|

市场调查报告书

商品编码

1365687

纯素巧克力市场:按类型、按产品、配销通路:2023-2032 年全球机会分析与产业预测Vegan Chocolate Market By Type, By Product, By Distribution Channel : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

2022 年纯素巧克力市场价值为 5.858 亿美元,预计到 2032 年将达到 20 亿美元,2023 年至 2032 年年复合成长率为 13.1%。

纯素巧克力是一种不含任何动物性成分的巧克力。传统巧克力通常含有牛奶或乳固态、乳脂等成分,有时也含有其他动物性添加剂。相较之下,纯素巧克力是用精心挑选的成分製成的,不含动物剥削或动物按产品。纯素巧克力中常见的乳製品替代品包括植物奶,如杏仁奶、豆奶、椰奶、燕麦奶和米奶。纯素巧克力也可以使用可可脂或椰子油等植物性脂肪来取代普通乳脂。

现今的消费者俱有健康意愿,并积极寻找符合其饮食偏好和目标的食品。不含乳製品和鸡蛋的纯素巧克力吸引了那些想要享受巧克力这种奢华享受同时减少饱和脂肪、胆固醇和过敏原摄入量的人。此外,素食和植物性饮食的日益普及也大大增加了对纯素巧克力的需求。出于道德、环境和健康原因,许多人采用纯素生活方式。纯素巧克力符合这些饮食选择,是传统巧克力的无罪恶感替代品。此外,食物过敏和不耐受在现代社会很普遍。乳製品和鸡蛋是常见的过敏原,但纯素巧克力不含这些成分,因此适合有特定用餐限制和偏好的人。透过提供不含乳製品和不含鸡蛋的选择,纯素巧克力迎合了更广泛的消费者群体,包括乳糖不耐症、牛奶过敏和鸡蛋过敏的消费者。

纯素巧克力通常使用优质原料并以道德和永续的方式生产,但生产成本可能更高。对价格敏感的消费者通常会优先考虑预算选择。由于製造成本较高,包括采购优质原料以及维持道德和永续实践,纯素巧克力的零售价通常较高。这使得纯素巧克力对于预算有限的消费者来说遥不可及。消费者可能不完全理解道德和永续做法带来的付加,因此可能不愿意为纯素巧克力替代品支付高价。

随着素食主义和植物性饮食变得越来越流行,需要更多种类的纯素巧克力产品。公司可以透过引入新口味、质地和形式的纯素巧克力来探索扩大产品线的机会。这包括纯素牛奶巧克力、黑巧克力、夹心巧克力和松露等选项。此外,许多消费者出于健康原因采用植物性饮食,并寻求不含动物成分、胆固醇和其他潜在过敏原的产品。采用有机和公平贸易可可、天然甜味剂和超级食品添加剂等优质原料製成的纯素巧克力可以吸引註重健康的人。公司可以透过强调纯素巧克力的高营养价值、低饱和脂肪含量和潜在的抗氧化特性来宣传纯素巧克力的健康益处。对纯素巧克力不断增长的需求为企业提供了充足的机会,可以满足消费者对植物来源替代不断变化的偏好。透过了解消费者动机,专注于品质、道德和环境永续性,并采用创新的行销策略,公司可以将自己定位为这个新兴市场的领导者。Masu。

COVID-19大流行对纯素巧克力市场产生了重大影响。在疫情期间,人们对健康和保健的兴趣增加导致对植物来源和纯素产品(包括纯素巧克力)的需求增加。许多消费者正在寻找更健康、更永续的替代,而纯素巧克力正好符合这一趋势。此外,疫情也扰乱了全球供应链,影响了原料的供应和采购。这种中断影响了一些纯素巧克力製造商,特别是那些依赖进口原料或面临运输挑战的製造商。然而,这种影响的程度可能会有所不同,具体取决于每个公司的特定供应链设定。此外,随着封锁和社交距离措施的实施,网上购物也发生了重大转变。这项变革使得许多纯素巧克力公司能够透过电子商务平台直接接触消费者。儘管市场面临挑战,适应这一趋势并投资线上业务的公司仍然实现了成长。

目录

第1章简介

第2章执行摘要

第3章市场概况

- 市场定义和范围

- 主要发现

- 影响要素

- 主要投资机会

- 波特五力分析

- 市场动态

- 促进因素

- 抑制因素

- 机会

- COVID-19 市场影响分析

- 市场占有率分析

- 品牌占有率分析

- 价值链分析

- 法规指引

- 专利形势

第4章纯素巧克力市场:依类型

- 概述

- 黑暗的

- 牛奶

- 白色的

第5章纯素巧克力市场:按产品

- 概述

- 模压棒

- 薯条和叮咬

- 盒装

第6章纯素巧克力市场:依配销通路

- 概述

- 大型超市/超市

- 专卖店

- 网路商城

- 便利商店

第7章纯素巧克力市场:依地区

- 概述

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 奥地利

- 瑞士

- 瑞典

- 其他的

- 亚太地区

- 台湾

- 纽西兰

- 印度

- 新加坡

- 澳洲

- 其他的

- 拉丁美洲/中东/非洲

- 巴西

- 阿拉伯聯合大公国

- 智利

- 南非

- 其他的

第8章竞争形势

- 介绍

- 关键成功策略

- 10家主要企业产品图谱

- 竞争仪表板

- 竞争热图

- 2022年主要企业定位

第9章公司简介

- Alter Eco

- MondelA"z International

- Barry Callebaut

- Nestle SA

- Endorfin Foods

- Evolved Chocolate

- Chocoladefabriken Lindt & Sprungli AG

- taza chocolate

- Montezuma's Direct Ltd.

- Endangered Species Chocolate, LLC.

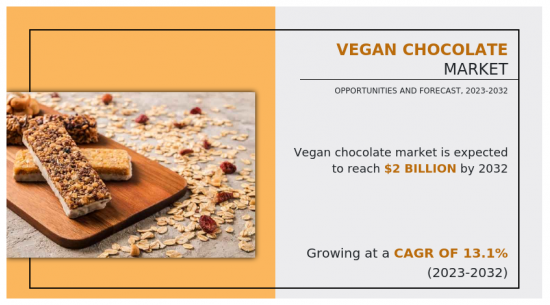

According to a new report published by Allied Market Research, titled, "Vegan Chocolate Market," The vegan chocolate market was valued at $585.80 million in 2022, and is estimated to reach $2 billion by 2032, growing at a CAGR of 13.1% from 2023 to 2032. Vegan chocolate refers to a kind of chocolate that is completely free from any animal-derived ingredients. Traditional chocolate normally contains ingredients like milk or milk solids, butterfat, and sometimes even other additives that may also come from animals. In contrast vegan chocolate is made with choice ingredients that do not contain animal exploitation or animal by-products. Common substitutes for dairy milk in vegan chocolate include plant-based milks such as almond milk, soy milk, coconut milk, oat milk, or rice milk. Instead of normal butterfat, vegan chocolate might also use plant-based fat like cocoa butter or coconut oil.

Consumers today are more health-conscious and are actively seeking out food products that align with their dietary preferences and goals. Vegan chocolate, made without dairy and eggs, appeals to those who want to enjoy chocolate as an indulgent treat while reducing their intake of saturated fats, cholesterol, and allergens. Moreover, the growing popularity of veganism and plant-based diets has significantly contributed to the demand for vegan chocolate. Many people are adopting vegan lifestyles for ethical, environmental, and health reasons. Vegan chocolate aligns with these dietary choices and provides a guilt-free alternative to traditional chocolate options. Furthermore, food allergies and intolerances are prevalent in today's society. Dairy and eggs are common allergens, and vegan chocolate eliminates these ingredients, making it suitable for individuals with specific dietary restrictions or preferences. By offering a dairy-free and egg-free option, vegan chocolate caters to a broader consumer base, including those with lactose intolerance, milk allergies, or egg allergies.

Vegan chocolates often use high-quality ingredients and are produced using ethical and sustainable practices, which can increase its production costs. Price-sensitive consumers typically prioritize budget-friendly options. The higher production costs associated with vegan chocolates, which include sourcing high-quality ingredients and maintaining ethical and sustainable practices, often lead to higher retail prices. This can make vegan chocolates less affordable for consumers with a tight budget. They might not fully appreciate the added value of ethical and sustainable practices, resulting in a reluctance to pay a premium for vegan alternatives.

With the increasing popularity of veganism and plant-based diets, there is a need for a wider variety of vegan chocolate products. Businesses can explore opportunities to expand their product lines by introducing new flavors, textures, and formats of vegan chocolate. This can include options such as vegan milk chocolate, dark chocolate, filled chocolates, truffles, and others. Moreover, many consumers are adopting plant-based diets for health reasons, seeking products that are free from animal ingredients, cholesterol, and other potential allergens. Vegan chocolate made with high-quality ingredients, such as organic or fair-trade cocoa, natural sweeteners, and superfood additions, can appeal to health-conscious individuals. Businesses can promote the health benefits of their vegan chocolate, emphasizing its nutritional value, lower saturated fat content, and potential antioxidant properties. The rising demand for vegan chocolate provides ample opportunities for businesses to cater to the evolving preferences of consumers seeking plant-based alternatives. By understanding consumer motivations, focusing on quality, ethics, and environmental sustainability, and adopting innovative marketing strategies, businesses can position themselves as leaders in this developing market.

The COVID-19 pandemic has had significant impacts on the market for vegan chocolate. During the pandemic, there has been a growing interest in health & wellness, which has led to an increase in demand for plant-based and vegan products, including vegan chocolates. Many consumers are seeking healthier and sustainable alternatives, and vegan chocolate fits into this trend. Moreover, the pandemic disrupted global supply chains, impacting the availability and sourcing of ingredients. This disruption affected some vegan chocolate manufacturers, particularly those relying on imported ingredients or facing transportation challenges. However, the extent of this impact may vary depending on the specific supply chain setup of each business. Furthermore, with lockdowns and social distancing measures in place, there has been a significant shift towards online shopping. This change has allowed many vegan chocolate companies to reach consumers directly through e-commerce platforms. Businesses that adapted to this trend and invested in their online presence experienced growth despite the overall market challenges.

The key players profiled in this report include: Alter Eco, Mondelez International, Barry Callebaut, Nestle, Endorfin Foods, Evolved Chocolate, Chocoladefabriken Lindt & Sprungli AG, Taza Chocolate, Montezuma's Direct Ltd., and Endangered Species Chocolate, LLC. The market players are continuously striving to achieve a dominant position in this competitive market using strategies such as collaborations and acquisitions.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the vegan chocolate market analysis from 2022 to 2032 to identify the prevailing vegan chocolate market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the vegan chocolate market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global vegan chocolate market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 20% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline talk to the sales executive to know more)

- Product Benchmarking / Product specification and applications

- Technology Trend Analysis

- Market share analysis of players by products/segments

- New Product Development/ Product Matrix of Key Players

- Regulatory Guidelines

- Strategic Recommedations

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Criss-cross segment analysis- market size and forecast

- Expanded list for Company Profiles

- Historic market data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- Market share analysis of players at global/region/country level

- SWOT Analysis

Key Market Segments

By Product

- Chips and Bites

- Boxed

- Molded Bars

By Type

- Dark

- Milk

- White

By Distribution Channel

- Hypermarkets/Supermarkets

- Specialty Stores

- Online Stores

- Convenience Stores

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- Austria

- Switzerland

- Sweden

- Rest of Europe

- Asia-Pacific

- Taiwan

- New Zealand

- India

- Singapore

- Australia

- Rest of Europe

- LAMEA

- Brazil

- United Arab Emirates

- Chile

- South Africa

- Rest of LAMEA

Key Market Players:

- Alter Eco

- Barry Callebaut

- Chocoladefabriken Lindt & Sprungli AG

- Endangered Species Chocolate, LLC.

- Endorfin Foods

- Evolved Chocolate

- MondelA"z International

- Montezuma's Direct Ltd.

- Nestle S.A.

- taza chocolate

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Market Share Analysis

- 3.7. Brand Share Analysis

- 3.8. Value Chain Analysis

- 3.9. Regulatory Guidelines

- 3.10. Patent Landscape

CHAPTER 4: VEGAN CHOCOLATE MARKET, BY TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Dark

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Milk

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. White

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

CHAPTER 5: VEGAN CHOCOLATE MARKET, BY PRODUCT

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Molded Bars

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Chips and Bites

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Boxed

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

CHAPTER 6: VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Hypermarkets/Supermarkets

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Specialty Stores

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Online Stores

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

- 6.5. Convenience Stores

- 6.5.1. Key market trends, growth factors and opportunities

- 6.5.2. Market size and forecast, by region

- 6.5.3. Market share analysis by country

CHAPTER 7: VEGAN CHOCOLATE MARKET, BY REGION

- 7.1. Overview

- 7.1.1. Market size and forecast By Region

- 7.2. North America

- 7.2.1. Key trends and opportunities

- 7.2.2. Market size and forecast, by Type

- 7.2.3. Market size and forecast, by Product

- 7.2.4. Market size and forecast, by Distribution Channel

- 7.2.5. Market size and forecast, by country

- 7.2.5.1. U.S.

- 7.2.5.1.1. Key market trends, growth factors and opportunities

- 7.2.5.1.2. Market size and forecast, by Type

- 7.2.5.1.3. Market size and forecast, by Product

- 7.2.5.1.4. Market size and forecast, by Distribution Channel

- 7.2.5.2. Canada

- 7.2.5.2.1. Key market trends, growth factors and opportunities

- 7.2.5.2.2. Market size and forecast, by Type

- 7.2.5.2.3. Market size and forecast, by Product

- 7.2.5.2.4. Market size and forecast, by Distribution Channel

- 7.2.5.3. Mexico

- 7.2.5.3.1. Key market trends, growth factors and opportunities

- 7.2.5.3.2. Market size and forecast, by Type

- 7.2.5.3.3. Market size and forecast, by Product

- 7.2.5.3.4. Market size and forecast, by Distribution Channel

- 7.3. Europe

- 7.3.1. Key trends and opportunities

- 7.3.2. Market size and forecast, by Type

- 7.3.3. Market size and forecast, by Product

- 7.3.4. Market size and forecast, by Distribution Channel

- 7.3.5. Market size and forecast, by country

- 7.3.5.1. Germany

- 7.3.5.1.1. Key market trends, growth factors and opportunities

- 7.3.5.1.2. Market size and forecast, by Type

- 7.3.5.1.3. Market size and forecast, by Product

- 7.3.5.1.4. Market size and forecast, by Distribution Channel

- 7.3.5.2. UK

- 7.3.5.2.1. Key market trends, growth factors and opportunities

- 7.3.5.2.2. Market size and forecast, by Type

- 7.3.5.2.3. Market size and forecast, by Product

- 7.3.5.2.4. Market size and forecast, by Distribution Channel

- 7.3.5.3. Austria

- 7.3.5.3.1. Key market trends, growth factors and opportunities

- 7.3.5.3.2. Market size and forecast, by Type

- 7.3.5.3.3. Market size and forecast, by Product

- 7.3.5.3.4. Market size and forecast, by Distribution Channel

- 7.3.5.4. Switzerland

- 7.3.5.4.1. Key market trends, growth factors and opportunities

- 7.3.5.4.2. Market size and forecast, by Type

- 7.3.5.4.3. Market size and forecast, by Product

- 7.3.5.4.4. Market size and forecast, by Distribution Channel

- 7.3.5.5. Sweden

- 7.3.5.5.1. Key market trends, growth factors and opportunities

- 7.3.5.5.2. Market size and forecast, by Type

- 7.3.5.5.3. Market size and forecast, by Product

- 7.3.5.5.4. Market size and forecast, by Distribution Channel

- 7.3.5.6. Rest of Europe

- 7.3.5.6.1. Key market trends, growth factors and opportunities

- 7.3.5.6.2. Market size and forecast, by Type

- 7.3.5.6.3. Market size and forecast, by Product

- 7.3.5.6.4. Market size and forecast, by Distribution Channel

- 7.4. Asia-Pacific

- 7.4.1. Key trends and opportunities

- 7.4.2. Market size and forecast, by Type

- 7.4.3. Market size and forecast, by Product

- 7.4.4. Market size and forecast, by Distribution Channel

- 7.4.5. Market size and forecast, by country

- 7.4.5.1. Taiwan

- 7.4.5.1.1. Key market trends, growth factors and opportunities

- 7.4.5.1.2. Market size and forecast, by Type

- 7.4.5.1.3. Market size and forecast, by Product

- 7.4.5.1.4. Market size and forecast, by Distribution Channel

- 7.4.5.2. New Zealand

- 7.4.5.2.1. Key market trends, growth factors and opportunities

- 7.4.5.2.2. Market size and forecast, by Type

- 7.4.5.2.3. Market size and forecast, by Product

- 7.4.5.2.4. Market size and forecast, by Distribution Channel

- 7.4.5.3. India

- 7.4.5.3.1. Key market trends, growth factors and opportunities

- 7.4.5.3.2. Market size and forecast, by Type

- 7.4.5.3.3. Market size and forecast, by Product

- 7.4.5.3.4. Market size and forecast, by Distribution Channel

- 7.4.5.4. Singapore

- 7.4.5.4.1. Key market trends, growth factors and opportunities

- 7.4.5.4.2. Market size and forecast, by Type

- 7.4.5.4.3. Market size and forecast, by Product

- 7.4.5.4.4. Market size and forecast, by Distribution Channel

- 7.4.5.5. Australia

- 7.4.5.5.1. Key market trends, growth factors and opportunities

- 7.4.5.5.2. Market size and forecast, by Type

- 7.4.5.5.3. Market size and forecast, by Product

- 7.4.5.5.4. Market size and forecast, by Distribution Channel

- 7.4.5.6. Rest of Europe

- 7.4.5.6.1. Key market trends, growth factors and opportunities

- 7.4.5.6.2. Market size and forecast, by Type

- 7.4.5.6.3. Market size and forecast, by Product

- 7.4.5.6.4. Market size and forecast, by Distribution Channel

- 7.5. LAMEA

- 7.5.1. Key trends and opportunities

- 7.5.2. Market size and forecast, by Type

- 7.5.3. Market size and forecast, by Product

- 7.5.4. Market size and forecast, by Distribution Channel

- 7.5.5. Market size and forecast, by country

- 7.5.5.1. Brazil

- 7.5.5.1.1. Key market trends, growth factors and opportunities

- 7.5.5.1.2. Market size and forecast, by Type

- 7.5.5.1.3. Market size and forecast, by Product

- 7.5.5.1.4. Market size and forecast, by Distribution Channel

- 7.5.5.2. United Arab Emirates

- 7.5.5.2.1. Key market trends, growth factors and opportunities

- 7.5.5.2.2. Market size and forecast, by Type

- 7.5.5.2.3. Market size and forecast, by Product

- 7.5.5.2.4. Market size and forecast, by Distribution Channel

- 7.5.5.3. Chile

- 7.5.5.3.1. Key market trends, growth factors and opportunities

- 7.5.5.3.2. Market size and forecast, by Type

- 7.5.5.3.3. Market size and forecast, by Product

- 7.5.5.3.4. Market size and forecast, by Distribution Channel

- 7.5.5.4. South Africa

- 7.5.5.4.1. Key market trends, growth factors and opportunities

- 7.5.5.4.2. Market size and forecast, by Type

- 7.5.5.4.3. Market size and forecast, by Product

- 7.5.5.4.4. Market size and forecast, by Distribution Channel

- 7.5.5.5. Rest of LAMEA

- 7.5.5.5.1. Key market trends, growth factors and opportunities

- 7.5.5.5.2. Market size and forecast, by Type

- 7.5.5.5.3. Market size and forecast, by Product

- 7.5.5.5.4. Market size and forecast, by Distribution Channel

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top winning strategies

- 8.3. Product Mapping of Top 10 Player

- 8.4. Competitive Dashboard

- 8.5. Competitive Heatmap

- 8.6. Top player positioning, 2022

CHAPTER 9: COMPANY PROFILES

- 9.1. Alter Eco

- 9.1.1. Company overview

- 9.1.2. Key Executives

- 9.1.3. Company snapshot

- 9.2. MondelA"z International

- 9.2.1. Company overview

- 9.2.2. Key Executives

- 9.2.3. Company snapshot

- 9.3. Barry Callebaut

- 9.3.1. Company overview

- 9.3.2. Key Executives

- 9.3.3. Company snapshot

- 9.4. Nestle S.A.

- 9.4.1. Company overview

- 9.4.2. Key Executives

- 9.4.3. Company snapshot

- 9.5. Endorfin Foods

- 9.5.1. Company overview

- 9.5.2. Key Executives

- 9.5.3. Company snapshot

- 9.6. Evolved Chocolate

- 9.6.1. Company overview

- 9.6.2. Key Executives

- 9.6.3. Company snapshot

- 9.7. Chocoladefabriken Lindt & Sprungli AG

- 9.7.1. Company overview

- 9.7.2. Key Executives

- 9.7.3. Company snapshot

- 9.8. taza chocolate

- 9.8.1. Company overview

- 9.8.2. Key Executives

- 9.8.3. Company snapshot

- 9.9. Montezuma's Direct Ltd.

- 9.9.1. Company overview

- 9.9.2. Key Executives

- 9.9.3. Company snapshot

- 9.10. Endangered Species Chocolate, LLC.

- 9.10.1. Company overview

- 9.10.2. Key Executives

- 9.10.3. Company snapshot

LIST OF TABLES

- TABLE 01. GLOBAL VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 02. VEGAN CHOCOLATE MARKET FOR DARK, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. VEGAN CHOCOLATE MARKET FOR MILK, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. VEGAN CHOCOLATE MARKET FOR WHITE, BY REGION, 2022-2032 ($MILLION)

- TABLE 05. GLOBAL VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 06. VEGAN CHOCOLATE MARKET FOR MOLDED BARS, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. VEGAN CHOCOLATE MARKET FOR CHIPS AND BITES, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. VEGAN CHOCOLATE MARKET FOR BOXED, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. GLOBAL VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 10. VEGAN CHOCOLATE MARKET FOR HYPERMARKETS/SUPERMARKETS, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. VEGAN CHOCOLATE MARKET FOR SPECIALTY STORES, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. VEGAN CHOCOLATE MARKET FOR ONLINE STORES, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. VEGAN CHOCOLATE MARKET FOR CONVENIENCE STORES, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. VEGAN CHOCOLATE MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. NORTH AMERICA VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 16. NORTH AMERICA VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 17. NORTH AMERICA VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 18. NORTH AMERICA VEGAN CHOCOLATE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 19. U.S. VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 20. U.S. VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 21. U.S. VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 22. CANADA VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 23. CANADA VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 24. CANADA VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 25. MEXICO VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 26. MEXICO VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 27. MEXICO VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 28. EUROPE VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 29. EUROPE VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 30. EUROPE VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 31. EUROPE VEGAN CHOCOLATE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 32. GERMANY VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 33. GERMANY VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 34. GERMANY VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 35. UK VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 36. UK VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 37. UK VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 38. AUSTRIA VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 39. AUSTRIA VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 40. AUSTRIA VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 41. SWITZERLAND VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 42. SWITZERLAND VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 43. SWITZERLAND VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 44. SWEDEN VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 45. SWEDEN VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 46. SWEDEN VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 47. REST OF EUROPE VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 48. REST OF EUROPE VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 49. REST OF EUROPE VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 50. ASIA-PACIFIC VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 51. ASIA-PACIFIC VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 52. ASIA-PACIFIC VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 53. ASIA-PACIFIC VEGAN CHOCOLATE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 54. TAIWAN VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 55. TAIWAN VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 56. TAIWAN VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 57. NEW ZEALAND VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 58. NEW ZEALAND VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 59. NEW ZEALAND VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 60. INDIA VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 61. INDIA VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 62. INDIA VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 63. SINGAPORE VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 64. SINGAPORE VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 65. SINGAPORE VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 66. AUSTRALIA VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 67. AUSTRALIA VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 68. AUSTRALIA VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 69. REST OF EUROPE VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 70. REST OF EUROPE VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 71. REST OF EUROPE VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 72. LAMEA VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 73. LAMEA VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 74. LAMEA VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 75. LAMEA VEGAN CHOCOLATE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 76. BRAZIL VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 77. BRAZIL VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 78. BRAZIL VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 79. UNITED ARAB EMIRATES VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 80. UNITED ARAB EMIRATES VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 81. UNITED ARAB EMIRATES VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 82. CHILE VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 83. CHILE VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 84. CHILE VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 85. SOUTH AFRICA VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 86. SOUTH AFRICA VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 87. SOUTH AFRICA VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 88. REST OF LAMEA VEGAN CHOCOLATE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 89. REST OF LAMEA VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 90. REST OF LAMEA VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 91. ALTER ECO: KEY EXECUTIVES

- TABLE 92. ALTER ECO: COMPANY SNAPSHOT

- TABLE 93. MONDELA"Z INTERNATIONAL: KEY EXECUTIVES

- TABLE 94. MONDELA"Z INTERNATIONAL: COMPANY SNAPSHOT

- TABLE 95. BARRY CALLEBAUT: KEY EXECUTIVES

- TABLE 96. BARRY CALLEBAUT: COMPANY SNAPSHOT

- TABLE 97. NESTLE S.A.: KEY EXECUTIVES

- TABLE 98. NESTLE S.A.: COMPANY SNAPSHOT

- TABLE 99. ENDORFIN FOODS: KEY EXECUTIVES

- TABLE 100. ENDORFIN FOODS: COMPANY SNAPSHOT

- TABLE 101. EVOLVED CHOCOLATE: KEY EXECUTIVES

- TABLE 102. EVOLVED CHOCOLATE: COMPANY SNAPSHOT

- TABLE 103. CHOCOLADEFABRIKEN LINDT & SPRUNGLI AG: KEY EXECUTIVES

- TABLE 104. CHOCOLADEFABRIKEN LINDT & SPRUNGLI AG: COMPANY SNAPSHOT

- TABLE 105. TAZA CHOCOLATE: KEY EXECUTIVES

- TABLE 106. TAZA CHOCOLATE: COMPANY SNAPSHOT

- TABLE 107. MONTEZUMA'S DIRECT LTD.: KEY EXECUTIVES

- TABLE 108. MONTEZUMA'S DIRECT LTD.: COMPANY SNAPSHOT

- TABLE 109. ENDANGERED SPECIES CHOCOLATE, LLC.: KEY EXECUTIVES

- TABLE 110. ENDANGERED SPECIES CHOCOLATE, LLC.: COMPANY SNAPSHOT

LIST OF FIGURES

- FIGURE 01. VEGAN CHOCOLATE MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF VEGAN CHOCOLATE MARKET, 2022-2032

- FIGURE 03. VEGAN CHOCOLATE MARKET,2022-2032

- FIGURE 04. TOP INVESTMENT POCKETS IN VEGAN CHOCOLATE MARKET (2023-2032)

- FIGURE 05. BARGAINING POWER OF SUPPLIERS

- FIGURE 06. BARGAINING POWER OF BUYERS

- FIGURE 07. THREAT OF SUBSTITUTION

- FIGURE 08. THREAT OF SUBSTITUTION

- FIGURE 09. COMPETITIVE RIVALRY

- FIGURE 10. GLOBAL VEGAN CHOCOLATE MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. REGULATORY GUIDELINES: VEGAN CHOCOLATE MARKET

- FIGURE 12. PATENT ANALYSIS BY COMPANY

- FIGURE 13. PATENT ANALYSIS BY COUNTRY

- FIGURE 14. VEGAN CHOCOLATE MARKET, BY TYPE, 2022(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR DARK, BY COUNTRY 2022-2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR MILK, BY COUNTRY 2022-2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR WHITE, BY COUNTRY 2022-2032(%)

- FIGURE 18. VEGAN CHOCOLATE MARKET, BY PRODUCT, 2022(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR MOLDED BARS, BY COUNTRY 2022-2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR CHIPS AND BITES, BY COUNTRY 2022-2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR BOXED, BY COUNTRY 2022-2032(%)

- FIGURE 22. VEGAN CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2022(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR HYPERMARKETS/SUPERMARKETS, BY COUNTRY 2022-2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR SPECIALTY STORES, BY COUNTRY 2022-2032(%)

- FIGURE 25. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR ONLINE STORES, BY COUNTRY 2022-2032(%)

- FIGURE 26. COMPARATIVE SHARE ANALYSIS OF VEGAN CHOCOLATE MARKET FOR CONVENIENCE STORES, BY COUNTRY 2022-2032(%)

- FIGURE 27. VEGAN CHOCOLATE MARKET BY REGION, 2022

- FIGURE 28. U.S. VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 29. CANADA VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 30. MEXICO VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 31. GERMANY VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 32. UK VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 33. AUSTRIA VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 34. SWITZERLAND VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 35. SWEDEN VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 36. REST OF EUROPE VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 37. TAIWAN VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 38. NEW ZEALAND VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 39. INDIA VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 40. SINGAPORE VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 41. AUSTRALIA VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 42. REST OF EUROPE VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 43. BRAZIL VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 44. UNITED ARAB EMIRATES VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 45. CHILE VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 46. SOUTH AFRICA VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 47. REST OF LAMEA VEGAN CHOCOLATE MARKET, 2022-2032 ($MILLION)

- FIGURE 48. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 49. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 50. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 51. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 52. COMPETITIVE DASHBOARD

- FIGURE 53. COMPETITIVE HEATMAP: VEGAN CHOCOLATE MARKET

- FIGURE 54. TOP PLAYER POSITIONING, 2022

全球纯素巧克力市场

全球纯素巧克力市场 纯素巧克力棒市场报告:2031 年趋势、预测与竞争分析

纯素巧克力棒市场报告:2031 年趋势、预测与竞争分析 素食巧克力市场 - 全球产业分析、规模、占有率、成长、趋势及2032年预测纯素巧克力市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

素食巧克力市场 - 全球产业分析、规模、占有率、成长、趋势及2032年预测纯素巧克力市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 纯素巧克力市场评估:依类型、形状、风味、最终用户、分销管道和地区划分的机会和预测(2017-2031)

纯素巧克力市场评估:依类型、形状、风味、最终用户、分销管道和地区划分的机会和预测(2017-2031) 全球纯素巧克力市场规模、份额、产业趋势分析报告:2023-2030 年按配销通路、类型和地区分類的展望和预测

全球纯素巧克力市场规模、份额、产业趋势分析报告:2023-2030 年按配销通路、类型和地区分類的展望和预测 纯素巧克力市场 - 2018-2028F 全球产业规模、份额、趋势、机会和预测,按类型、类别(盒装、条状、计数线等)、按地区、竞争的配销通路细分

纯素巧克力市场 - 2018-2028F 全球产业规模、份额、趋势、机会和预测,按类型、类别(盒装、条状、计数线等)、按地区、竞争的配销通路细分 全球纯素巧克力市场 - 2023-2030 年

全球纯素巧克力市场 - 2023-2030 年