|

市场调查报告书

商品编码

1851543

LED构装:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030年)LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

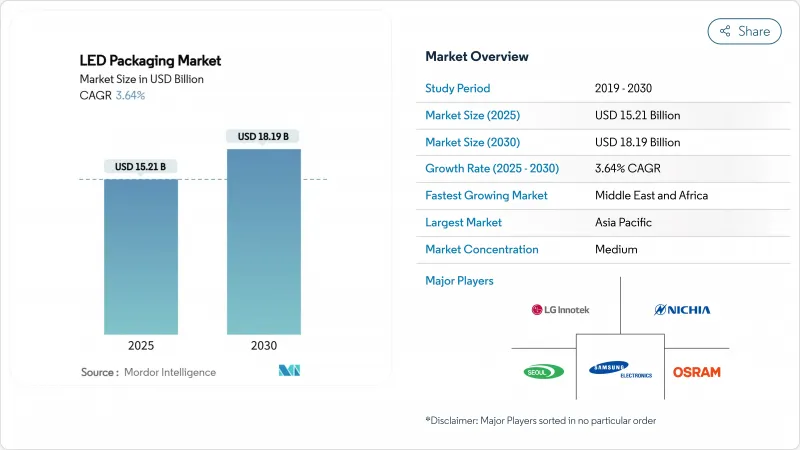

预计到 2025 年, LED构装市场规模将达到 152.1 亿美元,到 2030 年将达到 181.9 亿美元,年复合成长率为 3.64%。

价值成长并非来自大众化灯具,而是来自高阶细分市场,例如汽车自我调整头灯、UV-C紫外线杀菌模组和mini-LED显示器背光。性能驱动型封装架构,包括晶片级封装(CSP)和先进陶瓷基板,正随着汽车製造商和麵板製造商对更严格的热容差和更薄设计的需求而不断扩大市场份额。政策主导的萤光禁令以及政府对化合物半导体产能的资助进一步推动了LED构装市场的发展,而地缘政治供应链本地化也在影响投资决策。同时,智慧财产权纠纷和基板成本的波动提高了进入门槛并增加了资本需求,从而削弱了成长动能。

全球LED构装市场趋势与洞察

电视和IT面板向迷你/微型LED背光技术的过渡

Mini LED背光技术的应用正在重塑高阶电视和显示器市场,各大品牌利用100-200微米的晶片实现了超过2000个局部调光区域,峰值亮度超过2000尼特。封装在电路板上的製程保持了材料成本的竞争力,而晶片封装在玻璃上的製程则正在兴起,用于超薄工业设计。由于Mini LED在阳光下可视性和使用寿命方面优于OLED,汽车驾驶座显示器的可寻址面积正在不断扩大。高密度阵列会产生高热负荷,因此需要高效散热且不增加厚度的陶瓷基板和CSP解决方案。随着消费性电子製造商陆续公布其Mini LED蓝图,上游封装公司正在确保产能以支援多年的面板更换週期,从而扩大了LED构装市场。

CSP在欧洲和韩国的汽车头灯领域迅速普及。

晶片级封装无需引线键合,显着降低了光学高度,支援超过 150°C 的结温,同时降低 20% 的消费量。领先的自我调整光束系统,例如 ams Osram 的 EVIYOS 2.0(整合 25,600 个可独立寻址像素),展示了 CSP 如何实现对光分布的精确控制。欧洲关于眩光和能源效率的法规正在加速这一转变,韩国供应商已将 CSP 用于空间受限的车内环境照明模组。一级头灯规范要求 10 万小时的使用寿命,迫使封装厂商对陶瓷腔体和高导热晶粒晶片贴装进行认证。这一趋势凸显了LED构装市场的策略转变,高端汽车照明正将 CSP 作为安全关键灯具的参考架构。

蓝宝石芯片价格波动

蓝宝石晶圆占封装成本的20%之多,但其季度价格波动往往超过30%,挤压了代工封装厂商的毛利率。晶体生长集中在亚太地区少数几家供应商手中,这意味着地缘政治摩擦和电力短缺可能迅速导致供不应求。儘管主要厂商正在探索雷射剥离技术以实现基板的再利用,但高昂的资本投入限制了该技术的应用,使其仅限于一级厂商。这使得中小企业在没有回收对冲措施的情况下,面临原料风险,削弱了其扩大生产的能力,并限制了整个LED构装市场的韧性。

细分市场分析

CSP(复合表面封装)的出货量正以5.4%的复合年增长率成长,反映出其在汽车头灯和超薄显示器背光等领域的应用日益广泛。从以金额为准来看,CSP在LED构装市场中的份额也在不断增长。随着对整修照明的需求持续成长,SMD(表面贴装元件)的出货量预计在2024年将占到43%,因为其单位成本超过了小型化带来的优势。覆晶型LED主要面向3W以上的细分市场,虽然专利费较高,但由于其能够製造符合自我调整光束法规的紧凑型光学元件,因此在LED构装市场中保持着独特的份额。混合型和无封装结构仍处于实验阶段,受到贴片週期时间和重工挑战的限制。

晶圆级封装的持续创新模糊了晶片製造和封装组装之间的界限。台湾的半导体组装测试外包(OSAT)供应商正在扩大扇出型CSP生产线,以满足电视和智慧型手机背光製造商的紧急订单。另一方面,欧洲一级汽车製造商透过强制执行严格的AEC-Q102可靠性测试来确保双重采购,从而有效地将新兴供应商拒之门外。这种分化凸显了LED构装市场中成本优化和效能优化两种模式并存的现况。

到2024年,导线架架构仍将占出货量的34%,但随着设计人员追求导热係数超过150 W/mK,氮化铝基陶瓷腔体的出货量将增加4.3%。汽车、UV-C和园艺照明灯具将推高结温,导致有机基板过早劣化,因此陶瓷成为必需品。因此,基于陶瓷基板的LED构装市场将与功率密度呈线性成长,而非与出货量呈线性成长。

封装材料化学的演进与LED封装技术的发展同步进行。具有更优异排气性能的抗紫外线硅凝胶可防止在灭菌循环过程中变色,而银铜合金接合线则抵消了黄金带来的成本增加。远程磷光体和玻璃封装磷光体解决方案可望实现稳定的色移,但由于资本密集度高且年复合增长率为-0.5%,中型厂商仍在观望。因此,材料的选择已成为一种策略性对冲。陶瓷材料用于提高热裕度,有机材料用于降低成本,玻璃封装磷光体用于提高频谱均匀性,所有这些材料都在LED构装市场中争夺市场份额。

区域分析

亚太地区占全球LED构装市场68%的份额,其主导地位源自于垂直整合的电子供应链和国内消费。中国的基础建设和节能政策推动了销售量,而台湾OSAT(外包半导体封装测试)领军企业如日月光(ASE)在人工智慧硬体订单的推动下,2025年第二季营收季订单11%。日本正利用其在汽车级可靠性方面的专业知识,而韩国面板製造商则在推广CSP(聚光灯太阳能)车头灯模组。资料中心建设对高显色指数(CRI)陶瓷封装的需求也将推动该地区的成长。

北美的成长轨迹取决于监管催化剂,而非自然维修周期。萤光禁令和美国能源部能源效率法规确保了LED灯在2030年前的替代市场,从而保证了基准出货量不受宏观经济波动的影响。美国《晶片技术创新法案》(CHIPS Act)的激励措施,包括为Wolfspeed的碳化硅生产线提供7.5亿美元的资金,体现了政府对化合物半导体供应链的政策支持。

欧洲市场正朝着高端汽车需求和严格的环保设计标准发展。德国汽车製造商率先部署自我调整头灯,并倾向于采用CSP和覆晶封装,而更严格的眩光法规则要求实现像素级控制。同时,永续性框架优先考虑生命週期光通量维持率,从而强化了对陶瓷基板波湾合作理事会的基础设施计划正在其碳减排蓝图图下整合智慧节能照明。南美洲的市占率落后,但随着交通走廊升级和电费上涨,LED维修在经济上更具吸引力,因此仍有成长空间。这些区域趋势清晰地表明,监管意图和基础设施投资将如何重新平衡整个LED构装市场的需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电视和IT面板向迷你/微型LED背光技术的过渡

- CSP技术在欧洲和韩国迅速应用于汽车头灯。

- 北美政策主导的萤光逐步淘汰

- 亚洲资料中心蓬勃发展,推动高显色指数照明应用。

- 用于即时消毒的UV-C LED需求激增

- 台湾和中国的LED构装(OSAT)业务成长

- 市场限制

- 蓝宝石芯片价格波动

- 覆晶设计中的智慧财产权交叉授权壁垒

- 转型为磷光体玻璃需要大量资金投入

- 3W以上封装的功率密度温度控管限制

- 生态系分析

- 监理与技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按包装类型

- 表面黏着型元件(SMD)

- 板载晶片(COB)

- 晶片级封装(CSP)

- 覆晶

- 混合/无封装设计

- 透过包装材料

- 导线架和基板

- 陶瓷基板

- 键合线/晶片连接

- 封装树脂和硅胶镜片

- 磷光体和远程磷光体膜

- 按输出范围

- 低/中功率(小于1瓦)

- 高功率(1至3瓦)

- 高功率(超过 3W)

- 透过使用

- 一般照明

- 住宅

- 商业和工业

- 汽车照明

- 外观(头灯、日行灯)

- 内部的

- 背光

- 电视机和显示器

- 手机和平板电脑

- Flash &指示牌

- 手机闪光灯

- 数位电子看板和广告牌

- 专门食品和紫外线/红外线

- 园艺

- 紫外线C波段消毒

- 一般照明

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 其他南美洲

- 亚太地区

- 中国

- 日本

- 印度

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- OSRAM Opto Semiconductors GmbH

- LG Innotek Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding BV

- Everlight Electronics Co., Ltd.

- Cree LED(Smart Global Holdings)

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- TT Electronics plc

- Bridgelux, Inc.

- Epistar Corp.(Ennostar)

- Lite-On Technology Corp.

- Lextar Electronics Corp.

- Edison Opto Corp.

- Dominant Opto Technologies Sdn Bhd

- NationStar Optoelectronics Co., Ltd.

- MLS Co., Ltd.(Forest Lighting)

第七章 市场机会与未来展望

The LED packaging market size stands at USD 15.21 billion in 2025 and is forecast to touch USD 18.19 billion by 2030, registering a 3.64% CAGR.

Incremental value is coming less from commoditized lamps and more from premium niches such as adaptive automotive headlamps, UV-C disinfection modules and Mini-LED display backlights. Performance-oriented package architectures, notably chip-scale package (CSP) and advanced ceramic substrates, are gaining share as carmakers and panel makers demand tighter thermal tolerances and thinner form factors. Policy-driven fluorescent lamp bans and government funding for compound-semiconductor capacity add further impetus to the LED packaging market, while geopolitical supply-chain localization shapes investment decisions. Simultaneously, intellectual-property disputes and substrate cost volatility temper the growth trajectory by raising barriers to entry and amplifying capital requirements.

Global LED Packaging Market Trends and Insights

Transition to Mini/Micro-LED Backlighting in TVs and IT Panels

Mini-LED backlight adoption is reshaping premium TV and monitor categories as brands leverage 100-200 µm chips to unlock >2,000 local-dimming zones and >2,000-nit peak brightness. Package-on-Board formats keep the bill-of-materials competitive, yet Chip-on-Glass is emerging for ultra-slim industrial designs. Automotive cockpit displays extend the addressable volume because sunlight readability and life-cycle robustness favor Mini-LED over OLED. Densely packed arrays trigger higher thermal loads, directing demand toward ceramic-substrate and CSP solutions that dissipate heat efficiently without sacrificing thickness. As consumer-electronics makers publicize Mini-LED roadmaps, upstream packaging houses position capacity to catch a multi-year panel-replacement cycle, thereby widening the LED packaging market.

Rapid CSP Adoption in Automotive Headlamps across Europe and Korea

Chip-scale packages eliminate wire bonds and significantly shrink optical height, reducing energy draw by 20% while handling junction temperatures beyond 150 °C. Flagship adaptive-beam systems such as ams OSRAM's EVIYOS 2.0 integrate 25,600 individually addressable pixels, demonstrating how CSP enables finer light distribution control. European regulations on glare and energy efficiency accelerate the switch, and Korean suppliers use CSP for constrained interior ambient lighting modules. Headlamp Tier-1s stipulate 100,000-hour lifetimes, compelling package houses to qualify ceramic cavity and high-thermal-conductivity die attach. The momentum underscores a strategic inflection where premium automotive lighting steers the LED packaging market toward CSP as the reference architecture for safety-critical luminaires.

Volatility of Sapphire Wafer Pricing

Sapphire wafers contribute up to 20% of package cost, yet quarterly price swings often top 30%, squeezing gross margins for contract packagers. Because crystal growth is clustered in a handful of APAC vendors, geopolitical friction or power rationing quickly feeds into spot shortages. Large manufacturers explore Laser Lift-Off to reclaim substrates for reuse, but the capex burden confines adoption to top-tier producers. Smaller firms thus endure raw-material risk without the hedge of recycling, dampening their ability to scale output and constraining the LED packaging market's overall elasticity.

Other drivers and restraints analyzed in the detailed report include:

- Policy-Led Phase-Out of Fluorescent Lamps in North America

- Data-Centre Boom Driving High-CRI Lighting in Asia

- IP Cross-Licensing Barriers for Flip-Chip Designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CSP shipments climb at a 5.4% CAGR, reflecting their rising acceptance in automotive headlights and ultra-thin display backlights. In value terms, CSP contributes a growing slice of the LED packaging market size as lamp makers pay premiums for thermal headroom and pixel-level control. SMD formats still anchor 43% of shipments in 2024, sustaining refurb-lighting demand where unit cost outweighs miniaturization benefits. Flip-chip variants target >3 W niches, and while their royalty load is high, they enable compact optics aligned with adaptive-beam regulations, thereby sustaining a differentiated share of the LED packaging market. Hybrid and package-free constructs stay experimental, constrained by pick-and-place cycle-times and rework challenges.

Continuous innovation around wafer-level encapsulation blurs the boundary between chip fabrication and package assembly. Outsourced semiconductor assembly and test (OSAT) providers in Taiwan scale fan-out CSP lines to satisfy surge orders from TV and smartphone backlight makers. Conversely, European automotive Tier-1s secure dual sourcing by mandating stringent AEC-Q102 reliability tests, effectively locking out nascent vendors. The bifurcation accentuates how cost-optimized versus performance-optimized lanes coexist in the LED packaging market.

Lead-frame architectures still represented 34% of shipments in 2024, yet ceramic cavities based on aluminum nitride grow at 4.3% as designers chase thermal conductivity >150 W/mK. Automotive, UV-C and horticulture luminaires push junction temperatures where organic boards degrade prematurely, making ceramics a necessity. The LED packaging market size for ceramic substrates thus scales alongside power densities instead of shipment tonnage.

Encapsulation chemistries evolve in lockstep. UV-resistant silicone gels with improved outgassing properties prevent discoloration during sterilization cycles, while silver-copper alloy bonding wires offset gold cost exposure. Although remote-phosphor and phosphor-in-glass solutions promise color-shift stability, mid-tier players defer the investment, wary of -0.5% CAGR drag from capital intensity. Hence, material choice has become a strategic hedge: ceramics for thermal margin, organics for cost, and glass-embedded phosphors for spectral uniformity-all vying for allocation within the LED packaging market.

The LED Packaging Market Report is Segmented by Packaging Type (Surface-Mount Device, Chip-On-Board, Chip-Scale Package, and More), Package Material (Lead-Frame and Substrate, Ceramic Substrate, and More), Power Range (Low and Mid-Power (Less Than 1 W), High-Power (1-3 W), and More), Application (General Lighting, Automotive Lighting, Backlighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commands 68% of the LED packaging market, a dominance rooted in its vertically integrated electronics supply chain and domestic consumption. China's infrastructure rollouts and energy-efficiency mandates drive volume, while Taiwan's OSAT giants such as ASE posted 11% sequential revenue growth in Q2 2025 on the back of AI-hardware orders. Japan leans on auto-grade reliability know-how, and South Korea's panel makers advance CSP headlamp modules. Regional growth also leverages data-centre build-outs that require high-CRI ceramic packages.

North America's trajectory hinges on regulatory catalysts rather than organic renovation cycles. The fluorescent lamp ban and DOE efficacy rules create a captive LED replacement window to 2030, ensuring baseline shipments regardless of macro swings. US CHIPS Act incentives, including USD 750 million for Wolfspeed's silicon-carbide line, illustrate policy support for compound-semiconductor supply chains.

Europe's market tilts toward premium automotive demand and strict eco-design codes. German OEMs pioneer adaptive headlamp rollouts that favor CSP and flip-chip packages, while stricter glare regulations necessitate pixel-level control. Simultaneously, sustainability frameworks prioritize lifetime lumen maintenance, reinforcing the preference for ceramic substrates. Middle East & Africa, though smaller today, is forecast to expand at a 5.2% CAGR as Gulf Cooperation Council infrastructure projects integrate smart, energy-efficient lighting under carbon-reduction roadmaps. South America trails in share but holds upside from transportation-corridor upgrades and rising electricity tariffs that make LED retrofits financially compelling. Together, these regional vectors underscore how regulatory intent and infrastructure investment recalibrate demand across the LED packaging market.

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- OSRAM Opto Semiconductors GmbH

- LG Innotek Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Everlight Electronics Co., Ltd.

- Cree LED (Smart Global Holdings)

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- TT Electronics plc

- Bridgelux, Inc.

- Epistar Corp. (Ennostar)

- Lite-On Technology Corp.

- Lextar Electronics Corp.

- Edison Opto Corp.

- Dominant Opto Technologies Sdn Bhd

- NationStar Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transition to Mini/Micro-LED Backlighting in TVs and IT Panels

- 4.2.2 Rapid CSP Adoption in Automotive Headlamps across Europe and Korea

- 4.2.3 Policy-Led Phase-Out of Fluorescent Lamps in North America

- 4.2.4 Data-Centre Boom Driving High-CRI Lighting in Asia

- 4.2.5 Surge in UV-C LED Demand for Point-of-Use Disinfection

- 4.2.6 Outsourced LED Packaging (OSAT) Growth in Taiwan and China

- 4.3 Market Restraints

- 4.3.1 Volatility of Sapphire Wafer Pricing

- 4.3.2 IP Cross-Licensing Barriers for Flip-Chip Designs

- 4.3.3 Capital-Intensive Transition to Phosphor-in-Glass

- 4.3.4 Power Density Heat-Management Limitations Above 3 W Packages

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Packaging Type

- 5.1.1 Surface-Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip-Scale Package (CSP)

- 5.1.4 Flip-Chip

- 5.1.5 Hybrid/Package-Free Designs

- 5.2 By Package Material

- 5.2.1 Lead-Frame and Substrate

- 5.2.2 Ceramic Substrate

- 5.2.3 Bonding Wire/Die-Attach

- 5.2.4 Encapsulation Resin and Silicone Lens

- 5.2.5 Phosphor and Remote Phosphor Films

- 5.3 By Power Range

- 5.3.1 Low and Mid-Power (Less than 1 W)

- 5.3.2 High-Power (1-3 W)

- 5.3.3 Ultra-High-Power (Above 3 W)

- 5.4 By Application

- 5.4.1 General Lighting

- 5.4.1.1 Residential

- 5.4.1.2 Commercial and Industrial

- 5.4.2 Automotive Lighting

- 5.4.2.1 Exterior (Headlamp, DRL)

- 5.4.2.2 Interior

- 5.4.3 Backlighting

- 5.4.3.1 TV and Monitor

- 5.4.3.2 Mobile and Tablet

- 5.4.4 Flash and Signage

- 5.4.4.1 Mobile Camera Flash

- 5.4.4.2 Digital Signage and Billboards

- 5.4.5 Specialty and UV/IR

- 5.4.5.1 Horticulture

- 5.4.5.2 UV-C Disinfection

- 5.4.1 General Lighting

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Nichia Corporation

- 6.4.3 OSRAM Opto Semiconductors GmbH

- 6.4.4 LG Innotek Co., Ltd.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 Cree LED (Smart Global Holdings)

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Citizen Electronics Co., Ltd.

- 6.4.12 TT Electronics plc

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Epistar Corp. (Ennostar)

- 6.4.15 Lite-On Technology Corp.

- 6.4.16 Lextar Electronics Corp.

- 6.4.17 Edison Opto Corp.

- 6.4.18 Dominant Opto Technologies Sdn Bhd

- 6.4.19 NationStar Optoelectronics Co., Ltd.

- 6.4.20 MLS Co., Ltd. (Forest Lighting)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

晶片级封装LED市场:依LED类型、应用和最终用途划分-2026-2032年全球市场预测LED构装市场:依封装类型、基板材料、晶片类型和应用划分-全球预测,2026-2032年LED导线架市场按产品、材质、电镀类型、导线架类型和最终用户划分 - 全球预测 2026-2032

晶片级封装LED市场:依LED类型、应用和最终用途划分-2026-2032年全球市场预测LED构装市场:依封装类型、基板材料、晶片类型和应用划分-全球预测,2026-2032年LED导线架市场按产品、材质、电镀类型、导线架类型和最终用户划分 - 全球预测 2026-2032 LED构装市场规模、份额及成长分析(按应用、技术、最终用途及地区划分)-2026-2033年产业预测

LED构装市场规模、份额及成长分析(按应用、技术、最终用途及地区划分)-2026-2033年产业预测 晶片级封装LED市场-全球产业规模、份额、趋势、机会和预测,按应用、功率范围、地区和竞争格局划分,2020-2030年预测

晶片级封装LED市场-全球产业规模、份额、趋势、机会和预测,按应用、功率范围、地区和竞争格局划分,2020-2030年预测 晶片级封装LED(CSP LED)-全球市场份额和排名、总收入和需求预测(2025-2031年)

晶片级封装LED(CSP LED)-全球市场份额和排名、总收入和需求预测(2025-2031年) 亚太地区LED构装:市场占有率分析、产业趋势、成长预测(2025-2030 年)北美LED构装:市场占有率分析、产业趋势、成长预测(2025-2030 年)拉丁美洲LED构装:市场占有率分析、产业趋势、成长预测(2025-2030 年)欧洲LED构装:市场占有率分析、产业趋势、成长预测(2025-2030 年)

亚太地区LED构装:市场占有率分析、产业趋势、成长预测(2025-2030 年)北美LED构装:市场占有率分析、产业趋势、成长预测(2025-2030 年)拉丁美洲LED构装:市场占有率分析、产业趋势、成长预测(2025-2030 年)欧洲LED构装:市场占有率分析、产业趋势、成长预测(2025-2030 年)