|

市场调查报告书

商品编码

1850313

行动行销:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Mobile Marketing Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

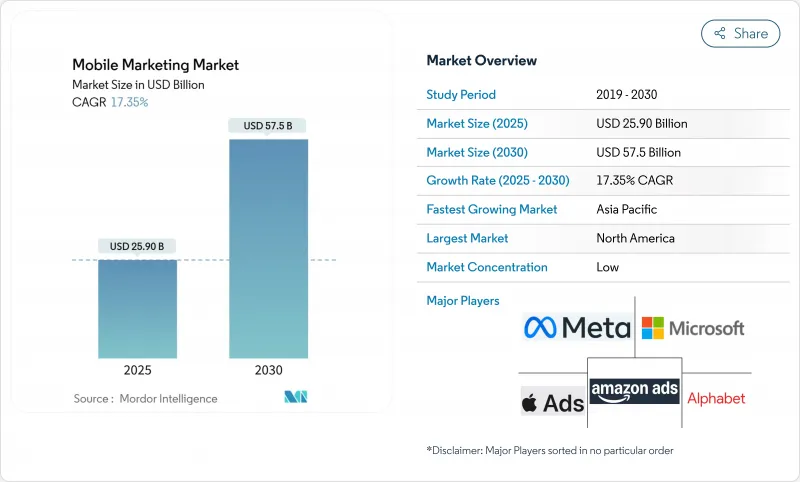

预计到 2025 年,行动行销市场规模将达到 259 亿美元,到 2030 年将成长至 575.3 亿美元,预测期内复合年增长率将达到 17.35%。

随着发现、评估和购买流程不断向行动装置转移,智慧型手机已成为商务、媒体和客户服务的预设入口。这促使广告主将预算分配到资料丰富的互动环节,将身分验证、授权管理和创新自动化整合到单一工作流程中。能够将这些功能统一到单一使用者介面下的平台提供者正在赢得更多广告支出,因为品牌团队无需在不同工具之间切换,即可测试、衡量和优化广告路径。亚太地区 20% 的复合年增长率反映了 5G 普及、数位钱包和超级应用生态系统的综合影响,而欧洲严格的隐私法规则促使负责人加强其第一方资料资产和闭合迴路衡量。

全球行动行销市场趋势与洞察

隐私安全识别码框架提升北美应用内收益

在美国主要出版商中,伺服器端事件收集和经使用者授权的装置令牌正在取代浏览器层级的 Cookie。采用这些框架的品牌报告称,匹配率实现了两位数的提升,从而在遵守州级隐私法规的同时,实现了更丰富的用户细分。同样的机制还能自动产生合规报告,并使财务团队能够将隐私升级视为技术投资。因此,行销和风险部门可以基于共用指标进行协作,广告商即使在监管日益严格的情况下也能保持个人化的推广。这些优势证明,合规的身份解析正在成为成长的驱动力,而非成本中心。

5G网路的部署使亚洲都市区能够开展超低延迟的宣传活动

商用5G网路现已覆盖亚洲大部分城市,行动影片平均载入时间远低于100毫秒。负责人正积极回应,推出互动式扩增实境产品展示,让使用者只需轻按一下即可在结帐前虚拟摆放产品。在首尔举行的2024年游戏展上,一场在网路边缘执行的即时A/B测试,与在4G网路上使用相同创新相比,将放弃率降低了近25%。这项经验表明,频宽可以作为创新画布,激发沉浸式故事叙述,而不仅仅是提升传输速度。随着5G网路的日益普及,行动行销市场有望迎来更丰富的素材形式和更高的转换效率。

无 Cookie 策略会扰乱全球跨应用归因分析

第三方 Cookie 正逐渐从主流浏览器中消失,跨装置图谱也随之缩小,迫使行销人员尝试机率测量和增量分析。过去依赖使用者级报告的财务经理现在需要使用基于提升率、专注于因果贡献的仪錶板。虽然学习週期会更长,但随着机率讯号能够容忍隐私波动,预算分配将逐步趋于稳定。儘管效果负责人短期内会面临一些阻力,但这种转变最终将打造一个更具韧性的规划流程,并增强行动行销市场抵御未来监管波动的能力。

细分市场分析

到2024年,平台软体将占总收入的67%,成为行动行销市场的营运支柱。供应商正在整合低程式码旅程建立器和隐私仪表板,使品牌团队能够在无需工程支援的情况下近乎即时地测试规则。服务线规模虽小,但正随着企业寻求在无尘室部署、创新自动化和区域法规方面的指导而迅速扩张。咨询业务的重点正从媒体套利转向技术赋能,从而建立新的收费体系并重新平衡供应链中的价值获取。展望未来,软体升级将有助于维持客户维繫,而服务合约将进一步增强客户锁定。

技术服务还负责促成广告商和发布商之间复杂的资料共用协议,并推动经用户同意的识别码的采用。这种对技术和专业知识的双重需求,使得混合型服务提供者能够占据更大的市场份额。因此,儘管软体仍保持其领先的市场份额,但与组件服务相关的行动行销市场规模预计将超过整体市场成长速度。

位置智慧占据行动行销市场规模的15%左右,预计到2030年将达到22%的复合年增长率,超过其他解决方案丛集。增强型技术堆迭融合了GPS、蓝牙信标和场所Wi-Fi,能够以亚米级的精度精确定位消费者的停留区域。即时优惠在兑换率和客单价指标上均优于一般优惠券。例如,2025年柏林的一项软性饮料促销活动就采用了柜檯下方的序号,引导消费者立即进入一款奖励丰厚的手机游戏。

由于推播通知的开启率更高,因此仍将至关重要,但编配引擎会根据预测的疲劳程度调整推播频率,以防止用户选择取消订阅。随着零售商在这些通知中嵌入富媒体内容,地点讯号将进一步精准定位推播时间,加深用户互动,并提高用户单次消费额。将地图 API、分析工具和创新工具整合到单一介面中的供应商将拓宽竞争优势,并在更广泛的行动行销市场中占据更大份额。

行动行销市场按组件(平台、服务)、解决方案类型(行动网页、简讯和彩信、其他)、分销管道(社交媒体行销、联盟行销、其他)、公司规模(大型企业、中小企业)、部署类型(云端、本地部署)、最终用户产业(零售和电子商务、媒体和娱乐/OTT)以及地区进行细分。市场预测以美元计价。

区域分析

北美地区将占2024年营收的38%,凸显其作为广告科技创新试验场的地位。各州隐私改革将加速第一方资料项目的推进,从而提高匹配率并建立合规的身份图谱。在2028年洛杉矶奥运会之前,一个活动层级的定位平台将应运而生,将票务、餐饮和赞助商通讯整合到一个统一的行动流程中。 2024年足球季后赛期间的一项试验表明,根据餐饮排队时间定制的动态优惠提高了人均消费额,且并未减少客流量,这不仅展现了营运效益,也体现了媒体价值。随着出版商竞相整合隐私安全的识别系统,创投依然强劲,为更广泛的行动行销市场提供了支持。

亚太地区预计将实现20%的复合年增长率,这反映了5G速度、超级应用生态系统和社交电商规范的综合影响。 2024年,东南亚一家领先的超级应用上的化妆品宣传活动扩增实境试妆与聊天结帐相结合,将购买时间缩短至60秒以内,销量增长了两倍。在印度,本地语言语音搜寻正在扩大覆盖范围,促使平台所有者推出针对低文化水平人群的主导广告形式。这些创新表明,技术普及不仅取决于技术成熟度,也取决于文化习惯。智慧型手机的快速更换週期和低廉的数据流量费用正在进一步扩大行动行销市场。

儘管欧洲严格的隐私法限制了基于cookie的推广范围,零售商们正透过闭合迴路零售媒体网路实现会员忠诚度计画的获利。 2025年,一家荷兰连锁超市推出了自助服务门户,供应商可以在此购买赞助商品图块并将其部署到该连锁超市的行动钱包中,从而在几天内实现端到端的归因分析。儘管北欧国家规模较小,但其用户行动端参与度在欧洲大陆最高,证明在赢得消费者信任的前提下,尊重隐私的个人化行销也能取得成功。监管政策的明确性可能会抑制短期成长,但有助于长期稳定,从而支持全部区域行动行销市场的稳定扩张。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 注重隐私的识别符框架提升北美应用内行销投资报酬率

- 5G的推出使亚洲各地能够开展超低延迟的富媒体宣传活动。

- 快速商务应用程式的激增推动了拉丁美洲都市区的推播通知支出

- 欧洲零售媒体网路强制要求建立第一方资料伙伴关係。

- 市场限制

- 使用无 cookie 策略进行跨应用程式归因的装置图简化

- 通讯业者简讯防火墙升级推高非洲A2P流量成本

- 价值/供应链分析

- 监管或技术前景

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- 新冠疫情对市场的影响

第五章 市场规模与成长预测

- 按组件

- 平台

- 服务

- 按解决方案类型

- 行动网页

- 简讯和彩信

- 基于位置的营销/地理围栏

- 应用程式内和游戏内广告

- 推播通知与富媒体

- QR码与近场行销

- 新兴技术(AR/VR、信标、5G边缘运算)

- 透过分销管道

- 社群媒体行销

- 联盟行销

- 全通路/零售应用

- 内容行销和影响者行销

- 线上公共关係

- 电子邮件和简讯宣传活动

- 游戏内/电子竞技

- 按公司规模

- 大公司

- 小型企业

- 透过部署模式

- 云

- 本地部署

- 按最终用户行业划分

- 零售与电子商务

- 媒体与娱乐/OTT

- BFSI

- 医疗保健和生命科学

- 旅游、观光和酒店

- 通讯

- 车

- 教育

- 其他(政府、公共产业)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- Strategic Developments

- Vendor Positioning Analysis

- 公司简介

- Alphabet Inc.(Google)

- Meta Platforms Inc.

- Apple Inc.(Apple Advertising)

- Microsoft Corporation

- Amazon.com Inc.(Amazon Ads)

- Twitter/X Corp.

- Snap Inc.

- Pinterest Inc.

- Verizon Communications Inc.(Yahoo Advertising)

- ATandT Inc.

- InMobi Pte Ltd

- AppLovin Corporation

- GroundTruth

- Criteo SA

- Airship

- Adobe Inc.

- Oracle Corporation

- Salesforce Inc.

- Publicis Groupe(Phonevalley)

- AdColony Inc.

- MoPub(AppLovin Exchange)

第七章 市场机会与未来展望

The mobile marketing market size is valued at USD 25.9 billion in 2025 and is forecast to climb to USD 57.53 billion by 2030, advancing at a 17.35% CAGR during the outlook period.

Continuous migration of discovery, evaluation, and purchase to handheld screens has turned smartphones into the default entry point for commerce, media, and customer service. Advertisers are therefore diverting budgets toward data-rich engagement moments where identity resolution, consent management, and creative automation converge inside one workflow. Platform providers that integrate these functions under a single user interface are winning incremental spend, because brand teams can test, measure, and optimise journeys without toggling between tools. Asia-Pacific's 20% CAGR signals the compounding effect of 5G coverage, digital wallets, and super-app ecosystems, while Europe's stringent privacy rules push marketers to fortify first-party data assets and closed-loop measurement.

Global Mobile Marketing Market Trends and Insights

Privacy-safe identifier frameworks lifting in-app returns in North America

Server-side event collection and consented device tokens are replacing browser-level cookies across major United States publishers. Brands embedding these frameworks report doubled-digit improvements in match rates, enabling richer segmentation while meeting state-level privacy mandates. The same mechanisms automate compliance reporting, allowing finance teams to capitalise on privacy upgrades as technology investments. Marketing and risk units, therefore, align on shared metrics, and advertisers can sustain personalised outreach even as regulations tighten. These gains validate that compliant identity resolution is becoming a growth accelerator rather than a cost centre.

5G roll-outs enabling ultra-low-latency campaigns across urban Asia

Commercial 5G networks now serve most tier-one Asian cities, pushing average mobile video load times well below 100 milliseconds. Marketers respond with interactive augmented-reality product demos that let users virtually place items in their environment before one-tap checkout. Live A/B switches executed at the network edge during a 2024 gaming convention in Seoul cut abandonment by nearly 25% versus identical creative on 4G. The experience reveals that bandwidth acts as a creative canvas, spurring immersive storytelling rather than functioning only as a distribution upgrade. As 5G densifies, the mobile marketing market will see richer asset formats and higher conversion efficiency.

Cookieless policies disrupt cross-app attribution worldwide

Third-party cookies are vanishing from mainstream browsers, shrinking cross-device graphs, and forcing marketers toward probabilistic measurement and incrementality experiments. Finance controllers who relied on user-level reports now train on lift-based dashboards focused on causal contribution. Learning cycles lengthen, yet budget allocations gradually stabilise because probabilistic signals tolerate privacy volatility. While performance marketers face near-term friction, the shift ultimately produces more resilient planning processes, cushioning the mobile marketing market against future regulatory swings.

Other drivers and restraints analyzed in the detailed report include:

- Quick-commerce boom drives specialised notification spend in South American capitals

- Retail media networks reshape European campaign supply chains

- Telco SMS firewall upgrades escalate A2P costs in Africa

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software contributed 67% of 2024 revenue, affirming its status as the operating backbone of the mobile marketing market. Vendors embed low-code journey builders and privacy dashboards that let brand teams test rules in near real time without engineering support. Services lines, though smaller, are expanding faster as enterprises seek guidance on clean-room deployment, creative automation and regional regulations. Advisory practices pivot from media arbitrage to technical enablement, carving fresh fee pools and rebalancing value capture along the supply chain. Over the forecast horizon, software upgrades will sustain retention, while service engagements deepen customer lock-in.

Technical services also mediate complex data-sharing agreements between advertisers and publishers, smoothing the adoption of consented identifiers. This dual need for technology and expertise positions hybrid providers to harvest greater wallet share. As a result, the mobile marketing market size tied to component services is projected to outpace overall market growth, even as software retains lead share.

Location intelligence holds a mid-teen fraction of the mobile marketing market size and is poised for a 22% CAGR, eclipsing other solution clusters by 2030. Enhanced stacks blend GPS, Bluetooth beacons, and venue Wi-Fi, pinpointing shopper dwell zones with sub-metre accuracy. Moment-specific offers then outperform generic coupons on redemption and basket value metrics. QR codes re-emerge as bridge technology between shelf and screen; a 2025 soft-drink promotion in Berlin used under-cap serialised codes to funnel consumers into a mobile game with instant rewards.

Push alerts remain indispensable for their superior open rates, but orchestration engines throttle frequency against predicted fatigue to prevent opt-outs. As retailers embed rich media into these alerts, location signals further sharpen timing, deepening engagement, and raising spending per user. Providers that integrate mapping APIs, analytics, and creative tooling within one interface widen their moat and expand their share within the wider mobile marketing market.

Mobile Marketing Market is Segmented by Component (Platform, Services), Solution Type (Mobile Web, SMS and MMS, and More), Distribution Channel (Social Media Marketing, Affiliate Marketing, and More), by Enterprise Size (Large Enterprises, Smes), Deployment Mode (Cloud, On-Premises), by End-User Industry (Retail and E-Commerce, Media and Entertainment / OTT), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38% of 2024 revenue, underscoring its role as a test bed for ad-tech innovation. State privacy amendments accelerate first-party data programs, leading to higher match rates and compliant identity graphs. Event-grade location platforms emerge ahead of the 2028 Los Angeles Olympics, merging ticketing, concessions, and sponsor messaging into unified mobile flows. Trials during the 2024 football playoffs demonstrated that dynamic offers aligned with concession wait times raised per-capita spend without adding foot traffic, showing operational upside beyond media value. Venture investment remains steady as publishers race to integrate privacy-safe IDs, supporting the broader mobile marketing market.

Asia-Pacific is forecast to post a 20% CAGR, reflecting the compounding effect of 5G speed, super-app ecosystems, and social commerce norms. A 2024 cosmetics campaign inside a leading Southeast Asian super-app combined augmented-reality try-ons with in-chat checkout, shrinking purchase journeys to under 60 seconds and tripling unit sales. In India, vernacular voice search expands reach, prompting platform owners to launch speech-driven ad formats for low-literacy segments. These innovations confirm that adoption curves depend on cultural habits as much as technology readiness. Rapid smartphone replacement cycles and low data costs further expand the mobile marketing market.

Europe's stringent privacy statutes restrict cookie-based reach, but retailers counter by monetising loyalty programs through closed-loop retail media networks. A 2025 Dutch grocery chain launched a self-service portal where suppliers buy sponsored product tiles that extend into the chain's mobile wallet, enabling end-to-end attribution within days. Nordic countries, although smaller, record the continent's highest per-user mobile engagement, proving that privacy-respecting personalisation thrives when consumer trust is secured. Regulatory clarity dampens short-term growth yet fosters long-term stability, supporting steady expansion of the mobile marketing market across the region.

- Alphabet Inc. (Google)

- Meta Platforms Inc.

- Apple Inc. (Apple Advertising)

- Microsoft Corporation

- Amazon.com Inc. (Amazon Ads)

- Twitter/X Corp.

- Snap Inc.

- Pinterest Inc.

- Verizon Communications Inc. (Yahoo Advertising)

- ATandT Inc.

- InMobi Pte Ltd

- AppLovin Corporation

- GroundTruth

- Criteo S.A.

- Airship

- Adobe Inc.

- Oracle Corporation

- Salesforce Inc.

- Publicis Groupe (Phonevalley)

- AdColony Inc.

- MoPub (AppLovin Exchange)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Privacy-safe Identifier Frameworks Boosting In-App Marketing ROI in North America

- 4.2.2 5G Roll-outs Enabling Ultra-Low-Latency Rich Media Campaigns Across Asia

- 4.2.3 Surge in Quick-Commerce Apps Fuelling Push Notification Spend in Urban South America

- 4.2.4 Retail Media Networks Mandating First-Party Mobile Data Partnerships in Europe

- 4.3 Market Restraints

- 4.3.1 Cookieless Policies Shrinking Device Graphs for Cross-App Attribution

- 4.3.2 Telco SMS Firewall Upgrades Escalating A2P Traffic Costs in Africa

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Value-Chain Analysis

- 4.8 Impact of COVID-19 on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Solution Type

- 5.2.1 Mobile Web

- 5.2.2 SMS and MMS

- 5.2.3 Location-Based Marketing / Geofencing

- 5.2.4 In-App and In-Game Advertising

- 5.2.5 Push Notification and Rich Media

- 5.2.6 QR-Code and Proximity Marketing

- 5.2.7 Emerging (AR/VR, Beacons, 5G Edge)

- 5.3 By Distribution Channel

- 5.3.1 Social Media Marketing

- 5.3.2 Affiliate Marketing

- 5.3.3 Omni-Channel / Retail Apps

- 5.3.4 Content and Influencer Marketing

- 5.3.5 Online Public Relations

- 5.3.6 Email and SMS Campaigns

- 5.3.7 In-Game / Esports

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Deployment Mode

- 5.5.1 Cloud

- 5.5.2 On-Premises

- 5.6 By End-user Industry

- 5.6.1 Retail and E-commerce

- 5.6.2 Media and Entertainment / OTT

- 5.6.3 BFSI

- 5.6.4 Healthcare and Life Sciences

- 5.6.5 Travel, Tourism and Hospitality

- 5.6.6 Telecommunications

- 5.6.7 Automotive

- 5.6.8 Education

- 5.6.9 Others (Government, Utilities)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Rest of Middle East and Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Alphabet Inc. (Google)

- 6.3.2 Meta Platforms Inc.

- 6.3.3 Apple Inc. (Apple Advertising)

- 6.3.4 Microsoft Corporation

- 6.3.5 Amazon.com Inc. (Amazon Ads)

- 6.3.6 Twitter/X Corp.

- 6.3.7 Snap Inc.

- 6.3.8 Pinterest Inc.

- 6.3.9 Verizon Communications Inc. (Yahoo Advertising)

- 6.3.10 ATandT Inc.

- 6.3.11 InMobi Pte Ltd

- 6.3.12 AppLovin Corporation

- 6.3.13 GroundTruth

- 6.3.14 Criteo S.A.

- 6.3.15 Airship

- 6.3.16 Adobe Inc.

- 6.3.17 Oracle Corporation

- 6.3.18 Salesforce Inc.

- 6.3.19 Publicis Groupe (Phonevalley)

- 6.3.20 AdColony Inc.

- 6.3.21 MoPub (AppLovin Exchange)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

行动行销市场:2026-2032年全球市场预测(依广告格式、装置类型、通路、作业系统及最终用户产业划分)行动互动市场:按装置类型、作业系统、网路类型、应用程式使用行为和购买管道划分 - 全球预测(2026-2032 年)

行动行销市场:2026-2032年全球市场预测(依广告格式、装置类型、通路、作业系统及最终用户产业划分)行动互动市场:按装置类型、作业系统、网路类型、应用程式使用行为和购买管道划分 - 全球预测(2026-2032 年) 2026年全球行动互动市场报告2026年全球QR码行动行销市场报告

2026年全球行动互动市场报告2026年全球QR码行动行销市场报告 全球行动行销市场规模、份额、趋势和成长分析报告(2026-2034)

全球行动行销市场规模、份额、趋势和成长分析报告(2026-2034) 行动行销市场-全球产业规模、份额、趋势、机会和预测,按组件、通路、组织规模、垂直产业、地区和竞争格局划分,2021-2031年预测

行动行销市场-全球产业规模、份额、趋势、机会和预测,按组件、通路、组织规模、垂直产业、地区和竞争格局划分,2021-2031年预测 防机器人拨号及品牌呼叫市场:2025年~2030年

防机器人拨号及品牌呼叫市场:2025年~2030年 全球行动行销市场规模、份额、趋势分析报告、按组成部分、公司规模、应用、最终用途、地区分類的展望和预测,2024 年至 2031 年全球行动互动市场规模(按解决方案、组织规模、最终用户产业、地区、范围和预测)

全球行动行销市场规模、份额、趋势分析报告、按组成部分、公司规模、应用、最终用途、地区分類的展望和预测,2024 年至 2031 年全球行动互动市场规模(按解决方案、组织规模、最终用户产业、地区、范围和预测)