|

市场调查报告书

商品编码

1850049

欧洲行销自动化软体市场:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Europe Marketing Automation Software Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

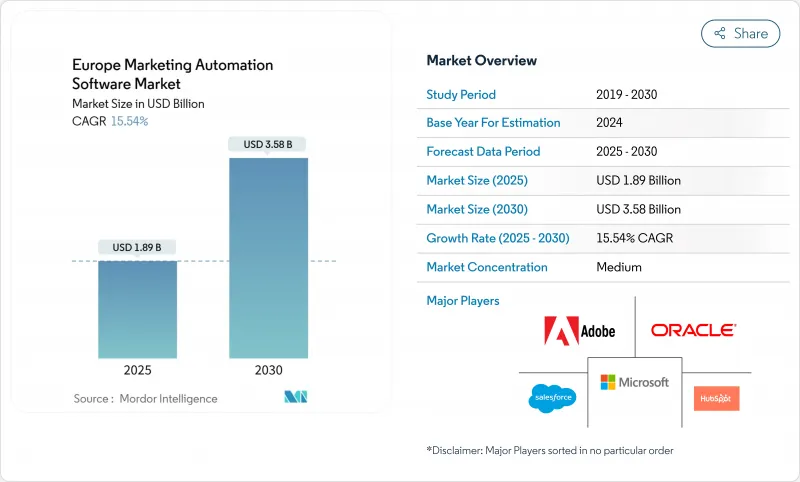

欧洲行销自动化软体市场预计到 2025 年将达到 18.9 亿美元,到 2030 年将达到 35.8 亿美元,在此期间的复合年增长率为 15.54%。

欧盟的「数位单一市场」计画旨在2030年实现75%的云端采用率,同时,79亿欧元(约85.5亿美元)的「数位欧洲计画」将透过津贴中小企业采用SaaS来支持近期云端技术的普及。同时,预计到2023年,该地区的电子商务经济规模将达到8,870亿欧元(约9,600亿美元),这将推动对以客户为中心的互动工具的需求,这些工具能够在遵守GDPR的同时实现精细化的个人化服务。随着全球平台供应商在欧洲不断扩张,竞争日益激烈,而本地专家则凭藉其多语言能力和监管方面的专业知识脱颖而出。儘管云端部署模式因其可扩展的合规管理而日益普及,但企业正迅速将支出转向将技术与精通GDPR的实施人才相结合的託管服务。德国18.5%的复合年增长率以及德语区(DACH)和北欧国家对人工智慧主导的个人化服务的重视,凸显了人工智慧准备度与行销自动化应用之间的连结。

欧洲行销自动化软体市场趋势与洞察

德国、奥地利和北欧地区电子商务中人工智慧驱动的个人化需求激增,正在推动市场发展。

人工智慧引擎正在德语区(德国、奥地利和瑞士)以及北欧零售业迅速普及,65%的高阶主管认为人工智慧将成为2025年核心成长要素。负责人正利用该地区先进的云端基础设施和较高的资料共用授权率来部署建议模型,从而提升转换率。 Telmore采用人工智慧主导的个人化策略后,销售额成长了11%,展现了可量化的投资报酬率,并正在加速同业的采用。 80%的公司计划增加人工智慧预算,但只有12%的公司能够证明其投资回报率,因此,拥有完善衡量框架的早期采用者正在获得竞争优势。德国公司正在利用生成式人工智慧来简化宣传活动创建和彙报流程,消除重复性任务,使员工能够专注于数据分析。因此,德语区和北欧地区将成为下一代个人化功能的试验场,这些功能随后将推广到整个欧洲。

欧盟数位单一市场倡议促进中小企业采用SaaS服务

79亿欧元(约85.5亿美元)的「数位欧洲」计画透过协调云端运算法规并资助设立欧洲数位创新中心提供实务指导,降低了中小企业的进入门槛。标准化API提高了资料可移植性,简化了不同行销应用程式之间的集成,并降低了供应商锁定风险。欧盟企业的云端运算采用率已达41%,预计2030年将达到75%。这些政策利好因素降低了中阶市场买家的合规复杂性,并扩大了欧洲行销自动化软体市场的潜在需求。

缺乏精通 GDPR 的行销自动化架构师

具备行销技术能力和法律洞察力的专业人才短缺,正日益阻碍实施计划的进展。银行业员工结构调整预示着数据专家的跨行业竞争加剧,此前,传统岗位的就业人数在2007年至2022年间下降了21%。中小企业受到的影响尤其严重,它们越来越依赖外部管理服务,这也解释了服务业16.1%的复合年增长率。欧洲数位创新中心的认证倡议带来了一定的缓解,但短期内的人才短缺仍将阻碍中小企业采用相关技术。

细分市场分析

儘管软体在2024年将占欧洲行销自动化软体市场收入的72%,但到2030年,託管服务将以16.1%的复合年增长率超越软体,凸显了企业倾向于将合规专业知识外包。服务的激增表明,企业对技术执行和监管检验的重视程度与对核心功能的重视程度不相上下。在软体领域,整合套件的表现优于独立工具,因为买家寻求的是资料隐私审核和人工智慧模型管治的单一资料资讯来源。专业服务在遗留系统整合和GDPR差距分析方面取得了成功,这使得顾问公司和系统整合成为供应商选择的安全隔离网闸。

对人工智慧立法日益严格的审查将促使企业更加重视从设计之初就融入审核的解决方案。供应商正将套装软体与咨询服务结合,以创造类似年金的收入模式。因此,欧洲行销自动化软体产业将出现混合型经营模式,将软体利润与高触感服务结合,以应对GDPR、PSD2以及特定产业义务等动态规则。

到2024年,云端解决方案将占据欧洲行销自动化软体市场78%的份额,这主要得益于欧盟对主权可信任云端框架的支持。云端采用率正以15.8%的复合年增长率成长,持续的平台更新使客户能够在无需大幅增加资本支出的情况下应对新的数据处理需求。行销团队可以利用弹性运算运行人工智慧模型,从而即时实现个人化的客户旅程。只有在公共和国防部门客户对资料驻留有严格要求的情况下,本地部署才仍然可行。

监管机构倾向于采用集中式云端控制平台,以支援自动化的授权日誌记录、违规通知和加密管理。这种监管一致性降低了用户感知到的风险,并促进了更广泛的云端迁移。 Oracle 和Oracle在欧盟安全云端区域的伙伴关係,展现了超大规模云端服务供应商如何透过在地化其技术堆迭来满足主权要求。随着云端迁移的成熟,云端供应商可能会在零信任架构和预认证 AI 沙箱等增值层展开竞争。

欧洲行销自动化软体市场按元件(软体、服务)、部署类型(云端基础、本地部署)、组织规模(中小企业、大型企业)、通路/功能(电子邮件行销、社群媒体行销、宣传活动管理等)、最终用户产业(零售/电子商务、银行、金融服务和保险等)以及国家进行细分。市场预测以美元计价。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 人工智慧驱动的个人化服务引领德语区和北欧地区的电子商务市场。

- 欧盟的数位单一市场倡议鼓励中小企业使用软体即服务(SaaS)。

- B2B科技中心采用帐户为基础的营销方式推动市场发展

- 欧洲金融服务领域的开放银行API整合推动市场发展

- 在分散的市场中编配多语言旅程

- 市场限制

- 精通 GDPR 的行销自动化架构师非常稀缺。

- 多语言个人化模组的总拥有成本较高

- 欧盟更严格的反垃圾邮件规则影响电子邮件的送达

- 价值链分析

- 监理展望

- 技术展望

- 评估市场宏观经济趋势

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按组件

- 软体

- 整合平台

- 独立工具

- 线索管理

- 社群媒体

- 电子邮件和分析

- 服务

- 专业服务

- 託管服务

- 软体

- 透过部署模式

- 云端基础的

- 本地部署

- 按公司规模

- 小型企业

- 大公司

- 按通道/功能

- 电子邮件行销

- 社群媒体行销

- 宣传活动管理

- 行动/简讯行销

- 入境内容行销

- 其他频道

- 按最终用户行业划分

- 零售与电子商务

- 银行、金融服务和保险业 (BFSI)

- 资讯科技和电信

- 製造业

- 医疗保健和生命科学

- 媒体与娱乐

- 政府和公共部门

- 其他终端用户产业

- 按国家/地区

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 荷兰

- 北欧国家

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Salesforce, Inc.

- Adobe Inc.(Marketo Inc.)

- HubSpot Inc.

- Oracle Corporation

- Microsoft Corporation

- SAP SE

- SAS Institute Inc.

- Act-On Software, Inc.

- Dotdigital Group PLC

- Force24 Ltd.

- ActiveCampaign LLC

- Mailchimp(Intuit Inc.)

- Sendinblue SAS(Brevo)

- GetResponse Sp. z oo

- Zoho Corporation

- Pipedrive OU

- SugarCRM Inc.

- Acoustic LP

- Iterable Inc.

- Klaviyo Inc.

第七章 市场机会与未来展望

The Europe marketing automation software market is valued at USD 1.89 billion in 2025 and is forecast to reach USD 3.58 billion by 2030, registering a brisk 15.54% CAGR across the period.

Ongoing EU Digital Single Market measures that target 75% cloud adoption by 2030, together with the EUR 7.9 billion (USD 8.55 billion) Digital Europe Programme, underpin near-term expansion by subsidizing SaaS adoption among small and medium-sized enterprises. Meanwhile, the region's EUR 887 billion (USD 960 billion) e-commerce economy in 2023 fuels demand for customer-centric engagement tools that remain compliant with GDPR while still delivering granular personalization. Competitive intensity is increasing as global platform vendors reinforce European footprints while local specialists differentiate through multilingual and regulatory expertise. Cloud deployment models dominate because they offer scalable compliance controls, yet the fastest corporate spending shift is toward managed services that bundle technology with GDPR-fluent implementation talent. Germany's 18.5% CAGR and the DACH-Nordics focus on AI-driven personalization highlight the link between AI readiness and marketing automation uptake, whereas EU AI Act obligations and a scarcity of certified data-privacy architects temper roll-out velocity.

Europe Marketing Automation Software Market Trends and Insights

AI-Powered Personalisation Surge in DACH and Nordics E-commerce Drives the Market

AI-enabled engines have permeated DACH and Nordic retail, with 65% of executives naming AI a core growth lever in 2025. Marketers exploit the regions' advanced cloud infrastructure and high data-sharing consent rates to roll out recommendation models that elevate conversion. Telmore recorded an 11% uplift in sales after adopting AI-driven personalization, illustrating quantifiable ROI that accelerates peer adoption. As 80% of companies earmark higher AI budgets yet only 12% prove ROI, early adopters with strong measurement frameworks gain competitive distance. German practitioners use generative AI to streamline campaign production and reporting, cutting repetitive tasks and redeploying staff toward analytics. Consequently, the DACH-Nordic corridor functions as a test bed for next-wave personalization capabilities that subsequently diffuse across Europe.

EU Digital Single-Market Initiatives Boosting SME SaaS Uptake

The EUR 7.9 billion (USD 8.55 billion) Digital Europe Programme lowers barriers for SMEs by harmonizing cloud regulations and funding European Digital Innovation Hubs that provide hands-on guidance. Standardized APIs improve data portability, easing integration among disparate marketing applications and mitigating vendor lock-in risks. Cloud adoption among EU enterprises stands at 41% and is slated to reach 75% by 2030, translating into a sizeable new customer pool for SaaS-based marketing automation. These policy tailwinds curtail compliance complexity for mid-market buyers and amplify addressable demand within the Europe marketing automation software market.

Scarcity of GDPR-Fluent Marketing-Automation Architects

Implementation projects increasingly stall because only a narrow cadre of professionals combines martech proficiency with legal insight. Banking workforce realignment illustrates cross-industry competition for data specialists after a 21% employment contraction in traditional roles between 2007 and 2022. SMEs are disproportionately affected, leading to a reliance on external managed services, which explains their 16.1% CAGR within the services component. Certification initiatives by European Digital Innovation Hubs provide relief, but near-term talent gaps constrain uptake within smaller economies.

Other drivers and restraints analyzed in the detailed report include:

- Account-Based Marketing Adoption in B2B Tech Hubs Drives the Market

- Open-Banking API Integration in European Financial Services Drives the Market

- High TCO for Multi-Language Personalisation Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software continued to generate 72% of Europe marketing automation software market revenue in 2024, though managed services outpaced with a 16.1% CAGR to 2030, underscoring corporates' preference for outsourced compliance know-how. The services surge signals that enterprises consider technical execution and regulatory validation equally critical as core functionality. Within software, integrated suites eclipse point tools because buyers demand one source of truth for data privacy audits and AI model governance. Professional services thrive on legacy-system integration and GDPR gap analysis, positioning consultancies and system integrators as gatekeepers for vendor selection.

Heightened AI Act scrutiny places a premium on solution blueprints that embed auditability by design. Vendors combine packaged software with advisory retainers, generating annuity-style revenue. The Europe marketing automation software industry will therefore see blended business models, where software margins pair with high-touch services to address dynamic rule-sets spanning GDPR, PSD2, and sector-specific mandates.

Cloud options owned 78% of the Europe marketing automation software market in 2024, bolstered by EU backing for sovereign and trusted cloud frameworks. Cloud deployments are expanding at 15.8% CAGR because continuous platform updates help clients absorb new data-handling obligations without capex spikes. Marketing teams benefit from elastic compute to run AI models that personalize journeys in real time. On-premise persists only where public-sector or defense clients demand strict data residency.

Regulators favor cloud's centralized control planes that support automated consent logging, breach notification, and encryption management. This regulatory alignment reduces perceived risk, spurring broader cloud migration. Partnerships, such as Oracle's tie-up with Palantir for secure EU cloud regions, illustrate how hyperscale providers localize stacks to satisfy sovereignty narratives. As uptake matures, cloud vendors will compete on value-add layers like zero-trust architectures and pre-certified AI sandboxing.

Europe Marketing Automation Software Market is Segmented by Component (Software, Services), Deployment Mode (Cloud-Based, On-Premise), Organisation Size (Small and Medium Enterprises, Large Enterprises), Channel / Function (Email Marketing, Social Media Marketing, Campaign Management, and More), End-User Industry (Retail and E-Commerce, BFSI, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Salesforce, Inc.

- Adobe Inc.(Marketo Inc.)

- HubSpot Inc.

- Oracle Corporation

- Microsoft Corporation

- SAP SE

- SAS Institute Inc.

- Act-On Software, Inc.

- Dotdigital Group PLC

- Force24 Ltd.

- ActiveCampaign LLC

- Mailchimp (Intuit Inc.)

- Sendinblue SAS (Brevo)

- GetResponse Sp. z o.o.

- Zoho Corporation

- Pipedrive OU

- SugarCRM Inc.

- Acoustic LP

- Iterable Inc.

- Klaviyo Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Powered Personalisation Surge in DACH and Nordics E-commerce Drives the Market

- 4.2.2 EU Digital Single-Market Initiatives Boosting SME SaaS Uptake

- 4.2.3 Account-Based Marketing Adoption in B2B Tech Hubs Drives the Market

- 4.2.4 Open-Banking API Integration in European Financial Services Drives the Market

- 4.2.5 Multi-Lingual Journey Orchestration Across Fragmented Market

- 4.3 Market Restraints

- 4.3.1 Scarcity of GDPR-Fluent Marketing-Automation Architects

- 4.3.2 High TCO for Multi-Language Personalisation Modules

- 4.3.3 Stringent EU Anti-Spam Rules Impacting Email Deliverability

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Assessment of Macro Economic Trends on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Integrated Platforms

- 5.1.1.2 Stand-Alone Tools

- 5.1.1.2.1 Lead Management

- 5.1.1.2.2 Social Media

- 5.1.1.2.3 Email and Analytics

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Organisation Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Channel / Function

- 5.4.1 Email Marketing

- 5.4.2 Social Media Marketing

- 5.4.3 Campaign Management

- 5.4.4 Mobile / SMS Marketing

- 5.4.5 Inbound and Content Marketing

- 5.4.6 Other Channels

- 5.5 By End-user Industry

- 5.5.1 Retail and E-commerce

- 5.5.2 BFSI (Banking, FinServ and Insurance)

- 5.5.3 IT and Telecom

- 5.5.4 Manufacturing

- 5.5.5 Healthcare and Life-Sciences

- 5.5.6 Media and Entertainment

- 5.5.7 Government and Public Sector

- 5.5.8 Other End-user Industries

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Nordics

- 5.6.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Salesforce, Inc.

- 6.4.2 Adobe Inc.(Marketo Inc.)

- 6.4.3 HubSpot Inc.

- 6.4.4 Oracle Corporation

- 6.4.5 Microsoft Corporation

- 6.4.6 SAP SE

- 6.4.7 SAS Institute Inc.

- 6.4.8 Act-On Software, Inc.

- 6.4.9 Dotdigital Group PLC

- 6.4.10 Force24 Ltd.

- 6.4.11 ActiveCampaign LLC

- 6.4.12 Mailchimp (Intuit Inc.)

- 6.4.13 Sendinblue SAS (Brevo)

- 6.4.14 GetResponse Sp. z o.o.

- 6.4.15 Zoho Corporation

- 6.4.16 Pipedrive OU

- 6.4.17 SugarCRM Inc.

- 6.4.18 Acoustic LP

- 6.4.19 Iterable Inc.

- 6.4.20 Klaviyo Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球行销自动化软体市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034年)

全球行销自动化软体市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034年) 行销自动化软体市场 - 全球产业规模、份额、趋势、机会及预测(按应用、部署模式、企业类型、最终用户、地区和竞争格局划分,2021-2031 年)

行销自动化软体市场 - 全球产业规模、份额、趋势、机会及预测(按应用、部署模式、企业类型、最终用户、地区和竞争格局划分,2021-2031 年) 行销自动化软体 - 全球市场占有率和排名、总收入和需求预测(2025-2031 年)

行销自动化软体 - 全球市场占有率和排名、总收入和需求预测(2025-2031 年) 自动化软体市场:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)

自动化软体市场:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年) 2025-2029年全球行销自动化软体市场亚太地区西方行销自动化软体市场 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)北美行销自动化软体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

2025-2029年全球行销自动化软体市场亚太地区西方行销自动化软体市场 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)北美行销自动化软体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)