|

市场调查报告书

商品编码

1940701

应征者追踪系统:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Applicant Tracking System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

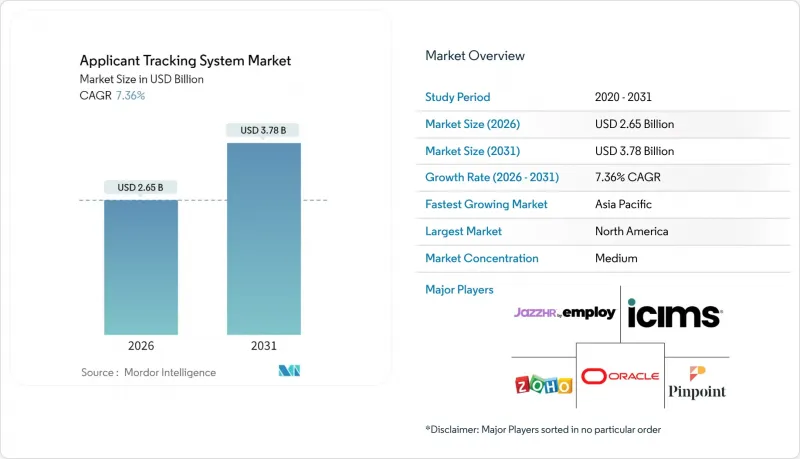

预计到 2026 年,求职者追踪系统市场价值将达到 26.5 亿美元,从 2025 年的 24.7 亿美元成长到 2031 年的 37.8 亿美元。

预计从 2026 年到 2031 年,其复合年增长率将达到 7.36%。

这一成长轨迹反映了企业以自动化工作流程取代人工招募流程的当前趋势,旨在加快招募速度并改善候选人体验。人才短缺、合规成本上升以及远距办公的激增推动了这一需求,使得随时随地招募成为一项策略重点。云端技术的采用正在推动这一扩张,基于订阅的授权模式降低了小规模团队的进入门槛,同时支援需要全天候运作的大规模全球部署。人工智慧 (AI) 的加入——简历解析、互动式聊天机器人和偏见筛检——正成为企业选择供应商的决定性因素,因为企业正在寻求能够随业务週期扩展的数据驱动型招聘。因此,应征者追踪系统 (ATS) 市场正在从利基人力资源软体转型为企业数位化架构的核心支柱,为那些在单一平台上整合 ATS、HCM 和人才智慧的供应商创造了新的机会。

全球应征者追踪系统市场趋势与洞察

招募流程自动化的需求日益增长

随着招募量的成长超过了人工筛检能力,企业被迫实施工作流程自动化,以将决策週期从数週缩短至数天。在2025财年,Workday的订阅收入年增16.9%,因为客户寻求能够整合日程安排、背景调查和入职流程的端到端人才管道。医疗保健机构就是这项转变的典型例子。美国一家大型医疗系统实施了基于规则的筛选和自动通讯,以便在每个阶段通知候选人他们的进展情况,最终节省了7300万美元的招聘机构费用。随着招募成本的上升,经营团队将ATS(申请人追踪系统)的延迟视为资产负债表问题,而非人力资源上的麻烦。因此,申请人追踪系统市场正在评估那些能够自动筛选履历、实现即时沟通并利用机器学习评分来识别最佳候选人的供应商。

多元化人才招募显着成长

由于多元化团队在创新指标上表现较佳,多元化专案已从合规性转向以营收为导向的优先事项。 Greenhouse 的客户在实施结构化职位评估和匿名回馈机制后,2024 年多元化、公平和包容性 (DEI) 目标达成率提高了 56%。 HireVue 透过将演算法偏见检测融入视讯评估,帮助一家英国银行实现了 50/50 的性别平等,这充分展现了技术驱动的公平性与品牌价值之间的联繫。因此,负责人期望 ATS 平台能够监控候选人的人口统计资料、标记带有偏见的问题,并记录面试官的回馈以供审核。面对日益增长的监管压力,「可解释性仪錶板」(用于向监管机构解释人工智慧模型如何避免歧视)已成为申请人追踪系统市场的差异化优势。

缺乏技术专长和整合复杂性

企业往往低估了将ATS工作流程与薪资核算系统、ERP和身分管理系统整合所需的资源,导致实施停滞不前,功能也未能充分利用。 Atlas MedStaff必须外包给专业的中介软体供应商来整合NetSuite和Bullhorn,这表明资料模型不相容会如何加剧预算压力并延缓投资回报。随着供应商引入需要持续调整和偏差审核的AI演算法,技能差距进一步扩大。对于没有专职技术人员的中小型企业而言,复杂的平台过于庞大,迫使它们转向不支援长期扩充性的简化工具,从而限制了应征者追踪系统市场的成长。

细分市场分析

到2025年,解决方案类别将以61.20%的市场份额引领市场,因为企业倾向于选择功能齐全的套件,这些套件能够全面涵盖职位创建、人才搜寻、评估和入职等环节。然而,服务领域预计将以11.02%的复合年增长率成长,成为成长最快的领域,这反映出整合知识和变革管理技能方面的差距正在扩大。到2031年,实施和支援领域的成长速度预计将超过授权收入,因为企业越来越重视合作伙伴在满足监管、品牌和分析目标方面的专业知识。供应商正在扩展其服务范围,涵盖资料清洗、演算法检验和持续用户体验测试,以确保客户能够从其人工智慧附加元件中获得可衡量的成果。随着人工智慧技术的应用遍及全球,全天候託管服务已成为一项基本要求,服务深度正成为一项竞标标准,即使对于以产品为中心的供应商也是如此。

第二波买家,包括中型製造企业和非营利组织,正在签署多年期託管服务协议,以缓解IT瓶颈。这促使ATS供应商与全球系统整合商建立新的联盟,将迁移蓝图、人力资源咨询和区域合规方案打包提供。同时,专注于人工智慧偏见审核和GDPR差距分析的纯粹顾问公司正在涌现,目标客户是金融和医疗保健行业中规避风险的客户。因此,申请人追踪系统市场中,用于降低复杂实施风险和确保经营团队KPI的服务支出占比越来越高。

云端服务占了77.35%的市场份额,并以9.68%的复合年增长率保持最快增长,这印证了订阅式託管已成为现代标准。企业优先考虑即时配置、自动修补程式和行动访问,以便负责人能够跨时区访问。随着混合办公和远距办公模式的普及,随时随地招聘已成为常态,与云端订阅相关的应征者追踪系统市场规模预计将会扩大。持续交付管道使供应商能够按季度推送人工智慧更新,让客户无需进行内部升级计划即可持续满足合规性要求。

在国防、公共部门和受资料主权法律约束的金融机构中,本地部署仍然普遍存在,但随着加密技术和区域託管降低了云端采用的门槛,这一领域正在萎缩。多租户设计也使曾经仅限于大型企业的高阶分析功能大众化,使小型企业也能进入应征者追踪系统市场。随着传统ATS系统即将到期,采购团队正在权衡伺服器、修补程式和专业人员等生命週期人事费用与云端订阅套餐,从而加速了迁移进程。

应征者追踪系统市场按产品类型(解决方案、服务(整合和维护))、部署模式(云端、本地部署)、最终用户行业垂直领域(运输和物流(包括仓储)、银行、金融和保险 (BFSI) 及其他)、组织规模(中小企业、大型企业)和地区进行细分。市场预测以美元计价。

区域分析

北美地区在2025年仍保持领先地位,市占率达37.45%,这主要得益于美国和加拿大企业早期采用基于云端的人力资源管理套件,他们现在已将人工智慧驱动的招聘视为标准做法。财富500强企业的统计数据显示,Workday Recruiting已超越Taleo,成为采用率最高的ATS(申请人追踪系统),显示ATS正处于持续更新迭代阶段,并强调持续交付架构。科罗拉多的人工智慧法案等法规日益关注演算法透明度,推动了系统升级,使其包含同意书、可解释性报告和资料保存管理功能。因此,儘管在这个成熟地区新用户成长放缓,但申请人追踪系统市场仍保持着稳定的许可证续约和模组新增。

随着企业适应GDPR、欧盟人工智慧法规以及各国特定的公平招募法律,欧洲正经历个位数的温和成长。供应商透过提供多语言介面、文件保留规则以及能够经受监管审查的审核系统来脱颖而出。英国后的企业重组正在推动该地区ATS市场规模的成长。随着跨国人才流动日益复杂,雇主正在实现合格审查的自动化。一些成功减少偏见的案例,例如英国一家零售银行将评估偏见减少了90%,证明了合规性和绩效提升相结合所带来的投资回报。

亚太地区预计将以11.62%的复合年增长率成为全球成长最快的地区。数位转型计画和云端基础设施的快速普及为求职者追踪系统(ATS)市场提供了巨大的成长潜力。一家总部位于新加坡的银行透过互动式人工智慧将招募週期缩短了一半,显着提高了效率。一家人力资源科技Start-Ups获得了740万美元的创业投资投资,这表明投资者对该地区的需求充满信心。中国和印度正在透过行动优先的工作流程实现校园招募的现代化,而日本则利用人工智慧排班来缓解人口结构变化带来的劳动力短缺问题。跨境电子商务的快速成长正在推动东南亚中小企业迅速采用基于SaaS的ATS,巩固了亚太地区作为2031年前关键成长引擎的地位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 招募流程自动化的需求日益增长

- 多元化人才招募显着成长

- 加速采用云端为基础的人力资源套件

- 利用人工智慧实现候选人体验个人化

- 将ATS与零工平台集成

- 审核工作流程的合规性要求

- 市场限制

- 缺乏技术专长和整合复杂性

- 资料隐私和GDPR合规性问题

- 演算法偏差监管措施会增加检验成本

- 内部人才市场将蚕食ATS的使用率。

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济影响评估

- 关键招募流程指标

第五章 市场规模与成长预测

- 报价

- 解决方案

- 服务(整合和维护)

- 透过部署模式

- 云

- 本地部署

- 按最终用户行业划分

- 运输和物流(包括仓储业)

- 银行、金融服务和保险(BFSI)

- 资讯科技与通讯

- 卫生保健

- 零售与电子商务

- 其他行业

- 按公司规模

- 中小企业

- 大公司

- 按地区

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 亚太地区

- 中国

- 印度

- 日本

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 非洲

- 南非

- 肯亚

- 南美洲

- 巴西

- 阿根廷

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Oracle Corporation

- Workday Inc.

- SAP SE(SuccessFactors)

- iCIMS Inc.

- Greenhouse Software Inc.

- JazzHR(Employ Inc.)

- Zoho Corporation Pvt. Ltd.

- Bamboo HR LLC

- Ceipal Corp.

- Pinpoint HQ Ltd.

- SmartRecruiters Inc.

- Lever Inc.

- Jobvite LLC

- Bullhorn Inc.

- Recruitee BV

- Breezy HR Inc.

- ADP LLC(Recruiting Management)

- UKG Inc.(UKG Pro Recruiting)

- IBM Corporation(Kenexa BrassRing)

- ClearCompany Talent Management

第七章 市场机会与未来展望

The applicant tracking system market size in 2026 is estimated at USD 2.65 billion, growing from 2025 value of USD 2.47 billion with 2031 projections showing USD 3.78 billion, growing at 7.36% CAGR over 2026-2031.

This trajectory captures how enterprises are replacing manual hiring with automated workflows that cut time-to-fill and improve candidate experiences. Demand stems from talent shortages, rising compliance costs, and the surge in remote work that makes location-agnostic recruitment a strategic priority. Cloud deployment anchors this expansion because subscription licensing lowers barriers for small teams while supporting large global rollouts that need round-the-clock uptime. Artificial-intelligence add-ons-resume parsing, conversational chatbots, bias screening-now decide vendor selection as companies look for data-driven hiring that scales with business cycles. As a result, the applicant tracking system market is moving from niche HR software to a core pillar of enterprise digital architecture, creating room for vendors that combine ATS, HCM, and talent intelligence on a single platform.

Global Applicant Tracking System Market Trends and Insights

Rising Need to Automate Recruitment Processes

Recruiting volumes are outpacing the capacity of manual screens, prompting firms to embed workflow automation that shortens decision cycles from weeks to days. Subscription revenue at Workday climbed 16.9% year-on-year in fiscal 2025 because clients demanded end-to-end talent pipelines that integrate scheduling, background checks, and onboarding. Healthcare providers illustrate the shift: a major US system cut agency fees by USD 73 million after introducing rules-based filtering and automated messaging that kept candidates informed at each stage. With vacancy costs rising, executives now view ATS latency as a balance-sheet issue rather than an HR inconvenience. Accordingly, the applicant tracking system market rewards vendors that can automate resume triage, communicate instantly, and surface best-fit applicants with machine-learning scoring.

Significant Growth in Diverse Talent Acquisition

Diversity programs have transitioned from compliance exercises to revenue-linked priorities because heterogeneous teams outperform on innovation metrics. Greenhouse clients recorded a 56% rise in DEI target achievement in 2024 after adopting structured job scoring and anonymized feedback loops. HireVue helped a UK bank equalize gender splits to 50/50 by embedding algorithmic bias detection in video assessments, proving the link between tech-enabled fairness and brand equity. Buyers therefore expect ATS platforms to monitor demographic pipelines, flag biased questions, and log interviewer feedback for audit. As legislation tightens, the applicant tracking system market differentiates on explainability dashboards that show regulators how AI models avoid discrimination.

Limited Technical Expertise & Integration Complexity

Enterprises underestimate the resources needed to mesh ATS workflows with payroll, ERP, and identity-management systems, leading to stalled rollouts and underused features. Atlas Medstaff had to contract specialist middleware to bridge NetSuite with Bullhorn, highlighting how data-model mismatches can drain budgets and delay ROI. Skills gaps intensify as vendors embed AI algorithms that demand continuous tuning and bias audits. For SMEs without dedicated tech staff, complex platforms can prove overwhelming, pushing them toward stripped-down tools that may not support long-term scalability, thus tempering applicant tracking system market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Adoption of Cloud-Based HR Suites

- AI-Driven Candidate-Experience Personalisation

- Data-Privacy & GDPR Compliance Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The solutions category dominated 2025 with 61.20% share as firms selected full-function suites to cover requisition creation, sourcing, assessment, and onboarding. Services, however, post the quickest rise at 11.02% CAGR, reflecting widening gaps in integration know-how and change-management skills. The applicant tracking system market size for implementation and support is projected to grow faster than license revenue through 2031 because enterprises now value partner expertise that aligns configuration with regulatory, branding, and analytics objectives. Vendors extend service lines to cover data cleansing, algorithm validation, and continuous UX testing, ensuring customers extract measurable outcomes from AI add-ons. As deployments stretch across continents, 24/7 managed services become non-negotiable, making service depth a tender-winning criterion even for product-centric providers.

Second-wave buyers, including mid-market manufacturers and non-profit organizations, sign multi-year managed-service contracts to mitigate IT bottlenecks. This sparks new alliances between ATS vendors and global system integrators that bundle migration roadmaps, talent advisory, and local compliance packs. Meanwhile, pure-play consultants specializing in AI bias audits and GDPR gap analyses appear, targeting risk-averse finance and healthcare accounts. Consequently, the applicant tracking system market funnels a growing share of spend toward service units that de-risk complex rollouts and guarantee executive KPIs.

Cloud owns 77.35% share and still grows the quickest at 9.68% CAGR, confirming that subscription hosting is the modern default. Firms value instant provisioning, automatic patching, and mobile access for hiring managers scattered across time zones. The applicant tracking system market size tied to cloud subscriptions is forecast to widen as hybrid and remote workforces cement location-independent recruitment norms. Continuous delivery pipelines let vendors push AI updates quarterly, ensuring clients keep pace with compliance mandates without internal upgrade projects.

On-premises deployments persist in defense, public sector, and financial institutions bound by data-sovereignty statutes, yet the segment is declining as encryption and regional hosting ease cloud objections. Multitenant designs also democratize advanced analytics once limited to top-tier corporate budgets, pulling SMEs into the applicant tracking system market. As legacy ATS renewals arise, procurement teams benchmark the lifetime cost of servers, patches, and specialized staff against cloud subscription packages, accelerating migration momentum.

Applicant Tracking System Market Segmented by Offering (Solutions, Services (Integration and Maintenance)), Deployment Mode (Cloud, On-Premise), End-User Industry (Transportation and Logistics (incl. Warehouse), BFSI, and More), Organization Size (SMEs, Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 37.45% share in 2025 because US and Canadian enterprises embraced cloud HR suites early and now treat AI-enabled hiring as standard practice. Fortune 500 statistics show Workday Recruiting overtaking Taleo as the most adopted ATS, evidencing a replacement cycle favouring continuous-delivery architectures. Legislation such as Colorado's AI Act heightens focus on algorithmic transparency, driving upgrades that embed consent forms, explainability reports, and data-retention controls. The applicant tracking system market consequently sees steady license renewals and module add-ons even though new-logo growth moderates in this mature region.

Europe posts mid-single-digit growth as firms align with GDPR, the EU AI Act, and country-specific fair-hiring statutes. Vendors differentiate on multilingual interfaces, document retention rules, and audit trails that withstand regulator inspections. The applicant tracking system market size across the region is bolstered by corporate restructuring after Brexit, which complicates cross-border talent flow and prompts employers to automate eligibility checks. Bias-reduction success stories-such as a UK retail bank cutting evaluation bias by 90%-illustrate how compliance and performance converge to justify investment.

Asia-Pacific is projected to expand at 11.62% CAGR, the fastest worldwide. Digital transformation programs and leapfrogging cloud infrastructure adoption give the applicant tracking system market an outsized runway. Singapore-based banks demonstrate efficiency gains from conversational AI that halves hiring cycles, while venture capital funding-USD 7.4 million for an HR tech start-up-signals investor belief in regional demand. China and India modernize campus hiring via mobile-first workflows, and Japan leans on AI scheduling to mitigate demographic labour shortages. Southeast Asian SMEs rapidly adopt SaaS ATS as cross-border e-commerce booms, cementing APAC as the prime growth engine through 2031.

- Oracle Corporation

- Workday Inc.

- SAP SE (SuccessFactors)

- iCIMS Inc.

- Greenhouse Software Inc.

- JazzHR (Employ Inc.)

- Zoho Corporation Pvt. Ltd.

- Bamboo HR LLC

- Ceipal Corp.

- Pinpoint HQ Ltd.

- SmartRecruiters Inc.

- Lever Inc.

- Jobvite LLC

- Bullhorn Inc.

- Recruitee B.V.

- Breezy HR Inc.

- ADP LLC (Recruiting Management)

- UKG Inc. (UKG Pro Recruiting)

- IBM Corporation (Kenexa BrassRing)

- ClearCompany Talent Management

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising need to automate recruitment processes

- 4.2.2 Significant growth in diverse talent acquisition

- 4.2.3 Accelerating adoption of cloud-based HR suites

- 4.2.4 AI-driven candidate-experience personalisation

- 4.2.5 Integration of ATS with gig-workforce platforms

- 4.2.6 Compliance demand for audit-ready workflows

- 4.3 Market Restraints

- 4.3.1 Limited technical expertise and integration complexity

- 4.3.2 Data-privacy and GDPR compliance concerns

- 4.3.3 Algorithmic-bias legislation raises validation cost

- 4.3.4 Internal talent-marketplaces cannibalise ATS usage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Macroeconomic Impact Assessment

- 4.9 Key Recruitment-Process Metrics

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.2 Services (Integration and Maintenance)

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By End-User Industry

- 5.3.1 Transportation and Logistics (incl. Warehouse)

- 5.3.2 Banking, Financial Services and Insurance (BFSI)

- 5.3.3 Information Technology and Telecom

- 5.3.4 Healthcare

- 5.3.5 Retail and E-commerce

- 5.3.6 Other Industries

- 5.4 By Organisation Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Kenya

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 Workday Inc.

- 6.4.3 SAP SE (SuccessFactors)

- 6.4.4 iCIMS Inc.

- 6.4.5 Greenhouse Software Inc.

- 6.4.6 JazzHR (Employ Inc.)

- 6.4.7 Zoho Corporation Pvt. Ltd.

- 6.4.8 Bamboo HR LLC

- 6.4.9 Ceipal Corp.

- 6.4.10 Pinpoint HQ Ltd.

- 6.4.11 SmartRecruiters Inc.

- 6.4.12 Lever Inc.

- 6.4.13 Jobvite LLC

- 6.4.14 Bullhorn Inc.

- 6.4.15 Recruitee B.V.

- 6.4.16 Breezy HR Inc.

- 6.4.17 ADP LLC (Recruiting Management)

- 6.4.18 UKG Inc. (UKG Pro Recruiting)

- 6.4.19 IBM Corporation (Kenexa BrassRing)

- 6.4.20 ClearCompany Talent Management

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球应征者追踪系统市场报告

2026年全球应征者追踪系统市场报告 应征者追踪系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分

应征者追踪系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分 全球应征者追踪系统市场规模、份额、趋势和成长分析报告(2026-2034)应征者追踪系统 (ATS) 市场规模、份额、成长率和全球产业分析:按类型、应用程式和地区分類的洞察,2026-2034 年预测

全球应征者追踪系统市场规模、份额、趋势和成长分析报告(2026-2034)应征者追踪系统 (ATS) 市场规模、份额、成长率和全球产业分析:按类型、应用程式和地区分類的洞察,2026-2034 年预测 应征者追踪系统市场规模、份额、趋势和预测(按部署类型、组织规模、组件、最终用户和地区划分),2026-2034 年

应征者追踪系统市场规模、份额、趋势和预测(按部署类型、组织规模、组件、最终用户和地区划分),2026-2034 年 应征者追踪系统市场 - 全球产业规模、份额、趋势、机会及预测(按服务、部署类型、组织规模、产业垂直领域、地区和竞争格局划分,2021-2031 年)日本应征者追踪系统市场报告(按组件、组织规模、部署方式、最终用户和地区划分,2026-2034 年)

应征者追踪系统市场 - 全球产业规模、份额、趋势、机会及预测(按服务、部署类型、组织规模、产业垂直领域、地区和竞争格局划分,2021-2031 年)日本应征者追踪系统市场报告(按组件、组织规模、部署方式、最终用户和地区划分,2026-2034 年) 应征者追踪系统市场规模、份额和成长分析(按组件、部署方式、规模、最终用途和地区划分)—产业预测(2026-2033 年)

应征者追踪系统市场规模、份额和成长分析(按组件、部署方式、规模、最终用途和地区划分)—产业预测(2026-2033 年) 电子处方笺系统:全球市场份额和排名、总收入和需求预测(2025-2031年)

电子处方笺系统:全球市场份额和排名、总收入和需求预测(2025-2031年) 申请人追踪系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

申请人追踪系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测