a handful of accredited laboratories exist between Riyadh and Johannesburg, forcing most operators to ship sensors to Europe for annual recalibration. Logistics lags can stretch to 12 weeks, freezing fleet availability during peak construction phases. Larger contractors respond by leasing pre-calibrated units from providers such as ClearSkies Geomatics, while smaller firms idle crews and absorb liquidated damages. The bottleneck also hampers adoption of advanced solid-state LiDAR, which often requires shorter service cycles to uphold warranty specifications. Several Gulf free-zones have announced incentives for foreign metrology houses to open branches, yet timelines suggest meaningful capacity will not arrive before 2027.

Other drivers and restraints analyzed in the detailed report include:

- Offshore Wind-Farm Bathymetry Needs Off Namibia and South Africa

- Security-Driven Perimeter Surveillance at UAE Critical Sites

- Limited GNSS Reference-Station Density Outside Gulf States

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aerial platforms generated 55% of the Middle East and Africa LiDAR market size in 2024, a position rooted in their ability to survey giga-project footprints that sprawl across arid terrains. Saudi engineering firms rely on helicopter and fixed-wing campaigns to update cut-and-fill quantities weekly, feeding dashboards that flag schedule slippage. The combination of oblique photogrammetry with high-density point clouds helps planners visualise rock-cut faces and desert wadis that influence road alignments. Aerial scanning also underpins coastal-erosion monitoring in Namibia, where green-wavelength laser pulses measure dune migration along tourist beaches.

Ground-based scanners, though holding a smaller share, are slated for 14.11% CAGR as municipalities digitise sewers, bridges, and heritage facades. Wearable systems map multistorey tunnels without GPS, letting inspectors detect spalling concrete behind tiles. The Middle East and Africa LiDAR market benefits from SLAM algorithms that register scans in real time, permitting overnight issuance of clash-detection reports that would once take a week. Hardware miniaturisation means a two-person crew can now capture an entire metro station in an evening, democratising high-precision documentation beyond tier-one contractors.

Time-of-Flight remained the workhorse with 63% revenue in 2024, prized for robust performance under dust-laden winds and intense solar glare typical of the Arabian Peninsula. Power utilities employ ToF units for corridor clearance checks on transmission lines, avoiding vegetation-related outages that could stall refinery production. Vendor roadmaps introduce eye-safe 1,550 nm lasers that extend range past 3 km, widening use in open-pit mine slope analysis.

Geiger-mode sensors post a 13.11% CAGR forecast because ultra-high-point densities accelerate environmental modelling. Forestry-carbon projects in Gabon use the technology to refine biomass estimates, an attractive quality as voluntary carbon markets tighten verification standards. Elevated altitude operation supports 366 km2/h coverage, enabling national-scale DEM refreshes on single aircraft sorties. Continued research into compressive sensing promises 64-fold resolution gains without heavier data volumes, enhancing suitability for real-time flood simulations.

Middle East and Africa LiDAR Market Share Report is Segmented by Product (Aerial LiDAR, Ground-Based and More), Technology (Time-Of-Flight, Geiger-Mode and More), Component (Laser Scanners, GPS and More), Deployment Platform (UAV-Based, and More), Range (Short-Range, and More), End-Use Industry (Engineering, and More), and Country (Saudi Arabia, and More). The Market Size and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Leica Geosystems AG

- Sick AG

- Ouster Inc.

- Cepton Technologies Inc.

- Hexagon AB

- MENA 3D

- Sandvik Mining and Rock Solutions

- Trimble Inc.

- FARO Technologies Inc.

- RIEGL Laser Measurement Systems

- Quanergy Systems Inc.

- LightWare LiDAR LLC

- GlobalScan Technologies LLC

- Microdrones GmbH

- Innoviz Technologies Ltd

- Velodyne Lidar Inc.

- Teledyne Optech

- Topcon Positioning Group

- Falcon-3D

- Sitech Gulf

- DJI Enterprise

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LiDAR mandate for smart-city digital twins in GCC

- 4.2.2 Surge in UAV-borne corridor mapping for Saudi giga-projects

- 4.2.3 Offshore wind-farm bathymetry needs off Namibia and South Africa

- 4.2.4 Security-driven perimeter surveillance at UAE critical sites

- 4.2.5 High-resolution topography for copper and gold open-pit mines

- 4.2.6 Climate-resilience flood-plain modelling across Nile basin

- 4.3 Market Restraints

- 4.3.1 Scarcity of regional calibration labs inflating lead-times

- 4.3.2 Customs duties on Class-3B laser imports in non-GCC Africa

- 4.3.3 Limited GNSS reference-station density outside Gulf states

- 4.3.4 Low public-sector CAPEX in post-conflict North Africa

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Aerial LiDAR

- 5.1.2 Mechanical Scanning

- 5.1.3 Solid-state Scanning

- 5.2 By Technology

- 5.2.1 Ground-based LiDAR

- 5.2.2 Time-of-Flight

- 5.2.3 Geiger-Mode

- 5.2.4 Phase-Shift

- 5.2.5 Flash LiDAR

- 5.3 By Component

- 5.3.1 Laser Scanners

- 5.3.2 GPS/GNSS Receiver

- 5.3.3 Inertial Measurement Unit

- 5.3.4 Cameras and MEMS Mirrors

- 5.3.5 Other Components

- 5.4 By Deployment Platform

- 5.4.1 Terrestrial Static Tripod

- 5.4.2 UAV-/Drone-based

- 5.4.3 Mobile Mapping (Vehicle-mounted)

- 5.4.4 Bathymetric/Airborne Hydrographic

- 5.5 By Range

- 5.5.1 Short-Range

- 5.5.2 Medium-Range

- 5.5.3 Long-Range

- 5.6 By End-Use Industry

- 5.6.1 Engineering and Construction

- 5.6.2 Oil and Gas

- 5.6.3 Aerospace and Defense

- 5.6.4 Automotive and ADAS

- 5.6.5 Mining and Quarrying

- 5.6.6 Agriculture and Forestry

- 5.7 By Country

- 5.7.1 Saudi Arabia

- 5.7.2 Qatar

- 5.7.3 Kuwait

- 5.7.4 United Arab Emirates

- 5.7.5 South Africa

- 5.7.6 Kenya

- 5.7.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Leica Geosystems AG

- 6.4.2 Sick AG

- 6.4.3 Ouster Inc.

- 6.4.4 Cepton Technologies Inc.

- 6.4.5 Hexagon AB

- 6.4.6 MENA 3D

- 6.4.7 Sandvik Mining and Rock Solutions

- 6.4.8 Trimble Inc.

- 6.4.9 FARO Technologies Inc.

- 6.4.10 RIEGL Laser Measurement Systems

- 6.4.11 Quanergy Systems Inc.

- 6.4.12 LightWare LiDAR LLC

- 6.4.13 GlobalScan Technologies LLC

- 6.4.14 Microdrones GmbH

- 6.4.15 Innoviz Technologies Ltd

- 6.4.16 Velodyne Lidar Inc.

- 6.4.17 Teledyne Optech

- 6.4.18 Topcon Positioning Group

- 6.4.19 Falcon-3D

- 6.4.20 Sitech Gulf

- 6.4.21 DJI Enterprise

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

光达市场:按类型、组件、技术、测量距离、最终用户和应用划分-2026-2032年全球市场预测

光达市场:按类型、组件、技术、测量距离、最终用户和应用划分-2026-2032年全球市场预测 光达测绘市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户和功能划分

光达测绘市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户和功能划分 2026年全球光达软体市场报告光达滤光片市场:按滤光片类型、波长、技术、应用和部署划分-2026-2032年全球预测

2026年全球光达软体市场报告光达滤光片市场:按滤光片类型、波长、技术、应用和部署划分-2026-2032年全球预测 光达技术市场:策略洞察与预测(2026-2031年)行动雷射扫描系统市场:按组件、扫描器类型、技术、应用和最终用户划分,全球预测,2026-2032年光达(LiDAR)市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,预测2026-2034年光达市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署、最终用户及解决方案划分铁路雷达和光达技术市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户、安装类型和解决方案划分2026-2034年全球光达市场规模、份额、趋势和成长分析报告

光达技术市场:策略洞察与预测(2026-2031年)行动雷射扫描系统市场:按组件、扫描器类型、技术、应用和最终用户划分,全球预测,2026-2032年光达(LiDAR)市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,预测2026-2034年光达市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署、最终用户及解决方案划分铁路雷达和光达技术市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户、安装类型和解决方案划分2026-2034年全球光达市场规模、份额、趋势和成长分析报告