|

市场调查报告书

商品编码

1910699

印度低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)India Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

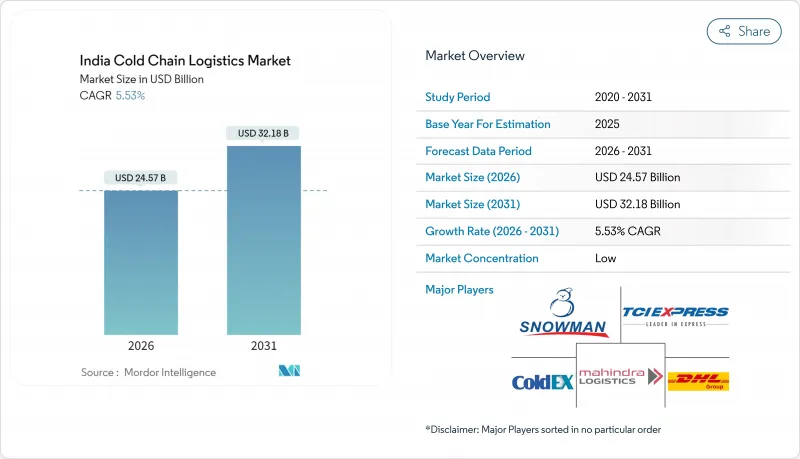

据估计,印度低温运输物流市场规模从2025年的232.8亿美元成长到2026年的245.7亿美元,预计到2031年将达到321.8亿美元,2026年至2031年的复合年增长率为5.53%。

蓬勃发展的都市区餐饮服务业、仓储公共补贴以及生物製药医药产品线的共同推动,印度物流业正从传统的分散式散装仓储模式向一体化、端到端的温控解决方案发生决定性转变。印度冷冻行动计画旨在推广节能资产,而国家物流政策则致力于提高物流业占GDP的比重,以反映效率的提升,鼓励营运商升级车队并采用基于人工智慧的路线规划。液化天然气高速公路、生鲜电商配送中心以及基于电子车辆识别码(eVIN)的疫苗监测系统,都进一步强化了对可靠的超低温配送的需求。同时,高效能压缩机的进口关税壁垒以及冷冻车司机长期短缺,限制了短期发展势头,同时也提高了市场准入门槛,有利于具有规模优势的一体化运营商。私人企业对太阳能混合动力仓库和绿色能源冷冻车的投资,进一步凸显了那些寻求碳中和成长路径的企业之间的差异化优势。

印度低温运输物流市场趋势与洞察

国家天然气管网的扩建将使冷藏液化天然气卡车运输成为可能。

预计2030年,全国天然气管道渗透率将达70%。这将促成1,000座液化天然气(LNG)加气站的建设,使冷藏车与柴油相比,燃料成本降低约20%,长途运输的二氧化碳排放减少约25%。古吉拉突邦和拉贾斯坦邦已在其高出口量路线上建造了LNG走廊,马哈拉施特拉邦的葡萄和洋葱出口商也受益于运输过程中更稳定的温度控制。马哈拉斯特拉邦石油公司计划在2025年建成50座LNG零售站,将缩短加气间隔,并加速冷冻车改造计画的实施。更清洁的燃烧带来的更低维护成本将使车队所有者的生命週期成本降低30-40%,进一步推动印度低温运输物流市场对LNG的采用。

政府补贴的大型冷藏仓库项目

在「总理农民财富计画」(PM Kisan Sampada Yojana)下,394个已获批准的计划旨在透过标准化枢纽建设,将果蔬采后损失减少25%至30%。国家低温运输发展中心提供工程模板,以协调包装厂和运输规范,从而提高印度低温运输物流市场的互通性。补贴将弥补小规模农业邦的资金缺口,但当地电网的可靠性和操作人员培训对于专案实施至关重要,目前正在推广公私合营,以维修太阳能备用电源装置。

地方城市电网不稳定

大城市以外的冷库经常遭遇停电,导致依赖柴油发电机,会使能源成本增加18%至22%,增加温度波动的风险,进而降低生鲜食品的价值。虽然阿萨姆邦的一个太阳能原型机可以将温度维持在摄氏4至10度之间长达30小时,但高昂的前期成本阻碍了小规模生产商采用该技术。长期电网现代化对于农村低温运输的永续性仍然至关重要。

细分市场分析

至2025年,冷藏将占印度低温运输物流市场40.62%的份额。这主要归因于以往对农产品散装商品的投资分散,以及「总理农民收入补贴计画」(PM Kisan Sampada)仍可用于扩大产能。虽然目前80%的冷藏运输路线为道路运输运输,但专用货运走廊(DFC)的建设有望推动运输方式的转变并缩短停留时间。从条码贴标到套件组装附加价值服务预计将推动市场在2031年前以5.22%的复合年增长率成长,因为全通路零售商正在寻求一站式解决方案。像Snowman 物流这样的营运商正在建立多客户冷库,并配备用于品质保证审核和托盘重新包装的整合工作台,从而提高交叉转运的处理速度。

对综合服务日益增长的需求也促使公共一体化仓储模式的出现。透过将资本投资与第三方物流管理合约分离,这种模式使中小型生产者无需前期投资即可使用更完善的设施。印度货柜公司(CONCOR)的铁路专用冷藏货柜抵达东部的渔业枢纽,减少了产品新鲜度的劣化,并扩大了印度海运出口的低温运输物流市场。虽然空运走廊是一个小众市场,货运量占不到2%,但它对于将高价值生技药品运往欧洲和北美仍然至关重要。随着零售商将仓库管理系统(WMS)平台直接连接到仓库温度记录,服务供应商正在利用数据分析仪表板来优化库存週转并减少能源高峰,从而实现盈利。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 都市化带动餐饮业快速发展

- 政府补贴的大型冷藏仓库项目

- 拓展生物製剂及疫苗研发管线

- 最后一公里冷藏生鲜电商配送的需求

- 引入人工智慧优化路线和载重规划

- 以绿色能源为基础的冷藏车队

- 市场限制

- 二、三线城市电网不稳定

- 小规模仓库所有权分散化

- 冷藏车驾驶人短缺

- 对高效率压缩机征收高额进口关税

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按服务类型

- 冷藏保管

- 公共仓库

- 私人仓库

- 冷藏运输

- 道路运输

- 铁路

- 海上运输

- 航空邮件

- 附加价值服务

- 冷藏保管

- 按温度类型

- 冷藏(0-5°C)

- 冷冻(-18 至 0°C)

- 环境的

- 超低温冷冻(低于-20°C)

- 透过使用

- 水果和蔬菜

- 肉类/家禽

- 鱼贝类

- 乳製品和冷冻甜点

- 麵包糖果甜点

- 速食食品

- 药品和生物製药

- 疫苗和临床试验材料

- 化学品/特殊材料

- 其他生鲜产品

- 按地区

- 印度北部

- 新德里(NCR)

- 旁遮普邦

- 哈里亚纳邦

- 其他的

- 南印度

- 卡纳塔克邦

- 泰米尔纳德邦

- 特伦甘纳邦

- 其他的

- 西印度群岛

- 马哈拉斯特拉邦

- 古吉拉突邦

- 其他的

- 东印度

- 西孟加拉邦

- 奥里萨邦

- 其他的

- 印度中部

- 中央邦

- 恰蒂斯加尔邦

- 印度北部

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Snowman Logistics Ltd

- ColdEx Logistics Pvt Ltd

- TCI Express Ltd

- DHL Supply Chain India

- Mahindra Logistics Ltd

- Gubba Cold Storage Ltd

- Cold Star Logistics Pvt Ltd

- CONCOR Cold Chain Logistics

- Crystal Logistics Cool Chain Ltd

- RK Foodland Pvt Ltd

- Indraprastha Cold Storage

- Arihant Cold Storage

- Godamwale

- Siddhi Cold Chain

- Coldrush Logistics

- Coldman Warehousing & Distribution

- Indicold Private Limited

- GK Cold Chain Solutions

- Transworld

- CEVA Logistics(Stellar Value Chain Solutions Pvt Ltd)

第七章 市场机会与未来展望

The India Cold Chain Logistics Market size in 2026 is estimated at USD 24.57 billion, growing from 2025 value of USD 23.28 billion with 2031 projections showing USD 32.18 billion, growing at 5.53% CAGR over 2026-2031.

Rapid urban food-service growth, public subsidies for warehousing, and biologics-heavy pharma pipelines collectively steer a decisive move from isolated bulk storage toward integrated end-to-end temperature-controlled solutions. The India Cooling Action Plan promotes energy-efficient assets, while the National Logistics Policy targets a logistics-to-GDP ratio that signifies enhanced efficiency, encouraging operators to upgrade fleets and adopt AI-based routing. LNG-ready highways, e-grocery fulfillment hubs, and eVIN-enabled vaccine monitoring strengthen demand for reliable sub-zero distribution. Meanwhile, import duty barriers on high-efficiency compressors and a chronic reefer-driver shortfall temper near-term momentum but also raise entry thresholds that favor integrated operators with scale advantages. Private investments in solar-hybrid depots and green-energy reefer fleets further differentiate players seeking carbon-aligned growth trajectories.

India Cold Chain Logistics Market Trends and Insights

Expansion of National Gas Grid Enabling LNG-Fuelled Reefer Trucking

Nationwide pipeline roll-outs are slated to lift natural-gas coverage to 70% by 2030, underpinning 1,000 LNG fueling points that offer refrigerated fleets fuel cost savings near 20% against diesel and carbon cuts near 25% for long hauls. Gujarat and Rajasthan already deploy LNG corridors on export-heavy routes, while Maharashtra's grape and onion exporters gain from steadier line-haul temperatures. Indian Oil's target of 50 LNG retail sites by 2025 shortens refueling gaps and accelerates reefer conversion programs. Lower maintenance expenses from cleaner combustion add 30-40% life-cycle savings for fleet owners, supplying further tailwinds to the India cold chain logistics market adoption curves.

Government-Subsidized Bulk-Cold-Storage Schemes

Under the PM Kisan Sampada Yojana, 394 sanctioned projects aim to curb the 25-30% post-harvest losses in fruit and vegetables by building standardized hubs. The National Centre for Cold-chain Development provides engineering templates that unify pack-house and transport specs, improving interoperability across the India cold chain logistics market. Subsidies close funding gaps in smaller agri-states, but execution rests on local grid reliability and operator training, prompting public-private tie-ups for solar-backup retrofits.

Power-Grid Instability in Tier-2/3 Cities

Cold stores outside metro hubs confront frequent outages that trigger diesel genset reliance, lifting energy spends by 18-22% and risking temperature excursions that jeopardize perishable value. Solar-powered prototypes in Assam sustain 4-10 °C for 30 hours, but upfront costs deter adoption among smallholders. Long-term grid modernization remains pivotal to rural cold chain viability.

Other drivers and restraints analyzed in the detailed report include:

- Pharma Biologics & Vaccine Pipeline Expansion

- E-Grocery Last-mile Refrigerated Demand

- Fragmented Ownership of Small Warehouses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated storage retains 40.62% India cold chain logistics market share in 2025, owing to historically siloed investments in bulk agri commodities, and it still attracts PM Kisan Sampada grants for capacity additions. Road haulage underpins 80% of refrigerated transportation lanes, but Dedicated Freight Corridors promise modal shifts that can curb dwell times. Value-added services, from barcoded labeling to kitting, are forecast to outperform at a 5.22% CAGR through 2031 as omnichannel retailers seek single-window solutions. Operators such as Snowman Logistics now position multi-client chambers adjacent to integration desks that handle QA audits and pallet reconsolidation, bolstering cross-dock velocity.

Demand for comprehensive offerings also sparks hybrid public-private depot models that split shell investment from 3PL management contracts, letting smaller farmers tap upgraded facilities without upfront capital. Rail-enabled reefer containers by CONCOR reach eastern fishery hubs, shrinking spoilage and expanding the reach of the India cold chain logistics market size for marine exports. Air-cargo corridors stay niche, accounting for less than 2% of volumes, yet remain indispensable for high-value biologics dispatches to Europe and North America. As retailers link WMS platforms directly to warehouse temperature logs, service providers monetize data analytics dashboards that optimize SKU rotation and cut energy peaks.

The India Cold Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, and Value-Added Services), Temperature Type (Chilled, Frozen, Ambient, and Deep-Frozen/Ultra-Low), Application (Fruits & Vegetables, Meat & Poultry, Fish & Seafood, Dairy & Frozen Desserts, and More), Region (North India, South India, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Snowman Logistics Ltd

- ColdEx Logistics Pvt Ltd

- TCI Express Ltd

- DHL Supply Chain India

- Mahindra Logistics Ltd

- Gubba Cold Storage Ltd

- Cold Star Logistics Pvt Ltd

- CONCOR Cold Chain Logistics

- Crystal Logistics Cool Chain Ltd

- R. K. Foodland Pvt Ltd

- Indraprastha Cold Storage

- Arihant Cold Storage

- Godamwale

- Siddhi Cold Chain

- Coldrush Logistics

- Coldman Warehousing & Distribution

- Indicold Private Limited

- GK Cold Chain Solutions

- Transworld

- CEVA Logistics (Stellar Value Chain Solutions Pvt Ltd)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanisation-linked Food-service Boom

- 4.2.2 Government-subsidised Bulk-Cold-Storage Schemes

- 4.2.3 Pharma Biologics & Vaccine Pipeline Expansion

- 4.2.4 E-grocery Last-mile Refrigerated Demand

- 4.2.5 AI-optimised Route & Load Planning Adoption

- 4.2.6 Green-Energy-Based Reefer Fleets

- 4.3 Market Restraints

- 4.3.1 Power-grid Instability in Tier-2/3 Cities

- 4.3.2 Fragmented Ownership of Small Warehouses

- 4.3.3 Reefer-truck Driver Shortage

- 4.3.4 High Import Duty on High-efficiency Compressors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.1.1 Public Warehousing

- 5.1.1.2 Private Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.1.1 Refrigerated Storage

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.3 By Application

- 5.3.1 Fruits & Vegetables

- 5.3.2 Meat & Poultry

- 5.3.3 Fish & Seafood

- 5.3.4 Dairy & Frozen Desserts

- 5.3.5 Bakery & Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals & Biologics

- 5.3.8 Vaccines & Clinical Trial Materials

- 5.3.9 Chemicals & Specialty Materials

- 5.3.10 Other Perishables

- 5.4 By Region

- 5.4.1 North India

- 5.4.1.1 Delhi-NCR

- 5.4.1.2 Punjab

- 5.4.1.3 Haryana

- 5.4.1.4 Others

- 5.4.2 South India

- 5.4.2.1 Karnataka

- 5.4.2.2 Tamil Nadu

- 5.4.2.3 Telangana

- 5.4.2.4 Others

- 5.4.3 West India

- 5.4.3.1 Maharashtra

- 5.4.3.2 Gujarat

- 5.4.3.3 Others

- 5.4.4 East India

- 5.4.4.1 West Bengal

- 5.4.4.2 Odisha

- 5.4.4.3 Others

- 5.4.5 Central India

- 5.4.5.1 Madhya Pradesh

- 5.4.5.2 Chhattisgarh

- 5.4.1 North India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Snowman Logistics Ltd

- 6.4.2 ColdEx Logistics Pvt Ltd

- 6.4.3 TCI Express Ltd

- 6.4.4 DHL Supply Chain India

- 6.4.5 Mahindra Logistics Ltd

- 6.4.6 Gubba Cold Storage Ltd

- 6.4.7 Cold Star Logistics Pvt Ltd

- 6.4.8 CONCOR Cold Chain Logistics

- 6.4.9 Crystal Logistics Cool Chain Ltd

- 6.4.10 R. K. Foodland Pvt Ltd

- 6.4.11 Indraprastha Cold Storage

- 6.4.12 Arihant Cold Storage

- 6.4.13 Godamwale

- 6.4.14 Siddhi Cold Chain

- 6.4.15 Coldrush Logistics

- 6.4.16 Coldman Warehousing & Distribution

- 6.4.17 Indicold Private Limited

- 6.4.18 GK Cold Chain Solutions

- 6.4.19 Transworld

- 6.4.20 CEVA Logistics (Stellar Value Chain Solutions Pvt Ltd)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

义大利低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

义大利低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本冷链物流市场规模、份额、趋势及预测(按服务、温度类型、应用和地区划分,2026-2034年)

日本冷链物流市场规模、份额、趋势及预测(按服务、温度类型、应用和地区划分,2026-2034年) 低温运输市场规模、份额和成长分析(按类型、温度、技术、温度控制和地区划分)—产业预测(2026-2033 年)

低温运输市场规模、份额和成长分析(按类型、温度、技术、温度控制和地区划分)—产业预测(2026-2033 年) 农产品低温运输物流市场预测至2032年:按组件、温度范围、运输方式、储存基础设施、技术、最终用户和地区分類的全球分析

农产品低温运输物流市场预测至2032年:按组件、温度范围、运输方式、储存基础设施、技术、最终用户和地区分類的全球分析 全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年)

全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年) 北美低温运输市场规模、份额和趋势分析报告:按类型、包装、设备、应用、国家和细分市场预测(2025-2033 年)

北美低温运输市场规模、份额和趋势分析报告:按类型、包装、设备、应用、国家和细分市场预测(2025-2033 年) 冷链物流设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

冷链物流设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 低温运输市场按温度范围、设备类型、服务模式、最终用户和分销管道划分-2025-2032 年全球预测低温运输物流市场(按服务类型、温度范围和最终用途)-全球预测,2025-2032

低温运输市场按温度范围、设备类型、服务模式、最终用户和分销管道划分-2025-2032 年全球预测低温运输物流市场(按服务类型、温度范围和最终用途)-全球预测,2025-2032