|

市场调查报告书

商品编码

1934813

淀粉及淀粉衍生物:市占率分析、产业趋势及统计、成长预测(2026-2031)Starch And Starch Derivatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

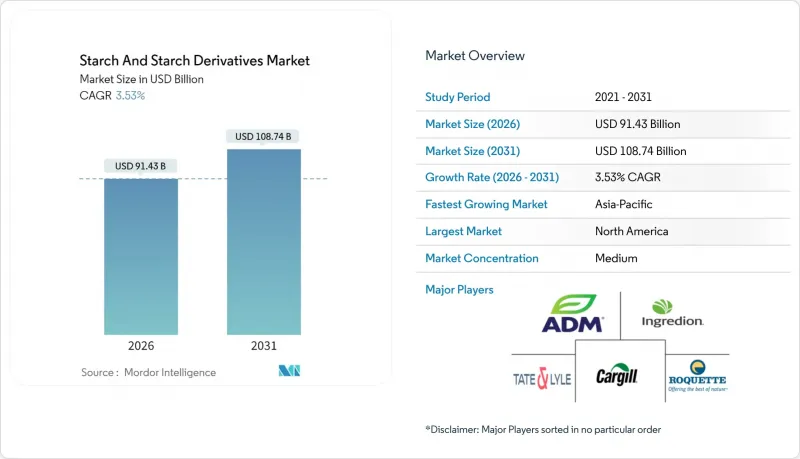

预计到 2026 年,淀粉及淀粉衍生物市场价值将达到 914.3 亿美元,高于 2025 年的 883.1 亿美元,预计到 2031 年将达到 1,087.4 亿美元。

预计2026年至2031年年复合成长率(CAGR)为3.53%。

市场成长主要由满足洁净标示、植物来源配方和工业生物解决方案等需求的专业细分市场所驱动。这些细分市场满足了消费者对食品、医药和工业应用中天然成分和永续产品日益增长的需求。儘管原材料成本(尤其是玉米和小麦价格)的波动会影响盈利,但监管机构对永续性重视为淀粉基生质塑胶和药用辅料创造了机会。针对特定应用开发创新型淀粉衍生物,例如用于食品增稠和稳定的改性淀粉,也促进了市场扩张。北美以34.76%的市占率主导,这得益于其成熟的食品加工业和技术进步。亚太地区成长更为强劲,复合年增长率达5.66%,这主要得益于新增产能、木薯用途的拓展以及在医疗保健领域的应用日益广泛。新兴经济体可支配收入的增加、饮食习惯的改变以及工业应用的拓展也进一步推动了这一成长。

全球淀粉及淀粉衍生物市场趋势与洞察

全球加工食品和简便食品产业的快速扩张

加工食品产业的演变正在显着改变淀粉的需求模式。製造商正在寻求更专业的淀粉解决方案,以在各种加工条件下保持稳定性并延长产品的保质期。这一趋势在调理食品领域尤其明显,改性淀粉因其更优异的冻融稳定性和更佳的质地保持性,正日益取代传统淀粉。业界向洁净标示配方的转变,为提供未经化学加工的功能性改质淀粉的供应商创造了巨大的机会。食品製造商正积极探索既能满足功能性要求又能满足消费者对清洁配料偏好的天然替代品。例如,英联食品配料公司(Ingredion)于2024年8月推出了一款功能性天然玉米粉,以扩展其洁净标示产品系列,从而响应市场对天然淀粉解决方案日益增长的需求。此举反映了行业整体趋势,即在保持食品应用所需技术性能的同时,致力于开发永续、以消费者为导向的配料。

消费者趋势正转向植物来源和功能性成分。

消费者对植物来源替代品的需求不断增长,为淀粉生产商创造了开发能够模拟动物基成分特性的专用质地改良剂的机会。根据美国农业部2023年的数据,德国已有158万人开始采用植物性饮食,这标誌着饮食习惯发生了显着转变。目前,淀粉基解决方案不仅能改善消化率和持续释放能量等功能性优势,还能创造新的质地。这些解决方案使食品生产商能够改善植物来源替代品的质地、稳定性以及整体口感。研发重点正转向具有特定营养成分的淀粉,例如可作为益生元纤维的抗解淀粉。这使得生产商能够在满足监管要求、提高加工食品营养价值的同时,在註重健康的食品类别中实施高价策略。淀粉技术的进步也促进了洁净标示产品的开发,满足了消费者对天然、低加工成分的需求。

农产品原物料价格波动会影响利润率。

原材料价格波动给淀粉加工商带来了巨大挑战,气候变迁和地缘政治紧张局势导致供应链中断和生产成本上升。美国农业部近期数据显示,2024年玉米价格波动剧烈,影响了製造商维持价格稳定的能力。原料品质的波动会降低淀粉萃取效率并增加加工成本,进而影响投入成本和产量。农业多样性有限且仓储基础设施不足的地区受到的影响尤其严重,更容易受到市场波动的影响。淀粉加工商正透过原材料来源多元化和采用即使在原材料品质较低的情况下也能保持产品品质的技术来应对这些挑战。这些措施包括与不同地区的多个供应商建立合作关係,以及投资建造先进的加工设施。行业适应策略还包括改善库存管理系统和开发避险机制,以减轻市场不确定性的影响。

细分市场分析

截至2025年,淀粉衍生物市占率达到54.02%,这主要得益于其在食品、医药和工业领域的广泛应用。改性淀粉虽然目前规模较小,但凭藉其更优异的功能性和洁净标示潜力,正迅速成为创新前沿,预计2026年至2031年的复合年增长率将达到5.30%。天然淀粉虽然仍持续用于传统应用,但其面临来自改性淀粉日益激烈的竞争,后者在严苛的加工条件下表现较佳。

在淀粉衍生物中,葡萄糖浆和高果糖玉米糖浆(HFCS)占据重要地位,尤其是在饮料应用领域。同时,麦芽糊精作为一种用途广泛的配料,在需要特定黏度和质地特性的食品配方中发挥重要作用。糊精类产品因其特殊的溶解性和黏附性,在需要特定溶解性和黏附性的特殊应用领域中也日益受到关注。

玉米淀粉因其供应充足、成本效益高以及用途广泛,预计2025年将占据市场主导地位,市占率高达68.95%。马铃薯淀粉预计将成为成长最快的原料,2026年至2031年的复合年增长率将达到5.05%,这主要得益于其优异的黏度和透明度,尤其是在马铃薯种植基地发达的地区,马铃薯淀粉在食品应用中具有显着优势。

小麦淀粉凭藉其本地农业生产和完善的加工设施,在欧洲,尤其是在欧洲,占据着重要的市场地位。木薯淀粉因其风味中性且非基因改造,在洁净标示应用领域备受关注。同时,大米和木薯等其他原料也在为特殊应用开闢利基市场。市场参与者正不断推出新的淀粉产品以满足日益增长的需求。例如,2024年8月,罗盖特兄弟公司推出了「Creamu」系列烹饪用木薯淀粉,该产品可用于烘焙馅料、甜点和乳製品。

区域分析

预计到2025年,北美将以34.41%的市占率引领淀粉及淀粉衍生物市场,这主要得益于该地区丰富的玉米产量和先进的加工基础设施。该地区强大的食品加工和製药业维持对特种淀粉产品的稳定需求。该产业正从提供大宗商品产品转向专注于高附加价值衍生物和特种产品,以期获得更高的利润率。此外,文明病的增加也推动了该地区对淀粉作为脂肪替代品的需求。根据美国疾病管制与预防中心(CDC)2023年的数据,美国成年人肥胖率为40.3%。

亚太地区拥有最高的成长潜力,2026年至2031年的复合年增长率将达到5.38%。这一成长主要得益于快速的工业化、不断扩张的食品加工业以及日益增长的製药业。日本专注于高品质特种淀粉产品,而澳洲则透过淀粉改质技术的研究做出贡献。该地区丰富的农业资源,包括水稻、玉米和木薯,使得淀粉生产来源多样化成为可能,从而支持了本地供应链和特种产品的开发。

欧洲凭藉其成熟的食品加工业和对永续植物来源原料的重视,拥有强大的市场地位。严格的食品标籤和永续性法规结构正在推动洁净标示淀粉解决方案和可生物降解应用领域的创新,这不仅给市场参与企业带来了挑战,也带来了机会。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球加工食品和简便食品产业的快速扩张

- 消费者趋势正转向植物来源和功能性成分。

- 与其他水溶性多醣相比,淀粉的成本效益

- 淀粉在食品和饮料应用中被广泛用作脂肪替代品

- 酶法和物理改质技术的进步

- 淀粉衍生物在非食品工业领域的应用

- 市场限制

- 农产品原物料价格波动对利润率的影响

- 天然淀粉的功能稳定性与保存期限限制

- 由于含有基因改造成分,引发了品质问题。

- 改质淀粉或功能性淀粉标籤方面的监管复杂性

- 供应链分析

- 监理展望

- 波特五力模型

- 新进入者的威胁

- 买方和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 天然淀粉

- 改性淀粉

- 淀粉衍生物

- 葡萄糖浆

- 高果糖玉米糖浆(HFCS)

- 麦芽糊精

- 糊精

- 其他的

- 按原料

- 玉米

- 小麦

- 马铃薯

- 木薯

- 其他的

- 按形式

- 粉末

- 液体

- 透过使用

- 食品/饮料

- 製药

- 个人护理和化妆品

- 饲料

- 纺织品

- 纸张和纸板

- 其他的

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 英国

- 德国

- 西班牙

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市场排名分析

- 公司简介

- Archer Daniels Midland Company

- Cargill, Incorporated

- Ingredion Inc.

- Tate & Lyle PLC

- Roquette Freres SA

- Sudzucker Group

- Avebe UA

- AGRANA Beteiligungs-AG

- Tereos SA

- Grain Processing Corporation

- Manildra Group

- Japan Corn Starch Co. Ltd

- Angel Starch & Food Pvt Ltd

- Gulshan Polyols Ltd

- Universal Starch-Chem Allied Ltd

- SPAC Starch Products(India)Private Ltd.

- Everest Starch India Pvt. Ltd.

- Sage Oil LLC

- Medikonda Nutrients

- Meelunie BV

第七章 市场机会与未来展望

The starch and starch derivatives market size in 2026 is estimated at USD 91.43 billion, growing from 2025 value of USD 88.31 billion with 2031 projections showing USD 108.74 billion, growing at 3.53% CAGR over 2026-2031.

The market growth is driven by specialized segments that meet the requirements for clean labels, plant-based formulations, and industrial biosolutions. These segments are responding to increasing consumer demand for natural ingredients and sustainable products across food, pharmaceutical, and industrial applications. Fluctuations in raw material costs, particularly corn and wheat, influence profitability, while increasing regulatory focus on sustainability creates opportunities in starch-based bioplastics and pharmaceutical excipients. The development of innovative starch derivatives for specific applications, such as modified starches for food thickening and stabilization, is contributing to market expansion. North America dominates the market with a 34.76% share, driven by established food processing industries and technological advancements. The Asia-Pacific region exhibits stronger growth at a 5.66% CAGR, supported by new production capacity, cassava diversification, and increased healthcare applications. This growth is further enhanced by rising disposable incomes, changing dietary preferences, and expanding industrial applications in emerging economies.

Global Starch And Starch Derivatives Market Trends and Insights

Rapid Expansion of the Global Processed and Convenience Food Industry

The processed food industry's evolution is driving significant changes in starch demand patterns, as manufacturers require increasingly specialized starch solutions that maintain stability during various processing conditions and extend product shelf life. This trend is particularly prominent in the ready-meal segment, where modified starches are replacing traditional varieties due to their enhanced freeze-thaw stability and superior texture retention capabilities. The industry's shift toward clean-label formulations presents substantial opportunities for suppliers offering functionally modified starches without chemical processing. Food manufacturers are actively seeking natural alternatives that meet both functional requirements and consumer preferences for cleaner ingredients. For example, Ingredion launched a functional native corn starch in August 2024 to expand its clean-label product portfolio, responding to the growing market demand for natural starch solutions. This development reflects the broader industry movement toward sustainable and consumer-friendly ingredients while maintaining the necessary technical performance in food applications.

Shifting Consumer Trends Towards Plant-Based and Functional Ingredients

The growing consumer demand for plant-based alternatives has created opportunities for starch producers to develop specialized texturizing agents that mimic the characteristics of animal-derived ingredients. According to the United States Department of Agriculture data from 2023, 1.58 million people in Germany adopted plant-based diets, reflecting a significant shift in dietary preferences. Starch-based solutions now deliver functional benefits, including improved digestibility and sustained energy release, while creating new sensory experiences. These solutions enable food manufacturers to enhance product texture, stability, and overall mouthfeel in plant-based alternatives. The development focus has shifted toward starches with specific nutritional profiles, such as resistant starches that act as prebiotic fiber. This enables manufacturers to implement premium pricing strategies in health-focused food categories while meeting regulatory requirements for improved nutritional content in processed foods. The advancement in starch technology has also facilitated the creation of clean-label products, addressing consumer demands for natural and minimally processed ingredients.

Volatility in Agricultural Raw Material Prices Impacting Profit Margins

Raw material price volatility presents a significant challenge for starch processors due to climate change and geopolitical tensions disrupting supply chains and affecting production costs. Recent data from the U.S. Department of Agriculture indicates that corn prices experienced substantial volatility in 2024, affecting manufacturers' ability to maintain consistent pricing. These disruptions influence both input costs and production yields, as variations in raw material quality reduce starch extraction efficiency and increase processing expenses. The impact is particularly severe in regions with limited agricultural diversity and inadequate storage infrastructure, leading to heightened vulnerability to market fluctuations. Starch processors are addressing these challenges by diversifying their raw material sources and implementing technologies capable of processing lower-grade inputs while maintaining output quality. This includes establishing relationships with multiple suppliers across different geographical regions and investing in advanced processing equipment. The industry's adaptation strategies also encompass improved inventory management systems and the development of risk-hedging mechanisms to mitigate the effects of market uncertainties.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Effectiveness of Starch Compared to Other Hydrocolloids

- Widespread Use of Starch as a Fat Replacer in Food and Beverage Application

- Limited Functional Stability and Shelf Life of Native Starches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The starch derivatives segment held 54.02% market share in 2025, benefiting from its diverse applications across food, pharmaceutical, and industrial sectors. Modified starch, though currently smaller, is emerging as the innovation frontier with 5.30% CAGR projected for 2026-2031, driven by its enhanced functional properties and clean-label potential. Native starch continues to serve traditional applications but faces increasing competition from modified variants that offer superior performance in challenging processing conditions.

Within starch derivatives, glucose syrups and high fructose corn syrup (HFCS) maintain significant positions, particularly in beverage applications, while maltodextrin serves as a versatile ingredient in food formulations requiring specific viscosity and texture profiles. The dextrins segment is gaining traction in specialty applications where specific solubility and adhesive properties are required.

Maize starch dominated the market with a 68.95% share in 2025, benefiting from its abundant supply, cost-effectiveness, and versatile functional properties across multiple applications. Potato starch is emerging as the fastest-growing source at 5.05% CAGR for 2026-2031, driven by its superior viscosity and clarity in food applications, particularly in regions with established potato cultivation infrastructure.

Wheat starch maintains a significant position, especially in Europe, where it benefits from local agricultural production and established processing facilities. Tapioca starch is gaining traction in clean-label applications due to its neutral flavor profile and non-GMO status, while other sources like rice and cassava are finding niches in specialty applications. The market players are launching new starches in the market to cater to the rising demand. For instance, in August 2024, Roquette Freres launched a range of cook-up tapioca starches, Clearem. They are used in bakery fillings, desserts, and dairy products.

The Starch and Starch Derivatives Market Report is Segmented by Type (Native Starch, Modified Starch, and Starch Derivatives), Source (Maize, Wheat, and More), Form (Powder and Liquid), Application (Food and Beverages, Pharmaceuticals, and More) and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America leads the starch and starch derivatives market with a 34.41% share in 2025, supported by its extensive corn production and advanced processing infrastructure. The region's strong food processing and pharmaceutical industries maintain consistent demand for specialized starch products. The industry has evolved beyond commodity offerings to focus on value-added derivatives and specialty products to achieve higher margins. Additionally, the demand for starches as fat replacers is increasing in the region, owing to the rising incidence of lifestyle diseases. According to the Centers for Disease Control and Prevention (CDC) , data from 2023, 40.3% of adults in the United States were obese.

Asia-Pacific demonstrates the highest growth potential with a projected CAGR of 5.38% during 2026-2031. This growth stems from rapid industrialization, expanding food processing sectors, and increasing pharmaceutical manufacturing. Japan specializes in high-quality, specialized starch products, while Australia contributes through research in starch modifications. The region's diverse agricultural resources, including rice, corn, and cassava, enable source diversification in starch production, supporting localized supply chains and specialized product development.

Europe holds a substantial market position through its established food processing industry and emphasis on sustainable, plant-based ingredients. The region's strict regulatory framework for food labeling and sustainability drives innovation in clean-label starch solutions and biodegradable applications, presenting both challenges and opportunities for market participants.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Ingredion Inc.

- Tate & Lyle PLC

- Roquette Freres S.A.

- Sudzucker Group

- Avebe U.A.

- AGRANA Beteiligungs-AG

- Tereos S.A.

- Grain Processing Corporation

- Manildra Group

- Japan Corn Starch Co. Ltd

- Angel Starch & Food Pvt Ltd

- Gulshan Polyols Ltd

- Universal Starch-Chem Allied Ltd

- SPAC Starch Products (India) Private Ltd.

- Everest Starch India Pvt. Ltd.

- Sage Oil LLC

- Medikonda Nutrients

- Meelunie B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of the Global Processed and Convenience Food Industry

- 4.2.2 Shifting Consumer Trends Towards Plant-Based and Functional Ingredients

- 4.2.3 Cost-Effectiveness of Starch Compared to Other Hydrocolloids

- 4.2.4 Widespread Use of Starch as a Fat Replacer in Food and Beverage Application

- 4.2.5 Advancement in Enzymatic and Physical Modification Techniques

- 4.2.6 Adoption of Starch Derivatives in Industrial Applications Beyond Food

- 4.3 Market Restraints

- 4.3.1 Volatility in Agricultural Raw Material Prices Impacting Profit Margins

- 4.3.2 Limited Functional Stability and Shelf Life of Native Starches

- 4.3.3 Quality Concerns Due to Genetically Modified Ingredient Adulteration

- 4.3.4 Regulatory Complexity in Labeling Modified or Functional Starches

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Native Starch

- 5.1.2 Modified Starch

- 5.1.3 Starch Derivatives

- 5.1.3.1 Glucose Syrups

- 5.1.3.2 High Fructose Corn Syrup (HFCS)

- 5.1.3.3 Maltodextrin

- 5.1.3.4 Dextrins

- 5.1.3.5 Others

- 5.2 By Source

- 5.2.1 Maize

- 5.2.2 Wheat

- 5.2.3 Potato

- 5.2.4 Tapioca

- 5.2.5 Others

- 5.3 By Form

- 5.3.1 Powder

- 5.3.2 Liquid

- 5.4 By Application

- 5.4.1 Food and Beverage

- 5.4.2 Pharmaceutial

- 5.4.3 Personal Care and Cosmetics

- 5.4.4 Animal Feed

- 5.4.5 Textile

- 5.4.6 Paper and Corrugating

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 Spain

- 5.5.2.4 France

- 5.5.2.5 Italy

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Archer Daniels Midland Company

- 6.4.2 Cargill, Incorporated

- 6.4.3 Ingredion Inc.

- 6.4.4 Tate & Lyle PLC

- 6.4.5 Roquette Freres S.A.

- 6.4.6 Sudzucker Group

- 6.4.7 Avebe U.A.

- 6.4.8 AGRANA Beteiligungs-AG

- 6.4.9 Tereos S.A.

- 6.4.10 Grain Processing Corporation

- 6.4.11 Manildra Group

- 6.4.12 Japan Corn Starch Co. Ltd

- 6.4.13 Angel Starch & Food Pvt Ltd

- 6.4.14 Gulshan Polyols Ltd

- 6.4.15 Universal Starch-Chem Allied Ltd

- 6.4.16 SPAC Starch Products (India) Private Ltd.

- 6.4.17 Everest Starch India Pvt. Ltd.

- 6.4.18 Sage Oil LLC

- 6.4.19 Medikonda Nutrients

- 6.4.20 Meelunie B.V.

7 Market Opportunities and Future Outlook

2026-2030年全球淀粉衍生物市场

2026-2030年全球淀粉衍生物市场 淀粉衍生物市场规模、份额及成长分析(按产品类型、原料、应用、功能及地区划分)-2026-2033年产业预测

淀粉衍生物市场规模、份额及成长分析(按产品类型、原料、应用、功能及地区划分)-2026-2033年产业预测 淀粉衍生物市场按应用、产品类型、来源、功能和物理形态划分-2025-2032年全球预测

淀粉衍生物市场按应用、产品类型、来源、功能和物理形态划分-2025-2032年全球预测 淀粉衍生物:市占率分析、产业趋势、统计、成长预测(2025-2030)

淀粉衍生物:市占率分析、产业趋势、统计、成长预测(2025-2030) 2025年全球淀粉衍生物市场报告印度淀粉及淀粉衍生物:市占率分析、产业趋势、统计及成长预测(2025-2030)

2025年全球淀粉衍生物市场报告印度淀粉及淀粉衍生物:市占率分析、产业趋势、统计及成长预测(2025-2030) 淀粉衍生物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

淀粉衍生物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 淀粉衍生物市场按产品(麦芽糊精、葡萄糖浆、环糊精、水解物、改性淀粉等)、应用(食品和饮料、化妆品、纸张、药品、饲料等)和地区划分,2025 年至 2033 年

淀粉衍生物市场按产品(麦芽糊精、葡萄糖浆、环糊精、水解物、改性淀粉等)、应用(食品和饮料、化妆品、纸张、药品、饲料等)和地区划分,2025 年至 2033 年 淀粉衍生物市场规模、份额、趋势分析报告:产品、应用、地区、细分市场预测,2025-2030 年

淀粉衍生物市场规模、份额、趋势分析报告:产品、应用、地区、细分市场预测,2025-2030 年 到 2030 年淀粉衍生物市场预测:全球类型、原材料、形式、功能、应用、最终用户和地区

到 2030 年淀粉衍生物市场预测:全球类型、原材料、形式、功能、应用、最终用户和地区