|

市场调查报告书

商品编码

1850114

虚拟行动服务业者(MVNO):市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Mobile Virtual Network Operator (MVNO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

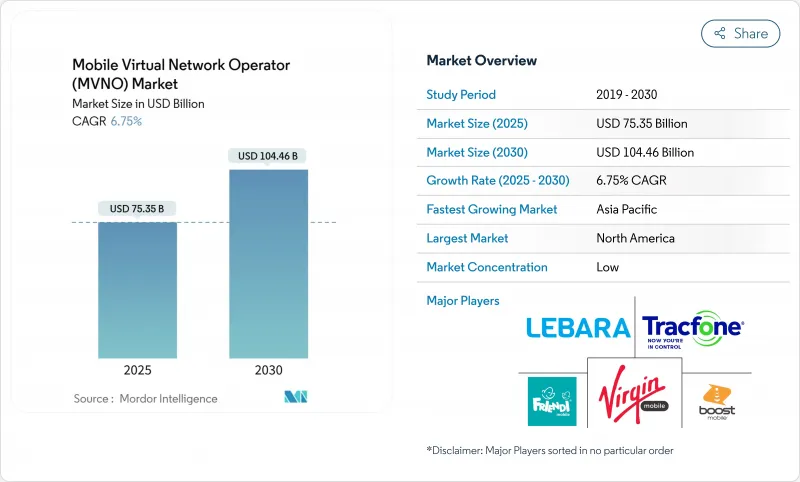

预计到 2025 年行动虚拟网路营运商 (MVNO) 市场规模将达到 753.5 亿美元,到 2030 年将达到 1,044.6 亿美元,复合年增长率为 6.75%。

这一成长反映了该细分市场的潜力,因为金融科技和通讯业者融合、批发定价改革以及向基于 eSIM 的激活方式转变,导致定价压力不断增加。 Revolut 在英国和德国推出 MVNO,以及 Nubank 在巴西推出 MVNO,伙伴关係表明银行业务和网路连接之间的界限正在变得模糊。与此同时,韩国等市场的监管机构正在将批发费用降低高达 52%,重塑竞争经济。云端部署模式已占据行动虚拟网路营运商市场的 57%,而受资本支出减少和推出週期加快的推动,云端原生平台正以 10.6% 的复合年增长率扩张。竞争差异化将取决于 5G 网路切片、卫星到基地台链路以及人工智慧驱动的服务个人化。

全球虚拟行动服务业者(MVNO) 市场趋势与洞察

行动用户数量和智慧型手机普及率不断上升

2023年底,亚太地区的行动连线将超过18亿,人口普及率将达到63%,为该地区的GDP贡献8,800亿美元。这种快速成长为那些提供针对年轻人和移民群体客製化套餐的营运商在行动虚拟网路营运商(MVN)市场开闢了潜在的利基市场。菲律宾环球电信公司(Globe Philippines)正透过固定无线接入服务挖掘农村需求,而Telkomsel则凭藉其应用优先的「by.U」品牌瞄准数位原民。孟加拉、印度和巴基斯坦等国家仍然存在巨大的使用缺口,这为成本主导的行动虚拟网路营运商(MVNO)提供了一条扩张之路。高智慧型手机拥有率鼓励了资料通讯密集型习惯,并强化了MVNO提供的基于使用量的典型收费系统。这些因素共同推动了行动虚拟网路营运商(MVNO)到2025年左右的普及前景。

对低成本语音和资料方案的需求

持续的通货膨胀使消费者对价值更加敏感,并推动行动虚拟网路营运商市场中的客户转向廉价的供应商。在英国,现有的行动网路营运商在 2024 年下半年首次失去签约线路,而虚拟网路营运商则增加了 170 万用户。 MobileX 以每月 3.48 美元起的价格出售经过人工智慧调整的套餐,客户解约率低于 0.5%。线上销售降低了零售开销并允许更大的折扣,而基于应用程式的支援进一步降低了服务交付成本。主机营运商整合对独立营运商构成威胁,但敏捷的虚拟网路营运商正在透过联合品牌和基于社群的推荐来抵消规模劣势并拓宽其盈利窗口。

激烈的价格竞争导致利润压力

转换摩擦的降低和子品牌的丰富推高了费率方案,给整个行动虚拟网路营运商市场的 EBITDA 带来压力。儘管 Lycamobile 在英国拥有 170 万条线路,但由于 5,100 万英镑的增值税2022 年仍面临 2,510 万英镑的亏损。託管 MNO 正在透过其自有折扣品牌加剧价格竞争,削弱独立营运商的竞争力。 MobileX 创办人 Peter Adderton 指出,MNO 对 TracFone 和 Mint Mobile 的收购减少了批发合作伙伴的数量并增强了他们的谈判能力。 Vodafone Three 合併计划于 2025 年完成,这将进一步增加英国的规模压力,迫使较小的 MVNO 专业化或接受收购提案。

細項分析

到2024年,云端部署将占行动虚拟网路营运商市场的57%,这反映出市场正在快速转向可扩展的基础设施,以降低资本支出。随着营运商寻求在流量激增期间实现弹性容量和自动化补丁管理,到2030年,云端原生平台的复合年增长率将达到10.6%。这种转变将加快功能部署,并推动基于人工智慧的留存工具,将客户流失降至1%以下。 CompaxDigital与T-Mobile的联合提案为中阶虚拟网路营运商(MVNO)提供了先进的BSS/OSS堆迭,将推出时间从数月缩短至数週。像Gigs这样的新兴企业已经筹集了7300万美元,用于销售“MVNO-in-a-box”,凸显了风险投资对轻资产参与企业的兴趣。

由于虚拟化频宽按需分配频宽,云端敏捷性进一步支援 5G 网路切片。这种灵活性使行动虚拟网路营运商 (MVNO) 能够瞄准微细分市场,例如游戏玩家或远端医疗服务供应商,而无需从主机行动网路营运商 (MNO) 过度购买容量。相反,需要自主资料託管的国防和银行客户可能会受益于本地部署。云端管理平面和边缘站点使用者平面功能的混合策略使完整的行动虚拟网路营运商 (MVNO) 能够获得自动化的优势,同时确保细粒度的安全性。随着许多城市的公共云端延迟降至 10 毫秒以下,外部部署完整核心的经济效益可能会更加强劲。

完全行动虚拟营运商 (MVNO) 受益于直接拥有 SIM 卡、控制 HLR/HSS 以及完整的客户生命週期数据,在 2024 年获得了 41%的收益份额。它们透过捆绑内容和云端储存等附加价值服务来获取更高的每用户平均收入 (ARPU)。然而,轻量级行动虚拟业者或品牌行动虚拟业者由于其快速进入市场且领先资本投入较少,其复合年增长率高达 13.2%。零售商和应用程式公司被这种轻量级模式所吸引,因为它使他们无需具备电讯知识即可为现有生态系统添加连接。

服务业者协议是一种折衷方案,允许营运商租赁核心网络,同时拥有收费和策略控制权。经销商协议仍然吸引沃尔玛等大型零售商,它们利用门市客流量销售预付套餐。德国1&1在获得5G频谱后,从一家成熟的行动虚拟网路营运商(MVNO)发展成为德国第四大行动网路营运商,展现了一条向上发展的行动发展之路。这样的发展为雄心勃勃的营运商在其用户群达到临界点后提供了蓝图。然而,精简模式可能会更快起飞,透过降低品牌进入门槛来启动行动虚拟网路营运商市场。

MVNO 市场报告按部署模式(云端、本地)、营运类型(经销商、服务供应商、其他)、用户类型(消费者、企业、物联网为中心)、用例(折扣、商业、蜂窝 M2M、其他)、网路技术(2G/3G、5G、其他)、分销管道(仅在线上/数位、实体零售、其他)和地区进行细分。

区域分析

2024年,北美以38.5%的市占率领先行动虚拟网路营运商市场,这得益于其ARPU值是全球平均水准的四倍,以及鼓励批发竞争的法规环境。营运商正在利用其庞大的后付费用户群,在不蚕食高端产品线的情况下,提升销售平价细分市场的子品牌销售。 Verizon收购TracFone后,新增了2,000万名预付用户,印证了该细分市场的策略重要性。

亚太地区的复合年增长率为 10.1%,预计到 2027 年,新增用户数将超过欧洲。这得归功于印度、印尼和中国的智慧型手机价格下降以及频谱竞标自由化。政府对开放存取和 5G 快速部署的强制要求,为金融科技支援的行动虚拟营运商 (MVNO) 提供了肥沃的土壤,这些营运商瞄准的是银行帐户的人群。云端原生参与企业也拥有丰富的开发人才,并降低了每张 SIM 卡的营运成本。

在欧洲,随着用户监管机构协调终端和漫游费用,用户成长依然强劲,对跨境虚拟网路营运商(MVNO)来说是个好兆头。英国沃达丰三公司(Vodafone Three)计划在未来八年投资110亿英镑,该公司必须兑现其支持至少三家独立MVNO的承诺,从而保持激烈的竞争。随着营运商向当地金融科技合作伙伴推出网路API,中东和非洲的新兴丛集获得了发展动力,而随着Nubank的扩张,拉丁美洲的融合趋势也在加速。总而言之,这些动态使区域动态成为行动虚拟网路营运商市场调整的关键视角。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 行动电话用户和智慧型手机普及率的增加

- 对低成本语音和资料方案的需求

- 物联网/M2M连接的兴起

- 促进开放批发接取和 eSIM 接取的监管

- 金融科技与电信业者的融合催生了银行品牌的虚拟营运商

- 卫星到行动电话的伙伴关係实现了全球MVNO覆盖

- 市场限制

- 价格竞争激烈,利润受到挤压

- 网路品质和批发价格取决于主机 MNO

- 设备 OEM 控制 eSIM 所有权,绕过 MVNO 模式

- 私有频谱共用允许公司自行提供服务

- 价值链分析

- 监管格局

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章市场规模及成长预测

- 按部署模型

- 云

- 本地部署

- 按运转方式

- 经销商

- 服务业者

- 完整的行动虚拟营运商

- 轻量/品牌 MVNO

- 依用户类型

- 消费者

- 公司

- 物联网专用

- 按用途

- 折扣

- 商业

- 蜂窝 M2M

- 媒体和娱乐

- 零售

- 漫游

- 移民

- 通讯批发

- 网路科技

- 2G/3G

- 4G/LTE

- 5G

- 卫星/NTN

- 按分销管道

- 仅限线上/数位版

- 传统零售店

- 开利子品牌店

- 第三方/批发

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 其他亚太地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- TracFone Wireless(Verizon)

- Tesco Mobile

- Virgin Mobile

- Lycamobile

- Lebara Group

- Boost Mobile(T-Mobile)

- Cricket Wireless(ATandT)

- Giffgaff

- 1and1 Drillisch

- PosteMobile

- Truphone

- Kajeet

- Ting Mobile

- Google Fi

- Altice Mobile

- Asahi Net

- FreedomPop

- Airvoice Wireless

- FRiENDi Mobile

- Voiceworks

第七章 市场机会与未来展望

The mobile virtual network operator market size reached USD 75.35 billion in 2025 and is on track to hit USD 104.46 billion by 2030, advancing at a 6.75% CAGR.

Growth reflects the segment's ability to thrive amid price pressure, spurred by fintech-telco convergence, wholesale price reforms, and the move toward eSIM-enabled activation. Partnerships such as Revolut's MVNO roll-out in the UK and Germany and Nubank's service launch in Brazil illustrate the blurring line between banking and connectivity. At the same time, regulators in markets like South Korea are cutting wholesale fees by up to 52%, reshaping competitive economics. The cloud deployment model already commands 57% of the mobile virtual network operator market, and cloud-native platforms are expanding at 10.6% CAGR on the back of lower capex and faster launch cycles. Competitive differentiation increasingly hinges on 5G network slicing, satellite-to-cell links, and AI-driven service personalization.

Global Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Rising Mobile-Subscriber Base and Smartphone Penetration

Mobile connections crossed 1.8 billion in Asia Pacific by end-2023, equal to 63% population penetration and contributing USD 880 billion to regional GDP. The surge opens addressable niches for operators that tailor plans to youth or migrant cohorts within the mobile virtual network operator market. Globe Philippines captured rural demand with fixed-wireless access, while Telkomsel's app-first "by.U" brand courts digital natives. Countries such as Bangladesh, India, and Pakistan still exhibit wide usage gaps, offering cost-led MVNOs a path to scale. High smartphone ownership propels data-heavy habits, reinforcing usage-based tariffs common to MVNO offers. These factors collectively lift adoption prospects through mid-decade.

Demand for Low-Cost Voice and Data Plans

Persistent inflation sharpens consumer sensitivity to value, pulling churn toward budget-centric providers inside the mobile virtual network operator market. In the UK, incumbent MNOs lost contract lines for the first time in late 2024, while MVNOs added 1.7 million subscribers. MobileX sells AI-tailored bundles from USD 3.48 per month and holds churn below 0.5%, an illustration of how data-driven pricing sustains loyalty. Online distribution trims retail overheads, enabling deeper discounts, and app-based support further reduces cost-to-serve. Although consolidation by host carriers threatens independents, agile MVNOs offset scale disadvantages through brand partnerships and community-based referrals, lengthening the window for profit capture.

Margin Squeeze from Intense Price Competition

Lower switching friction and plentiful sub-brands push tariffs toward cost, compressing EBITDA across the mobile virtual network operator market. Lycamobile battled £25.1 million losses in 2022 despite 1.7 million UK lines, burdened by a GBP 51 million VAT dispute and prolonged 5G service outages. Host MNOs intensify price warfare through owned discount brands, undercutting independents. MobileX founder Peter Adderton notes that MNO acquisitions of TracFone and Mint Mobile leave fewer wholesale partners, tightening negotiation leverage. The completed VodafoneThree merger in 2025 adds further scale pressure in the UK, forcing smaller MVNOs either to specialize or accept buy-out offers.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of IoT/M2M Connections

- Regulatory Push for Open Wholesale Access and eSIM-Enabled Entry

- Dependence on Host MNOs for Network Quality and Wholesale Fees

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 57% of the mobile virtual network operator market in 2024, reflecting rapid migration toward scalable infrastructure that lowers capex. Cloud-native platforms are posting a 10.6% CAGR through 2030 as operators seek elastic capacity during traffic spikes and automated patch management. The shift enables faster feature rollouts and facilitates AI-based retention tools that keep customer churn below 1%. CompaxDigital's joint offer with T-Mobile brings advanced BSS/OSS stacks to mid-tier MVNOs, cutting launch times from months to weeks. Start-ups like Gigs raised USD 73 million to market "MVNO-in-a-box," underscoring venture appetite for asset-light entrants.

Cloud agility further supports 5G network slicing because virtualized cores allocate bandwidth on demand. This flexibility equips MVNOs to target micro-segments such as gamers or tele-medicine providers without over-buying capacity from host MNOs. Conversely, on-premise installations remain relevant for defense or banking clients requiring sovereign data hosting. A hybrid strategy-cloud management plane paired with edge-site user-plane functions-gives full MVNOs granular security while still harvesting automation gains. As public-cloud latency falls below 10 milliseconds in many metros, the economic case for full off-premise cores will continue to strengthen.

Full MVNOs secured 41% revenue share in 2024, benefitting from direct SIM ownership, HLR/HSS control, and complete customer-life-cycle data. They capture higher ARPU by bundling value-added services such as content or cloud storage. Light or brand MVNOs, however, are expanding at 13.2% CAGR owing to quicker go-to-market and minimal upfront capital. Retailers and app firms gravitate toward this lighter model to append connectivity to existing ecosystems without deep telecom expertise.

Service-operator constructs offer a compromise, allowing ownership of billing and policy while leasing the core. Reseller agreements still attract big-box merchants like Walmart that leverage store traffic to sell prepaid bundles. Germany's 1&1 demonstrated an upward mobility pathway, evolving from full MVNO to the nation's fourth MNO after securing 5G spectrum. Such evolution provides a blueprint for ambitious operators once the subscriber base crosses critical mass. Yet light models will likely proliferate faster, energizing the mobile virtual network operator market by lowering brand-entry barriers.

The MVNO Market Report is Segmented by Deployment Model (Cloud and On-Premise), Operational Mode (Reseller, Service Operator, and More), Subscriber Type (Consumer, Enterprise, and IoT-Specific), Application (Discount, Business, Cellular M2M, and More), Network Technology (2G/3G, 5G, and More), Distribution Channel (Online/Digital-only, Traditional Retail Stores, and More), and Geography.

Geography Analysis

North America led the mobile virtual network operator market with a 38.5% share in 2024, underpinned by ARPU levels four times the global mean and a regulatory climate that fosters wholesale competition. Operators leverage large post-paid bases to upsell value-segment sub-brands without cannibalizing premium lines. The TracFone acquisition by Verizon added 20 million prepaid users, affirming the segment's strategic weight.

Asia Pacific is advancing at a 10.1% CAGR and is set to overtake Europe in gross additions by 2027, powered by smartphone affordability and liberalized spectrum auctions in India, Indonesia, and China. Government mandates for open access plus rapid 5G rollouts make the region fertile ground for fintech-backed MVNOs targeting unbanked populations. Cloud-native entrants also find abundant developer talent, lowering operating cost per SIM.

Europe maintains steady subscriber growth as regulators harmonize termination rates and roaming fees, a boon for cross-border MVNOs. The UK's VodafoneThree entity plans GBP 11 billion investment over eight years but must honor undertakings to support at least three independent MVNOs, preserving competitive intensity. Emerging clusters in the Middle East and Africa gain traction as operators deploy network APIs to local fintech partners, while Latin America's convergence trend accelerates after Nubank's expansion. Collectively, these dynamics position geography as a critical lens for go-to-market adjustments inside the mobile virtual network operator market.

- TracFone Wireless (Verizon)

- Tesco Mobile

- Virgin Mobile

- Lycamobile

- Lebara Group

- Boost Mobile (T-Mobile)

- Cricket Wireless (ATandT)

- Giffgaff

- 1and1 Drillisch

- PosteMobile

- Truphone

- Kajeet

- Ting Mobile

- Google Fi

- Altice Mobile

- Asahi Net

- FreedomPop

- Airvoice Wireless

- FRiENDi Mobile

- Voiceworks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising mobile-subscriber base and smartphone penetration

- 4.2.2 Demand for low-cost voice and data plans

- 4.2.3 Expansion of IoT/M2M connections

- 4.2.4 Regulatory push for open wholesale access and eSIM-enabled entry

- 4.2.5 Fintech-telco convergence spawning bank-branded MVNOs

- 4.2.6 Satellite-to-cell partnerships enabling global MVNO coverage

- 4.3 Market Restraints

- 4.3.1 Margin squeeze from intense price competition

- 4.3.2 Dependence on host MNOs for network quality and wholesale fees

- 4.3.3 Device-OEM control of eSIM ownership bypassing MVNO model

- 4.3.4 Private-spectrum sharing lets enterprises self-provision service

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Operational Mode

- 5.2.1 Reseller

- 5.2.2 Service Operator

- 5.2.3 Full MVNO

- 5.2.4 Light / Brand MVNO

- 5.3 By Subscriber Type

- 5.3.1 Consumer

- 5.3.2 Enterprise

- 5.3.3 IoT-specific

- 5.4 By Application

- 5.4.1 Discount

- 5.4.2 Business

- 5.4.3 Cellular M2M

- 5.4.4 Media and Entertainment

- 5.4.5 Retail

- 5.4.6 Roaming

- 5.4.7 Migrant

- 5.4.8 Telecom Wholesale

- 5.5 By Network Technology

- 5.5.1 2G/3G

- 5.5.2 4G/LTE

- 5.5.3 5G

- 5.5.4 Satellite/NTN

- 5.6 By Distribution Channel

- 5.6.1 Online/Digital-only

- 5.6.2 Traditional Retail Stores

- 5.6.3 Carrier Sub-brand Stores

- 5.6.4 Third-Party/Wholesale

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Colombia

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 ASEAN

- 5.7.4.6 Rest of Asia Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 TracFone Wireless (Verizon)

- 6.4.2 Tesco Mobile

- 6.4.3 Virgin Mobile

- 6.4.4 Lycamobile

- 6.4.5 Lebara Group

- 6.4.6 Boost Mobile (T-Mobile)

- 6.4.7 Cricket Wireless (ATandT)

- 6.4.8 Giffgaff

- 6.4.9 1and1 Drillisch

- 6.4.10 PosteMobile

- 6.4.11 Truphone

- 6.4.12 Kajeet

- 6.4.13 Ting Mobile

- 6.4.14 Google Fi

- 6.4.15 Altice Mobile

- 6.4.16 Asahi Net

- 6.4.17 FreedomPop

- 6.4.18 Airvoice Wireless

- 6.4.19 FRiENDi Mobile

- 6.4.20 Voiceworks

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)西班牙电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)越南电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)西班牙电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)越南电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 虚拟行动服务业者(MVNO)市场-2026-2031年预测

虚拟行动服务业者(MVNO)市场-2026-2031年预测