|

市场调查报告书

商品编码

1716572

家用锅炉市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Residential Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

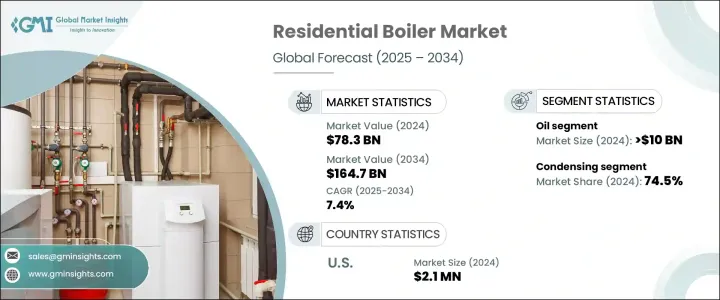

2024 年全球家用锅炉市场规模达 783 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 7.4%。对节能供暖解决方案的需求不断增长,加上严格的环境法规,正在推动市场扩张。世界各国政府正在实施更严格的碳排放标准,使得家用锅炉技术比以往任何时候都更重要。随着消费者转向先进的高性能加热系统,在监管压力和生活方式偏好变化的共同推动下,现代锅炉的采用率正在上升。

市场正在经历变革性转变,房主优先考虑永续性、成本节约和长期能源效率。随着可支配收入的增加和对生态生活的重视,消费者正在积极寻求既可靠又能减少环境影响的供暖解决方案。此外,智慧家庭技术的进步在市场动态中发挥关键作用。家用锅炉与基于物联网的温度控制和远端监控系统的整合进一步提升了消费者的兴趣。锅炉技术的创新,例如增强的热交换效率和低氮氧化物排放设计,正在为永续性和性能设定新的基准。人们对智慧互联供暖解决方案的日益青睐正在重塑行业趋势,并将现代家用锅炉定位为节能家庭的必需品。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 783亿美元 |

| 预测值 | 1647亿美元 |

| 复合年增长率 | 7.4% |

天然气家用锅炉的需求正在上升,预计到 2034 年将以 7% 的复合年增长率成长。充足的天然气供应,加上政府鼓励更清洁的暖气解决方案的政策,正在加速市场渗透。随着环境问题持续推动政策制定,消费者正在选择符合永续发展目标的低排放替代品。减少碳足迹的推动和向绿色能源的转变进一步支持了天然气驱动的家用锅炉的采用。

市场分为冷凝技术和非冷凝技术,其中冷凝锅炉占据主导地位。 2024年冷凝式家用锅炉占74.5%的市占率。这些高效能係统因其能够最大限度地降低能耗并提供卓越的加热性能而越来越受欢迎。它们对环境的影响较小,且节省成本,因此成为寻求长期供暖解决方案的房主的首选。随着环保意识的增强,预计到 2034 年冷凝锅炉的需求将持续增长,从而巩固其在市场上的主导地位。

受极端天气条件、智慧家庭自动化日益普及以及空间供暖需求不断增长的推动,预计到 2034 年北美家用锅炉市场将以 8.5% 的复合年增长率扩张。随着寒冷季节的持续和老旧的暖气基础设施升级,对现代节能供暖系统的需求日益增长。此外,智慧家庭暖气解决方案的技术进步正在增强消费者的兴趣,远端控制和可程式锅炉系统越来越受欢迎。随着消费者寻求可靠、高性能的暖气解决方案,北美家用锅炉市场将在未来十年实现显着成长。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依燃料,2021 年至 2034 年

- 主要趋势

- 天然气

- 油

- 电的

- 其他的

第六章:市场规模及预测:依技术分类,2021 年至 2034 年

- 主要趋势

- 冷凝

- 天然气

- 油

- 电的

- 其他的

- 无凝结

- 天然气

- 油

- 电的

- 其他的

第七章:市场规模及预测:依地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 丹麦

- 芬兰

- 挪威

- 瑞典

- 英国

- 俄罗斯

- 罗马尼亚

- 波兰

- 奥地利

- 比利时

- 法国

- 德国

- 荷兰

- 瑞士

- 希腊

- 义大利

- 葡萄牙

- 西班牙

- 亚太地区

- 中国

- 日本

- 韩国

- 澳洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 卡达

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

第八章:公司简介

- AO Smith

- Allied Technologies

- BDR Thermea Group

- Bradford White Corporation

- Carrier

- Ferroli

- Laars Boilers

- Lennox International

- Lochinvar

- Navien

- NTI Boilers

- PB Heat

- Smith Boilers

- Thermona

- US Boiler Company

- Viessmann

- Weil-McLain

- Wolf

The Global Residential Boiler Market reached USD 78.3 billion in 2024 and is projected to grow at a CAGR of 7.4% between 2025 and 2034. The increasing demand for energy-efficient heating solutions, coupled with stringent environmental regulations, is fueling market expansion. Governments worldwide are enforcing stricter carbon emission standards, making residential boiler technologies more crucial than ever. As consumers shift toward advanced, high-performance heating systems, the adoption of modern boilers is rising, driven by a combination of regulatory pressure and changing lifestyle preferences.

The market is witnessing a transformative shift, with homeowners prioritizing sustainability, cost savings, and long-term energy efficiency. With rising disposable incomes and an emphasis on eco-conscious living, consumers are actively seeking heating solutions that offer both reliability and reduced environmental impact. Additionally, advancements in smart home technologies are playing a pivotal role in market dynamics. The integration of residential boilers with IoT-based temperature controls and remote monitoring systems is further elevating consumer interest. Innovations in boiler technology, such as enhanced heat exchange efficiency and low-NOx emission designs, are setting new benchmarks for sustainability and performance. This growing preference for intelligent, connected heating solutions is reshaping industry trends and positioning modern residential boilers as a staple in energy-conscious households.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $78.3 Billion |

| Forecast Value | $164.7 Billion |

| CAGR | 7.4% |

The demand for natural gas residential boilers is on the rise, projected to grow at a CAGR of 7% by 2034. Abundant natural gas availability, along with government policies encouraging cleaner heating solutions, is accelerating market penetration. As environmental concerns continue to drive policymaking, consumers are opting for low-emission alternatives that align with sustainability goals. The push for reduced carbon footprints and the transition toward greener energy sources are further supporting the adoption of natural gas-powered residential boilers.

The market is categorized into condensing and non-condensing technologies, with condensing boilers leading the segment. In 2024, condensing residential boilers accounted for 74.5% of the market share. These high-efficiency systems are gaining traction due to their ability to minimize energy consumption while delivering superior heating performance. Their lower environmental impact and cost-saving benefits make them a preferred choice among homeowners looking for long-term heating solutions. As eco-consciousness rises, the demand for condensing boilers is expected to witness sustained growth through 2034, reinforcing their dominance in the market.

North America Residential Boiler Market is expected to expand at a CAGR of 8.5% by 2034, driven by extreme weather conditions, the rising adoption of smart home automation, and increasing space heating requirements. The need for modern, energy-efficient heating systems is growing as colder seasons persist and older heating infrastructures undergo upgrades. Additionally, technological advancements in smart home heating solutions are amplifying consumer interest, with remote-controlled and programmable boiler systems gaining popularity. As consumers seek reliable, high-performance heating solutions, the North American residential boiler market is poised for significant growth over the next decade.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel, 2021 – 2034 (‘000 Units & USD Million)

- 5.1 Key trends

- 5.2 Natural gas

- 5.3 Oil

- 5.4 Electric

- 5.5 Others

Chapter 6 Market Size and Forecast, By Technology, 2021 – 2034 (‘000 Units & USD Million)

- 6.1 Key trends

- 6.2 Condensing

- 6.2.1 Natural gas

- 6.2.2 Oil

- 6.2.3 Electric

- 6.2.4 Others

- 6.3 Non-condensing

- 6.3.1 Natural gas

- 6.3.2 Oil

- 6.3.3 Electric

- 6.3.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (‘000 Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Denmark

- 7.3.2 Finland

- 7.3.3 Norway

- 7.3.4 Sweden

- 7.3.5 UK

- 7.3.6 Russia

- 7.3.7 Romania

- 7.3.8 Poland

- 7.3.9 Austria

- 7.3.10 Belgium

- 7.3.11 France

- 7.3.12 Germany

- 7.3.13 Netherlands

- 7.3.14 Switzerland

- 7.3.15 Greece

- 7.3.16 Italy

- 7.3.17 Portugal

- 7.3.18 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Mexico

Chapter 8 Company Profiles

- 8.1 A.O. Smith

- 8.2 Allied Technologies

- 8.3 BDR Thermea Group

- 8.4 Bradford White Corporation

- 8.5 Carrier

- 8.6 Ferroli

- 8.7 Laars Boilers

- 8.8 Lennox International

- 8.9 Lochinvar

- 8.10 Navien

- 8.11 NTI Boilers

- 8.12 PB Heat

- 8.13 Smith Boilers

- 8.14 Thermona

- 8.15 U.S. Boiler Company

- 8.16 Viessmann

- 8.17 Weil-McLain

- 8.18 Wolf