|

市场调查报告书

商品编码

1937282

南美汽车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)South America Automotive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

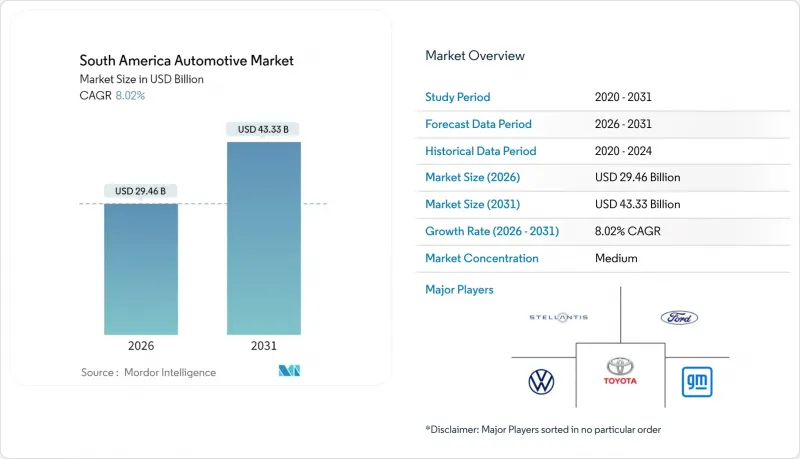

预计南美汽车市场将从 2025 年的 272.8 亿美元成长到 2026 年的 294.6 亿美元,到 2031 年将达到 433.3 亿美元,2026 年至 2031 年的复合年增长率为 8.02%。

南美汽车市场持续受惠于快速的基础设施投资、日益灵活的燃油政策(例如巴西的E30强制令)以及数位化零售平台的蓬勃发展,这些因素缩短了购买週期并扩大了消费群体。儘管不断上涨的借贷成本和半导体短缺仍构成短期不利因素,但强劲的家庭消费和不断壮大的中产阶级支撑着该地区的长期成长。日益激烈的竞争,例如Stellantis承诺到2030年投资56亿欧元,以及中国汽车製造商为规避南方共同市场不断上涨的关税而将生产本地化,正在重塑产品组合、技术应用和供应商生态系统。

南美洲汽车市场趋势与洞察

OEM厂商对区域汽车平臺的投资

在南美,传统汽车和电动车销量的成长,以及大众汽车集团和Stellantis NV等主要厂商加大投资,正在推动盈利的提升。光是Stellantis就投资了56亿欧元,创下该地区历史上单笔投资额的最高纪录。大众汽车集团为其在阿根廷的Amarq计画拨款5.8亿美元,以满足当地的运作週期需求。同时,丰田汽车公司和宝马集团也宣布了专注于混合动力和灵活燃料驱动系统的多年扩张计画。通用汽车和现代汽车的合资计划(目标是在五款车型中实现年销量80万辆)等合作项目,标誌着南美汽车市场正朝着共用分摊和产品週期加速的方向发展。这些本地化平台降低了外汇风险,符合当地监管标准,并享受南方共同市场(Mercosur)的关税优惠,从而提升了南美汽车市场的整体竞争力。

疫情后GDP復苏与消费信贷成长

预计2025年区域GDP将年增2.5%(2016年为1.9%),儘管基准利率较高,但仍将支撑家庭收入成长和汽车融资。巴西经济预计2024年将成长3.4%,失业率为6.5%,为购车创造了有利环境。阿根廷的改革已将月通膨率降至2.8%,为购车者开闢了新的融资管道。同时,哥伦比亚的製造业产出年增,进一步增强了南美汽车市场的成长动能。儘管融资成本仍然较低,但大多数央行的宽鬆货币政策预计将逐步恢復信贷管道。预计更强劲的宏观经济基本面将支撑2025年全年展示室客流量和累积订单的成长。

由于通货膨胀,融资利率高企,汽车价格也不断上涨。

巴西的政策利率(Selic)预计在2025年升至14.25%,这将推高汽车贷款利率,使购车更加困难。儘管阿根廷的通膨有所缓解,但由于披索动,贷款利差仍然较大,而本币的波动也使得进口价格前景不明朗。虽然汽车製造商目前提供贷款延期和利率补贴,但信贷渗透率仍低于疫情前水准。因此,在金融环境好转之前,南美汽车市场的短期销售可能仍将低于潜在水准。

细分市场分析

截至2025年,乘用车占南美汽车市场的73.68%,预计到2031年将以11.95%的复合年增长率增长,这主要得益于都市化和中产阶级收入的增长。 SUV和跨界车因其更高的乘坐位置和安全性而成为市场需求的主要驱动力,而紧凑型轿车则凭藉其燃油效率在汽油价格上涨的背景下保持着一定的市场份额。商用车虽然销售量较小,但却在农业和矿业走廊的物流运输中扮演重要角色。小型皮卡是巴西农场的主要交通工具,而大型卡车则是智利铜出口的主要运输工具。摩托车作为一种经济实惠的交通方式,在拥挤的大都会圈越来越受欢迎,而非公路用车则受益于公共工程支出。

Stellantis计划在2030年推出40多款新产品,其中许多产品将采用在地化平台,并相容于灵活燃料驱动系统,这将进一步增强乘用车市场的成长动能。融资促销活动旨在缓解利率上升导致的销售放缓,并维持展示室的客流量;同时,二手车平台提高了置换流动性,降低了实际更换成本,并保持了销售周转率。车辆组合凸显了南美洲汽车市场如何在个人出行需求和商务传输需求之间取得平衡。

儘管到2025年,内燃机汽车仍将占据南美汽车市场72.95%的份额,但由于财政激励措施和中国本地化生产缩小了价格差距,电池式电动车正以11.15%的复合年增长率快速增长。巴西的E30计画为灵活燃料引擎提供了成本竞争力保护,有助于减少汽油进口并提高国内乙醇需求。混合动力汽车,尤其是可使用乙醇的车型,正发挥过渡技术的作用,与汽油动力汽车相比,它们能够实现更大的排放效果。

柴油车在长途运输(跨越数千公里)中仍然扮演着重要角色,而压缩天然气(CNG)汽车则在拥有完善加气网路的市政车队中找到了自己的应用领域。燃料电池技术的研究尚处于起步阶段,但随着现代汽车宣布在巴西投资11亿美元发展氢能的蓝图,该技术正日益受到关注。预计到2026年,C级纯电动车的进口关税将提高至35%,届时,当地的电机和电池工厂将努力维持价格优势并加速普及,逐步改变南美汽车市场的动力系统结构。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 疫情后GDP復苏与消费信贷扩张

- 巴西扩大弹性燃料奖励

- 按地区分類的汽车平臺OEM投资

- 中国汽车製造商利用南方共同市场关税优惠建造待开发区电动车工厂

- 二手车平台正在促进以旧换新交易。

- 矿业特许权使用费基金补贴电动车购买

- 市场限制

- 融资利率上升和车辆价格通膨上涨

- 本地组装半导体供应的波动

- 港口拥塞导致CKD套件和电池进口延误

- 消费者对城际充电网路可靠性的不信任

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按车辆类型

- 搭乘用车

- 掀背车

- 轿车

- SUV 与跨界车

- MPV

- 商用车辆

- 轻型商用皮卡

- 轻型商用货车

- 大型卡车

- 巴士和长途汽车

- 摩托车

- 摩托车

- Scooter/轻型机踏车

- 非公路用车辆

- 农用拖拉机

- 施工机械

- 搭乘用车

- 依推进类型

- 内燃机(ICE)

- 汽油

- 柴油引擎

- 弹性燃料(乙醇)

- 天然气(CNG/LNG)

- 电动车

- 电池式电动车(BEV)

- 混合动力电动车(HEV)

- 插电式混合动力汽车(PHEV)

- 燃料电池汽车(FCEV)

- 内燃机(ICE)

- 按销售管道

- OEM/直销

- 经销商/零售

- 车队和企业销售

- 线上直接面向消费者

- 最终用户

- 个人/一般消费者

- 小型企业车队

- 企业舰队

- 政府和地方政府车队

- 出行业者(叫车、共乘)

- 按国家/地区

- 巴西

- 阿根廷

- 智利

- 秘鲁

- 哥伦比亚

- 厄瓜多

- 南美洲其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Stellantis NV

- Volkswagen AG

- General Motors Company

- Toyota Motor Corporation

- Ford Motor Company

- Hyundai Motor Company

- Nissan Motor Co. Ltd.

- Honda Motor Co. Ltd.

- Renault SA

- Mercedes-Benz Group AG

- Kia Corporation

- BYD Company Limited

- Chery Automobile Co. Ltd.

- Great Wall Motor Co. Ltd.

- Geely Automobile Holdings

- BMW AG

- Volvo Car AB

第七章 市场机会与未来展望

The South American automotive market is expected to grow from USD 27.28 billion in 2025 to USD 29.46 billion in 2026 and is forecast to reach USD 43.33 billion by 2031 at 8.02% CAGR over 2026-2031.

The South American automotive market continues to benefit from swift infrastructure spending, flexible-fuel policy enhancements such as Brazil's E30 mandate, and the proliferation of digital retail platforms that shorten purchase cycles and expand consumer reach. Elevated borrowing costs and semiconductor shortages continue to pose near-term headwinds, yet resilient household consumption and an expanding middle class underpin the region's long-term growth profile. Competitive intensity has risen as Stellantis commits EUR 5.6 billion through 2030, and Chinese OEMs localize production to avoid rising Mercosur tariffs, all of which is reshaping the product mix, technology adoption, and supplier ecosystems.

South America Automotive Market Trends and Insights

OEM Investments in Regional Vehicle Platforms

In South America, growing sales of traditional and electrified vehicles and heightened investments from major players like Volkswagen AG and Stellantis NV have increased profitability. Stellantis alone invested EUR 5.6 billion, the most significant single commitment in regional history . Volkswagen AG allocated USD 580 million to an Argentina-based Amarok program tailored to local duty-cycle needs. At the same time, Toyota Motor and BMW Group announced multi-year expansions focusing on hybrid and flex-fuel drivetrains. Joint projects such as the GM-Hyundai collaboration covering five models and targeting 800,000 annual sales illustrate a pivot toward shared cost structures and accelerated product cadence. These localized platforms reduce currency risk, meet regional regulatory norms, and leverage Mercosur tariff preferences, collectively enhancing the competitiveness of the South American automotive market.

Post-Pandemic Rebound in GDP and Consumer Credit Availability

Regional GDP is projected to increase by 2.5% in 2025, up from 1.9% the previous year, which is expected to lift household incomes and stimulate automotive lending, even as benchmark rates remain elevated . Brazil's economy expanded by 3.4% in 2024, with an unemployment rate of 6.5%, creating a supportive backdrop for vehicle purchases. Argentina's reforms have cut monthly inflation to 2.8%, unlocking new credit channels for auto buyers, while Colombia's manufacturing output is growing annually, reinforcing the momentum in the South American automotive market. Although financing costs remain restrained, easing monetary conditions across most central banks should gradually revive loan accessibility. Stronger macroeconomic fundamentals are expected to translate into higher showroom traffic and order backlogs throughout 2025.

Elevated Financing Rates and Inflation-Driven Vehicle Prices

Brazil's Selic rate climbed to 14.25% in 2025, pushing automotive loan coupons as high as and squeezing affordability. Although Argentina's inflation has moderated, peso volatility keeps lending spreads wide, while regional currency fluctuations cloud import-price visibility. OEMs now offer tenures and subsidized rates, but credit penetration still lags pre-pandemic norms. Consequently, near-term volumes in the South American automotive market may undershoot potential until monetary conditions ease.

Other drivers and restraints analyzed in the detailed report include:

- Chinese OEM Green-Field EV Plants Using Mercosur Tariff Breaks

- Digitally Enabled Used-Car Platforms Boosting Trade-Ins

- Semiconductor Supply Volatility for Local Assembly

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars accounted for 73.68% of the South American automotive market size in 2025 and are projected to expand at a 11.95% CAGR through 2031, benefiting from rising urbanization and middle-class income gains. SUVs and crossovers lead the surge, prized for higher seating positions and perceived safety, whereas compact sedans preserve a foothold due to fuel efficiency at premium pump prices. Though smaller in unit terms, commercial vehicles underpin logistics in agriculture and mining corridors, with light pickups favored by Brazilian farms and heavy trucks powering Chilean copper exports. Two-wheelers are proliferating in congested megacities as cost-effective mobility, while off-highway equipment enjoys tailwinds from public works spending.

The passenger-car momentum is reinforced by Stellantis' plan to launch more than 40 new products by 2030, many of them on localized platforms geared to flexible-fuel drivetrains. Financing promotions aim to mitigate loan-rate headwinds that otherwise dampen showroom traffic. Meanwhile, used-car digital platforms improve trade-in liquidity, lowering the effective upgrade cost and sustaining turnover. The vehicle-type mix underscores how the South American automotive market balances personal-mobility aspirations with commercial transport imperatives.

Internal-combustion engines retained 72.95% of the South American automotive market in 2025; however, battery electrics are accelerating at a 11.15% CAGR as fiscal incentives and localized Chinese production narrow the price gaps. Brazil's E30 scheme provides a cost-parity hedge for flex-fuel engines, reducing gasoline imports and increasing domestic ethanol demand. Hybrids serve as a bridge technology, especially ethanol-compatible variants that achieve greater emission reductions compared to gasoline equivalents.

Diesel retains relevance in heavy-duty routes that span thousands of kilometers, while CNG finds niche use in municipal fleets where refueling networks exist. Fuel-cell exploration is nascent but gaining attention following Hyundai's USD 1.1 billion hydrogen roadmap for Brazil. As import tariffs on C-segment BEVs rise to 35% by 2026, localized motor and battery plants are expected to protect affordability and accelerate adoption, gradually shifting the propulsion landscape of the South American automotive market.

The South America Automotive Market Report is Segmented by Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers, and Off-Highway Vehicles), Propulsion Type (Internal-Combustion Engine and Electrified Vehicles), Sales Channel (OEM/Direct, Dealer/Retail, and More), End User (Individual/Private, SME Fleets, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Stellantis NV

- Volkswagen AG

- General Motors Company

- Toyota Motor Corporation

- Ford Motor Company

- Hyundai Motor Company

- Nissan Motor Co. Ltd.

- Honda Motor Co. Ltd.

- Renault S.A.

- Mercedes-Benz Group AG

- Kia Corporation

- BYD Company Limited

- Chery Automobile Co. Ltd.

- Great Wall Motor Co. Ltd.

- Geely Automobile Holdings

- BMW AG

- Volvo Car AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-Pandemic Rebound in GDP and Consumer Credit Availability

- 4.2.2 Expansion of Flexible-Fuel Incentives in Brazil

- 4.2.3 OEM Investments in Regional Vehicle Platforms

- 4.2.4 Chinese OEM Green-Field EV Plants Using Mercosur Tariff Breaks

- 4.2.5 Digitally Enabled Used-Car Platforms Boosting Trade-Ins.

- 4.2.6 Mining-Royalty Funded EV Purchase Subsidies

- 4.3 Market Restraints

- 4.3.1 Elevated Financing Rates and Inflation-Driven Vehicle Prices

- 4.3.2 Semiconductor Supply Volatility for Local Assembly

- 4.3.3 Port Congestion Delaying CKD Kits and Battery Imports

- 4.3.4 Consumer Distrust in Inter-City Charging-Network Reliability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.1.1 Hatchbacks

- 5.1.1.2 Sedans

- 5.1.1.3 SUVs and Crossovers

- 5.1.1.4 MPVs

- 5.1.2 Commercial Vehicles

- 5.1.2.1 Light Commercial Pick-ups

- 5.1.2.2 Light Commercial Vans

- 5.1.2.3 Heavy Trucks

- 5.1.2.4 Buses and Coaches

- 5.1.3 Two-Wheelers

- 5.1.3.1 Motorcycles

- 5.1.3.2 Scooters/Mopeds

- 5.1.4 Off-Highway Vehicles

- 5.1.4.1 Agricultural Tractors

- 5.1.4.2 Construction Equipment

- 5.1.1 Passenger Cars

- 5.2 By Propulsion Type

- 5.2.1 Internal-Combustion (ICE)

- 5.2.1.1 Gasoline

- 5.2.1.2 Diesel

- 5.2.1.3 Flexible-Fuel (Ethanol)

- 5.2.1.4 Natural Gas (CNG/LNG)

- 5.2.2 Electrified Vehicles

- 5.2.2.1 Battery-Electric (BEV)

- 5.2.2.2 Hybrid Electric (HEV)

- 5.2.2.3 Plug-in Hybrid (PHEV)

- 5.2.2.4 Fuel-Cell (FCEV)

- 5.2.1 Internal-Combustion (ICE)

- 5.3 By Sales Channel

- 5.3.1 OEM / Direct Sales

- 5.3.2 Dealer and Retail Sales

- 5.3.3 Fleet and Corporate Sales

- 5.3.4 Online Direct-to-Consumer

- 5.4 By End User

- 5.4.1 Individual / Private Consumers

- 5.4.2 Small and Medium Enterprise Fleets

- 5.4.3 Large Corporate Fleets

- 5.4.4 Government and Municipal Fleets

- 5.4.5 Mobility Operators (Ride-hailing, Car-sharing)

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Chile

- 5.5.4 Peru

- 5.5.5 Colombia

- 5.5.6 Ecuador

- 5.5.7 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 Stellantis NV

- 6.4.2 Volkswagen AG

- 6.4.3 General Motors Company

- 6.4.4 Toyota Motor Corporation

- 6.4.5 Ford Motor Company

- 6.4.6 Hyundai Motor Company

- 6.4.7 Nissan Motor Co. Ltd.

- 6.4.8 Honda Motor Co. Ltd.

- 6.4.9 Renault S.A.

- 6.4.10 Mercedes-Benz Group AG

- 6.4.11 Kia Corporation

- 6.4.12 BYD Company Limited

- 6.4.13 Chery Automobile Co. Ltd.

- 6.4.14 Great Wall Motor Co. Ltd.

- 6.4.15 Geely Automobile Holdings

- 6.4.16 BMW AG

- 6.4.17 Volvo Car AB

7 Market Opportunities & Future Outlook

撒哈拉以南非洲汽车市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)非洲汽车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)北美汽车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

撒哈拉以南非洲汽车市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)非洲汽车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)北美汽车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 越南汽车涂料市场(2025)中国的汽车用涂料市场(2025年)印尼的汽车用涂料市场(2025年)印度的汽车用涂料市场:2025年日本的汽车用涂料市场:2025年美国的汽车用涂料市场(2025年)

越南汽车涂料市场(2025)中国的汽车用涂料市场(2025年)印尼的汽车用涂料市场(2025年)印度的汽车用涂料市场:2025年日本的汽车用涂料市场:2025年美国的汽车用涂料市场(2025年) 汽车市场-全球产业规模、份额、趋势、机会和预测(按车型、推进类型、地区和竞争情况划分,2020-2030 年预测)

汽车市场-全球产业规模、份额、趋势、机会和预测(按车型、推进类型、地区和竞争情况划分,2020-2030 年预测)