|

市场调查报告书

商品编码

1808959

近眼显示市场趋势与技术分析(2025年)2025 Near-Eye Display Market Trend and Technology Analysis |

|||||||

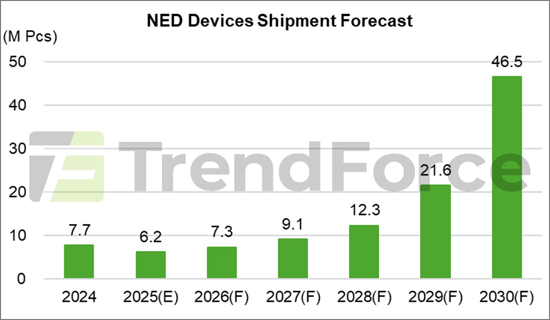

在 "近眼显示市场趋势与技术分析(2025)" 中,预计近眼显示设备市场短期内将保持低迷,2025年全球出货量预测为620万台。 Meta的Quest 3s表现低于预期,预计2025年出货量将降至560万台。相比之下,AR设备短期内表现出强劲势头。在新型AI+AR产品的推动下,以及OLEDoS成本下降,预计2025年出货量将达到60万台。从中长期来看,Meta和苹果等主要公司对VR/MR产品的开发预计将增强生态系统。同时,基于通知功能的AR设备的强劲需求以及高端全彩AR产品的兴起将推动长期增长,预计到2030年,全球NED设备出货量将激增至4650万台。

AR显示技术展望

AR显示技术的选择反映了品牌策略和市场趋势。 TrendForce指出,OLEDoS面临来自其他显示技术的日益激烈的竞争。目前,其成本优势预计将在中国保持主导地位。由于Meta的采用,LCoS预计将推动市场成长,而采用单色LEDoS的通知功能AR眼镜的成长也推动了LEDoS的普及。

长远来看,AR 设备将需要更高的运算能力、更长的电池续航时间和更强大的显示效能。全球品牌正倾向高规格、全彩的 LEDoS 技术。随着成本下降和效能提升,TrendForce 预测,到 2030 年,配备全彩 LED 的 Surface AR 设备出货量将达到 2,090 万台,占总市场渗透率的 65%。

波导製程与 SiC 联盟分析

波导技术仍是 AR 光学引擎的关键差异化因素。衍射波导目前是主流,但仍需提高效率。

波导製造主要由两种製程技术主导:

- 奈米压印光刻 (NIL) - 低模具成本和对复杂奈米结构设计的适应性使其适合早期小批量开发。

- 光刻 (PL) - 高产量、长光罩寿命以及高折射率 SiC 材料的直接加工使其适合大规模生产。

TrendForce 观察到,中国 SiC 供应商与波导製造商的合作正在增加。 SiC 的高折射率使其成为一种极具前景的材料。目前,中国的 SiC 基板主要以 4 英吋和 6 英吋为主,但成本效益正在推动其朝向更大尺寸转变。到 2030 年,8 吋 SiC 晶圆的出货量预计将超过 20%,12 吋也有望发展。这将进一步加速 PL 技术的普及。

AR 品牌策略与规格趋势

随着 AR 光学引擎模组尺寸的缩小,规格趋于趋同,从而限制了差异化。 CMOS 基板尺寸和设计正趋向标准化以控製成本。目前,大多数 LEDoS 和 LCoS 面板尺寸为 0.13-0.18 英寸,像素密度超过 5,500 PPI。 LEDoS 的解析度通常在 640x480 到 720x720 之间,而 LCoS 面板的解析度通常为 720x720。这促使各品牌追求不同的策略方向。

Xreal 专注于扩大视野角 (FOV) 和提升运算效能的显示技术和演算法。 RayNeo 正在推广全彩 LEDoS+波导 AR 眼镜,同时强化其用于媒体消费的 OLEDoS+Birdbath 解决方案。同时,INMO 优先考虑一体化 AI 驱动的 AR 设备。 Meta 计划打造完整的产品线,并大力投资 AI 功能,以应对苹果未来的市场进入。

这一趋势凸显了 AR 市场正从单纯的硬体竞争转向更整合的软硬体生态系统。

目录

第1章 近眼显示设备市场分析

- NED设备出货分析,2025年~2030年

- VR/MR出货分析,2025年~2030年

- 全球VR/MR设备市场占有率(各技术),2025年~2030年

- VR/MR设备市场规模分析:LCD/OLEDoS,2025年~2030年

- AR出货分析,2025年~2030年

- AR设备市场占有率(各地区)

- 全球AR设备市场占有率(各技术),2025年~2030年

- AR设备市场规模分析:LCD/OLEDoS,2025年~2030年

第2章 近眼显示技术的开发趋势分析

- 2.1.VR/MR显示器技术与市场趋势分析

- VST 的固有问题:几何失真

- 注视点技术可减少资料传输和功耗

- 亮度感知也聚焦在註视点 - 晕影

- 利用偏光和饼状技术实现注视点 VR 显示屏

- 降低 LCD 功耗的解决方案

- Mini-LED 背光饼状补偿的损耗

- 直射光会降低 Mini-LED 背光的对比增益

- RGB Mini-LED 背光拓展 LCD VR 的潜力

- 我们会从蓝光 Mini-LED 升级到 RGB Mini-LED 吗?

- 定向背光是LCD VR的理想目标

- 12吋OLEDoS厂商产能分析

- 全彩OLEDoS技术横向比较

- 采用三喷嘴蒸镀系统PPI上限的改良型OLEDoS

- VR/MR发展

- 2.2.AR显示器技术与市场趋势分析

- 光源规格与价格最佳点分析

- 多区域Micro/Mini LED背光增强LCoS对比度并降低功耗

- LCoS的进一步小型化:平面光技术的持续研究

- LCoS技术发展趋势

- LEDoS从X-Cube向单晶片全彩演进过程中所面临的课题

- 推动从X-Cube转向单晶片全彩解决方案的因素LEDoS 技术

- 全彩 LEDoS 技术横向比较

- 全彩 LEDoS 技术纵向堆迭横向比较

- 垂直堆迭 LEDoS 关键技术分析:首尔伟傲世/JBD

- 全彩 LEDoS 技巧 - InGaN 横向比较

- CMOS 驱动微型显示器背板尺寸扩展至 12 吋

- 从背板设计到系统整合,LEDoS CMOS 技术面临的技术课题

- 晶片键合製程分析

- 晶圆键合製程分析

- 索尼半导体也提出 LEDoS 的 D2W2W 技术

- LEDoS 参与者产能分析

- LCoS 和 LEDoS

- DoS 和 LCoS 功耗比较

- LEDoS 和 LCoS 显示器规格分析

- LEDoS 和 LCoS 规格分析全彩光引擎

- 2.3. AR光学技术及市场趋势分析

- 几何波导

- 绕射波导

- 绕射波导三大关键参数的折衷

- 衍射波导的效率课题

- 奈米压印微影 (NIL) 与光刻 (PL)

- 热NIL和紫外线NIL

- 热NIL的课题

- 几何光学波导的Rain技术

- 偏振系统

- Ant Reality Optics - 混合波导

- 合束器技术的优缺点

- 元波导专利策略

- 友达光电和京东方参与SRG波导

- 2.4.SiC 光波导技术及市场趋势分析

- Meta Orion AR:SiC 光波导+双面光栅

- SiC 波导应用的可行性与局限性

- 各 SiC 晶圆尺寸 AR 玻璃产量

- SiC 晶圆市场分析

- SiC 产业链厂商

- 2.5.AR 系统技术及市场趋势分析

- 新兴技术:近眼显示中的眼动追踪

- AR/VR - 眼动追踪优势分析

- 眼动追踪 - PCCR 与 AI 影像分析

- 眼动追踪 - 品牌策略及价值链分析

- SoC

第3章 全球AR产品开发趋势分析

- 3.1.中国的AR产品开发趋势分析

- AR的开发

- 中国AR品牌-Xreal

- 中国AR品牌-RayNeo

- 中国AR品牌-INMO

- 中国AR品牌-Rokid/MEIZU

- 中国AR眼镜的比较:重量/显示器技术

- 中国AR眼镜的比较:价格/显示器技术

- 3.2.AR产品开发趋势分析- 中国以外

- AI/AR眼镜发展路线图

- 海外AI/AR眼镜对比

- 2014年至2024年AR眼镜发展趋势

- 海外AR眼镜全彩显示技术

第4章 参与企业的动态更新

- VR/MR Supply Chain

- Seeya

- Sidtek

- BOE Achieved Milestone of Double 5K for 0.9-inch OLEDoS

- AR Supply Chain

- EV Group

- Porotech

- Polar Light Technologies AB (PLT)

- Q Pixel

- Micledi Microdisplays

- VueReal

- JBD

- Hongshi

- Raysolve

- Giga-Image

- GIS/JorJin

- Himax

- Meta

- Snap

TrendForce, "2025 Near-Eye Display Market Trend and Technology Analysis" observes that the near-eye display device market is expected to remain subdued in the short term, with global shipments protected at 6.2 million units in 2025. Meta's Quest 3s has underperformed expectations, with shipments forecast to decline to 5.6 million units in 2025. In contrast, AR devices are showing stronger short-term momentum. Driven by new AI+AR products and falling OLEDoS costs, shipments are expected to reach 600,000 units in 2025. Over the medium to long term, ongoing VR/MR product development by major players such as Meta and Apple will help strengthen the ecosystem. On the other hand, strong demand in notification-type AR devices and the rise of high-end full-color AR products are set to fuel long-term growth, with global NED devices shipment forecast to surge to 46.5 million units by 2030.

Outlook on AR Display Technology

Choices regarding AR display technology reflect brand strategies and market trends. In the near term, OLEDoS will remain dominant in China due to cost advantages, though TrendForce notes it faces rising competition from other display technologies. LCoS is expected to gain market traction with adoption by Meta, while growth in notification-type AR glasses using single-color LEDoS is also driving LEDoS penetration.

Over the long term, AR devices will increasingly demand higher computing power, longer battery life, and enhanced display performance-particularly with the integration of AI. Global brands are leaning toward high-spec full-color LEDoS technology. As costs decline and performance improves, TrendForce forecasts shipments of AR devices equipped with full-color LEDoS to reach 20.9 million units by 2030, accounting for 65% penetration.

Waveguide Process and SiC Alliance Analysis

In AR optical engines, waveguide technology remains a critical differentiator. While diffractive waveguides are the current mainstream, efficiency improvements are still needed.

Two primary process technologies dominate waveguide manufacturing:

- Nanoimprint lithography (NIL): Suited for early-stage small-batch development due to lower mother mold costs and adaptability to complex nanostructure design.

- Photolithography (PL): Better for mass production, with higher throughput, longer mask lifetimes, and direct processing capability for high-refractive-index SiC materials.

TrendForce observes a growing number of Chinese SiC suppliers forming alliances with waveguide makers. SiC's high refractive index makes it a highly promising material. Currently, Chinese SiC substrates are mainly 4- and 6-inch, but cost efficiency is driving a shift to larger sizes. By 2030, shipments of 8-inch SiC wafers are expected to exceed 20%, with 12-inch development on the horizon. This will further accelerate the adoption of PL technology.

AR Brand Strategies and Specification Trends

As AR optical engine modules shrink, specifications are converging and limiting differentiation. CMOS substrate sizes and designs are trending toward standardization to manage costs. Currently, most LEDoS and LCoS panels range from 0.13-0.18 inches, with pixel densities exceeding 5,500 PPI. LEDoS resolutions typically range 640x480 to 720x720, while LCoS panels generally sit at 720x720. This has pushed brands to pursue distinct strategic directions.

Xreal is focused on display technology and algorithms to expand FOV and enhance computing performance, and RayNeo is strengthening its OLEDoS + Birdbath solution for media consumption while advancing full-color LEDoS + waveguide AR glasses. Meanwhile, INMO is prioritizing all-in-one AI-driven AR terminals and Meta plans to build a full product lineup and invest heavily in AI capabilities to counter Apple's future market entry.

This trend highlights a shift in the AR market from hardware-only competition to a more integrated hardware-software ecosystem.

Table of Contents

Chapter 1. Near-Eye Display Devices Market Analysis

- 2025-2030 NED Device Shipment Analysis

- 2025-2030 VR/MR Shipment Analysis

- 2025-2030 Global VR/MR Devices Market Share by Technology

- 2025-2030 VR/MR Devices Market Size Analysis: LCD/OLEDoS

- 2025-2030 AR Shipment Analysis

- AR Devices Market Share by Region

- 2025-2030 Global AR Devices Market Share by Technology

- 2025-2030 AR Devices Market Size Analysis: LCD/OLEDoS

Chapter 2. Near-Eye Display Technology Development Trend Analysis

- 2.1. VR/MR Display Technology and Market Trend Analysis

- Native Issue of VST : Geometric Distortion

- Foveation Reduces Data Transmission and Power Consumption

- Brightness Perception Also Focuses on Fovea - Peripheral Dimming

- Foveated VR Display Achieved through Polarization + Pancake

- Solutions in Reducing Power Consumption for LCD

- Losses Generated from Compensation on Pancake by Mini LED Backlight

- Straight Light Lowers Contrast Gain of Mini LED Backlight

- RGB Mini LED Backlight Enter Possible Realm of LCD VR

- Upgrading from Blue Light Mini LED to RGB Mini LED?

- Directional Backlight an Ideal Target of LCD VR

- 12-inch OLEDoS Player Capacity Analysis

- Lateral Comparison of Full-Color OLEDoS Technology

- OLEDoS PPI Cap Elevated by Triple-Nozzle Evaporation System

- Development of VR/MR

- 2.2. AR Display Technology and Market Trend Analysis

- Light Source Specification and Pricing Sweet Spot Analysis

- Multi-Zone Micro/Mini LED Backlight Increases Contrast and Reduces Power Consumption for LCoS

- LCoS Further Shrinking: Planar Optical Technology Ongoing Exploration

- Summarized Development Trends of LCoS Technology

- Challenges in Advancing from X-Cube to Single-Chip Full-Color for LEDoS

- Drivers Behind Transition from X-Cube to Single-Chip Full-Color Solution for LEDoS

- Lateral Comparison of Full-Color LEDoS Technology

- Lateral Comparison of Full-Color LEDoS Technology-Vertical Stacking

- Vertical Stacking LEDoS Key Technology Analysis- Seoul Viosys / JBD

- Lateral Comparison of Full-Color LEDoS Technology-InGaN

- CMOS Driving Backplanes of Microdisplays Marching to 12-inch

- Technical Challenges on CMOS for LEDoS from Backplane Designs to System Integration

- Chip Bonding Process Analysis

- Wafer Bonding Process Analysis

- Sony Semiconductor Also Proposed D2W2W for LEDoS

- LEDoS Player Capacity Analysis

- LCoS vs LEDoS

- Power consumption comparison between LEDoS and LCoS

- Analysis on Specifications of LEDoS and LCoS Displays

- Analysis on Specifications of LEDoS and LCoS Full-Color Light Engines

- 2.3. AR Optical Technology and Market Trend Analysis

- Geometric Waveguide

- Diffractive Waveguide

- Compromises of Diffraction Waveguides in the Three Major Specifications

- The Efficiency Challenges of Diffractive Waveguides

- Nano Imprint Lithography (NIL) vs. Photolithography (PL)

- Thermal NIL vs. UV NIL

- Thermal NIL Challenges

- Rain Technology Adopted with Geometric Optical Waveguide of

- the Polarization System

- Ant Reality Optics - Mixed Waveguide

- Pros and Cons of Combiner Technology

- Meta waveguide patent strategy

- AUO and BOE Both Involved in SRG Waveguide

- 2.4. SiC Optical Wavegudie Technology and Market Trend Analysis

- Meta Orion AR:SiC Optical Wavegudie + Dual-sided Grating

- Feasibility and limitation of SiC waveguide applications

- AR Glasses Output by SiC Wafer Size

- SiC Wafer Market Analysis

- SiC Industry Chain Manufacturers

- 2.5. AR System Technology and Market Trend Analysis

- Emerging Technology: Eye Tracking in Near-Eye Displays

- AR/VR - Analysis on Advantages of Eye Tracking

- Eye Tracking - PCCR vs. Al Image Analysis

- Eye Tracking - Analysis on Brand Strategies and Value Chain

- SoC

Chapter 3. Global AR Product Development Trend Analysis

- 3.1. AR Product Development Trend Analysis in China

- Development of AR

- China AR Brand-Xreal

- China AR Brand-RayNeo

- China AR Brand-INMO

- China AR Brand- Rokid / MEIZU

- China AR Glasses Comparison: Weight/Display Technology

- China AR Glasses Comparison: Price/Display Technology

- 3.2. AR Product Development Trend Analysis - Non China

- AI/AR Glasses Roadmap

- Non China AI/AR Glasses Comparison

- Development of AR glasses from 2014 to 2024

- Non China AR glasses Full-color Display Technology

Chapter 4. Player Dynamic Updates

- VR/MR Supply Chain

- Seeya

- Sidtek

- BOE Achieved Milestone of Double 5K for 0.9-inch OLEDoS

- AR Supply Chain

- EV Group

- Porotech

- Polar Light Technologies AB (PLT)

- Q Pixel

- Micledi Microdisplays

- VueReal

- JBD

- Hongshi

- Raysolve

- Giga-Image

- GIS /JorJin

- Himax

- Meta

- Snap

近眼显示市场 - 全球产业规模、份额、趋势、机会及预测(按组件、设备类型、技术、最终用户、地区和竞争格局划分,2021-2031年)

近眼显示市场 - 全球产业规模、份额、趋势、机会及预测(按组件、设备类型、技术、最终用户、地区和竞争格局划分,2021-2031年) 近眼显示器市场按显示器类型、设备类型、视角、连接性、应用和分销管道划分 - 全球预测,2025-2030 年

近眼显示器市场按显示器类型、设备类型、视角、连接性、应用和分销管道划分 - 全球预测,2025-2030 年 全球近眼显示器市场

全球近眼显示器市场 近眼显示市场规模、份额及趋势分析报告(按显示技术、设备类型、最终用途、地区及细分市场预测,2025 年至 2033 年)

近眼显示市场规模、份额及趋势分析报告(按显示技术、设备类型、最终用途、地区及细分市场预测,2025 年至 2033 年) 近眼显示器市场,规模,占有率,产业分析报告:各亮度等级,各零件,各技术,不同设备类型,各业界,各地区-2025年~2034年市场预测全球近眼设备 Micro LED 市场

近眼显示器市场,规模,占有率,产业分析报告:各亮度等级,各零件,各技术,不同设备类型,各业界,各地区-2025年~2034年市场预测全球近眼设备 Micro LED 市场 近眼显示器市场(按技术、设备类型、解析度、垂直领域和地区)- 预测至 2030 年

近眼显示器市场(按技术、设备类型、解析度、垂直领域和地区)- 预测至 2030 年 近眼显示器市场报告:趋势、预测和竞争分析(至 2031 年)

近眼显示器市场报告:趋势、预测和竞争分析(至 2031 年) 2030 年近眼显示器市场预测:按组件、解析度、技术、应用、最终用户和地区进行的全球分析

2030 年近眼显示器市场预测:按组件、解析度、技术、应用、最终用户和地区进行的全球分析 近眼显示器市场、机会、成长动力、产业趋势分析与预测,2024-2032

近眼显示器市场、机会、成长动力、产业趋势分析与预测,2024-2032