|

市场调查报告书

商品编码

1910873

菲律宾宅配、速递和小包裹(CEP) 市场:份额分析、产业趋势、统计数据和成长预测 (2026-2031)Philippines Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

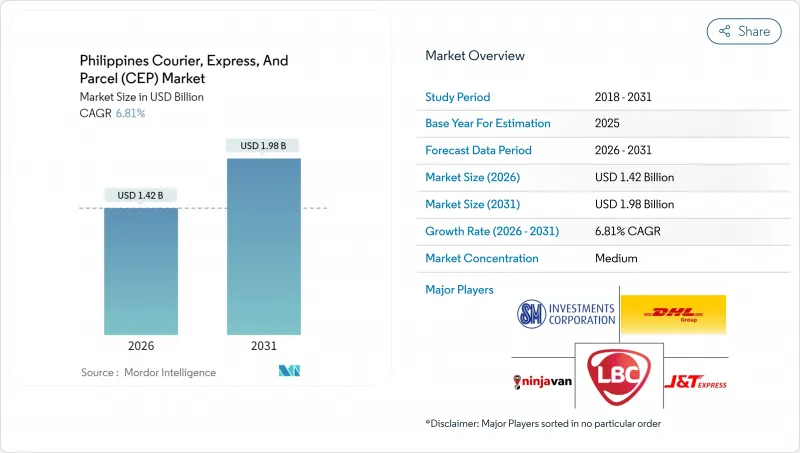

预计菲律宾宅配、速递和小包裹(CEP) 市场将从 2025 年的 13.3 亿美元成长到 2026 年的 14.2 亿美元,预计到 2031 年将达到 19.8 亿美元,2026 年至 2031 年的复合年增长率为 6.81%。

这一成长主要得益于电子商务交易量的激增、持续的基础设施投资以及菲律宾群岛的地理环境,这些因素共同造就了岛际配送解决方案的巨大潜在市场。日益激烈的竞争、不断更新的监管法规以及消费者对即时可见性的日益增长的需求,正促使营运商升级其技术基础设施并重新设计其中心辐射模式。燃油价格的波动和资产密集型网路需求给小规模业者带来了压力,而大型业者则利用自动化技术来保障利润率,这进一步加剧了产业整合的趋势。因此,菲律宾的宅配、快捷邮件和小包裹市场正从以交易量为主导的模式向以技术主导、服务差异化为导向的市场转型,更加註重速度、可靠性和地理覆盖范围。

菲律宾宅配、速递与小包裹(CEP) 市场趋势与洞察

电子商务订单量爆炸性成长

预计到2025年,贸易额将占国内生产总值)的5.5%,这意味着每位消费者的平均小包裹递送频率将成长三倍,现有分拣能力面临巨大压力。营运商正在利用协调高效的自动化系统和动态路线规划工具,改造全国7,641个岛屿上的多种运输方式。模组化枢纽、可扩展的软体和数据驱动的运力规划,使菲律宾宅配、速递和小包裹(CEP)市场能够在不相应增加成本的情况下,应对小型、高频次递送的激增。以电子产品和时尚为主导的零售类别,在提升包裹总量的同时,压缩了平均小包裹收入,这有利于那些实现路线密集化的承运商。电子商务平台越来越重视保证送达时间,并将其作为竞标的关键因素,这推动了承运商对预测分析和即时可见性的运用。在菲律宾的宅配、速递和小包裹(CEP) 产业,投资机器人分拣机和应用程式介面 (API) 整合正成为保持竞争力的先决条件。

马尼拉大都会地区对当日/即时送达的需求

马尼拉大都会区居住1,300万居民,交通网络密集,交通壅塞反而让更灵活的摩托车配送网络比货车配送网络更具优势。随着当日达服务从加值服务转变为基本需求,快递公司正在都会区部署微型仓配中心。这些中心缩短了配送距离,降低了漏送风险,并实现了严格的两小时送达窗口。即时追踪、自动送达证明和主动通知客户已成为主流平台的标准功能。未能达到可见性标准的快递公司可能会面临客户流失的风险,因为那些基于应用程式的竞争对手凭藉透明的、支援GPS定位的服务抢占了市场份额。为了解决当日达服务资本密集的问题,各大快递公司正尝试轻资产的特许经营模式。这种模式将公司自有的配送中心与众包配送团队结合,提高了网路密度,从而支持菲律宾宅配、速递和小包裹(CEP)市场的快速成长。

港口拥挤及岛际交通瓶颈

马尼拉港和宿雾港在旺季期间的运作通常超出设计吞吐能力40%至50%,导致平均延误两天,影响下游货物的交付。泊位有限和人工装卸货柜延长了船舶週转时间,而滚装船(RORO)服务因天气原因取消也会扰乱轻库存模式下至关重要的运营节奏。在港口自动化和泊位扩建计划完成之前,菲律宾宅配、速递和小包裹(CEP)市场的承运商必须保持缓衝库存,确保跨多个港口的替代路线,并製定客户沟通通讯协定以维持服务水准。

细分市场分析

到2025年,电子商务将占据42.10%的市场份额,其中线上市场、D2C品牌和社群卖家将推动每日出货量激增。仓储、退货管理和全通路整合服务的结合正在增强大型平台的客户留存率。 2026年至2031年,医疗物流将维持7.10%的强劲复合年增长率,因为远端医疗、疫苗分发和邮购配药项目需要温控、监管链合规和快速交付。符合GDP认证的仓库、检验的包装和符合监管规定的文件将成为菲律宾宅配、速递和小包裹(CEP)行业的关键差异化因素。

金融服务领域(信用卡帐单、法律文件等)正稳步向数位化管道转型,但某些监管流程仍需要安全的实体交付。製造业和批发业的货物运输涉及大量库存单位(SKU)和重复的大宗订单模式。包括农业和采矿业在内的一级产业依赖宅配网络运输时效性强的样品、备件和合规文件,这印证了该领域对国民经济现代化进程的广泛重要性。

到2025年,国内物流收入将占总收入的64.40%,反映出马尼拉-宿雾-达沃三角地区的贸易集中度较高,该地区的网路密度降低了小包裹成本。业者利用固定路线的卡车运输和模组化微型仓库,在吕宋岛70%的始发地-目的地之间实现48小时内送达。菲律宾国内宅配、快捷邮件和小包裹市场规模预计将稳定成长,但随着基于应用程式的竞争对手不断加大折扣力度,利润率将面临下降。国际小包裹虽然绝对数量较小,但预计在2026年至2031年间将以7.05%的复合年增长率增长,这主要得益于跨境电子商务购物、“balaikbayan boxes”(寄给海外微企业的小包裹)以及中小微企业对海外买家的出口。海关清关、空运空间和监管合规的高额定价有助于提高单位经济效益,使跨境业务成为菲律宾宅配、速递和小包裹(CEP) 市场利润的稳定因素。

双边贸易协定的拓展和电子清关平台的引入,使清关时间缩短了多达48小时,缩小了与区域竞争对手的服务品质差距。克拉克机场和宿雾机场综合货运站的落成,有助于实现南北韩之间货物运输的多元化,并缓解了马尼拉枢纽的压力。这加快了生鲜产品和高价值电子产品的运输速度。市场领导目前提供的服务将国际递送与本地退货安排相结合,充分利用了海外侨民的汇款购物需求,并拓展了菲律宾宅配、速递和小包裹(CEP)行业的全球互联互通。

其他福利

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 人口统计数据

- 按经济活动分類的GDP分配

- 按经济活动分類的GDP成长

- 通货膨胀

- 经济表现及概览

- 电子商务产业的趋势

- 製造业趋势

- 运输和仓储业的GDP

- 出口趋势

- 进口趋势

- 燃油价格

- 物流绩效

- 基础设施

- 法律规范

- 价值炼和通路分析

- 市场驱动因素

- 电子商务订单量爆炸性成长

- 马尼拉大都会地区对当日送达和即时送达的需求

- 首都区以外中小微企业数位化销售蓬勃发展

- 政府发展「更好、更多」的物流走廊

- 透过加强对叫车服务使用者的安全监管来改善劳动力供应

- 在岛国测试无人机和自动配送

- 市场限制

- 港口拥挤及岛际交通瓶颈

- 燃油额外费用上涨对最后一公里配送利润率带来压力

- 将地址系统划分到地方社区

- 基于应用程式的企业之间价格竞争日益激烈

- 市场创新

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 收件地址

- 国内的

- 国际的

- 配送速度

- 表达

- 非快递

- 模型

- B2B

- B2C

- C2C

- 运输重量

- 重型货物

- 轻型货物

- 中等重量货物

- 交通工具

- 航空邮件

- 陆上

- 其他的

- 终端用户产业

- 电子商务

- 金融服务(BFSI)

- 卫生保健

- 製造业

- 一级产业

- 批发零售(线下)

- 其他的

第六章 竞争情势

- 市场集中度

- 关键策略措施 竞争格局:市场集中 / 关键策略倡议 / 市场占有率分析 / 公司简介 / 阿亚拉集团

- 市占率分析

- 公司简介

- Ayala Corporation

- DHL Group

- FedEx

- J& T Express

- Lalamove

- LBC Express Holdings, Inc.

- Ninja Van

- Philippine Postal Corporation(PHLPost)

- SM Investments Corporation(including 2GO)

- United Parcel Service(UPS)

- Ximex Delivery Express Logistics Inc.(XDE)

第七章 市场机会与未来展望

The Philippines courier, express, and parcel market is expected to grow from USD 1.33 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 1.98 billion by 2031 at 6.81% CAGR over 2026-2031.

This growth is propelled by surging e-commerce volumes, sustained infrastructure investment, and the country's archipelagic geography, which together create a large addressable base for island-to-island delivery solutions. Intensifying competition, regulatory modernization, and rising consumer expectations for real-time visibility are prompting operators to upgrade technology stacks and redesign hub-and-spoke models. Consolidation pressure is growing as fuel price volatility and asset-heavy network requirements strain smaller fleets, while scale players leverage automation to protect margins. As a result, the Philippines courier, express, and parcel market is evolving from a volume-oriented model toward a technology-enabled, service-differentiated landscape that prizes speed, reliability, and geographic reach.

Philippines Courier, Express, And Parcel (CEP) Market Trends and Insights

Explosive E-Commerce Order Volumes

Transaction values are expected to represent 5.5% of national GDP in 2025, tripling the average parcel frequency per consumer and stretching existing sortation capacity. Operators are pivoting to high-throughput automation and dynamic routing tools that can orchestrate multiple transport modes across 7,641 islands. Modular hubs, scalable software, and data-driven capacity planning are enabling the Philippines courier, express, and parcel market to absorb a wave of small, frequent shipments without proportionate cost increases. Retail categories led by consumer electronics and fashion are compressing average parcel revenue yet boosting overall volume, rewarding carriers that achieve densification at the route level. E-commerce platforms increasingly condition tender awards on guaranteed delivery windows, pushing carriers toward predictive analytics and real-time visibility. Investments in robotic sorters and application-programming-interface integrations are becoming table stakes for relevance in the Philippines courier, express, and parcel industry.

Same-Day / Instant Delivery Preference in Metro Manila

Metro Manila houses 13 million residents within a dense road network where traffic congestion paradoxically favors nimble motorcycle fleets over vans. Same-day arrival has shifted from premium to baseline expectation, prompting couriers to roll out micro-fulfillment nodes inside the metropolis. These nodes shorten stem mileage, lower failed-delivery risk, and enable tighter two-hour delivery windows. Real-time tracking, automated proof-of-delivery, and proactive customer notifications are now standard features across leading platforms. Carriers that fail to meet visibility benchmarks risk customer churn as app-based challengers capture share with transparent, GPS-enabled service. To meet the capital intensity of same-day service, larger players are experimenting with asset-light franchise models that blend company-owned hubs with crowd-sourced rider supply, reinforcing the network density that underpins express profitability within the Philippines courier, express, and parcel market.

Port Congestion and Inter-Island Shipping Bottlenecks

Manila and Cebu ports routinely operate at 40-50% above designed throughput during peak periods, creating two-day average dwell overruns that ripple into downstream delivery commitments. Limited berthing slots and manual container handling extend vessel turnaround, while weather-driven RORO cancellations disrupt the sailing cadence vital for inventory-light models. Until port automation and berth expansion projects reach completion, carriers must maintain buffer inventory, multi-port contingency routes, and customer communication protocols to protect service levels in the Philippines courier, express, and parcel market.

Other drivers and restraints analyzed in the detailed report include:

- MSME Digital-Selling Boom Outside NCR

- Government "Build Better More" Logistics Corridors

- Rising Fuel Surcharges Pressuring Last-Mile Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-commerce commanded 42.10% share in 2025 as online marketplaces, direct-to-consumer brands, and social sellers collectively fueled daily shipment spikes. Bundled warehousing, returns management, and omnichannel integration services enhance retention of large platform accounts. Healthcare logistics posts a robust 7.10% CAGR between 2026-2031 as telemedicine, vaccine distribution, and prescription-by-mail programs demand temperature integrity, chain-of-custody compliance, and rapid fulfillment. GDP-certified warehouses, validated packaging, and regulatory-aligned documentation become critical differentiators in the Philippines courier, express, and parcel industry.

Financial-services parcels credit-card statements, legal documents-continue a measured migration to digital channels but still require secure physical handover in certain regulatory workflows. Manufacturing and wholesale shipments incorporate heavier SKUs and scheduled bulk-order patterns. Primary industries including agriculture and mining rely on courier networks for time-sensitive samples, spare parts, and compliance paperwork, underscoring the sector's broad-based relevance to national economic modernization.

Domestic flow anchored 64.40% of 2025 revenue, reflecting concentrated trade along the Manila-Cebu-Davao triangle where network density lowers per-parcel cost. Operators leverage fixed-route trucking and modular micro-depots to hit sub-48-hour delivery for 70% of intra-Luzon origin-destination pairs. The Philippines courier, express, and parcel market size for domestic services is projected to grow steadily yet face thinning margins as app-based competitors intensify discounting. International parcels, although smaller in absolute volume, register a 7.05% CAGR between 2026-2031, driven by cross-border e-commerce purchases, balikbayan boxes, and export shipments from MSMEs tapping overseas buyers. Premium pricing for customs clearance, airfreight space, and regulatory compliance underpins higher unit economics, making cross-border a profit stabilizer within the wider Philippines courier, express, and parcel market.

Expanding bilateral trade agreements and electronic customs platforms are shaving up to 48 hours off clearance times, narrowing service-quality gaps with regional peers. As Clark and Cebu airports add integrated cargo terminals, north-south diversion reduces Manila hub pressure, enabling faster transit for perishables and high-value electronics. Market leaders now bundle international shipping with localized returns orchestration, capitalizing on the diaspora's remittance-linked purchases and expanding the Philippines courier, express, and parcel industry's global connectivity.

The Philippines Courier, Express, and Parcel Market Report is Segmented by End User Industry (E-Commerce and More), Destination (Domestic and International), Speed of Delivery (Express and More), Shipment Weight (Heavy Weight Shipments and More), Mode of Transport (Air, Road, and Others), and Model (Business-To-Business, Business-To-Consumer, and Consumer-To-Consumer). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ayala Corporation

- DHL Group

- FedEx

- J&T Express

- Lalamove

- LBC Express Holdings, Inc.

- Ninja Van

- Philippine Postal Corporation (PHLPost)

- SM Investments Corporation (including 2GO)

- United Parcel Service (UPS)

- Ximex Delivery Express Logistics Inc. (XDE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Explosive E-Commerce Order Volumes

- 4.15.2 Same-Day/Instant Delivery Preference in Metro Manila

- 4.15.3 MSME Digital-Selling Boom Outside NCR

- 4.15.4 Government "Build Better More" Logistics Corridors

- 4.15.5 Rider-Security Regulations Improving Workforce Supply

- 4.15.6 Drone and Autonomous Delivery Pilots in Island Provinces

- 4.16 Market Restraints

- 4.16.1 Port Congestion and Inter-Island Shipping Bottlenecks

- 4.16.2 Rising Fuel Surcharges Pressuring Last-Mile Margins

- 4.16.3 Fragmented Address System in Rural Barangays

- 4.16.4 Intensifying Price Wars Among App-Based Players

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Ayala Corporation

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 J&T Express

- 6.4.5 Lalamove

- 6.4.6 LBC Express Holdings, Inc.

- 6.4.7 Ninja Van

- 6.4.8 Philippine Postal Corporation (PHLPost)

- 6.4.9 SM Investments Corporation (including 2GO)

- 6.4.10 United Parcel Service (UPS)

- 6.4.11 Ximex Delivery Express Logistics Inc. (XDE)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球国际宅配市场

2026-2030年全球国际宅配市场 2026-2030年全球宅配市场

2026-2030年全球宅配市场 2026-2030年全球宅配递送服务市场

2026-2030年全球宅配递送服务市场 义大利快递、速递、小包裹:市场占有率分析、产业趋势、统计数据、成长预测(2026-2031 年)欧洲宅配、速递和小包裹(CEP) 市场:市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)法国快递、速递、小包裹市场:份额分析、行业趋势、统计数据和成长预测(2026-2031 年)马来西亚宅配、速递和小包裹(CEP) 市场:市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)

义大利快递、速递、小包裹:市场占有率分析、产业趋势、统计数据、成长预测(2026-2031 年)欧洲宅配、速递和小包裹(CEP) 市场:市场份额分析、行业趋势和统计数据、成长预测 (2026-2031)法国快递、速递、小包裹市场:份额分析、行业趋势、统计数据和成长预测(2026-2031 年)马来西亚宅配、速递和小包裹(CEP) 市场:市场份额分析、行业趋势和统计数据、成长预测 (2026-2031) 2032年超当地语系化生鲜配送市场预测:依产品类型、服务类型、平台类型、经营模式、最终用户和地区分類的全球分析

2032年超当地语系化生鲜配送市场预测:依产品类型、服务类型、平台类型、经营模式、最终用户和地区分類的全球分析 日本国内快递和包裹市场报告(按商业模式(企业对企业、企业对消费者、消费者对消费者)、类型、最终用户和地区划分,2026-2034 年)日本国际快递和包裹市场报告(按业务类型(企业对企业、企业对消费者和消费者对消费者)、类型、最终用户和地区划分,2026-2034 年)

日本国内快递和包裹市场报告(按商业模式(企业对企业、企业对消费者、消费者对消费者)、类型、最终用户和地区划分,2026-2034 年)日本国际快递和包裹市场报告(按业务类型(企业对企业、企业对消费者和消费者对消费者)、类型、最终用户和地区划分,2026-2034 年)