|

市场调查报告书

商品编码

1958442

环保食品包装市场规模(至 2035 年):依材料类型、包装类型、产品类型、技术、策略细分、应用领域、最终用户、公司、地区、产业趋势和预测Eco-friendly Food Packaging Market Till 2035: Distribution by Type of Material, Type of Packaging, Product, Technique, Layer, Areas of Application, End-User, Enterprise, and Geographical Regions: Industry Trends & Global Forecasts |

||||||

环保食品包装市场概况

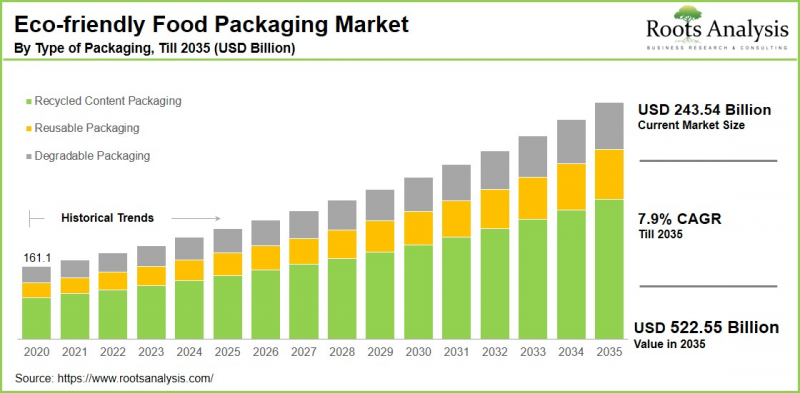

全球环保食品包装市场预计将从目前的 2,435.4 亿美元成长至 2035 年的 5,225.5 亿美元,2035 年前的复合年增长率 (CAGR) 为 7.9%。

环保食品包装市场:成长与趋势

环保食品包装是指使用环境安全且天然的材料包装。 可降解材料。这些材料必须能够保护食品免受物理、化学和生物威胁造成的篡改和污染。目前,活性包装是确保食品安全的首选包装类型。

受消费者偏好变化和严格的环境法规的推动,环保食品包装市场正呈现显着成长。塑造该市场的关键趋势之一是可生物降解和可堆肥包装材料的日益普及。这些材料由植物纤维和生物聚合物等可再生资源製成,因其能够自然分解而备受关注,有助于减少垃圾掩埋场的废物和环境污染。

此外,各公司正致力于开发符合永续发展目标的创新包装解决方案,包括水性涂层和可回收阻隔技术。对零浪费和无塑胶包装替代品的需求不断增长,以及材料科学的进步,正在加速向环保食品包装的转变。循环经济倡议日益重要,以及消费者期望企业在其营运中优先考虑永续性,也推动了这一趋势。 考虑到这些因素,预计环保食品包装市场在预测期内将显着成长。

本报告分析了全球环保食品包装市场,提供了市场规模估算、机会分析、竞争格局和公司概况。

目录

第一部分:报告概述

第一章:引言

第二章:研究方法

第三章:市场动态

第四章:宏观经济指标

第二部分:质性研究结果

第五章:摘要整理

第六章:引言

第七章:监理环境

第三部分:市场概览

第八章:关键指标综合资料库

第九章:竞争格局

第十章:市场空白分析

第十一章:竞争分析

第十二章:环保食品包装市场的新创企业生态系

第四部分:公司简介

第十三章:公司简介

- 章节概述

- 安姆科

- 波尔公司

- 巴斯夫

- 生物质

- 加拿大纸业

- 杜邦

- 生态产品

- 常青

- 福建青山

- 乔治亚-太平洋地区

- 绿包

- 克拉宾

- 蒙迪

- 北欧纸业

- SCG 包装

- 永续包装

- 利乐

- TIPA

- 特种东海纸

- 蔬菜

- 西石

- 温帕克

第 5 部分:市场趋势

第 14 章:大趋势分析

第 15 章:未满足的需求分析

第 16 章:专利分析

章节第 17 章:最新进展

第 6 节:市场机会分析

第 18 章:全球环保食品包装市场

第 19 章:依材料类型划分的市场机会

第 20 章:依包装类型划分的市场机会

第 21 章:依产品类型划分的市场机会

第 22 章:依技术类型划分的市场机会

第 23 章:以层类型划分的市场机会

第 24 章:依应用领域划分的市场机会

第 25 章:依最终使用者划分的市场机会

第26章:依公司类型划分的市场机会

第27章:北美环保食品包装市场的市场机会

第28章:欧洲环保食品包装市场的市场机会

第29章:亚洲环保食品包装市场的市场机会

第30章:中东和北非(MENA)环保食品包装市场的市场机会

第31章:拉丁美洲环保食品包装市场的市场机会

第32章:其他地区环保食品包装市场的市场机会

第33章:主要参与者的市场集中度分析

第32章:邻近市场分析

第7节:策略工具

第33章:关键成功策略

第34章:波特五力分析

第35章:SWOT分析

第36章:价值链分析

第37章:对Roots的策略建议

第8节:其他独家发现

第38章:主要研究发现

第39章:报告结论

第九节:附录

Eco-Friendly Food Packaging Market Overview

As per Roots Analysis, the global eco-friendly food packaging market size is estimated to grow from USD 243.54 billion in the current year USD 522.55 billion by 2035, at a CAGR of 7.9% during the forecast period, till 2035.

The opportunity for eco-friendly food packaging market has been distributed across the following segments:

Type of Material

- Glass

- Metal

- Paper & Paperboard

- Plastic

- Scratch-Based Materials

Type of Packaging

- Degradable Packaging

- Recycled Content Packaging

- Reusable Packaging

Type of Product

- Bags

- Bottles and Jars

- Boxes

- Cans

- Containers

- Films

- Pouches and Sachets

- Trays

- Tubes

- Other products

Type of Technique

- Active Packaging

- Alternate Fiber Packaging

- Molded Packaging

- Multipurpose Packaging

- Other techniques

Type of Layer

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

Areas of Application

- Beverages

- Food

Type of End-user

- Foodservice

- Food Processing

- Retail

Type of Enterprise

- Large Enterprises

- Small and Medium Enterprises

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Eco-Friendly Food Packaging Market: Growth and Trends

Eco-friendly food packaging involves using materials that are environmentally safe and capable of breaking down naturally. Such materials must ensure protection against tampering or contamination from any physical, chemical, or biological threats; currently, the most favored type of packaging used for food safety is active packaging.

The market for eco-friendly food packaging is witnessing significant growth, driven by shifts in consumer preferences and stringent environmental regulations. A key trend shaping this market is the increasing adoption of biodegradable and compostable packaging materials. Made from renewable sources such as plant-based fibers and biopolymers, these materials are gaining traction because of their ability to decompose naturally, which helps reduce landfill waste and environmental pollution.

Further, the companies are focusing on developing innovative packaging solutions that align with sustainability goals, which includes water-based coatings and recyclable barrier technologies. The rising demand for zero-waste and plastic-free packaging alternatives, combined with advancements in material science, is accelerating the shift toward eco-friendly food packaging. This movement is also backed by an increased emphasis on circular economy initiatives and consumer expectations for companies that prioritize sustainability in their practices. Overall, considering the above mentioned factors, the eco-friendly food packaging market is expected to grow significantly during the forecast period.

Eco-Friendly Food Packaging Market: Key Segments

Market Share by Type of Material

Based on type of material, the global eco-friendly food packaging market is segmented into glass, metal, paper & paperboard, plastic, scratch-based materials. According to our estimates, currently, the paper & paperboard sub-segment captures the majority of the market share. This is due to its broad availability, recyclability, and versatility. Paper-based materials are economical, lightweight, and easily customizable, which makes them a favored option for food packaging across different sectors.

Conversely, the scratch-based materials segment is expected to experience rapid growth throughout the forecast period. This is driven by the increasing demand for innovative, biodegradable, and compostable packaging solutions. Scratch-based materials fit well within the circular economy model, providing a sustainable alternative to conventional plastics.

Market Share by Type of Packaging

Based on type of packaging, the global eco-friendly food packaging market is segmented into degradable packaging, recycled content packaging and reusable packaging. According to our estimates, currently, the recycled content packaging segment captures the majority of the market share. This is due to the increasing focus on circular economy initiatives and the rising demand for sustainable packaging made from materials that are either post-consumer or post-industrial waste.

However, the reusable packaging segment is expected to grow at a higher CAGR during the forecast period. This growth is fueled by the growing awareness of the need to minimize single-use packaging waste and the transition towards more durable and long-lasting packaging options.

Market Share by Type of Product

Based on type of product, the global eco-friendly food packaging market is segmented into bags, bottles and jars, boxes, cans, containers, films, pouches and sachets, trays, tubes and other products. According to our estimates, currently, the containers segment captures the majority of the market share. This growth is primarily due to its widespread usage in various applications like food storage and takeout services. Containers crafted from biodegradable materials such as cardboard, paper, and bioplastics are increasingly preferred for their capacity to reduce environmental impact while maintaining food quality.

However, the bags segment is expected to grow at a higher CAGR during the forecast period. The expansion of this segment is fueled by growing consumer demand for convenient and lightweight packaging options. Eco-friendly bags, frequently constructed from materials such as recycled paper or compostable plastics, are becoming more popular due to their versatility in transporting food items and their alignment with sustainability objectives.

Market Share by Type of Technique

Based on type of technique, the global eco-friendly food packaging market is segmented into active packaging, alternate fiber packaging, molded packaging, multipurpose packaging, and other techniques. According to our estimates, currently, the active packaging segment captures the majority of the market share. This growth is primarily due to its capability to enhance food safety and quality while decreasing waste, making it a popular option among manufacturers and consumers looking for sustainable choices.

However, the molded packaging segment is expected to grow at a higher CAGR during the forecast period. Molded packaging, which encompasses products like trays and containers made from biodegradable materials, is gaining popularity due to its flexibility and effectiveness in safeguarding food products. Moreover, the rising demand for lightweight yet resilient packaging solutions that also reduce environmental impact is propelling market growth.

Market Share by Type of Layer

Based on type of layer, the global eco-friendly food packaging market is segmented into primary packaging, secondary packaging, and tertiary packaging. According to our estimates, currently, the primary packaging segment captures the majority of the market share. Primary containers refer to items that directly hold food products, such as bags, bottles, and containers. This segment is experiencing growth due to heightened consumer awareness and regulatory demands for reducing plastic usage.

However, the secondary packaging segment is expected to grow at a higher CAGR during the forecast period. The increasing focus on sustainability and environmental consciousness among consumers is boosting the demand for secondary packaging solutions that are both functional and compatible with ecological objectives.

Market Share by Areas of Application

Based on areas of application, the global eco-friendly food packaging market is segmented into beverages and food. According to our estimates, currently, the food segment captures the majority of the market share. This segment benefits from the widespread adoption of sustainable packaging solutions across different food categories, such as bakery items, dairy products, meat, fruits, and vegetables. The growth of this segment is being driven by the increasing consumer demand for fresh and minimally processed foods, along with a heightened awareness of environmental concerns.

However, the beverages segment is expected to grow at a higher CAGR during the forecast period. This growth is attributed to the rising consumer inclination toward sustainable packaging options in beverage products, which include both alcoholic and non-alcoholic varieties.

Market Share by Type of End-User

Based on type of end-user, the global eco-friendly food packaging market is segmented into foodservice, food processing and retail. According to our estimates, currently, the foodservice segment captures the majority of the market share. This growth is primarily due to the rising focus on sustainability and environmental accountability among restaurants and catering firms, which are progressively adopting eco-friendly packaging solutions to satisfy consumer demand for greener packaging options.

However, the food processing segment is expected to grow at a higher CAGR during the forecast period. This growth is propelled by an increasing emphasis on sustainable practices in food manufacturing, as processors aim to lessen their environmental impact.

Market Share by Type of Enterprise

Based on type of enterprise, the global eco-friendly food packaging market is segmented into large and small and medium enterprises. According to our estimates, currently, the large enterprise segment captures the majority of the market share. This can be attributed to their flexibility, innovative approaches, emphasis on specialized markets, and capability to adjust to evolving customer preferences and market dynamics.

Market Share by Geographical Regions

Based on geographical regions, the eco-friendly food packaging market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and the rest of the world. According to our estimates, currently Europe captures the majority share of the market. This increase is largely fueled by the restrictions on single-use plastics enforced by government regulations within the European Union. The European Directive has set forth guidelines for the circular economy and sustainability standards that are being adopted by businesses across Europe.

Example Players in Eco-Friendly Food Packaging Market

- Amcor

- Ball Corporation

- BASF

- Be Green

- Berry Global

- Billerudkorsnas

- Biomass

- Biopak

- Canfor

- Crown Holdings

- CTI Paper

- Daio Paper Construction

- DS Smith

- DuPont

- Gascogne Papier

- Genpak

- Genus Paper and Boards

- International Paper

- Karl Knauer

- Klabin

- Oji Holdings

- PacknWood

- Paperfoam

- Printpak

- SCG PACKAGING

- Sealed Air

- Segezha

- Sulapac

- Sustainable Packaging

- Swedbrand

- Tetra Pak

- TIPA

- Tokushu Tokai Paper

- Vegware

- WestRock

- Winpak

Eco-Friendly Food Packaging Market: Research Coverage

The report on the eco-friendly food packaging market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the eco-friendly food packaging market, focusing on key market segments, including [A] type of material, [B] type of packaging, [C] type of product, [D] type of technique, [E] type of layer, [F] areas of application, [G] type of end-user, [H] type of enterprise, and [I] geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the eco-friendly food packaging market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the eco-friendly food packaging market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the eco-friendly food packaging industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the eco-friendly food packaging domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the eco-friendly food packaging market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the eco-friendly food packaging market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

- Value Chain Analysis: A comprehensive analysis of the value chain, providing information on the different phases and stakeholders involved in the eco-friendly food packaging market.

Key Questions Answered in this Report

- How many companies are currently engaged in eco-friendly food packaging market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Eco-friendly Food Packaging Market

- 6.2.1. Type of Material

- 6.2.2. Type of Packaging

- 6.2.3. Type of Product

- 6.2.4. Type of Technique

- 6.2.5. Type of Layer

- 6.2.6. Areas of Application

- 6.2.7. By End-Users

- 6.3. Future Perspective

7. REGULATORY SCENARIO

SECTION III: MARKET OVERVIEW

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Eco-friendly Food Packaging Market: Overall Market Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Ownership Structure

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM IN THE ECO-FRIENDLY FOOD PACKAGING MARKET

- 12.1. Eco-friendly Food Packaging Market: Market Landscape of Startups

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Company Size

- 12.1.3. Analysis by Company Size and Year of Establishment

- 12.1.4. Analysis by Location of Headquarters

- 12.1.5. Analysis by Company Size and Location of Headquarters

- 12.1.6. Analysis by Ownership Structure

- 12.2. Key Findings

SECTION IV: COMPANY PROFILES

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. Amcor*

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Service / Product Portfolio (project specific)

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- 13.3. Ball Corporation

- 13.4. BASF

- 13.5. Biomass

- 13.6. Canadian Paper

- 13.7. DuPont

- 13.8. Eco Products

- 13.9. Evergreen

- 13.10. Fujian Qingshan

- 13.11. Georgia-Pacific

- 13.12. Green Pack

- 13.13. Klabin

- 13.14. Mondi

- 13.15. Nordic Paper

- 13.16. SCG PACKAGING

- 13.17. Sustainable Packaging

- 13.18. Tetra Pak

- 13.19. TIPA

- 13.20. Tokushu Tokai Paper

- 13.21. Vegware

- 13.22. WestRock

- 13.23. Winpak

SECTION V: MARKET TRENDS

14. MEGA TRENDS ANALYSIS

15. UNMET NEED ANALYSIS

16. PATENT ANALYSIS

17. RECENT DEVELOPMENTS

- 17.1. Chapter Overview

- 17.2. Recent Funding

- 17.3. Recent Partnerships

- 17.4. Other Recent Initiatives

SECTION VI: MARKET OPPORTUNITY ANALYSIS

18. GLOBAL ECO-FRIENDLY FOOD PACKAGING MARKET

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Trends Disruption Impacting Market

- 18.4. Demand Side Trends

- 18.5. Supply Side Trends

- 18.6. Global Eco-friendly Food Packaging Market, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 18.7. Multivariate Scenario Analysis

- 18.7.1. Conservative Scenario

- 18.7.2. Optimistic Scenario

- 18.8. Investment Feasibility Index

- 18.9. Key Market Segmentations

19. MARKET OPPORTUNITIES BASED ON TYPE OF MATERIAL

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Eco-friendly Food Packaging Market for Glass: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 19.7. Eco-friendly Food Packaging Market for Metal: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 19.8. Eco-friendly Food Packaging Market for Paper and Paperboard: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 19.9. Eco-friendly Food Packaging Market for Plastic: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 19.10. Eco-friendly Food Packaging Market for Scratch-Based Materials: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 19.11. Data Triangulation and Validation

- 19.11.1. Secondary Sources

- 19.11.2. Primary Sources

- 19.11.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON TYPE OF PACKAGING

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Eco-friendly Food Packaging Market for Degradable Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 20.7. Eco-friendly Food Packaging Market for Recycled Content Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 20.8. Eco-friendly Food Packaging Market for Reusable Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 20.9. Data Triangulation and Validation

- 20.9.1. Secondary Sources

- 20.9.2. Primary Sources

- 20.9.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON TYPE OF PRODUCT

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Eco-friendly Food Packaging Market for Bags: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.7. Eco-friendly Food Packaging Market for Bottles and Jars: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.8. Eco-friendly Food Packaging Market for Boxes: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.9. Eco-friendly Food Packaging Market for Cans: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.10. Eco-friendly Food Packaging Market for Containers: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.11. Eco-friendly Food Packaging Market for Films: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.12. Eco-friendly Food Packaging Market for Pouches and Sachets: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.13. Eco-friendly Food Packaging Market for Trays: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.14. Eco-friendly Food Packaging Market for Tubes: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.15. Eco-friendly Food Packaging Market for Other products: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.16. Data Triangulation and Validation

- 21.16.1. Secondary Sources

- 21.16.2. Primary Sources

- 21.16.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON TYPE OF TECHNIQUE

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Eco-friendly Food Packaging Market for Active Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 22.7. Eco-friendly Food Packaging Market for Alternate Fiber Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 22.8. Eco-friendly Food Packaging Market for Molded Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 22.9. Eco-friendly Food Packaging Market for Multipurpose Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 22.10. Eco-friendly Food Packaging Market for Other techniques: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 22.11. Data Triangulation and Validation

- 22.11.1. Secondary Sources

- 22.11.2. Primary Sources

- 22.11.3. Statistical Modeling

23. MARKET OPPORTUNITIES BASED ON TYPE OF LAYER

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Eco-friendly Food Packaging Market for Primary Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 23.7. Eco-friendly Food Packaging Market for Secondary Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 23.8. Eco-friendly Food Packaging Market for Tertiary Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 23.9. Data Triangulation and Validation

- 23.9.1. Secondary Sources

- 23.9.2. Primary Sources

- 23.9.3. Statistical Modeling

24. MARKET OPPORTUNITIES BASED ON AREAS OF APPLICATION

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Eco-friendly Food Packaging Market for Beverages: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 24.7. Eco-friendly Food Packaging Market for Food: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 24.8. Data Triangulation and Validation

- 24.8.1. Secondary Sources

- 24.8.2. Primary Sources

- 24.8.3. Statistical Modeling

25. MARKET OPPORTUNITIES BASED ON TYPE OF END-USER

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Eco-friendly Food Packaging Market for Foodservice: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.7. Eco-friendly Food Packaging Market for Food Processing: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.8. Eco-friendly Food Packaging Market for Retail: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.9. Data Triangulation and Validation

- 25.9.1. Secondary Sources

- 25.9.2. Primary Sources

- 25.9.3. Statistical Modeling

26. MARKET OPPORTUNITIES BASED ON TYPE OF ENTERPRISE

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Eco-friendly Food Packaging Market for Large Enterprise: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 26.7. Eco-friendly Food Packaging Market for Small and Medium Enterprise (SME): Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 26.8. Data Triangulation and Validation

- 26.8.1. Secondary Sources

- 26.8.2. Primary Sources

- 26.8.3. Statistical Modeling

27. MARKET OPPORTUNITIES FOR ECO-FRIENDLY FOOD PACKAGING MARKET IN NORTH AMERICA

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Eco-friendly Food Packaging Market in North America: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.1. Eco-friendly Food Packaging Market in the US: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.2. Eco-friendly Food Packaging Market in Canada: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.3. Eco-friendly Food Packaging Market in Mexico: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.4. Eco-friendly Food Packaging Market in Other North American Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR ECO-FRIENDLY FOOD PACKAGING MARKET IN EUROPE

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Eco-friendly Food Packaging Market in Europe: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.1. Eco-friendly Food Packaging Market in Austria: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.2. Eco-friendly Food Packaging Market in Belgium: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.3. Eco-friendly Food Packaging Market in Denmark: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.4. Eco-friendly Food Packaging Market in France: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.5. Eco-friendly Food Packaging Market in Germany: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.6. Eco-friendly Food Packaging Market in Ireland: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.7. Eco-friendly Food Packaging Market in Italy: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.8. Eco-friendly Food Packaging Market in Netherlands: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.9. Eco-friendly Food Packaging Market in Norway: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.10. Eco-friendly Food Packaging Market in Russia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.11. Eco-friendly Food Packaging Market in Spain: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.12. Eco-friendly Food Packaging Market in Sweden: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.13. Eco-friendly Food Packaging Market in Switzerland: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.14. Eco-friendly Food Packaging Market in the UK: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.15. Eco-friendly Food Packaging Market in Other European Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.7. Data Triangulation and Validation

29. MARKET OPPORTUNITIES FOR ECO-FRIENDLY FOOD PACKAGING MARKET IN ASIA

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Revenue Shift Analysis

- 29.4. Market Movement Analysis

- 29.5. Penetration-Growth (P-G) Matrix

- 29.6. Eco-friendly Food Packaging Market in Asia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.1. Eco-friendly Food Packaging Market in China: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.2. Eco-friendly Food Packaging Market in India: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.3. Eco-friendly Food Packaging Market in Japan: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.4. Eco-friendly Food Packaging Market in Singapore: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.5. Eco-friendly Food Packaging Market in South Korea: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.6. Eco-friendly Food Packaging Market in Other Asian Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.7. Data Triangulation and Validation

30. MARKET OPPORTUNITIES FOR ECO-FRIENDLY FOOD PACKAGING MARKET IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 30.1. Chapter Overview

- 30.2. Key Assumptions and Methodology

- 30.3. Revenue Shift Analysis

- 30.4. Market Movement Analysis

- 30.5. Penetration-Growth (P-G) Matrix

- 30.6. Eco-friendly Food Packaging Market in Middle East and North Africa (MENA): Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.1. Eco-friendly Food Packaging Market in Egypt: Historical Trends (Since 2020) and Forecasted Estimates (Till 205)

- 30.6.2. Eco-friendly Food Packaging Market in Iran: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.3. Eco-friendly Food Packaging Market in Iraq: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.4. Eco-friendly Food Packaging Market in Israel: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.5. Eco-friendly Food Packaging Market in Kuwait: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.6. Eco-friendly Food Packaging Market in Saudi Arabia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.7. Eco-friendly Food Packaging Market in United Arab Emirates (UAE): Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.8. Eco-friendly Food Packaging Market in Other MENA Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.7. Data Triangulation and Validation

31. MARKET OPPORTUNITIES FOR ECO-FRIENDLY FOOD PACKAGING MARKET IN LATIN AMERICA

- 31.1. Chapter Overview

- 31.2. Key Assumptions and Methodology

- 31.3. Revenue Shift Analysis

- 31.4. Market Movement Analysis

- 31.5. Penetration-Growth (P-G) Matrix

- 31.6. Eco-friendly Food Packaging Market in Latin America: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.1. Eco-friendly Food Packaging Market in Argentina: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.2. Eco-friendly Food Packaging Market in Brazil: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.3. Eco-friendly Food Packaging Market in Chile: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.4. Eco-friendly Food Packaging Market in Colombia Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.5. Eco-friendly Food Packaging Market in Venezuela: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.6. Eco-friendly Food Packaging Market in Other Latin American Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.7. Data Triangulation and Validation

32. MARKET OPPORTUNITIES FOR ECO-FRIENDLY FOOD PACKAGING MARKET IN REST OF THE WORLD

- 32.1. Chapter Overview

- 32.2. Key Assumptions and Methodology

- 32.3. Revenue Shift Analysis

- 32.4. Market Movement Analysis

- 32.5. Penetration-Growth (P-G) Matrix

- 32.6. Eco-friendly Food Packaging Market in Rest of the World: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 32.6.1. Eco-friendly Food Packaging Market in Australia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 32.6.2. Eco-friendly Food Packaging Market in New Zealand: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 32.6.3. Eco-friendly Food Packaging Market in Other Countries

- 32.7. Data Triangulation and Validation

33. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

32. ADJACENT MARKET ANALYSIS

SECTION VII: STRATEGIC TOOLS

33. KEY WINNING STRATEGIES

34. PORTER'S FIVE FORCES ANALYSIS

35. SWOT ANALYSIS

36. VALUE CHAIN ANALYSIS

37. ROOTS STRATEGIC RECOMMENDATIONS

- 37.1. Chapter Overview

- 37.2. Key Business-related Strategies

- 37.2.1. Research & Development

- 37.2.2. Product Manufacturing

- 37.2.3. Commercialization / Go-to-Market

- 37.2.4. Sales and Marketing

- 37.3. Key Operations-related Strategies

- 37.3.1. Risk Management

- 37.3.2. Workforce

- 37.3.3. Finance

- 37.3.4. Others

SECTION VIII: OTHER EXCLUSIVE INSIGHTS

38. INSIGHTS FROM PRIMARY RESEARCH

39. REPORT CONCLUSION

SECTION IX: APPENDIX

40. TABULATED DATA

41. LIST OF COMPANIES AND ORGANIZATIONS

42. CUSTOMIZATION OPPORTUNITIES

43. ROOTS SUBSCRIPTION SERVICES

44. AUTHOR DETAILS

环保食品包装市场机会、成长要素、产业趋势分析及2026-2035年预测

环保食品包装市场机会、成长要素、产业趋势分析及2026-2035年预测 环保食品包装市场分析及预测(至2035年):类型、产品类型、材料类型、应用、技术、最终用户、组件、製程、实施方案、解决方案

环保食品包装市场分析及预测(至2035年):类型、产品类型、材料类型、应用、技术、最终用户、组件、製程、实施方案、解决方案 全球甘蔗容器市场规模、份额、趋势和成长分析报告(2026-2034年)环保食品包装市场规模、份额、成长及全球产业分析:按类型和应用划分,区域洞察及2026-2034年预测

全球甘蔗容器市场规模、份额、趋势和成长分析报告(2026-2034年)环保食品包装市场规模、份额、成长及全球产业分析:按类型和应用划分,区域洞察及2026-2034年预测 2026年全球环保食品包装市场报告

2026年全球环保食品包装市场报告 永续包装和环保食品解决方案市场预测至2032年:按包装材料、产品类型、技术、分销管道、最终用户和地区分類的全球分析环保包装材料市场预测至2032年:按包装类型、材料、形式、工艺、应用和地区分類的全球分析甘蔗餐具市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)可生物降解和可堆肥包装市场预测至2032年:按产品类型、材料类型、技术、应用、最终用户和地区分類的全球分析

永续包装和环保食品解决方案市场预测至2032年:按包装材料、产品类型、技术、分销管道、最终用户和地区分類的全球分析环保包装材料市场预测至2032年:按包装类型、材料、形式、工艺、应用和地区分類的全球分析甘蔗餐具市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)可生物降解和可堆肥包装市场预测至2032年:按产品类型、材料类型、技术、应用、最终用户和地区分類的全球分析 生物分解性食品包装薄膜市场(按材料类型、厚度、包装类型、最终用户产业、应用和分销管道)—2025-2030 年全球预测

生物分解性食品包装薄膜市场(按材料类型、厚度、包装类型、最终用户产业、应用和分销管道)—2025-2030 年全球预测