|

市场调查报告书

商品编码

1940723

露营车和旅居车:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Caravan And Motorhome - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

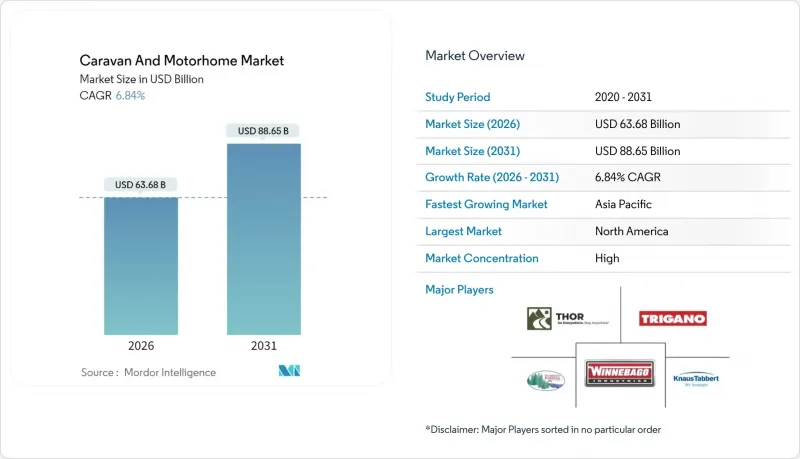

预计到 2026 年,露营车和旅居车市场价值将达到 636.8 亿美元,高于 2025 年的 596 亿美元。

预计到 2031 年将达到 886.5 亿美元,2026 年至 2031 年的复合年增长率为 6.84%。

持续成长与体验式旅游需求的不断增长、远距办公生活方式的兴起以及疫情期间国内自驾游热潮的持续升温相符。模组化底盘平台和48伏特直流电气系统等技术进步提升了离网能力。同时,千禧世代和Z世代消费者的涌入为房旅居车市场注入了新的购买力。北美凭藉着成熟的房车文化和完善的露营地基础设施,保持着主导地位。而亚太地区则实现了最快的区域扩张,这主要得益于可支配收入的成长和户外休閒参与率的提高。欧洲品牌的全球化以及专注于电动和模组化房车的新兴参与企业,使得传统住宿设施难以匹敌,市场竞争日益激烈。

全球露营车与旅居车市场趋势与洞察

后疫情时代,人们对国内旅行和户外旅行的偏好日益增强。

近期产业调查显示,人们越来越偏好规划好的露营和公路旅行,反映出旅行重心正从国际旅行转向国内旅行。安全顾虑、跨境的复杂性以及探索本地地区的经济效益是推动这一趋势的主要因素。房车露营持续走红,有助于在经济普遍不确定性的情况下稳定房旅居车市场。北美和欧洲完善的露营地网路提供的便利程度堪比饭店,进一步提升了房车旅行的吸引力。对许多家庭而言,拥有一辆房车是应对旅行成本波动的有效策略,从而支撑了房车旅行的长期需求。

千禧世代和Z世代的房车拥有量激增。

随着千禧世代和Z世代消费者将冒险旅行置于财富累积之上,房车买家的平均年龄已从53岁降至49岁,这使得年轻一代更有能力影响房车的设计和行销策略。许多35至54岁的车主优先考虑互联性、永续性和灵活的内部空间,这促使製造商开发轻质材料、整合式太阳能係统和模组化家具。社群媒体进一步推动了需求,用户评价和网红内容使全职或混合型游牧生活方式广受欢迎。贷款机构也纷纷效法汽车贷款的还款期限结构,帮助首次购车者克服高昂的价格。透过升级和数位化功能不断提升客户参与度,提高了客户维繫,鼓励重复购买,并支持房旅居车市场的持续成长。

高昂的初始购买和拥有成本

购买新房车和二手房车的融资成本给家庭预算带来了沉重负担。保险、维护和存放等额外费用往往会导致提前出售,降低客户亲和性,并减少口碑。虽然房车旅行是一种流行的生活方式选择,但由于可支配收入有限,年轻买家对价格非常敏感。某些市场的供应过剩导致价格大幅回调,凸显了价格虚高可能加剧的市场波动。如何在保持价格可负担的同时又不损害盈利盈利,仍然是房车行业面临的一大挑战。

细分市场分析

到2025年,旅行拖车将占露营车和旅居车市场总收入的61.34%,这主要得益于注重成本的买家偏好低廉的采集费用以及拖挂车辆进行日常出行的灵活性。在这一细分市场中,旅行拖车的吸引力正在不断扩大,产品涵盖从经济型到豪华型的各种选择。同时,第五轮拖车正吸引那些寻求住宅舒适体验的全职用户层。折迭式露营车轻鬆易携,适合车库存放,但由于隔热性和安全性更高的硬壳车型逐渐占据市场,其市场份额正在下降。同时,由于整合式生活空间和驾驶空间带来的自由移动性,旅居车预计到2031年将以8.08%的复合年增长率成长,超过整个露营车和旅居车市场的成长速度。 B型厢型车因其便利的停车条件而受到城市探险者的青睐,而A型房车则吸引了愿意投资宽敞内部空间的退休人士和数位游民。

千禧世代对「承包解决方案」日益增长的兴趣,使得旅居车更受欢迎,因为与拖挂式房车相比,自行式房车更容易整合驾驶辅助技术、太阳能电池板和智慧家庭控制系统。 Thor Industries 的混合动力 A 型原型车和 Jayco 售价 46 万美元的 Embarc EV 房车,正是高端市场采用整合推进和居住系统的典范。露营车製造商正透过轻质复合材料墙体和模组化内装来缩小创新差距。随着露营地预订 API 以及太阳能和储能套件的普及,产品差异化将更多地取决于数位生态系统,而不是仅仅取决于平面布局。因此,露营车将继续保持其销售主导地位,而旅居车将主导露营车和旅居车市场的技术发展趋势。

截至2025年,内燃机车型将占露营车和旅居车市场收入的91.74%,这反映了其成熟的燃料供应网络和久经考验的耐用性。然而,在日益严格的环保法规和电池成本下降的推动下,纯电动房车预计到2031年将以8.94%的复合年增长率成长,显着超过露营车和旅居车市场的整体成长速度。像Lightship的空气动力学旅行拖车这样的领先车型凸显了市场对静音运行和低运行成本的需求。混合动力系统则介于两者之间,它结合了内燃机以提供续航里程,以及电动马达在营地内移动和夜间静音运行的功能。

车队租赁公司是最早一批采用电动车的企业之一,他们利用可预测的路线和集中充电来弥补基础设施的不足。虽然消费者对电动车的接受度受国家公园充电限制和前期成本的影响较大,但州和地方政府的奖励正在逐年提高投资报酬率。製造商正在利用福特E-Transit和梅赛德斯-奔驰e-Sprinter等商用电动车底盘来缩短开发週期。电池密度的提高使得车身重量更轻,从而释放了车内空间,并缓解了车辆总长度的限制。总而言之,儘管内燃机在未来十年仍将占据主导地位,但电动化将主导露营车和旅居车市场的创新发展。

区域分析

2025年,北美将占全球露营车和旅居车市场收入的53.25%,这得益于其浓厚的房车文化、广阔的公共土地以及有利于大宗采购的融资结构。 2025年,美国的房车出货量有所成长,预计未来几年将持续成长,显示儘管利率上升,但国内需求依然强劲。加拿大拥有特殊复合板供应商,全职数位游牧者的数量也在不断增长,这增强了当地的售后市场生态系统。国家公园门票收入和露营地维修等公共资金支持了房车使用量的增长,公共资金也用于设施扩建。此外,B型改装房车的流行也促进了市场发展,这类房车更适合都市区储存限制。

在德国的引领下,欧洲正稳步发展。狭窄的道路和严格的排放气体控制区意味着紧凑的布局仍然至关重要。义大利和西班牙正着力发展可容纳房车的农业旅游设施,从而丰富商业露营地以外的住宿选择。在斯堪地那维亚国家,可再生能源奖励政策正在推动电动车的普及,为当地的房旅居车市场增添了技术优势。

亚太地区预计到2031年将以8.55%的复合年增长率成为全球房车市场成长最快的地区,这主要得益于可支配收入的成长和旅游政策的不断完善。日本的房车市场持续成长,并涌现许多创新技术,例如符合车库高度限制的电动升降车顶。在中国,中产阶级对房车的兴趣日益浓厚,这得益于政府大力推广国内旅游走廊,但西部省份基础设施的匮乏仍然是一大挑战。在澳洲成熟的房车市场,P2P租赁模式越来越受欢迎,Camplify车队的扩张也推动了房车利用率的提升。在韩国和印度等新兴市场,对配备房车介面设施的公路休息区的投资正在催生新的市场需求。总体而言,在基础设施不断完善和生活方式转变的推动下,亚太地区将继续在全球房旅居车市场规模成长中扮演核心角色。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 千禧世代和Z世代的房车拥有量激增。

- 「房车办公」生活方式的兴起,使得远距办公成为可能。

- 感染疾病后,人们更偏好国内旅行和户外旅行。

- 模组化、可升级房车平台的出现

- 采用48V直流电气系统实现离网功能

- 透过连接OEM和露营地API实现即时场地预订功能

- 市场限制

- 高昂的初始购买和拥有成本

- 对利率敏感的资金筹措环境

- 来自自助改装货车和个人租赁服务的竞争

- 国家公园对配备高容量电池的房车接入电网有限制

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测(价值、数量)

- 依产品类型

- 露营车

- 旅行拖车

- 第五轮拖车

- 折迭式露营拖车

- 卡车露营车

- 旅居车

- A级

- B 型(厢型车改装)

- C级

- 露营车

- 透过推广

- 内燃机(ICE)

- 混合式(并联/串联)

- 电池电电动房车

- 按长度

- 小于6米

- 6至8米

- 超过8米

- 最终用户

- 直接买家

- 车队车主租赁和订阅平台

- 按销售管道

- 特许经销商

- 直营店

- 线上直销

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 澳洲

- 韩国

- 印度

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Thor Industries Inc.

- Forest River Inc.

- Winnebago Industries Inc.

- Trigano SA

- Knaus Tabbert AG

- Swift Group

- Erwin Hymer Group

- Jayco Inc.

- Burstner GmbH & Co. KG

- Dethleffs GmbH and Co. KG

- Triple E Recreational Vehicles

- Tiffin Motorhomes Inc.

- Coachmen RV

- REV Group

- Leisure Travel Vans

- Airstream Inc.

- Adria Mobil doo

- Hobby-Wohnwagenwerk

- Westfalia Mobil GmbH

第七章 市场机会与未来展望

The caravan and motorhome market size in 2026 is estimated at USD 63.68 billion, growing from 2025 value of USD 59.60 billion with 2031 projections showing USD 88.65 billion, growing at 6.84% CAGR over 2026-2031.

Continued growth aligns with rising demand for experiential travel, the spread of remote-work lifestyles, and sustained interest in domestic road trips that gained traction during the pandemic. Technological advances such as modular chassis platforms and 48-volt DC electrical systems enhance off-grid capability. At the same time, demographic shifts toward millennial and Gen-Z buyers inject fresh spending power into the caravan and motorhome market. North America retains leadership because of a mature RV culture and expansive campground infrastructure. In contrast, the Asia-Pacific region registers the fastest regional expansion as disposable incomes and outdoor recreation participation climb. Competitive intensity rises as European brands globalize and new entrants focus on electric and modular formats that traditional hospitality options struggle to match.

Global Caravan And Motorhome Market Trends and Insights

Growing Preference for Domestic and Outdoor Travel Post-COVID

The recent industry survey highlights a growing preference for planned camping and road trips, reflecting a shift from international to domestic travel. Safety concerns, border complexities, and the cost-effectiveness of local exploration drive this trend. RV camping continues to gain popularity, helping stabilize the caravan and motorhome market amid broader economic uncertainties. Well-developed campground networks in North America and Europe offer convenience comparable to hotels, enhancing the appeal of RV travel. For many families, owning an RV is a strategic way to manage unpredictable travel costs, reinforcing long-term demand.

Surging Millennial and Gen-Z RV Ownership

The average RV buyer's age fell from 53 to 49 years as millennials and Gen-Z consumers elevated adventure travel over asset accumulation, positioning younger cohorts to influence design and marketing strategies . Most owners aged 35-54 prioritize connectivity, sustainability, and flexible interiors, steering manufacturers toward lighter materials, solar integration, and modular furniture. Social media further amplifies demand, as peer reviews and influencer content normalize full-time or hybrid nomadic lifestyles. Lenders have responded with term structures that mirror auto financing, helping first-time buyers surmount high ticket prices. Continuous engagement through upgrades and digital features improves retention and feeds repeat purchases, supporting sustained caravan and motorhome market growth.

High Initial Purchase and Ownership Cost

The cost of financing new and used RV units is placing significant pressure on household budgets. Additional expenses like insurance, maintenance, and storage often lead to early resale, dampening customer satisfaction and reducing positive word-of-mouth. Despite strong lifestyle alignment with RV travel, younger buyers are susceptible to pricing due to limited disposable income. Oversupply in some markets has led to notable price corrections, underscoring how elevated prices can amplify volatility. The industry continues to face the challenge of managing affordability without compromising profitability.

Other drivers and restraints analyzed in the detailed report include:

- Rise in Remote-Work-Enabled "Work-From-RV" Lifestyle

- Emergence of Modular, Upgradable RV Platforms

- Competition From DIY Van Conversions and Peer-To-Peer Rentals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Caravans captured 61.34% of the caravan and motorhome market revenue in 2025 as value-minded buyers favored lower acquisition costs and the flexibility of using the tow vehicle for daily transit. Within this segment, travel trailers span budget to luxury price points, broadening appeal, while fifth-wheel units attract full-time users seeking residential comfort. Folding campers, though lighter and garage-friendly, lose share as customers graduate to hard-sided models that offer better insulation and security. Motorhomes, however, are forecast for an 8.08% CAGR through 2031, eclipsing the broader caravan and motorhome market pace thanks to integrated living-driving layouts that ease spontaneous travel. Class B vans stand out among urban adventurers for parking convenience, whereas Class A coaches draw retirees and digital nomads willing to invest in spacious interiors.

Growing millennial interest in turnkey solutions benefits motorhomes, incorporating driver-assistance tech, solar arrays, and smart-home controls more readily than towables. Thor Industries' hybrid Class A prototype and Jayco's USD 460,000 Embark EV illustrate premium adoption of integrated propulsion and living systems. Caravan makers counter with lighter composite walls and modular interiors to close the innovation gap. As campsite booking APIs and solar-storage packages become standard, product differentiation hinges on digital ecosystems as much as floor plans. Consequently, caravans will retain volume leadership, but motorhomes will set the technological agenda of the caravan and motorhome market.

Internal combustion engine models retained 91.74% of the caravan and motorhome market revenue in 2025, reflecting well-established fueling networks and proven durability. Yet battery-electric RVs are projected for a 8.94% CAGR through 2031, well above the overall caravan and motorhome market size trajectory, as environmental regulations tighten and battery costs fall. Early entrants like Lightship's aerodynamic travel trailer highlight demand for silent operation and low running costs. Hybrid systems serve as a bridge, pairing combustion engines for range with electric motors for campground maneuverability and quiet overnight power.

Fleet rental firms adopt electrics fastest, using predictable routes and depot charging to mitigate infrastructure gaps. Consumer adoption remains sensitive to national park charging restrictions and upfront pricing, but state and provincial incentives improve ROI metrics annually. Manufacturers leverage commercial EV chassis from Ford E-Transit or Mercedes eSprinter platforms to shorten development cycles. Lighter packs free interior space as battery density rises, easing the length-regulation tension. Overall, combustion will dominate this decade, yet electrification sets the innovation narrative for the caravan and motorhome market.

The Caravan and Motorhome Market Report is Segmented by Product Type (Caravan and Motorhome), Propulsion (Internal Combustion Engine, Hybrid, and Battery-Electric), Length (Below 6m, 6-8m, and Above 8m), End User (Direct Buyers and Fleet Owners), Sales Channel (Franchise Dealerships, Company-Owned Stores, and Online Direct-To-Consumer), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America controlled 53.25% of the caravan and motorhome market revenue in 2025, underpinned by deep-rooted RV culture, vast public lands, and financing structures that ease high-ticket purchases. The United States shipments climbed in 2025 and are projected to grow in the coming years, signaling resilient domestic demand despite higher interest rates. Canada contributes specialized composite-panel suppliers and a growing cohort of full-time digital nomads, strengthening regional aftermarket ecosystems. National park entry fees and campground upgrades funnel public funds into site expansion, supporting usage growth. The caravan and motorhome market also benefits from the widespread availability of Class B conversions that suit urban storage restrictions.

Europe advanced steadily, led by Germany. Compact layouts remain essential due to narrow roads and stringent emission zones. Italy and Spain focus on agri-tourism sites that welcome RVs, diversifying overnight options beyond commercial campgrounds. Scandinavian countries see higher electric adoption spurred by renewable energy incentives, adding a technology edge to the region's caravan and motorhome market.

Asia-Pacific records the fastest 8.55% CAGR through 2031, propelled by rising disposable income and evolving tourism policies. Japan's RV market is growing, featuring innovations like electric pop-up roofs that preserve garage height limits. China's middle class shows growing interest, supported by government promotion of domestic tourism corridors, yet infrastructure gaps persist in western provinces. Australia's mature caravan scene benefits from peer-to-peer rentals, with Camplify's fleet expansion driving utilization. Emerging markets like South Korea and India invest in roadway rest areas with RV hookups, establishing early-stage demand. Overall, infrastructural progress and lifestyle shifts keep the Asia-Pacific pivotal to future caravan and motorhome market size growth.

- Thor Industries Inc.

- Forest River Inc.

- Winnebago Industries Inc.

- Trigano SA

- Knaus Tabbert AG

- Swift Group

- Erwin Hymer Group

- Jayco Inc.

- Burstner GmbH & Co. KG

- Dethleffs GmbH and Co. KG

- Triple E Recreational Vehicles

- Tiffin Motorhomes Inc.

- Coachmen RV

- REV Group

- Leisure Travel Vans

- Airstream Inc.

- Adria Mobil d.o.o

- Hobby-Wohnwagenwerk

- Westfalia Mobil GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Millennial and Gen-Z RV Ownership

- 4.2.2 Rise in Remote-Work-Enabled "Work-From-RV" Lifestyle

- 4.2.3 Growing Preference for Domestic and Outdoor Travel Post-COVID

- 4.2.4 Emergence Of Modular, Upgradable RV Platforms

- 4.2.5 Adoption of 48-V DC Electrical Architectures for Off-Grid Capability

- 4.2.6 OEM-Campground API Integrations Enabling Real-Time Site Booking

- 4.3 Market Restraints

- 4.3.1 High Initial Purchase and Ownership Cost

- 4.3.2 Interest-Rate-Sensitive Financing Environment

- 4.3.3 Competition From DIY Van Conversions and Peer-To-Peer Rentals

- 4.3.4 Grid-Access Restrictions for High-Capacity Battery RVs in National Parks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD), Volume (Units))

- 5.1 By Product Type

- 5.1.1 Caravan

- 5.1.1.1 Travel Trailers

- 5.1.1.2 Fifth-Wheel Trailers

- 5.1.1.3 Folding Camp Trailers

- 5.1.1.4 Truck Campers

- 5.1.2 Motorhome

- 5.1.2.1 Class A

- 5.1.2.2 Class B (Van Conversions)

- 5.1.2.3 Class C

- 5.1.1 Caravan

- 5.2 By Propulsion

- 5.2.1 Internal-Combustion Engine (ICE)

- 5.2.2 Hybrid (Parallel / Series)

- 5.2.3 Battery-Electric RV

- 5.3 By Length

- 5.3.1 Below 6 meters

- 5.3.2 6-8 meters

- 5.3.3 Above 8 meters

- 5.4 By End User

- 5.4.1 Direct Buyers

- 5.4.2 Fleet Owners - Rental and Subscription Platforms

- 5.5 By Sales Channel

- 5.5.1 Franchise Dealerships

- 5.5.2 Company-Owned Stores

- 5.5.3 Online Direct-to-Consumer

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 Australia

- 5.6.4.4 South Korea

- 5.6.4.5 India

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Thor Industries Inc.

- 6.4.2 Forest River Inc.

- 6.4.3 Winnebago Industries Inc.

- 6.4.4 Trigano SA

- 6.4.5 Knaus Tabbert AG

- 6.4.6 Swift Group

- 6.4.7 Erwin Hymer Group

- 6.4.8 Jayco Inc.

- 6.4.9 Burstner GmbH & Co. KG

- 6.4.10 Dethleffs GmbH and Co. KG

- 6.4.11 Triple E Recreational Vehicles

- 6.4.12 Tiffin Motorhomes Inc.

- 6.4.13 Coachmen RV

- 6.4.14 REV Group

- 6.4.15 Leisure Travel Vans

- 6.4.16 Airstream Inc.

- 6.4.17 Adria Mobil d.o.o

- 6.4.18 Hobby-Wohnwagenwerk

- 6.4.19 Westfalia Mobil GmbH

7 Market Opportunities and Future Outlook

自主型旅居车组装市场:依产品类型、燃料类型、通路和最终用户划分-2026年至2032年全球预测旅居车车租赁市场:2026年至2032年全球预测(依产品类型、租赁期限、客户类型、促销方式、价格范围、座位数、分销管道及最终用户划分)

自主型旅居车组装市场:依产品类型、燃料类型、通路和最终用户划分-2026年至2032年全球预测旅居车车租赁市场:2026年至2032年全球预测(依产品类型、租赁期限、客户类型、促销方式、价格范围、座位数、分销管道及最终用户划分) 欧洲旅居车:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲旅居车:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 旅居车市场规模、份额和成长分析(按类型、燃料类型、长度、应用和地区划分)-2026-2033年产业预测

旅居车市场规模、份额和成长分析(按类型、燃料类型、长度、应用和地区划分)-2026-2033年产业预测 全球旅居车市场

全球旅居车市场 房车市场 - 全球产业规模、份额、趋势、机会和预测,按类型(A 类、B 类、C 类)、按最终用户(车队所有者、直接买家)、按地区和竞争进行细分,2020 年至 2030 年预测

房车市场 - 全球产业规模、份额、趋势、机会和预测,按类型(A 类、B 类、C 类)、按最终用户(车队所有者、直接买家)、按地区和竞争进行细分,2020 年至 2030 年预测 2025-2029 年全球大篷车与旅居车市场

2025-2029 年全球大篷车与旅居车市场 2025-2033 年按产品类型(大篷车、房车)、最终用户(直接买家、车队所有者)和地区分類的大篷车和房车市场报告

2025-2033 年按产品类型(大篷车、房车)、最终用户(直接买家、车队所有者)和地区分類的大篷车和房车市场报告 房车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

房车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2030 年旅居车市场预测:按类型、燃料、应用、价格、应用、最终用户和地区进行的全球分析

2030 年旅居车市场预测:按类型、燃料、应用、价格、应用、最终用户和地区进行的全球分析