|

市场调查报告书

商品编码

1934882

德国自助仓储市场占有率分析、产业趋势与统计、成长预测(2026-2031)Germany Self-Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

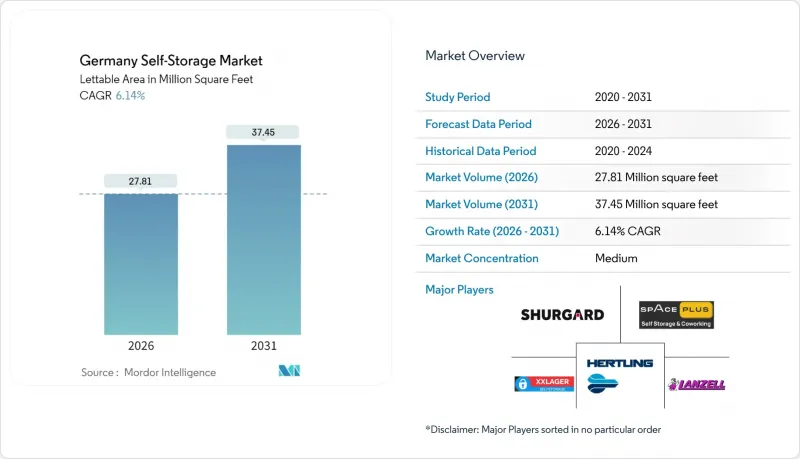

德国自助仓储市场预计将从 2025 年的 2,620 万平方英尺成长到 2026 年的 2,781 万平方英尺,从 2026 年到 2031 年的复合年增长率为 6.14%,到 2031 年将达到 3,745 万平方英尺。

儘管德国各地的建设活动有所萎缩,但都市区的住宅短缺、强劲的电子商务成长以及持续的机构资本流入,仍支撑着高需求。企业正转向轻资产租赁物业以缓解建筑成本上涨,预计2024年建筑成本指数将达到118.9点。房地产科技(Proptech)的应用,包括智慧门锁、自动收费和人工智慧安防,可将营运成本降低高达20%,并实现全天候访问,从而增强无人值守营运的竞争力。温控设施的成长最为迅速,因为中小企业需要可靠的温控库存储存空间,而保险折扣也鼓励家庭将贵重物品存放在安全的设施中。产业整合正在加速,像SureGuard和MyPlace这样资金雄厚的公司正积极进行收购,而97亿欧元的不良商业房地产贷款为其提供了资金支持,从而形成了大量不良资产。

德国自助仓储市场趋势与分析

都市化和平均居住面积缩小

2024年柏林住宅建设许可数量较去年同期下降24%,导致公寓空置率降至历史新低。这迫使居民搬入面积较小的住宅,个人空间受到挤压,并推高了对外部储物单元的需求。单身家庭数量的增加以及千禧世代住宅的推迟,都加剧了储物需求,而不断上涨的建材成本(2024年达到119.9指数点)则限制了住宅供应。市政高密度化政策限制了容积率,促使人们选择垂直居住,并鼓励居民在附近租用储物柜。即使建筑量趋于稳定,长期的人口压力仍将维持收纳需求。位于人口密集住宅5公里范围内的企业运转率超过90%,证实了生活空间缩小与利用率提高之间的相关性。

电子商务成长和小型企业库存需求

预计到2025年,德国线上零售业将成长3%(相较之下,整体零售业成长率为2%),这将推动德国线上零售业实现多年强劲成长,并扩大对弹性储存的需求。中小企业正在使用面积在50至150平方英尺之间的温控仓库作为微型仓配中心,以应对季节性需求高峰、退货以及欧盟跨境配送。按月租赁协议使经销商能够在销售波动不定的情况下避免长期仓储义务。汉堡和科隆週边的物流园区平均运转率高达92%,因为企业都在寻求接近性小包裹转运中心的位置。温控仓库的租金溢价为15%至20%,反映出企业愿意为温度控制带来的安全性和保险合规性支付更高的价格。这也凸显了德国自助仓储市场为何持续调整产品设计以适应全通路零售的需求。

限制性分区和土地使用许可

多层审批制度延长了开发週期,在柏林和汉堡等地,开发週期往往超过24个月。联邦和州级建筑法规的差异增加了技术复杂性。环境评估和噪音评估进一步延缓了核准流程。开发商承担持有成本,导致损益两租金上涨,并在租金无法覆盖资本成本的情况下阻碍计划进度。地方政府对相关规定的不同解读也增加了不确定性,阻碍了閒置的零售和工业地产改建为仓储设施,儘管有潜在租金。

细分市场分析

截至2025年,个人用途将占德国自助仓储市场份额的73.96%。这主要是由于随着住宅面积的减少,家庭对外部储存空间的依赖性日益增强。该细分市场目前占德国自助仓储市场1,937万平方英尺,预计到2031年将达2,640万平方英尺,年均成长率为5.29%。由于单身家庭数量增加、住宅计画延后以及都市区租金上涨,个人用途的仓储日利用率依然居高不下。个人租赁合约的平均面积为56平方英尺,为营运商提供了稳定的现金流。

儘管企业用户的规模较小,但预计其储存面积将以7.74%的复合年增长率成长,从2025年的683万平方英尺成长到2031年的1,070万平方英尺。中小企业正在使用温控仓库来管理尖峰时段和处理退货。随着混合办公模式减少办公空间,专业服务公司正在将文件异地储存。 Sirius Real Estate的Smartspace平台是商业转型的典型例子,在70%的运转率下,每年可创造870万欧元的储存租金。

截至2025年,小型和中型储物间(面积小于40平方英尺)将占德国自助仓储市场的47.35%,相当于1,241万平方英尺的可出租面积。学生、外籍人士和都市区居住者选择这些储物间来存放季节性物品和个人物品。平均租期为7.4个月,略长于其他欧洲国家。

面积较大的仓储单位(超过100平方英尺)成长最快,复合年增长率达6.86%,这主要得益于企业和住宅维修对库存、设备和家具储存的需求。预计到2031年,此细分市场将填补市场空白,达到1,010万平方英尺。营运商正在引入车辆直达通道和装卸平台来吸引商业租户,与中型仓储单元相比,这些单元的每平方英尺出租收入最多可提高18%。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 都市化和平均居住面积缩小

- 电子商务的成长和小型企业的库存需求

- 提高学生和专业的住宅流动性

- 由于住宅存量老化,住宅维修迅速增加。

- 高价值物品异地存放可享保险折扣。

- 利用Proptech进行无人设施操作

- 市场限制

- 限制性分区和土地使用许可

- 都市区土地价格和建筑成本不断上涨

- 能源价格上涨正在挤压温控设施的利润空间。

- 当地居民发起“社区反位置运动”,反对新位置。

- 产业价值链分析

- 监管环境

- 宏观经济因素的影响

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

- PESTEL 分析

- 消费者在选择自助仓储设施时需要考虑的关键因素

第五章 德国市场动态

- 运转率分析

- 平均租金趋势

- 新冠疫情前后市场受到的影响

- 盈利分析

- 新冠疫情前后市场受到的影响

- 平均设施规模

第六章 市场规模及成长预测(单位)

- 最终用户

- 个人

- 商业

- 按储存尺寸

- 小型至中型单位(小于40平方英尺)

- 大单元(超过 40 平方英尺)

- 其他(储物柜/双层堆迭)

- 依储存类型

- 空调控制型

- 非空调型

- 依所有权类型

- 拥有

- 租赁

第七章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Shurgard Self-Storage SA

- SelfStorage Dein Lagerraum GmbH(MyPlace Self-Storage)

- Space Plus Store GmbH

- Rousselet Groupe SA(HOMEBOX)

- Pickens Selfstorage GmbH

- Lagerbox Holding GmbH and Co. KG

- 1BOX Deutschland GmbH

- Storebox Holding GmbH

- ZeitLager GmbH

- XXLAGER Selfstorage GmbH

- BOXIE24 Deutschland GmbH

- Hertling GmbH and Co. KG

- Lanzell Spezialtransporte GmbH

- Klassik Umzuge GmbH

- KingBox Self-Storage GmbH

- CityBox24 GmbH

- CubeStorage Deutschland GmbH

- Jojo-Lagerhaus GmbH

- Easy-Selfstorage GmbH

- Container Self-Storage AG

第八章:主要自助仓储业者的市场份额

第九章:市场机会与未来展望

- 閒置频段与未满足需求评估

The Germany Self-Storage market is expected to grow from 26.2 million sq.ft in 2025 to 27.81 million sq.ft in 2026 and is forecast to reach 37.45 million sq.ft by 2031 at 6.14% CAGR over 2026-2031.

Urban housing shortages, resilient e-commerce growth and sustained institutional capital flows keep demand elevated even as Germany's wider construction activity contracts. Operators favor asset-light leased facilities to mitigate construction cost inflation that hit 118.9 index points in 2024. PropTech adoption, including smart-lock, automated billing and AI security, cuts operating costs by up to 20% and unlocks 24/7 access, strengthening the competitive position of unmanned formats. Climate-controlled capacity grows fastest because SMEs seek reliable storage for temperature-sensitive inventory while insurance discounts encourage households to protect valuables in secure facilities. Consolidation intensifies as Shurgard, MyPlace and other well-capitalized players pursue acquisitions amid EUR 9.7 billion in non-performing commercial real-estate loans, creating a pipeline of distressed assets.

Germany Self-Storage Market Trends and Insights

Urbanisation and Shrinking Average Dwelling Size

Housing permits fell 24% year over year in 2024 and apartment vacancies hit record lows in Berlin, forcing households into smaller homes, tightening personal space and fueling demand for external units. Single-person households and delayed ownership among millennials intensify storage requirements, while building-material costs that climbed to 119.9 index points in 2024 discourage new residential supply. Municipal densification policies cap floor-space ratios, making vertical living unavoidable and prompting residents to rent nearby storage lockers. Long-term demographic pressure keeps demand durable even if construction volumes stabilize. Operators located within 5 kilometers of dense residential districts report occupancy above 90%, confirming the correlation between shrinking living space and take-up rates.

Growth in E-commerce and SME Inventory Needs

German online retail will grow 3% in 2025 versus 2% for total retail, extending a multiyear outperformance that enlarges flexible storage demand. SMEs use 50- to 150-sq ft climate-controlled rooms as micro-fulfillment nodes to manage seasonal peaks, returns and cross-border shipments within the EU. For merchants, month-to-month leases avoid long warehouse contracts amid uncertain sales volatility. Logistics parks ringing Hamburg and Cologne see blended occupancy of 92% as businesses seek proximity to parcel hubs. Rent premiums of 15-20% for climate-controlled units illustrate a willingness to pay for temperature safety and insurance compliance. This reinforces why the Germany self-storage market keeps aligning product design with omnichannel retail needs.

Restrictive Zoning and Land-Use Permits

Multi-layered permitting regimes lengthen development cycles, often exceeding 24 months in Berlin and Hamburg. Compliance with separate federal and state building codes adds technical complexity. Environmental reviews and noise assessments further protract approvals. Developers incur holding costs that raise breakeven rents, sometimes stalling projects where achievable rates cannot cover higher capitalized costs. Variability in municipal interpretations also adds uncertainty, discouraging conversion of vacant retail or industrial properties into storage despite latent demand.

Other drivers and restraints analyzed in the detailed report include:

- Higher Residential Mobility Among Students and Professionals

- Surge in Home Renovations Amid Ageing Housing Stock

- Escalating Urban Land and Construction Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Personal accounts generated 73.96% of Germany self-storage market share in 2025 as households relied heavily on external space amid shrinking apartments. The segment occupies 19.37 million sq ft within the Germany self-storage market size and is expected to reach 26.4 million sq ft by 2031, growing 5.29% annually. Single-person households, delayed homeownership and higher urban rents keep day-to-day occupancy high. Personal contracts average 56 sq ft, underpinning steady cash flow for operators.

Business users account for a smaller base but contribute a 7.74% CAGR, climbing from 6.83 million sq ft in 2025 to an estimated 10.7 million sq ft by 2031. SMEs leverage climate-controlled rooms to manage peak inventory and returns. Professional service firms archive documents off-site as offices downsize under hybrid-work models. Sirius Real Estate's Smartspace platform illustrates the commercial pivot, generating EUR 8.7 million annualized storage rent at 70% occupancy.

Small and medium rooms under 40 sq ft held 47.35% of Germany self-storage market share in 2025, equating to 12.41 million sq ft of lettable area within the Germany self-storage market size. Students, expatriates and urban renters choose these units for seasonal items and personal effects. Average stay lasts 7.4 months, moderately longer than European peers.

Large units above 100 sq ft recorded the fastest trajectory at 6.86% CAGR as businesses and home renovators require roomier space for inventory, equipment and furniture. The segment should reach 10.1 million sq ft by 2031, narrowing the share gap. Operators have introduced drive-up access and loading docks to attract commercial tenants, enhancing revenue per occupied square foot by up to 18% compared with mid-sized rooms.

The Germany Self-Storage Market Report is Segmented by End-User (Personal and Business), Storage Size (Small and Medium Units Less Than 40 Sq Ft, Large Units Above 40 Sq Ft, and More), Storage Type (Climate-Controlled and Non-Climate-Controlled), Ownership Pattern (Owned and Leased). The Market Forecasts are Provided in Terms of Volume (Units).

List of Companies Covered in this Report:

- Shurgard Self-Storage SA

- SelfStorage Dein Lagerraum GmbH (MyPlace Self-Storage)

- Space Plus Store GmbH

- Rousselet Groupe SA (HOMEBOX)

- Pickens Selfstorage GmbH

- Lagerbox Holding GmbH and Co. KG

- 1BOX Deutschland GmbH

- Storebox Holding GmbH

- ZeitLager GmbH

- XXLAGER Selfstorage GmbH

- BOXIE24 Deutschland GmbH

- Hertling GmbH and Co. KG

- Lanzell Spezialtransporte GmbH

- Klassik Umzuge GmbH

- KingBox Self-Storage GmbH

- CityBox24 GmbH

- CubeStorage Deutschland GmbH

- Jojo-Lagerhaus GmbH

- Easy-Selfstorage GmbH

- Container Self-Storage AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanisation and shrinking average dwelling size

- 4.2.2 Growth in e-commerce and SME inventory needs

- 4.2.3 Higher residential mobility among students and professionals

- 4.2.4 Surge in home renovations amid ageing housing stock

- 4.2.5 Insurance discounts for off-site storage of high-value goods

- 4.2.6 PropTech-enabled unmanned facility operations

- 4.3 Market Restraints

- 4.3.1 Restrictive zoning and land-use permits

- 4.3.2 Escalating urban land and construction costs

- 4.3.3 Rising energy tariffs squeezing climate-controlled margins

- 4.3.4 Local "Not-In-My-Back-Yard" opposition to new sites

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

- 4.10 PESTEL Analysis

- 4.11 Key Considerations of Consumers while selecting a Self-Storage Facility

5 MARKET DYNAMICS IN GERMANY

- 5.1 Analysis of Occupancy Rates

- 5.2 Average Rental Trends

- 5.2.1 Pre-Covid and Post-Covid Market Implications

- 5.3 Profitability Analysis

- 5.3.1 Pre-Covid and Post-Covid Market Implications

- 5.4 Average Facility Size

6 MARKET SIZE AND GROWTH FORECASTS (UNITS)

- 6.1 By End-User

- 6.1.1 Personal

- 6.1.2 Business

- 6.2 By Storage Size

- 6.2.1 Small and Medium Units (less than 40 sq ft)

- 6.2.2 Large Units (above 40 sq ft)

- 6.2.3 Others (Lockers/Double-Stacked)

- 6.3 By Storage Type

- 6.3.1 Climate-Controlled

- 6.3.2 Non-Climate-Controlled

- 6.4 By Ownership Pattern

- 6.4.1 Owned

- 6.4.2 Leased

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Shurgard Self-Storage SA

- 7.4.2 SelfStorage Dein Lagerraum GmbH (MyPlace Self-Storage)

- 7.4.3 Space Plus Store GmbH

- 7.4.4 Rousselet Groupe SA (HOMEBOX)

- 7.4.5 Pickens Selfstorage GmbH

- 7.4.6 Lagerbox Holding GmbH and Co. KG

- 7.4.7 1BOX Deutschland GmbH

- 7.4.8 Storebox Holding GmbH

- 7.4.9 ZeitLager GmbH

- 7.4.10 XXLAGER Selfstorage GmbH

- 7.4.11 BOXIE24 Deutschland GmbH

- 7.4.12 Hertling GmbH and Co. KG

- 7.4.13 Lanzell Spezialtransporte GmbH

- 7.4.14 Klassik Umzuge GmbH

- 7.4.15 KingBox Self-Storage GmbH

- 7.4.16 CityBox24 GmbH

- 7.4.17 CubeStorage Deutschland GmbH

- 7.4.18 Jojo-Lagerhaus GmbH

- 7.4.19 Easy-Selfstorage GmbH

- 7.4.20 Container Self-Storage AG

8 MARKET SHARE OF KEY SELF-STORAGE OPERATORS

9 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 9.1 White-space and Unmet-Need Assessment

自助仓储市场规模、份额、趋势和预测:按储存单元规模、最终用途和地区划分,2026-2034 年

自助仓储市场规模、份额、趋势和预测:按储存单元规模、最终用途和地区划分,2026-2034 年 2026年全球自助仓储市场报告

2026年全球自助仓储市场报告 自助仓储市场:2026-2032年全球市场预测(按单位类型、租赁期限、单位面积、存取方式及最终用户划分)自助仓储及搬家服务市场:自助仓储、搬家服务、单位规模、应用、全球预测(2026-2032年)

自助仓储市场:2026-2032年全球市场预测(按单位类型、租赁期限、单位面积、存取方式及最终用户划分)自助仓储及搬家服务市场:自助仓储、搬家服务、单位规模、应用、全球预测(2026-2032年) 欧洲自助仓储:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲自助仓储:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 自助仓储市场-全球产业规模、份额、趋势、机会、预测:按应用、最终用户、地区和竞争格局划分,2021-2031年日本自助仓储市场报告(按仓储单元尺寸(小型仓储单元、中型仓储单元、大型仓储单元)、最终用途(个人、商业)和地区划分,2026-2034年)

自助仓储市场-全球产业规模、份额、趋势、机会、预测:按应用、最终用户、地区和竞争格局划分,2021-2031年日本自助仓储市场报告(按仓储单元尺寸(小型仓储单元、中型仓储单元、大型仓储单元)、最终用途(个人、商业)和地区划分,2026-2034年) 自助仓储市场规模、份额、按类型、单位规模、最终用途和地区分類的成长分析 - 产业预测,2025 年至 2032 年美国自助仓储:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)亚太地区自助仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

自助仓储市场规模、份额、按类型、单位规模、最终用途和地区分類的成长分析 - 产业预测,2025 年至 2032 年美国自助仓储:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)亚太地区自助仓储:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)