|

市场调查报告书

商品编码

1906279

印尼施工机械市场:市场占有率分析、产业趋势、统计数据和成长预测(2026-2031年)Indonesia Construction Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

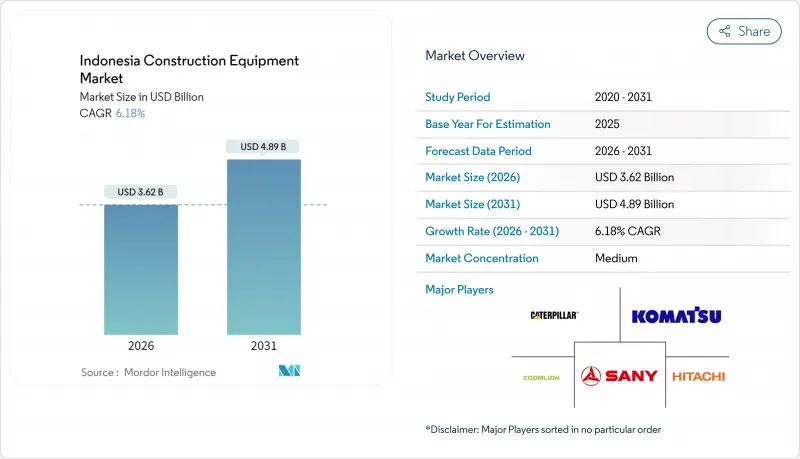

2025年印尼施工机械市场价值为34.1亿美元,预计从2026年的36.2亿美元成长到2031年的48.9亿美元,在预测期(2026-2031年)内复合年增长率为6.18%。

国家战略计划(PSN)的持续推进、350亿美元的新首都(IKN)计划以及强劲的矿业投资,都支撑着土木机械、物料输送和专用机械等各类设备的需求。能够提供本地组装、灵活资金筹措和远端资讯处理服务的供应商,最有利于最大限度地运转率以雅加达为中心的庞大车队。

印尼施工机械市场趋势与洞察

印尼2030年基础建设计画公共部门支出激增

印尼41个已进入最后阶段的PSN工程要求在收费公路、水坝、港口和工业园区等地不间断地部署设备。每投入印尼币用于基础建设,就能产生1.9印尼币的经济价值,进而增加承包商和租赁公司的采购预算。这种乘数效应在经济特区和电力计划中最为显着,推动了需求高峰从传统的爪哇岛集中型转变为全国性。北苏门答腊和南苏拉威西的生产成长最为显着,使这两个省份成为区域租赁需求中心。计划的长期性使得供应商能够制定长达五至七年的维护合同,从而确保在设备的整个生命週期内获得零件和业务收益。

城市铁路和收费公路的快速发展促进了土木工程车辆的更新换代。

计画于2024年完工的芝芒吉斯-芝比通收费公路象征高强度的土木工程建设,施工高峰期将部署大量挖土机和自动卸货卡车。卡朗若安-卡良高3A段的数位化现场监控显着减少了设备停机时间,提高了设备运转率,凸显了远端资讯处理整合的重要性日益凸显。采用精准导航系统的建设公司在燃油效率和施工速度方面均取得了显着提升。目前,北苏门答腊省帕拉帕特等基础设施走廊的省级政府正在推广这些倡议,表明技术主导的升级改造正在爪哇岛以外的地区普及。随着更严格的排放气体法规对老旧的二级排放标准设备提出了更高的要求,建设公司正在加速向更清洁、运作强度更低的三级排放标准和混合动力设备转型。

印尼币汇率波动推高进口设备价格和资金筹措成本。

资本财进口在印尼贸易结构中占比很大,这使得建筑公司极易受到外汇波动的影响,汇率波动可能在几週内导致采购预算减少0.25%。信用证可以提供成本缓衝,但在地采购要求使得选择全球品牌的规格变得复杂。 8/2024号贸易条例简化了港口清关流程,但汇率风险仍存在,迫使设备贷款机构收紧对中小企业的贷款价值比(LTV)。经销商越来越多地将以美元计价的零件合约与以印尼币计价的机械贷款捆绑在一起,虽然减少了错配,但也增加了文件负担。在巴淡岛和芝卡朗进行本地组装有助于降低风险,但Tier 4F引擎的进口价格仍以美元计价。

细分市场分析

2025年,印尼施工机械市场中土木机械的销售额将超过10亿美元,占市场份额的48.12%,这主要得益于公共网路服务(PSN)和矿业基础建设的蓬勃发展。平地平土机、履带挖土机和铰接式自动卸货卡车是收费公路和水坝建设计划的核心设备,而混凝土搅拌站和破碎设备则为大规模EPC(工程、采购和施工)计划提供配套支援。先进的远端资讯处理技术能够追踪怠速油耗和底盘磨损情况,促使承包商在排放法规生效前更换老旧的Tier 2车型。

受仓库自动化和港口现代化的推动,物料输送设备市场正以7.32%的复合年增长率成长,并占据了较大的市场份额。锂离子电池驱动的堆高机无需更换电池即可实现三班倒作业,从而减少了25%的停机时间。丹戎不碌港的遥控岸桥提高了泊位作业效率,并促使丹戎霹雳港和吉京港追加订单。

到2025年,液压平台将占销售额的84.55%,这主要得益于其成本绩效优势以及印尼业者的亲和性。供应商改进了滑阀调校和能源回收迴路,在不改变作业习惯的情况下,降低了8%的燃油消费量。远端钻探计划优先考虑液压系统的可靠性而非电气系统的复杂性,从而维持了半径超过100公里矿场的液压设备更换需求。

目前,电动和混合动力车的租赁量仅为4,200辆,但其复合年增长率(CAGR)却达到了6.45%,这主要得益于排碳权激励措施以及在地采购电动车可享10%的增值税折扣。一项针对20吨挖土机的试点改造表明,每立方米土方的营运成本降低了30个基点。使用混合动力机械的承包商在符合碳捕获与封存/碳捕获、利用与封存(CCS/CCUS)法规的公共竞标中往往能获得优先评估。资金筹措方案中包含绿色标籤的资产支持证券,与传统融资相比,其票储存差较小。这将鼓励从2027年起,混合动力机械在主流竞标中得到更广泛的应用。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 印尼2030年基础建设计画公共部门支出激增

- 城市铁路和收费公路的快速发展促进了土木工程车辆的更新换代。

- 电子商务仓储的蓬勃发展推动了对物料输送设备的需求。

- 大宗商品超级週期提振加里曼丹矿业领域的资本投资

- 排碳权奖励鼓励建筑公司采用电动/混合动力汽车

- 泛东协供应链重返印尼,扩大建设项目规模

- 市场限制

- 印尼币汇率波动导致进口设备价格上涨和资金筹措成本增加。

- 由于土地征用程序繁琐,计划延期

- 分散的租赁生态系统限制了全国范围内的车队可用性。

- 高级机器控制操作方面持续存在的技能差距

- 价值/供应链分析

- 技术展望

- 监管环境

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模和成长预测(价值和数量)

- 透过装置

- 土木工程施工机械

- 挖土机

- 后铲式装载机

- 平土机机

- 推土机

- 道路施工机械

- 压路机

- 沥青铺筑机

- 物料输送设备

- 起重机

- 堆高机和伸缩臂堆高机

- 曲臂式升降机

- 其他施工机械

- 土木工程施工机械

- 按驱动类型

- 油压

- 电动/混合动力

- 按输出功率(千瓦)

- 小于100千瓦

- 101~200 kW

- 201~400 kW

- 超过400千瓦

- 最终用户

- 基础设施和房地产建筑公司

- 采矿和采石公司

- 製造和工业设施

- 农业和人工林

- 透过使用

- 住宅

- 商业建筑

- 工业建筑

- 交通运输和基础设施计划

- 能源和公共产业计划

- 按地区

- Java

- 苏门答腊

- 加里曼丹

- 苏拉威西

- 巴布亚马鲁古群岛

- 印尼其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- JC Bamford Excavators Ltd.(JCB)

- HD Hyundai Construction Equipment

- SANY Heavy Industry Co., Ltd.

- Xuzhou Construction Machinery Group(XCMG)

- Zoomlion Heavy Industry Sci & Tech

- Liebherr Group

- Kubota Corporation

- Yanmar Co., Ltd.

- Takeuchi Mfg. Co., Ltd.

- Kobelco Construction Machinery

- Manitou Group

- Toyota Material Handling

- Volvo Construction Equipment

- Doosan Bobcat

- Sumitomo Construction Machinery

- CNH Industrial(CASE Construction)

- Shantui Construction Machinery Co., Ltd.

第七章 市场机会与未来展望

The Indonesia Construction Equipment Market was valued at USD 3.41 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 4.89 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031).

Continued implementation of the Proyek Strategis Nasional (PSN) pipeline, the USD 35 billion New Capital City (IKN) program, and resilient mining investment jointly anchors demand across earth-moving, material-handling, and specialized machinery categories. Suppliers that blend local assembly, flexible financing, and telematics services are best positioned to capitalize on utilization rates in Jakarta-centric fleets.

Indonesia Construction Equipment Market Trends and Insights

Surging Public-Sector Spend on Indonesia's 2030 Infrastructure Vision

Indonesia's 41 final-stage PSN schemes require uninterrupted equipment deployment across toll roads, dams, ports, and industrial parks. Every rupiah spent on infrastructure has generated 1.9 rupiah in economic value, reinforcing procurement budgets for contractors and rental houses. The multiplier appears strongest in economic zones and power projects, prompting nationwide demand peaks rather than the historical Java concentration. North Sumatra and South Sulawesi have posted the sharpest output lifts, turning each province into a regional rental hotspot. Longer project pipelines permit suppliers to structure five- to seven-year maintenance contracts, locking in parts and service revenue throughout machine life cycles.

Rapid Urban Rail & Toll-Road Build-Outs Driving Earth-Moving Fleet Renewal

Completed in 2024, the Cimanggis-Cibitung Toll Road exemplifies high earth-moving intensity, with significant deployment of excavators and dump trucks during peak construction. On-site digital monitoring at the Karangjoang-Kariangau Section 3A helped reduce equipment idle time significantly while improving utilization rates-highlighting the growing importance of telematics integration. Contractors adopting precision guidance systems are seeing notable gains in fuel efficiency and operational speed. These practices are now being extended by provincial authorities to infrastructure corridors like Parapat in North Sumatra, indicating that technology-driven upgrades are expanding beyond Java. With stricter emission norms tightening around aging Tier 2 equipment, contractors are increasingly turning to cleaner, low-hour Tier 3 and hybrid machines.

Volatile Rupiah Elevating Imported Equipment Prices & Financing Costs

Capital-goods imports form a significant share of Indonesia's trade basket, exposing contractors to foreign-exchange swings that erode purchasing budgets by quarter-points in weeks. Letters of credit add cost buffers, while local content mandates complicate specification choices for global brands. Trade Ministerial Regulation No. 8/2024 streamlines port clearance, yet currency risk persists, prompting equipment financiers to tighten loan-to-value ratios for smaller firms. Dealers increasingly bundle dollar-indexed parts contracts with rupiah-denominated machine loans, reducing mismatch but raising documentation overheads. Local assembly in Batam and Cikarang mitigates exposure, though Tier 4F engine imports remain priced in USD.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Warehousing Boom Lifting Demand for Material-Handling Equipment

- Commodity Super-Cycle Fueling Mining-Sector Capex in Kalimantan

- Project Execution Delays Tied to Land-Acquisition Bureaucracy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Earth-moving machinery generated more than a billion USD within the Indonesian construction equipment market in 2025, translating into a 48.12% share amid a surge of PSN and mining groundwork. Motor graders, crawler excavators, and articulated haulers form the backbone of toll-road and dam packages, while batching plants and crushing units round out larger EPC scopes. Advanced telematics now track idle fuel-burn and undercarriage wear, nudging contractors to upgrade older Tier 2 models ahead of emission mandates.

Material-handling equipment contributed significant share and is expanding at a 7.32% CAGR, propelled by warehouse automation and port modernization. Forklifts with lithium-ion packs enable triple-shift operations without battery swaps, cutting downtime by 25%. At Tanjung Priok, remote-operated quay cranes improve berth productivity, driving follow-on orders from Tanjung Perak and Kijing.

Hydraulic platforms captured 84.55% revenue in 2025, underpinned by cost-performance equilibrium and familiarity among Indonesian operators. Suppliers refine spool-valve tuning and energy-recovery circuits to cut fuel consumption by 8% without shifting working habits. Remote drilling projects value hydraulic robustness over electrical complexity, sustaining replacement demand in 100 km-plus radius mines.

Electric and hybrid variants, although only 4,200 units on rent today, post a 6.45% CAGR backed by carbon-credit incentives and 10% VAT discounts on locally contented EVs. Pilot retrofits on 20-tonne excavators show operating-cost drops of 30 basis points per cubic meter moved. Contractors adopting hybrids often secure preferential scoring in public tenders aligned with CCS/CCUS compliance. Financing bundles include green-label asset-backed securities, trimming coupon spreads versus conventional loans, and nudging adoption into mainstream bids for 2027 onward.

The Indonesia Construction Equipment Market Report is Segmented by Equipment Type (Earth-Moving Equipment, Road Construction Equipment, and More), Drive Type (Hydraulic and Electric/Hybrid), Power Output (Less Than 100 KW and More), End-User (Infrastructure & Real-Estate Contractors and More), Application (Residential Construction and More), and Region. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- J.C. Bamford Excavators Ltd. (JCB)

- HD Hyundai Construction Equipment

- SANY Heavy Industry Co., Ltd.

- Xuzhou Construction Machinery Group (XCMG)

- Zoomlion Heavy Industry Sci & Tech

- Liebherr Group

- Kubota Corporation

- Yanmar Co., Ltd.

- Takeuchi Mfg. Co., Ltd.

- Kobelco Construction Machinery

- Manitou Group

- Toyota Material Handling

- Volvo Construction Equipment

- Doosan Bobcat

- Sumitomo Construction Machinery

- CNH Industrial (CASE Construction)

- Shantui Construction Machinery Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Public-Sector Spend on Indonesia's 2030 Infrastructure Vision

- 4.2.2 Rapid Urban Rail & Toll-Road Build-Outs Driving Earth-Moving Fleet Renewal

- 4.2.3 E-Commerce Warehousing Boom Lifting Demand for Material-Handling Equipment

- 4.2.4 Commodity Super-Cycle Fueling Mining-Sector Capex in Kalimantan

- 4.2.5 Carbon-Credit Incentives Pushing Contractors Toward Electric/Hybrid Fleets

- 4.2.6 ASEAN-Wide Supply-Chain Re-Shoring into Indonesia Expanding Construction Pipelines

- 4.3 Market Restraints

- 4.3.1 Volatile Rupiah Elevating Imported Equipment Prices & Financing Costs

- 4.3.2 Project Execution Delays Tied to Land-Acquisition Bureaucracy

- 4.3.3 Fragmented Rental Ecosystem Limiting Nationwide Fleet Utilisation

- 4.3.4 Persistent Skills Gap in Advanced Machine-Control Operation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Equipment Type

- 5.1.1 Earth-moving Equipment

- 5.1.1.1 Excavators

- 5.1.1.2 Backhoe Loaders

- 5.1.1.3 Motor Graders

- 5.1.1.4 Bulldozers

- 5.1.2 Road Construction Equipment

- 5.1.2.1 Road Rollers

- 5.1.2.2 Asphalt Pavers

- 5.1.3 Material-Handling Equipment

- 5.1.3.1 Cranes

- 5.1.3.2 Forklifts & Telescopic Handlers

- 5.1.3.3 Articulated Boom Lifts

- 5.1.4 Other Construction Equipment

- 5.1.1 Earth-moving Equipment

- 5.2 By Drive Type

- 5.2.1 Hydraulic

- 5.2.2 Electric / Hybrid

- 5.3 By Power Output (kW)

- 5.3.1 Less than 100 kW

- 5.3.2 101 to 200 kW

- 5.3.3 201 to 400 kW

- 5.3.4 More than 400 kW

- 5.4 By End-user

- 5.4.1 Infrastructure & Real-estate Contractors

- 5.4.2 Mining & Quarrying Companies

- 5.4.3 Manufacturing & Industrial Facilities

- 5.4.4 Agriculture & Plantation Sector

- 5.5 By Application

- 5.5.1 Residential Construction

- 5.5.2 Commercial Construction

- 5.5.3 Industrial Construction

- 5.5.4 Transportation & Infrastructure Projects

- 5.5.5 Energy & Utilities Projects

- 5.6 By Region

- 5.6.1 Java

- 5.6.2 Sumatra

- 5.6.3 Kalimantan

- 5.6.4 Sulawesi

- 5.6.5 Papua & Maluku

- 5.6.6 Rest of Indonesia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Hitachi Construction Machinery Co., Ltd.

- 6.4.4 J.C. Bamford Excavators Ltd. (JCB)

- 6.4.5 HD Hyundai Construction Equipment

- 6.4.6 SANY Heavy Industry Co., Ltd.

- 6.4.7 Xuzhou Construction Machinery Group (XCMG)

- 6.4.8 Zoomlion Heavy Industry Sci & Tech

- 6.4.9 Liebherr Group

- 6.4.10 Kubota Corporation

- 6.4.11 Yanmar Co., Ltd.

- 6.4.12 Takeuchi Mfg. Co., Ltd.

- 6.4.13 Kobelco Construction Machinery

- 6.4.14 Manitou Group

- 6.4.15 Toyota Material Handling

- 6.4.16 Volvo Construction Equipment

- 6.4.17 Doosan Bobcat

- 6.4.18 Sumitomo Construction Machinery

- 6.4.19 CNH Industrial (CASE Construction)

- 6.4.20 Shantui Construction Machinery Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

东协施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中国施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国施工机械市场占有率分析、产业趋势及统计、成长预测(2026-2031)

东协施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)中国施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)施工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国施工机械市场占有率分析、产业趋势及统计、成长预测(2026-2031) 2026年全球建筑及道路施工机械市场报告2026年全球施工机械市场报告2026年全球液压搭乘用电梯市场报告

2026年全球建筑及道路施工机械市场报告2026年全球施工机械市场报告2026年全球液压搭乘用电梯市场报告 施工机械市场机会、成长要素、产业趋势分析及2026年至2035年预测

施工机械市场机会、成长要素、产业趋势分析及2026年至2035年预测 CPT履带市场按产品类型、分销管道、应用和最终用户划分 - 全球预测(2026-2032年)叶形抹刀市场:依产品类型、材料、价格范围、应用、最终用户和分销管道划分,全球预测,2026-2032年

CPT履带市场按产品类型、分销管道、应用和最终用户划分 - 全球预测(2026-2032年)叶形抹刀市场:依产品类型、材料、价格范围、应用、最终用户和分销管道划分,全球预测,2026-2032年