|

市场调查报告书

商品编码

1910463

中东和非洲电动车市场:份额分析、行业趋势、统计数据和成长预测(2026-2031 年)Middle East And Africa Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

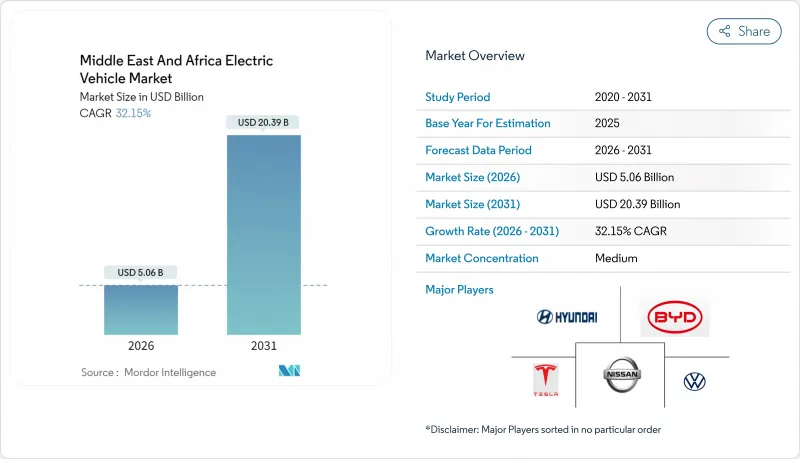

2025年中东和非洲电动车市场价值为38.3亿美元,预计从2026年的50.6亿美元成长到2031年的203.9亿美元,在预测期(2026-2031年)内复合年增长率为32.15%。

主权财富基金正向国内生产生态系统注入数十亿美元,石油出口国则利用其丰富的太阳能资源降低充电成本,吸引全球汽车製造商。具有约束力的脱碳义务、电池成本的下降以及公共快速充电走廊的建设正在推动需求成长,而二手内燃机汽车的进口则构成短期阻力。儘管乘用车仍然是最大的装机量,但随着油气业者启动大规模电气化竞标,商用车队正占据成长的大部分份额。主要能源公司与汽车製造商之间的策略合作,以及高温环境下电池温度控管技术的创新,正使该地区成为电动车在极端温度下性能的技术试验场。

中东及非洲电动车市场趋势及分析

政府的脱碳指令与内燃机禁令目标

波湾合作理事会(GCC)成员国已将电动车配额纳入国家发展议程,设定了汽车製造商(OEM)投资决策的最低需求标准。沙乌地阿拉伯的「2030愿景」要求到2030年,利雅德30%的车辆必须为电动车;而阿联酋的联邦战略则力争2050年实现50%的车辆为电动车。这些强制性规定引导公共部门购买转向零排放车型,鼓励私家车改装,统一海湾标准组织(GSO)的认证标准,并促进跨国贸易。从摩洛哥到2026年安装2500个充电桩的强制规定,显示强而有力的政策能够加速基础建设。具有法律约束力的目标与《巴黎协定》第二十八届联合国气候变迁大会(COP28)的承诺一致,并为投资者提供长期可见性,从而抵消初期需求波动的影响。

快速部署公共直流快速充电走廊

城际快速充电走廊将使电动车从短途都市区出行转变为跨区域出行。 EVIQ 在利雅得-卡西姆高速公路上建造的旗舰级 150kW 充电站证明了其在主要道路上的可行性,并预示着其将扩展到沙乌地阿拉伯王国十大最繁忙的高速公路。同时,阿联酋计划在 2030 年之前在阿布达比安装 7 万个公共充电桩,杜拜的目标是到 2025 年安装 1000 个,从而有效消除酋长国内的里程焦虑。摩洛哥计划连接卡萨布兰卡、拉巴特和丹吉尔,届时将使用可再生能源运作充电桩,实现 30 分钟以内的快速充电。奈及利亚将于 2025 年运作西非最大的充电中心之一,将基础设施覆盖范围扩展到新兴市场。沿线充电密度的增加将大幅提高商用车辆的运作,并鼓励杰贝阿里港等港口的货运营运商实现电气化。

高昂的车辆前期成本和有限的消费者融资

儘管电池价格下降,但高昂的购车成本阻碍了低收入群体对电动车的大规模普及。在埃及,由于分期付款计划有限以及外汇支出有外汇风险,电动车仅占新车销量的0.1%。习惯为二手进口车辆提供证券化服务的传统金融机构缺乏电动车贷款的残值基准,导致利率利差较大。在二手以南非洲,小额信贷机构的目标客户是两轮计程车而非四轮汽车,这进一步阻碍了汽车製造商实现规模经济。

细分市场分析

截至2025年,电池式电动车(BEV)占据了电动车市场78.64%的份额。这印证了该地区对纯电动驱动系统的偏好,并避免了与插电式混合动力汽车燃油税相关的复杂性。纯电动车的吸引力在于其易于维护,以及购物中心、机场、工业园区等场所目的地充电桩的日益普及。该细分市场强劲的利润结构吸引了特斯拉、比亚迪和吉利等製造商推出绕过传统经销商网路的直销平台。

车队营运商正采用夜间在停车场充电的方式,以减少白天营运中断的影响。随着沙乌地阿拉伯在工业走廊週边扩建绿色氢气加氢站,燃料电池电动车(FCEV)预计到2031年将以35.90%的复合年增长率成长,凸显了其在长程运输领域的潜力。同时,插混合动力汽车仍是一种过渡性选择,可在电网可靠性较低的地区提供续航里程保障。因此,动力系统构成比反映了基础设施的成熟度,纯电动车(BEV)在海湾地区的都市区沿岸地区占据主导地位,而燃料电池汽车则在沙漠货运路线上崭露头角。

2025年,乘用车收入占比达到64.05%,而中重型商用车预计到2031年将以35.05%的复合年增长率加速成长,从而扩大企业采购通路的电动车市场规模。油田服务卡车和末端配送货车由于每日行驶里程长,可大幅节省燃油成本并带来碳审核效益。吉达自由贸易区的物流公司目前在竞标中指定使用电动车型,以符合港务局的排放法规。开罗和开普敦的公车电动化试点计画显示公共交通需求不断增长,而叫车服务供应商正在引入小型掀背车电动车,以符合城市地区的清洁空气法规。原始设备製造商(OEM)正在透过客製化区域有效负载容量规格、增强型车厢空调系统和强化型越野悬吊来应对这一需求。随着商用车销量的成长,供应链在地化程度不断加深,卡车车身、电池机壳和远端资讯处理服务等均可在国内采购。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府的脱碳指令和禁止内燃机汽车的目标

- 进口电动车的补贴和免税措施(海湾合作委员会国家)

- 快速部署公共直流快速充电走廊

- 电池组价格下降和续航里程延长

- 石油和天然气车队电气化承诺推动大订单

- 利用白天多余的太阳能,实现超低成本充电费用

- 市场限制

- 车辆初始成本高,且消费者融资管道有限。

- 原始设备製造商限制高温车型的供应

- 不稳定的电网限制了充电器的运作时间(撒哈拉以南地区)

- 廉价二手内燃机汽车进口量的增加损害了电动车的需求。

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

5. 市场规模及成长预测(价值,百万美元)

- 按驱动类型

- 电池式电动车(BEV)

- 插电式混合动力汽车(PHEV)

- 燃料电池电动车(FCEV)

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和重型商用车辆

- 公车和长途客车

- 两轮车和三轮车

- 电池化学

- 锂离子电池(NMC/NCA/LFP)

- 镍氢电池

- 其他的

- 按电荷等级

- 交流充电功率低于 7kW(速度慢)

- 7kW 至 22kW 交流充电(半快充)

- 直流22千瓦或以上(高速/超高速)

- 按国家/地区

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 以色列

- 埃及

- 南非

- 奈及利亚

- 肯亚

- 卡达

- 阿曼

- 其他中东和非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Tesla Inc.

- BYD Co. Ltd.

- Hyundai Motor Co.

- Kia Corp.

- Volkswagen AG

- Nissan Motor Co. Ltd.

- BMW Group

- Toyota Motor Corp.

- Stellantis NV

- Mercedes-Benz Group AG

- Renault Group

- Jaguar Land Rover Ltd.

- Zhejiang Geely Holding

- Lucid Group

- Ceer Motors

- Togg AS

- General Motors Co.

- SAIC-MG Motor

- Ford Motor Co.

- Rivian Automotive Inc.

第七章 市场机会与未来展望

The electric vehicle market in the Middle East and Africa was valued at USD 3.83 billion in 2025 and estimated to grow from USD 5.06 billion in 2026 to reach USD 20.39 billion by 2031, at a CAGR of 32.15% during the forecast period (2026-2031).

Sovereign wealth funds are directing multibillion-dollar allocations toward domestic production ecosystems, and oil-exporting nations are leveraging abundant solar resources to lower charging costs and attract global original-equipment manufacturers (OEMs). Binding decarbonization mandates, falling battery costs, and the rollout of public fast-charging corridors reinforce demand momentum even as used internal-combustion-engine (ICE) imports remain a short-term headwind. Passenger cars retain the most extensive installed base, yet commercial fleets increasingly dominate incremental volume as oil-and-gas operators issue bulk electrification tenders. Strategic partnerships between energy majors and automakers and hot-climate battery-thermal innovations are positioning the region as a technical test bed for extreme-heat EV performance.

Middle East And Africa Electric Vehicle Market Trends and Insights

Government Decarbonization Mandates and ICE-Ban Targets

Gulf Cooperation Council (GCC) members have embedded electric-mobility quotas into national development agendas, creating demand floors that anchor OEM investment decisions. Saudi Arabia's Vision 2030 compels 30% of Riyadh's vehicles to be electric by 2030, while the UAE's federal strategy targets a 50% electric-vehicle mix by 2050. These directives funnel public-sector procurement toward zero-emission models, catalyze private-sector fleet conversions, and standardize certification under Gulf Standardization Organization (GSO) rules, which ease cross-border trade. Morocco's mandates 2,500 charging points by 2026, illustrating how firm policy anchors accelerate infrastructure scale-up. Binding targets dovetail with COP28 commitments, giving investors long-cycle visibility, compensating for initial demand volatility.

Rapid Rollout of Public DC Fast-Charging Corridors

Intercity fast-charging corridors convert EVs from urban runabouts into region-wide mobility options. EVIQ's flagship 150 kW site on the Riyadh-Qassim motorway demonstrates highway viability and signals forthcoming coverage of the kingdom's 10 busiest arterial routes. In parallel, the UAE plans 70,000 public chargers across Abu Dhabi by 2030, while Dubai targets 1,000 sites by 2025, effectively eliminating intra-emirate range anxiety. Morocco's plan links Casablanca, Rabat, and Tangier with green-energy-powered DC units that supply sub-30-minute stops. Nigeria's 2025 inauguration of West Africa's largest assembled charging hub widens the infrastructure map to frontier markets. Corridor density materially lifts commercial-vehicle uptime, unlocking electrification for freight operators serving ports such as Jebel Ali.

High Upfront Vehicle Price and Limited Consumer Financing

Purchase-price premiums continue to deter mass-market adoption in lower-income segments even as batteries cheapen. Egypt's EV share remains just 0.1% of new-car sales due to limited installment plans and hard-currency outlays that expose buyers to exchange-rate swings. Traditional lenders, accustomed to securitizing used imports, lack residual-value benchmarks for electric vehicle market loans, inflating interest spreads. In Sub-Saharan Africa, microfinance mechanisms target two-wheeler taxis rather than four-wheeler purchases, further stalling scale economics for OEMs.

Other drivers and restraints analyzed in the detailed report include:

- Day-Time Solar-PV Surplus Driving Ultra-Low-Cost Charging Tariffs

- Oil-and-Gas Fleet-Electrification Pledges Unlocking Bulk Orders

- Influx of Cheap Used ICE Imports Undermines EV Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery-electric vehicles (BEVs) commanded 78.64% of the electric vehicle market share in 2025, validating the region's preference for fully electric drivetrains and sidestepping the fuel-duty complexity of plug-in hybrids. BEV appeal stems from simpler maintenance and the rollout of destination chargers at malls, airports, and industrial parks. The segment's robust margin structure has enticed Tesla, BYD, and Geely to launch direct-to-consumer sales portals that bypass traditional dealerships.

Fleet operators adopt BEVs for depot-night charging, reducing daytime operational disruptions. Fuel-cell electric vehicles post a 35.90% CAGR through 2031 as Saudi Arabia scales green-hydrogen refueling nodes around its industrial corridors, underscoring their long-haul potential. Meanwhile, plug-in hybrids remain transitional, offering range security where grid reliability lags. The drive-type mix therefore mirrors infrastructure maturity, with BEVs prevailing in the urban Gulf and fuel-cells rising along desert freight links.

Passenger cars controlled 64.05% of 2025 revenue, yet medium and heavy commercial vehicles are forecast to outpace with a 35.05% CAGR to 2031, expanding the electric vehicle market size in corporate procurement channels. Oil-field service trucks and last-mile delivery vans accrue higher daily mileage, magnifying fuel savings and carbon audit benefits. Logistics firms in the Jeddah free zone now specify electric models in tenders to comply with port authority emissions limits. Bus electrification pilots in Cairo and Cape Town indicate growing public-transport appetite, while ride-hailing operators deploy small hatchback EVs to meet city-center clean-air mandates. OEMs are responding with region-tuned payload ratings, enhanced cabin HVAC, and reinforced suspensions for unpaved routes. As commercial volumes climb, supply-chain localization deepens because truck bodies, battery enclosures, and telematics services can all be sourced domestically.

The Middle East and Africa Electric Vehicle Market Report is Segmented by Drive Type (Battery-Electric, Plug-In Hybrid, and Fuel-Cell Electric), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Battery Chemistry (Lithium-Ion, Nickel-Metal Hydride, and Others), Charging Level (AC Below 7 KW, and More), and by Country. Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Tesla Inc.

- BYD Co. Ltd.

- Hyundai Motor Co.

- Kia Corp.

- Volkswagen AG

- Nissan Motor Co. Ltd.

- BMW Group

- Toyota Motor Corp.

- Stellantis N.V.

- Mercedes-Benz Group AG

- Renault Group

- Jaguar Land Rover Ltd.

- Zhejiang Geely Holding

- Lucid Group

- Ceer Motors

- Togg A.S.

- General Motors Co.

- SAIC-MG Motor

- Ford Motor Co.

- Rivian Automotive Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Decarbonizations Mandates and ICE-Ban Targets

- 4.2.2 Subsidies And Zero-Customs Duties on EV Imports (GCC)

- 4.2.3 Rapid Rollout of Public DC Fast-Charging Corridors

- 4.2.4 Declining Battery Pack Prices and Longer Driving Range

- 4.2.5 Oil-and-Gas Fleet Electrification Pledges Unlocking Bulk Orders

- 4.2.6 Day-Time Solar-PV Surplus Driving Ultra-Low-Cost Charging Tariffs

- 4.3 Market Restraints

- 4.3.1 High Upfront Vehicle Price and Limited Consumer Financing

- 4.3.2 Restricted Hot-Climate Model Availability From OEMs

- 4.3.3 Grid Unreliability Curbing Charger Uptime (Sub-Saharan Sites)

- 4.3.4 Influx of Cheap Used ICE Imports Undermines EV Demand

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Million)

- 5.1 By Drive Type

- 5.1.1 Battery-Electric (BEV)

- 5.1.2 Plug-in Hybrid (PHEV)

- 5.1.3 Fuel-Cell Electric (FCEV)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Buses and Coaches

- 5.2.5 Two and Three Wheelers

- 5.3 By Battery Chemistry

- 5.3.1 Lithium-ion (NMC / NCA / LFP)

- 5.3.2 Nickel-Metal Hydride

- 5.3.3 Others

- 5.4 By Charging Level

- 5.4.1 AC below 7 kW (Slow)

- 5.4.2 AC above 7 kW - 22 kW (Semi-fast)

- 5.4.3 DC above 22 kW (Fast / Ultra-fast)

- 5.5 By Country

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Israel

- 5.5.4 Egypt

- 5.5.5 South Africa

- 5.5.6 Nigeria

- 5.5.7 Kenya

- 5.5.8 Qatar

- 5.5.9 Oman

- 5.5.10 Rest of Middle East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Tesla Inc.

- 6.4.2 BYD Co. Ltd.

- 6.4.3 Hyundai Motor Co.

- 6.4.4 Kia Corp.

- 6.4.5 Volkswagen AG

- 6.4.6 Nissan Motor Co. Ltd.

- 6.4.7 BMW Group

- 6.4.8 Toyota Motor Corp.

- 6.4.9 Stellantis N.V.

- 6.4.10 Mercedes-Benz Group AG

- 6.4.11 Renault Group

- 6.4.12 Jaguar Land Rover Ltd.

- 6.4.13 Zhejiang Geely Holding

- 6.4.14 Lucid Group

- 6.4.15 Ceer Motors

- 6.4.16 Togg A.S.

- 6.4.17 General Motors Co.

- 6.4.18 SAIC-MG Motor

- 6.4.19 Ford Motor Co.

- 6.4.20 Rivian Automotive Inc.

7 Market Opportunities & Future Outlook

高性能电动车市场:按车辆类型、电池容量、动力传动系统和最终用户划分-2026-2032年全球市场预测小型电动车市场:按车辆类型、动力系统、电池容量、最终用户和销售管道划分-2026-2032年全球市场预测电动车市场:2026-2032年全球市场预测(按车辆类型、驱动系统、零件、电池技术、电池容量、续航里程、最终用户和销售管道)

高性能电动车市场:按车辆类型、电池容量、动力传动系统和最终用户划分-2026-2032年全球市场预测小型电动车市场:按车辆类型、动力系统、电池容量、最终用户和销售管道划分-2026-2032年全球市场预测电动车市场:2026-2032年全球市场预测(按车辆类型、驱动系统、零件、电池技术、电池容量、续航里程、最终用户和销售管道) 电动车市场规模、份额、趋势和预测:按组件、充电方式、驱动系统、车辆类型和地区划分,2026-2034 年

电动车市场规模、份额、趋势和预测:按组件、充电方式、驱动系统、车辆类型和地区划分,2026-2034 年 电动车市场(至2035年):产业趋势与全球预测

电动车市场(至2035年):产业趋势与全球预测 2026年全球小型电动车市场报告2026年全球搭乘用电动车市场报告2026年全球电动车市场报告2026年全球电动车虚拟原型製作市场报告

2026年全球小型电动车市场报告2026年全球搭乘用电动车市场报告2026年全球电动车市场报告2026年全球电动车虚拟原型製作市场报告 800V电动车架构市场:策略洞察与预测(2026-2031年)

800V电动车架构市场:策略洞察与预测(2026-2031年)