|

市场调查报告书

商品编码

1938978

网路安全:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

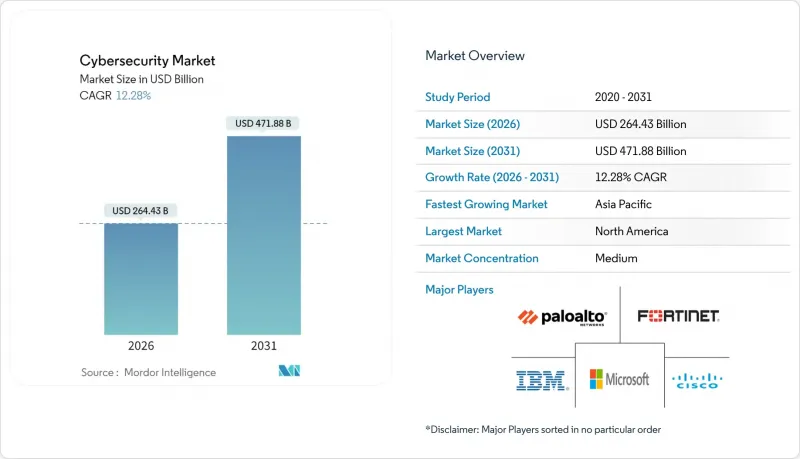

预计到 2026 年,网路安全市场规模将达到 2,644.3 亿美元,高于 2025 年的 2,355 亿美元。

预计到 2031 年将达到 4,718.8 亿美元,2026 年至 2031 年的复合年增长率为 12.28%。

这一成长主要受零信任架构投入增加、IT与操作技术(OT)防御整合以及量子加密准备工作的推动。北美仍保持其支出主导地位,而亚太地区则经历了最快的成长,因为企业正将工作负载迁移到云端优先环境。此外,由于网路保险承保人要求检验的控制措施,预算拨款也在增加,促使企业转向能够简化监控的整合安全平台。同时,随着供应商竞相应对新的攻击手法,透过併购的平台整合也不断增加。

全球网路安全市场趋势与洞察

加速云端优先的数位转型

随着分散式环境中边界控制失效,云端迁移正在重新调整安全投资的优先顺序。云端采用率持续成长,超过了本地部署的配置,并推动了对整合身分、工作负载和资料保护功能的云端原生应用程式保护平台的需求。企业正在寻求统一的主机来减少工具的冗余,而供应商则透过提供能够关联混合环境中遥测资料的平台来回应这一需求,从而提高可见性和回应效率。

关键基础设施中IT与OT安全的整合

工业4.0的推进正将传统上与空气间隙的系统接入网络,使传统控製网络暴露于与攻击IT资产相同的攻击者之下。这推动了网路安全市场的需求。诸如ISA/IEC 62443等法规结构要求建构从工厂车间到资料中心的整合防御体系,从而促进了对专用OT威胁侦测和隔离工具的投资。随着国家级骇客对电网漏洞的侦测,能源供应商正主导这一趋势,而OT专用安全措施带来的风险降低效益也超过了同类IT计划。

网路安全人才短缺和薪资上涨

网路安全专业人员短缺340万人,加之云端运算、营运技术(OT)和人工智慧驱动的防御等稀缺技能人才薪资不断上涨,令预算捉襟见肘。这种限制因素正推动市场整合,转向专业人员需求较少的平台,同时也为提供资安管理服务和人工智慧自动化工具的供应商创造了机会。此外,网路安全专业人员的高离职率也加剧了这一局面,64%的网路安全专业人员因工作压力过大而考虑换工作。这导致招募和培训成本不断攀升,持续影响企业的安全预算。

区域分析

北美地区拥有成熟的法规环境和许多主要供应商,预计到2025年将占全球网路安全市场收入的43.20%。受第14028号行政命令下广泛推行的零信任政策的推动,该地区到2027年的网路安全支出预计将超过1,376亿美元。 2023年,美国共发生9,036起网路安全事件,远超欧洲的2557起,这持续推动了对高阶威胁情报和託管安全营运中心(SOC)服务的需求。加拿大和墨西哥正透过公私合作项目,协调跨境外洩报告和事件回应,为市场成长做出贡献。

亚太地区以16.85%的复合年增长率 (CAGR) 实现最快增长,各国主导的数位化国家计划将网路安全提升至关键基础设施层级。中国、印度、日本和韩国已为国家网路安全战略拨出多年预算,而澳洲和纽西兰则实施了全面的弹性框架,强制要求揭露安全事件。该地区的买家通常从一开始就采用云端原生安全,从而跳过传统的控制措施,加速采用以身分为中心和人工智慧驱动的分析技术。

欧洲的成长主要得益于GDPR和NIS2指令的实施,后者将适用范围扩大到更多产业。德国、英国和法国是主要的支出国,而中东欧市场则在适应欧盟要求的过程中,从小规模的基数上成长。法国和西班牙的主权云端计画刺激了对本土託管安全架构的需求,而跨境资料传输限制则加速了隐私增强加密技术的普及。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 市场定义与研究假设

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 借助云端优先加速数位转型

- 关键基础设施中IT与OT安全的整合

- 混合型劳动力的零信任架构要求

- 网路保险承保要求激增

- 数位主权监管促进区域化安全架构

- 抗量子密码技术过渡时间表

- 市场限制

- 网路安全人才短缺和薪资上涨

- 与传统基础设施整合的复杂性

- API 的激增增加了攻击面的复杂性。

- SOC警报疲劳与误报超限投资回报率

- 价值链分析

- 重要法规结构评估

- 关键相关人员影响评估

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 主要用例和案例研究

- 定价及定价模式分析

- 网路安全培训趋势

- 宏观经济因素的影响

第五章 市场规模与成长预测

- 报价

- 解决方案

- 应用程式安全

- 云端安全

- 资料安全

- 身分和存取管理

- 基础设施保护

- 综合风险管理

- 网路安全

- 端点安全

- 服务

- 专业服务

- 託管服务

- 解决方案

- 透过部署模式

- 云

- 本地部署

- 按最终用户行业划分

- BFSI

- 卫生保健

- 资讯科技和电信

- 工业与国防

- 零售与电子商务

- 能源与公共产业

- 製造业

- 其他的

- 最终用户公司规模

- 大公司

- 中小企业

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- CrowdStrike Holdings, Inc.

- Trend Micro Incorporated

- Zscaler, Inc.

- Okta, Inc.

- Gen Digital Inc.(formerly NortonLifeLock Inc.)

- Sophos Limited

- Proofpoint, Inc.

- McAfee LLC

- Darktrace plc

- Rapid7, Inc.

- SentinelOne, Inc.

- Imperva, Inc.

- Qualys, Inc.

- Trellix Holdings LLC

- Splunk Inc.

- Elastic NV

- Akamai Technologies, Inc.

- Broadcom Inc.(Symantec Enterprise Division)

- VMware, Inc.

- Cybereason

- Ivanti, Inc.

- Tenable Holdings, Inc.

- CyberArk Software Ltd.

第七章 市场机会与未来趋势

- 评估差距和未满足的需求

Cybersecurity Market size in 2026 is estimated at USD 264.43 billion, growing from 2025 value of USD 235.5 billion with 2031 projections showing USD 471.88 billion, growing at 12.28% CAGR over 2026-2031.

Increased spending on zero-trust architectures, the integration of IT and operational technology (OT) defenses, and preparations for quantum-ready encryption are the primary forces behind this expansion. North America retains spending leadership, while Asia-Pacific registers the most rapid gains as enterprises migrate workloads to cloud-first environments. Budget allocations are also rising as cyber-insurance underwriters demand verifiable controls, pushing organizations toward unified security platforms that simplify oversight. Simultaneously, platform consolidation through mergers and acquisitions is intensifying as vendors race to cover emerging threat vectors.

Global Cybersecurity Market Trends and Insights

Accelerated Cloud-First Digital Transformation

Cloud migration is reshaping security investment priorities as perimeter controls fail in distributed environments. Cloud deployment is growing, outpacing on-premise allocations and driving demand for cloud-native application protection platforms that integrate identity, workload, and data safeguards. Enterprises are seeking unified consoles to reduce tool sprawl, and vendors are responding with platforms that correlate telemetry across hybrid estates, improving visibility and response efficiency .

IT-OT Security Convergence Across Critical Infrastructure

Industry 4.0 forces formerly air-gapped systems online, exposing legacy control networks to the same adversaries that target IT assets, driving heightened demand in the cybersecurity market. Regulatory frameworks such as ISA/IEC 62443 now require integrated defenses that span production floors and data centers, encouraging investment in specialized OT threat detection and segmentation tools. Energy utilities are leading adoption as nation-state actors probe grid vulnerabilities, and returns on OT-focused security initiatives now exceed comparable IT projects in risk-reduction value.

Cyber-Security Talent Deficit and Wage Inflation

The shortfall of 3.4 million professionals strains budgets as salaries climb for scarce skills in cloud, OT, and AI-driven defense. This constraint is driving market consolidation toward platforms that require fewer specialized personnel to operate, while simultaneously creating opportunities for vendors offering managed security services and AI-powered automation tools. The situation is exacerbated by high turnover rates, with 64% of cybersecurity professionals considering job changes due to workload stress, creating a continuous cycle of recruitment and training costs that impact organizational security budgets .

Other drivers and restraints analyzed in the detailed report include:

- Zero-Trust Architecture Mandates for Hybrid Workforce

- Surge in Cyber-Insurance Underwriting Requirements

- Integration Complexity with Legacy Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Geography Analysis

North America controlled 43.20% of 2025 revenue in the cybersecurity market, underpinned by mature regulations and the presence of major vendors. Regional spending is forecast to surpass USD 137.6 billion by 2027 as Executive Order 14028 obliges extensive zero-trust migration. The United States reported 9,036 cyber incidents in 2023, dwarfing Europe's 2,557 events and sustaining demand for advanced threat intelligence feeds and managed SOC services. Canada and Mexico contribute to growth through joint public-private programs that harmonise cross-border breach reporting and incident response.

Asia-Pacific is the fastest-growing area at 16.85% CAGR, with state-backed digital-nation plans elevating security to critical-infrastructure status. China, India, Japan, and South Korea allocate multi-year budgets to national cyber strategies, while Australia and New Zealand implement comprehensive resilience frameworks that require mandatory incident disclosure. Regional buyers often leapfrog legacy controls by adopting cloud-native security from the outset, accelerating uptake of identity-centric and AI-driven analytics.

Europe region growth is propelled by GDPR enforcement and the forthcoming NIS2 directive that expands coverage to more sectors. Germany, the United Kingdom, and France headline spending, whereas Central and Eastern European markets grow from a smaller base as they align with EU requirements. Sovereign-cloud initiatives in France and Spain stimulate demand for domestically hosted security stacks, while cross-border data-transfer restrictions accelerate adoption of privacy-enhancing encryption techniques.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- CrowdStrike Holdings, Inc.

- Trend Micro Incorporated

- Zscaler, Inc.

- Okta, Inc.

- Gen Digital Inc. (formerly NortonLifeLock Inc.)

- Sophos Limited

- Proofpoint, Inc.

- McAfee LLC

- Darktrace plc

- Rapid7, Inc.

- SentinelOne, Inc.

- Imperva, Inc.

- Qualys, Inc.

- Trellix Holdings LLC

- Splunk Inc.

- Elastic N.V.

- Akamai Technologies, Inc.

- Broadcom Inc. (Symantec Enterprise Division)

- VMware, Inc.

- Cybereason

- Ivanti, Inc.

- Tenable Holdings, Inc.

- CyberArk Software Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated cloud-first digital transformation

- 4.2.2 IT-OT security convergence across critical infrastructure

- 4.2.3 Zero-trust architecture mandates for hybrid workforce

- 4.2.4 Surge in cyber-insurance underwriting requirements

- 4.2.5 Digital-sovereignty regulations driving localised security stacks

- 4.2.6 Timelines for quantum-ready cryptography migration

- 4.3 Market Restraints

- 4.3.1 Cyber-security talent deficit and wage inflation

- 4.3.2 Integration complexity with legacy infrastructure

- 4.3.3 API-sprawl expanding attack-surface complexity

- 4.3.4 SOC alert-fatigue and false-positive overload limiting ROI

- 4.4 Value Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Key Use Cased and Case Studies

- 4.10 Analysis of Pricing and Pricing Model

- 4.11 Cybersecurity Training Trends

- 4.12 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security

- 5.1.1.8 End-point Security

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By End-user Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Retail and E-commerce

- 5.3.6 Energy and Utilities

- 5.3.7 Manufacturing

- 5.3.8 Others

- 5.4 By End-user Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Palo Alto Networks, Inc.

- 6.4.5 Fortinet, Inc.

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 CrowdStrike Holdings, Inc.

- 6.4.8 Trend Micro Incorporated

- 6.4.9 Zscaler, Inc.

- 6.4.10 Okta, Inc.

- 6.4.11 Gen Digital Inc. (formerly NortonLifeLock Inc.)

- 6.4.12 Sophos Limited

- 6.4.13 Proofpoint, Inc.

- 6.4.14 McAfee LLC

- 6.4.15 Darktrace plc

- 6.4.16 Rapid7, Inc.

- 6.4.17 SentinelOne, Inc.

- 6.4.18 Imperva, Inc.

- 6.4.19 Qualys, Inc.

- 6.4.20 Trellix Holdings LLC

- 6.4.21 Splunk Inc.

- 6.4.22 Elastic N.V.

- 6.4.23 Akamai Technologies, Inc.

- 6.4.24 Broadcom Inc. (Symantec Enterprise Division)

- 6.4.25 VMware, Inc.

- 6.4.26 Cybereason

- 6.4.27 Ivanti, Inc.

- 6.4.28 Tenable Holdings, Inc.

- 6.4.29 CyberArk Software Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment

网路安全软体和服务市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署模式、最终用户和解决方案划分

网路安全软体和服务市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署模式、最终用户和解决方案划分 物联网网路安全标籤市场(按最终用途、应用、组件和部署类型划分),全球预测(2026-2032 年)

物联网网路安全标籤市场(按最终用途、应用、组件和部署类型划分),全球预测(2026-2032 年) 社交工程攻击防御解决方案市场规模、份额和成长分析:按组件、部署模式、组织规模、最终用户、地区和行业预测,2026-2033 年

社交工程攻击防御解决方案市场规模、份额和成长分析:按组件、部署模式、组织规模、最终用户、地区和行业预测,2026-2033 年 无人机网路安全市场规模、份额和成长分析(按组件、无人机类型、网路安全解决方案、应用、最终用户、部署模式和地区划分)—2026-2033年产业预测区块链网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

无人机网路安全市场规模、份额和成长分析(按组件、无人机类型、网路安全解决方案、应用、最终用户、部署模式和地区划分)—2026-2033年产业预测区块链网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 亚太网路安全:市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡网路安全:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国网路安全:市场占有率分析、产业趋势与统计、成长预测(2026-2031)网路安全软体:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

亚太网路安全:市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡网路安全:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国网路安全:市场占有率分析、产业趋势与统计、成长预测(2026-2031)网路安全软体:市场占有率分析、产业趋势与统计、成长预测(2026-2031)