|

市场调查报告书

商品编码

1684587

婴幼儿玩具市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Infants and Toddlers Toy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

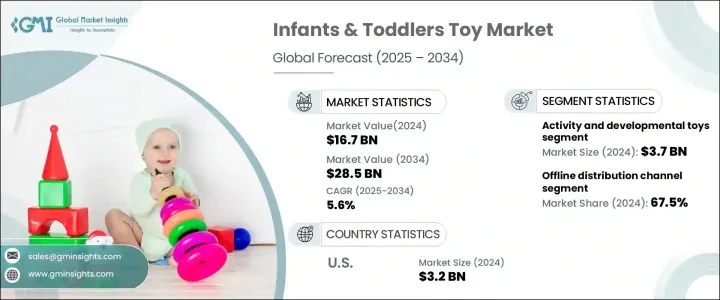

2024 年全球婴幼儿玩具市场规模达到 167 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.6%。旨在增强运动技能、促进早期学习和提高解决问题能力的玩具已成为致力于支持孩子成长和认知发展的父母的首要任务。人们越来越意识到早期儿童发展的重要性以及玩具在其中的作用,这正在重塑购买行为。此外,随着全球中产阶级的崛起和新兴市场的购买力不断增强,越来越多的家长开始投资购买对孩子的学习过程有积极贡献的优质玩具。

婴幼儿玩具市场涵盖多个类别,包括益智玩具、软玩具、活动和发展玩具、骑乘玩具、建筑套装玩具、洗澡玩具等。其中,活动和发展玩具预计将在 2024 年占据主导地位,市占率达到 37 亿美元。由于人们对刺激认知和身体发育的玩具的偏好日益增加,预计 2025 年至 2034 年期间这一细分市场每年将增长 6%。家长们尤其喜欢那些鼓励解决问题和创造力的玩具,因为它们对于早期儿童教育至关重要。因此,这些玩具不仅被视为玩物,也是有价值的教育工具。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 167亿美元 |

| 预测值 | 285亿美元 |

| 复合年增长率 | 5.6% |

婴幼儿玩具的销售管道主要有线上和线下两个。 2024年,线下销售引领市场,占67.5%的市占率。预计 2025 年至 2034 年期间,这一领域的成长率将达到 5.4%。对于父母来说,这一点尤其重要,因为他们在选择玩具时会优先考虑安全性、品质和适合年龄。这些因素极大地影响着购买决策,使得店内购物对于寻求确保孩子成长得到最好的玩具支持的父母来说成为一种宝贵的体验。

2024年,美国以38.2%的份额占据婴幼儿玩具市场的主导地位。强大的消费文化和日益增长的儿童数量助长了这种主导地位。线上线下销售管道均已完善,可满足各种消费者的偏好。同样,在亚太地区,中国在 2024 年占据婴幼儿玩具市场的 31.2% 的显着份额。中国在全球玩具製造业的突出地位也增强了在该市场的地位。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测参数

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 零售商

- 衝击力

- 成长动力

- 人们对早期儿童发展的认识不断提高

- 环保安全玩具受欢迎

- 个性化和可客製化的玩具

- 产业陷阱与挑战

- 仿冒和仿冒品

- 育儿趋势和不断变化的消费者偏好

- 成长动力

- 技术与创新格局

- 消费者购买行为分析

- 人口趋势

- 影响购买决策的因素

- 消费者产品采用

- 首选配销通路

- 成长潜力分析

- 监管格局

- 定价分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按产品类型,2021 年至 2034 年

- 主要趋势

- 益智玩具

- 绒毛玩具

- 活动和发展玩具

- 骑乘玩具

- 建筑套件

- 洗澡玩具

- 其他(出牙玩具、拖拉玩具)

第 6 章:市场估计与预测:依材料类型,2021 年至 2034 年

- 主要趋势

- 塑胶

- 木製的

- 布料/布料

- 硅胶/橡胶

- 环保材料(如竹子、再生材料)

第七章:市场估计与预测:依年龄组,2021 – 2034 年

- 主要趋势

- 0–6个月

- 6-12个月

- 1-2岁

- 2–4 岁

第 8 章:市场估计与预测:按价格,2021 年至 2034 年

- 主要趋势

- 低的

- 中等的

- 高的

第 9 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 在线的

- 电子商务平台

- 品牌网站

- 离线

- 超市/大卖场

- 玩具专卖店

- 百货公司

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 马来西亚

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 沙乌地阿拉伯

- 阿联酋

- 南非

第 11 章:公司简介

- Mattel, Inc.

- Hasbro, Inc.

- Spin Master Corp.

- LEGO Group

- Hamleys

- VTech

- Fisher-Price

- Melissa & Doug

- Little Tikes

- Chicco

- Playmobil

- Tomy

- Clementoni

- Hape

- Janod

The Global Infants And Toddlers Toys Market reached USD 16.7 billion in 2024 and is projected to grow at a CAGR of 5.6% between 2025 and 2034. As more parents and guardians recognize the vital role toys play in the development of young children, the demand for educational and developmental toys continues to rise. Toys designed to enhance motor skills, foster early learning, and promote problem-solving abilities have become a top priority for parents dedicated to supporting their child's growth and cognitive development. The increasing awareness around the importance of early childhood development and the role of engaging toys in it is reshaping buying behaviors. Furthermore, with a rising global middle class and expanding purchasing power in emerging markets, more parents are investing in quality toys that contribute positively to their child's learning process.

The market for infants & toddlers toys spans various categories, including educational, soft, activity and developmental, ride-on, construction sets, bath toys, and others. Among these, activity and developmental toys are expected to dominate in 2024, representing a market share of USD 3.7 billion. This segment is projected to grow by 6% annually from 2025 to 2034, driven by an increasing preference for toys that stimulate both cognitive and physical development. Parents are particularly drawn to toys that encourage problem-solving and creativity, which are essential to early childhood education. As such, these toys are not only seen as playthings but also as valuable tools for educational engagement.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.7 Billion |

| Forecast Value | $28.5 Billion |

| CAGR | 5.6% |

Toys for infants & toddlers are primarily distributed through two channels: online and offline. In 2024, offline sales led the market, accounting for 67.5% of the market share. This segment is expected to experience a growth rate of 5.4% from 2025 to 2034. Physical stores, such as toy retailers, department stores, and supermarkets, offer a key advantage by allowing customers to physically inspect and handle toys before making a purchase. This is especially important for parents, who prioritize safety, quality, and age appropriateness when choosing toys. These factors significantly influence purchasing decisions, making in-store shopping a valuable experience for parents seeking to ensure their child's development is supported by the best possible toys.

In 2024, the U.S. dominated the infants and toddlers toy market with a 38.2% share. The strong consumer culture and the growing number of young children in the country fuel this dominance. Both offline and online sales channels are well-established and cater to a variety of consumer preferences. Similarly, in the Asia-Pacific region, China holds a notable share of 31.2% of the infants & toddlers toy market in 2024. The country benefits from a rapidly expanding child population and a robust domestic production capacity, which supports the growing demand across both urban and rural areas. China's prominent role in the global toy manufacturing sector also enhances its position in this market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing awareness of early childhood development

- 3.2.1.2 Popularity of eco-friendly and safe toys

- 3.2.1.3 Personalized and customizable toys

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Imitation and counterfeit products

- 3.2.2.2 Parenting trends and changing consumer preferences

- 3.2.1 Growth drivers

- 3.3 Technology & innovation landscape

- 3.4 Consumer buying behavior analysis

- 3.4.1 Demographic trends

- 3.4.2 Factors affecting buying decision

- 3.4.3 Consumer product adoption

- 3.4.4 Preferred distribution channel

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.7 Pricing analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 – 2034, (USD Billion)

- 5.1 Key trends

- 5.2 Educational toys

- 5.3 Soft toys

- 5.4 Activity and developmental toys

- 5.5 Ride-on toys

- 5.6 Building sets

- 5.7 Bath toys

- 5.8 Others (teething toys, pull-along toys)

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 – 2034, (USD Billion)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Wooden

- 6.4 Fabric/cloth

- 6.5 Silicone/rubber

- 6.6 Eco-friendly materials (e.g., bamboo, recycled materials)

Chapter 7 Market Estimates & Forecast, By Age Group, 2021 – 2034, (USD Billion)

- 7.1 Key trends

- 7.2 0–6 Months

- 7.3 6–12 Months

- 7.4 1–2 Years

- 7.5 2–4 Years

Chapter 8 Market Estimates & Forecast, By Price, 2021 – 2034, (USD Billion)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 – 2034, (USD Billion)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce platforms

- 9.2.2 Brand websites

- 9.3 Offline

- 9.3.1 Supermarkets/hypermarkets

- 9.3.2 Specialty toy stores

- 9.3.3 Department stores

Chapter 10 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Mattel, Inc.

- 11.2 Hasbro, Inc.

- 11.3 Spin Master Corp.

- 11.4 LEGO Group

- 11.5 Hamleys

- 11.6 VTech

- 11.7 Fisher-Price

- 11.8 Melissa & Doug

- 11.9 Little Tikes

- 11.10 Chicco

- 11.11 Playmobil

- 11.12 Tomy

- 11.13 Clementoni

- 11.14 Hape

- 11.15 Janod

教育玩具市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、最终用户及功能划分

教育玩具市场分析及预测(至2035年):依类型、产品、技术、组件、应用、材料类型、最终用户及功能划分 全球教育玩具市场规模、份额、趋势和成长分析报告(2026-2034)

全球教育玩具市场规模、份额、趋势和成长分析报告(2026-2034) 全球儿童认知发展技术市场:预测(至2034年)-依经营模式、年龄层、通路、技术、应用和地区进行分析

全球儿童认知发展技术市场:预测(至2034年)-依经营模式、年龄层、通路、技术、应用和地区进行分析 教育玩具市场-全球产业规模、份额、趋势、机会、预测:按产品、年龄层、销售管道、地区和竞争格局划分,2021-2031年

教育玩具市场-全球产业规模、份额、趋势、机会、预测:按产品、年龄层、销售管道、地区和竞争格局划分,2021-2031年 按解决方案类型、部署类型、服务类型和最终用户分類的负责任博弈解决方案市场 - 2026-2032 年全球预测STEM玩具市场预测至2032年:按产品类型、类别、年龄层、材料、价格范围、通路和地区分類的全球分析

按解决方案类型、部署类型、服务类型和最终用户分類的负责任博弈解决方案市场 - 2026-2032 年全球预测STEM玩具市场预测至2032年:按产品类型、类别、年龄层、材料、价格范围、通路和地区分類的全球分析 STEM玩具市场规模、份额和成长分析(按类型、产品类型、材料、年龄层、价格分布、型号、最终用户、分销管道和地区划分)—2026-2033年行业预测

STEM玩具市场规模、份额和成长分析(按类型、产品类型、材料、年龄层、价格分布、型号、最终用户、分销管道和地区划分)—2026-2033年行业预测 教育玩具市场规模、份额和成长分析(按产品、年龄层、分销管道、类别和地区划分)-2026-2033年产业预测

教育玩具市场规模、份额和成长分析(按产品、年龄层、分销管道、类别和地区划分)-2026-2033年产业预测 STEM玩具市场机会、成长驱动因素、产业趋势分析及2025-2034年预测游戏化学习互动解决方案市场预测至2032年:全球游戏类型、交付形式、存取模式、部署模式、应用程式、最终用户和区域分析

STEM玩具市场机会、成长驱动因素、产业趋势分析及2025-2034年预测游戏化学习互动解决方案市场预测至2032年:全球游戏类型、交付形式、存取模式、部署模式、应用程式、最终用户和区域分析