|

市场调查报告书

商品编码

1850362

自助仓储:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Self Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

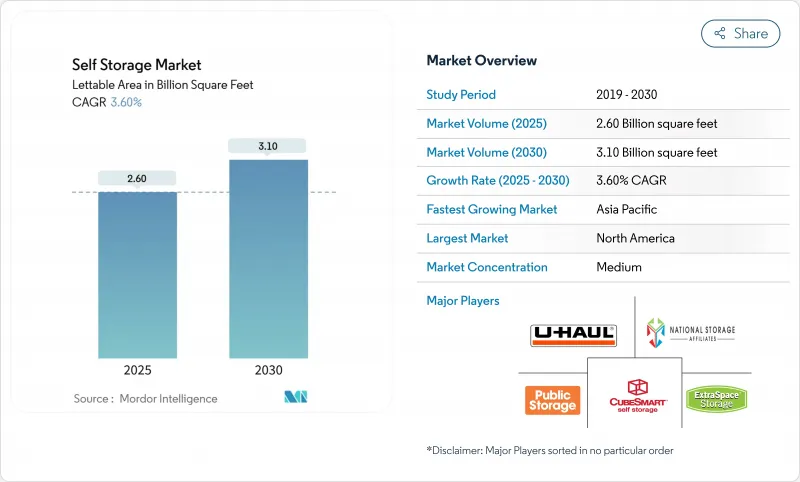

预计到 2025 年,自助仓储市场面积将达到 26 亿平方英尺,到 2030 年将达到 31 亿平方英尺,年复合成长率为 3.6%。

目前,自助仓储市场的成长主要依赖稳健的资产优化,而非疫情期间的大规模新建。都市化、电子商务小型企业的蓬勃发展以及对气候适应型资产的保护,共同支撑着结构性需求;而数位化租赁平台则能为采用智慧门禁系统的企业降低高达25%的营运成本。上市房地产投资信託基金(REITs)的整合扩大了市场规模,同时许多城市的规划限制也维持了较高的进入门槛,从而自助仓储了租金市场。温控仓储空间目前已占所有可出租空间的一半以上,且价格弹性最大,因为客户愿意为温湿度控制支付溢价。整体而言,自助仓储市场展现出稳健的现金流特征,即使在极端天气相关的保险费上涨的情况下,仍持续吸引机构资本的关注。

全球自助仓储市场趋势与洞察

都市化与居住空间缩小

大都会圈的快速人口成长是由求职者涌入人口密集的城市所驱动的,而这些城市的平均居住空间却不断缩小。预计到2030年,伦敦的人口将达到1000万,这表明人均居住空间的减少意味着可支配支出正转向外部存储,而不是更大的住宅。千禧世代占美国租屋者的40%,他们的流动性越来越强,这表明他们对灵活居住的需求持续存在。雅加达、马尼拉和墨西哥城也经历了类似的密集化进程,从而带动了对自助仓储的相应需求。这种需求的产生是由于都市区租赁住房的普遍存在,租户很少能管理自己的储存空间,而且经常搬家。当住房负担能力危机对居住空间带来压力时,自助仓储市场就成为城市居住的可行延伸。

电子商务微型商家的激增

低门槛的线上零售模式允许创业者在家办公,但需要靠近客户的小型仓库。因此,微型商家正在将标准储物柜改造成低成本的履约中心,从而加速提升其在自助仓储市场的商业份额。营运商现在透过提供专为包裹取件设计的装卸区、Wi-Fi 和全天候访问,以及用于保护需要温控的库存区域,来实现差异化竞争。这种商业性趋势提高了每平方英尺的平均收入,并提升了吞吐量,使其超越了传统的个人储存模式,成为核心利润驱动力。这种转变在人口密集的郊区尤为显着,因为叫车配送车队可以在一小时内送达消费者手中。

严格的区域划分与土地使用法规

市政当局越来越不鼓励新建仓库,而是倾向于发展员工人数更多、运转率的零售和工业。自2019年以来,美国已有超过15个州颁布了仓库建设禁令,欧洲一些城市议会也实施了类似的上限措施。虽然现有企业享有较高的入住率和价格优势,但供应限制阻碍了新企业的进入,并促使棕地选择对待开发区建筑进行改造而非新建。因此,精通合规的开发商将混合用途元素(例如街角咖啡馆和共享办公空间)打包开发,以规避审批障碍,但这增加了计划流程的复杂性和成本。

细分市场分析

儘管个人用户仍占据储物柜市场的大多数,但商业子部门的使用量正在不断增长。商业用户正以7.9%的复合年增长率快速成长,他们利用储物柜进行库存清理、季节性促销和文件归檔,从而推动了最后一公里配送模式的现代化。随着全通路零售商将库存集中在更靠近消费者的位置以控製配送成本,商业自助仓储市场规模将进一步扩大。个人用户占自助仓储市场总量的60%,而诸如结婚、离婚和搬迁等可预见的人生大事是导致租约终止和续约的主要原因。非接触式访问的普及提高了两个细分市场的自动化程度,87%的租户更倾向于使用智慧型手机进入储物柜。

从营运角度来看,小型企业客户的平均停留时间更长,并且会购买包裹取件等辅助服务,从而带来更高的每平方英尺可用面积收入。对于个人使用者而言,恆温储物柜因其适合存放传家宝、电子产品和收藏品而价格更高。因此,营运商制定了混合型商品行销,将亲民的品牌形象与企业级装卸平台功能结合。这种双层模式在不稀释品牌股权的前提下,扩大了可触及的自助仓储市场。

温控仓储占库存的52%,预计将以9.8%的复合年增长率成长,这主要得益于消费者对潮湿损害的日益关注以及电商商家对温度稳定环境的需求。虽然开发成本在每平方英尺35至70美元之间,但营运商可享有20%至50%的租金回报率和约11%的年利润率。标准非防风雨储物柜仍然是耐用品价格的领导者,但在极端天气事件中面临替代风险。可携式货柜仓储凭藉其门到门的便利性加剧了竞争,但该细分市场中资金较少的运营商往往缺乏土地资产来构建长期的市场准入壁垒。

该领域的经济效益有利于那些设计便于灵活维修的资产——例如空调升级、太阳能通风系统——从而在气候变迁预期上升的情况下,降低资本密集度。在高风险地区,保险公司越来越倾向于将抗震性能作为承保条件,这加速了隔热单元的普及,而这些单元本身就拥有较高的租金。因此,气候智慧型设计标准正逐渐成为新开发案的必备条件。

自助仓储市场按使用者类型(个人、企业)、储存类型(恆温、非恆温、可携式/货柜、其他)、租赁期限(短期(小于3个月)、中期(3-12个月)、其他)、单元面积(小型(小于50平方英尺)、中型(50-100平方英尺))和地区进行细分。以上所有细分市场的市场规模和预测均以美元计价。

区域分析

北美将继续保持主导地位,预计到2024年将占全球销售额的45%。成熟的自存仓收益率优于许多其他房地产资产类别,但纽约和波特兰等城市的规划限制正在减缓新增供应,并推动将过时的零售空间改造为垂直仓储。北美自助仓储市场规模受益于先进的数位平台,但受气候变迁影响的沿海次级市场面临着不断上涨的保险成本。

亚太地区是成长最快的市场,复合年增长率达9.3%。以三菱地所和帕尔玛(Parma)为代表的日本伙伴关係模式,正将机构资本引入提供非接触式服务的多层设施。帕尔玛的业务流程外包(BPO)引擎管理日本约60%的营运商,从而形成网路效应。澳洲的年市场规模达20亿美元,入住率接近90%,吸引了贝莱德以4亿美元收购StoreLocal,以及Public Storage以19亿美元竞标Abacus Storage。新加坡和韩国的成长速度相对较慢,但随着其高密度公寓市场的成熟,非接触式储存的普及率也不断提高。

欧洲正经历稳定扩张,这得益于其1.5亿平方英尺的办公大楼存量,覆盖近5亿人口。舒尔加德预计2024年营收将达4.067亿欧元(4.342亿美元),较前一年成长13%。欧洲大陆的营运商正实现高运转率,充分利用其多元化的用户群体,包括搬家公司、小型企业和文件储存公司。外汇收益和与办公大楼市场週期较低的相关性,对寻求稳定收入的退休基金极具吸引力。

拉丁美洲和中东地区尚处于起步阶段,但前景广阔。墨西哥城和圣保罗的中阶不断壮大,电商经销商需求旺盛,但所有权分散和机构资本有限阻碍了规模扩张。波湾合作理事会成员国也迎来了早期投资,因为外籍人士需要温控空间来保护他们的物品免受酷暑侵袭。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 都市化与生活空间缩小

- 小型电子商务企业的崛起

- 住宅房地产价格上涨

- 数位化、非接触式租赁平台

- 自助仓储作为微型仓配中心

- 对具有气候适应能力的资产保护的需求

- 市场限制

- 严格的区域划分与土地使用法规

- 成熟都会大都会圈供应过剩地区

- 极端天气导致保险费上涨

- 智慧设施中的网路安全风险

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依使用者类型

- 个人

- 商业

- 依储存类型

- 气候控制

- 没有空调

- 可携式/容器为基础的

- 车辆及特产(房车、船隻、葡萄酒)

- 按租赁期间

- 短期(少于3个月)

- 中期(3-12个月)

- 长期(12个月或以上)

- 按单位大小

- 小型(小于50平方英尺)

- 中等大小(50-100平方英尺)

- 大型(100-200平方英尺)

- 超大(超过 200 平方英尺)

- 按地区

- 北美洲

- 美国

- 加拿大

- 南美洲

- 巴西

- 阿根廷

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚洲

- 中国

- 日本

- 澳洲

- 印度

- 中东和非洲

- GCC

- 南非

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Public Storage

- Extra Space Storage Inc.

- U-Haul International Inc.

- CubeSmart LP

- National Storage Affiliates Trust

- Life Storage Inc.

- Safestore Holdings PLC

- StorageMart

- Shurgard Self-Storage SA

- Big Yellow Group PLC

- Prime Storage Group

- Metro Storage LLC

- SmartStop Asset Management LLC

- Clutter Inc.

- MakeSpace Inc.

- Kennards Self Storage

- Access Self Storage Ltd.

- Urban Self Storage Inc.

- Global Self Storage Inc.

- World Class Capital Group LLC(Great Value Storage)

- Amsdell Cos./Compass Self Storage

- All Storage

第七章 市场机会与未来展望

第八章 评估閒置频段和未满足的需求

The self storage market spans 2.6 billion square feet in 2025 and is forecast to reach 3.1 billion square feet by 2030, expanding at a 3.6% CAGR.

The self storage market now grows through disciplined asset optimization rather than the pandemic-era rush to build new sites. Urbanization, e-commerce micro-merchants, and climate-resilient asset protection underpin structural demand, while digitized leasing platforms trim operating expenses by up to 25% for operators deploying smart-access systems. Consolidation among public REITs raises operational scale, yet zoning limits in many cities keep barriers to entry high, supporting rental rate stability. Climate-controlled capacity-already more than half of total rentable space-shows the strongest price elasticity as customers pay premiums for temperature and humidity safeguards. Overall, the self storage market demonstrates durable cash-flow characteristics that continue to attract institutional capital even amid rising insurance costs linked to extreme weather.

Global Self Storage Market Trends and Insights

Urbanization & Shrinking Living Spaces

Rapid metropolitan population growth stems from job-seekers flocking to dense cities where average apartment footprints trend downward. London's population trajectory toward 10 million by 2030 illustrates how reduced per-capita living space channels discretionary spending into external storage rather than larger accommodation. Millennials-who make up 40% of U.S. renters-exhibit higher mobility, translating into recurring demand for flexible units. Similar densification in Jakarta, Manila, and Mexico City drives parallel storage uptake. Urban rental dominance magnifies this need because tenants rarely control on-site storage, and recurring relocations compound volume requirements. Where housing affordability crises squeeze living space, the self storage market becomes a practical extension of the urban dwelling.

Proliferation of E-commerce Micro-merchants

Low-barrier online retail models enable entrepreneurs to operate from homes yet require mini-warehousing close to customers. Micro-merchants therefore convert standard lockers into low-cost fulfillment nodes, accelerating the commercial share of the self storage market. Operators now differentiate by offering loading bays, Wi-Fi, and 24/7 access designed for shipment pick-ups, while climate-controlled sections protect temperature-sensitive inventory. This commercial pivot lifts average revenue per square foot and pushes throughput higher than traditional personal storage, making the segment a core margin driver. The shift is most visible in dense suburbs where ride-share delivery fleets can reach consumers within one-hour windows.

Stringent Zoning & Land-use Regulations

Municipalities increasingly block new storage construction, preferring retail or industrial developments with higher headcount and tax multipliers. More than 15 U.S. states have enacted moratoria since 2019, and European city councils apply similar caps. Existing operators see occupancy and pricing tailwinds, yet supply constraints hinder new entrants and encourage brownfield conversions over greenfield builds. Compliance-savvy developers thus bundle mixed-use components-street-level cafes, co-working zones-to pass entitlement hurdles, adding complexity and cost to the project pipeline.

Other drivers and restraints analyzed in the detailed report include:

- Rising Residential Real-estate Costs

- Self-storage as Micro-fulfillment Hubs

- Escalating Insurance Premiums from Extreme Weather

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The business sub-sector contributes rising volume even though personal customers still occupy the majority of lockers. Business users, expanding at a 7.9% CAGR, leverage units for inventory spill-over, seasonal promotions, and document archiving, thereby modernizing last-mile economics. Self storage market size for business users is set to accelerate as omnichannel retailers balance stock closer to consumers to suppress delivery costs. The personal segment retains 60% of overall self storage market share, anchored by predictable life-event triggers-marriage, divorce, relocation-that sustain churn and lease renewals. Contactless access means 87% of all renters now prefer smartphone entry, pushing automation across both sub-segment.

Operationally, small-business customers exhibit longer average stay durations and purchase ancillary services such as package acceptance, raising revenue per available square foot. For personal renters, climate-controlled lockers grant premium rates for heirlooms, electronics, and collectibles. Operators therefore engineer hybrid merchandising, combining residential-friendly branding with enterprise-grade dock features. This two-tier model widens the addressable self storage market without diluting brand equity.

Climate-controlled capacity represents 52% of stock and is forecast to grow at 9.8% CAGR, propelled by heightened consumer awareness of humidity damage and by e-commerce merchants seeking temperature-stable conditions. Development costs run USD 35-70 per square foot, yet operators enjoy 20-50% rental premiums and roughly 11% annual profit margins. Standard non-climate lockers remain price leaders for durable goods but face substitution risk where extreme weather intensifies. Portable container storage adds competitive pressure by offering door-to-door convenience; however, capex-light operators in this niche often lack land assets to secure long-term barriers to entry.

Segment economics favor assets engineered for flexible retrofits-HVAC upgrades, solar-powered ventilation-that keep capital intensity manageable as climate expectations rise. In high-risk zones, insurers increasingly condition coverage on resilient construction, accelerating adoption of insulated units that already command premium rents. As a result, climate-ready design standards are becoming table stakes for new developments.

The Self Storage Market Segments Into User Type (Personal, Business), by Storage Type (Climate-Controlled, Non-Climate-Controlled, Portable / Container-Based, and More), by Lease Duration (Short-Term (<3 Months), Mid-Term (3-12 Months) and More), Unit Size (Small (<50 Sq Ft), Medium (50-100 Sq Ft)) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

Geography Analysis

North America maintains leadership with 45% of global revenue in 2024, reflecting deep consumer familiarity and institutional consolidation. Mature yields exceed many real-estate asset classes, but zoning restrictions in cities such as New York and Portland slow new supply, encouraging conversions of obsolete retail into vertical storage. The self storage market size in North America benefits from advanced digital platforms, yet climate-exposed coastal sub-markets face insurance-driven cost inflation.

Asia-Pacific is the fastest-growing theater at 9.3% CAGR. Japan's partnership model-exemplified by Mitsubishi Estate and Palma-channels institutional capital into multi-story facilities offering contactless service, while Palma's BPO engine manages roughly 60% of national operators, creating network effects. Australia, valued at USD 2 billion annually, posts near 90% occupancy, enticing BlackRock's USD 400 million StoreLocal buy-in and Public Storage's USD 1.9 billion bid for Abacus Storage King Singapore and South Korea trail but show rising adoption as dense condo markets mature.

Europe delivers steady expansion underpinned by a 150 million sq ft stock base spread across almost 500 million inhabitants. Shurgard's revenue rose 13% YoY to EUR 406.7 million (USD 434.2 million) in 2024, with the Lok'nStore deal doubling its UK footprint and signaling ongoing consolidation . Continental operators leverage diverse user mixes-personal movers, SMEs, document-archiving firms-to achieve high occupancy. Currency-hedged returns and low correlation to office cycles attract pension funds seeking income stability.

Latin America and the Middle East remain nascent yet promising. Mexico City and Sao Paulo experience strong demand from growing middle classes and e-commerce sellers, but fragmented ownership and limited institutional capital slow scale-up. Gulf Cooperation Council economies witness early-stage investments as expatriate populations search for temperature-controlled space to shield belongings from intense heat.

- Public Storage

- Extra Space Storage Inc.

- U-Haul International Inc.

- CubeSmart LP

- National Storage Affiliates Trust

- Life Storage Inc.

- Safestore Holdings PLC

- StorageMart

- Shurgard Self-Storage SA

- Big Yellow Group PLC

- Prime Storage Group

- Metro Storage LLC

- SmartStop Asset Management LLC

- Clutter Inc.

- MakeSpace Inc.

- Kennards Self Storage

- Access Self Storage Ltd.

- Urban Self Storage Inc.

- Global Self Storage Inc.

- World Class Capital Group LLC (Great Value Storage)

- Amsdell Cos./Compass Self Storage

- All Storage

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanization & shrinking living spaces

- 4.2.2 Proliferation of e-commerce micro-merchants

- 4.2.3 Rising residential real-estate costs

- 4.2.4 Digitized, contact-free leasing platforms

- 4.2.5 Self-storage as micro-fulfillment hubs (under-reported)

- 4.2.6 Climate-resilient asset preservation demand (under-reported)

- 4.3 Market Restraints

- 4.3.1 Stringent zoning & land-use regulations

- 4.3.2 Oversupply pockets in mature metros

- 4.3.3 Escalating insurance premiums from extreme weather (under-reported)

- 4.3.4 Cyber-security risks for smart facilities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS

- 5.1 By User Type

- 5.1.1 Personal

- 5.1.2 Business

- 5.2 By Storage Type

- 5.2.1 Climate-controlled

- 5.2.2 Non-climate-controlled

- 5.2.3 Portable / Container-based

- 5.2.4 Vehicle & Specialty (RV, boat, wine)

- 5.3 By Lease Duration

- 5.3.1 Short-term (<3 months)

- 5.3.2 Mid-term (3-12 months)

- 5.3.3 Long-term (>12 months)

- 5.4 By Unit Size

- 5.4.1 Small (<50 sq ft)

- 5.4.2 Medium (50-100 sq ft)

- 5.4.3 Large (100-200 sq ft)

- 5.4.4 Mega (>200 sq ft)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.4 Asia

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 Australia

- 5.5.4.4 India

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Public Storage

- 6.4.2 Extra Space Storage Inc.

- 6.4.3 U-Haul International Inc.

- 6.4.4 CubeSmart LP

- 6.4.5 National Storage Affiliates Trust

- 6.4.6 Life Storage Inc.

- 6.4.7 Safestore Holdings PLC

- 6.4.8 StorageMart

- 6.4.9 Shurgard Self-Storage SA

- 6.4.10 Big Yellow Group PLC

- 6.4.11 Prime Storage Group

- 6.4.12 Metro Storage LLC

- 6.4.13 SmartStop Asset Management LLC

- 6.4.14 Clutter Inc.

- 6.4.15 MakeSpace Inc.

- 6.4.16 Kennards Self Storage

- 6.4.17 Access Self Storage Ltd.

- 6.4.18 Urban Self Storage Inc.

- 6.4.19 Global Self Storage Inc.

- 6.4.20 World Class Capital Group LLC (Great Value Storage)

- 6.4.21 Amsdell Cos./Compass Self Storage

- 6.4.22 All Storage

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

8 White-space & Unmet-need Assessment

自助仓储市场规模、份额、按类型、单位规模、最终用途和地区分類的成长分析 - 产业预测,2025 年至 2032 年

自助仓储市场规模、份额、按类型、单位规模、最终用途和地区分類的成长分析 - 产业预测,2025 年至 2032 年 2025年全球自助仓储市场报告

2025年全球自助仓储市场报告 美国自助仓储:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

美国自助仓储:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 2025 年至 2033 年自助储存市场规模、份额、趋势及预测(按储存单元大小、最终用途和地区)日本自助储存市场报告(按储存单元大小(小型储存单元、中型储存单元、大型储存单元)、最终用途(个人、商业)和地区划分)2025 年至 2033 年亚太地区自助仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

2025 年至 2033 年自助储存市场规模、份额、趋势及预测(按储存单元大小、最终用途和地区)日本自助储存市场报告(按储存单元大小(小型储存单元、中型储存单元、大型储存单元)、最终用途(个人、商业)和地区划分)2025 年至 2033 年亚太地区自助仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 自助仓储市场报告:2031 年趋势、预测与竞争分析

自助仓储市场报告:2031 年趋势、预测与竞争分析 自助储存市场 - 全球产业规模、份额、趋势、机会和预测,按应用程式、最终用户、地区、竞争细分,2020-2030F新加坡自助仓储:市场占有率分析、产业趋势和成长预测(2025-2030 年)

自助储存市场 - 全球产业规模、份额、趋势、机会和预测,按应用程式、最终用户、地区、竞争细分,2020-2030F新加坡自助仓储:市场占有率分析、产业趋势和成长预测(2025-2030 年) 全球自助仓储与搬运服务市场,2025-2029

全球自助仓储与搬运服务市场,2025-2029