|

市场调查报告书

商品编码

1721615

唇部和脸部油市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Lip and Face Oil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

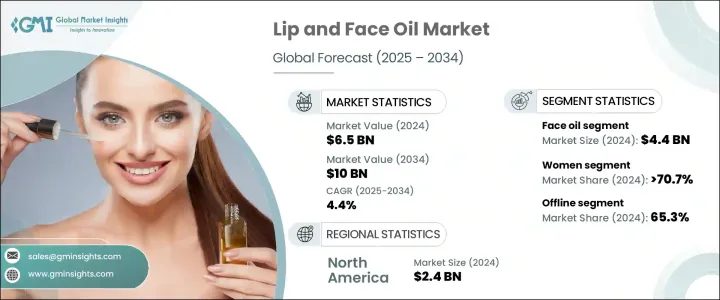

2024 年全球唇部和脸部油市场价值为 65 亿美元,预计到 2034 年将以 4.4% 的复合年增长率增长,达到 100 亿美元。受对优先考虑健康、永续性和透明度的清洁美容解决方案的需求激增的推动,该市场在全球范围内越来越受欢迎。随着消费者越来越关注皮肤上涂抹的产品,他们明显转向使用天然、植物性和符合道德标准的成分的产品。护肤程序正在演变成健康仪式,促使购物者寻找具有保湿、滋养和保护功能的多功能油。随着消费者意识到唇油和脸部油能够带来明显的、长期的皮肤益处,它们正成为美容护理中不可或缺的一部分。社群媒体影响力的增强、对皮肤敏感性的认识以及对无残忍和纯素认证产品的日益增长的倾向正在强化这种转变。除了监管支持和扩大有机认证之外,这些因素还在继续重塑美容行业格局,为品牌在全球范围内创新和扩张创造了肥沃的土壤。随着美容习惯变得更加有目的性和整体性,唇部和脸部油领域预计将吸引更大的消费者群体。

脸部精油在 2024 年创造了 44 亿美元的市场价值,预计到 2034 年将以 4.5% 的复合年增长率成长。脸部精油越来越受欢迎,是因为它们能够灵活地解决常见的皮肤护理问题,例如干燥、暗沉、细纹和发炎。如今,消费者更青睐脸部油而非传统保湿霜,因为它们含有植物成分、不致粉刺的质地以及更深层的保湿能力。这些油由轻质、富含活性成分的成分配製而成,可完美融入现代多步骤护肤程序。它们不仅可以改善皮肤质地和光泽,还可以修復皮肤屏障并提供抗衰老功效,因此非常适合各种皮肤类型。与主要提供水分和光泽的唇油不同,脸部油具有针对性的护肤功能,这提升了它们在不断增长的清洁美容市场中的价值。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 65亿美元 |

| 预测值 | 100亿美元 |

| 复合年增长率 | 4.4% |

随着女性对自我照顾和护肤意识的日益重视,到 2024 年,女性保养品的市占率将达到 70.7%。现代女性消费者积极寻求能够体现她们价值观的美容产品——青睐清洁、自然和透明的配方。有影响力的行销和皮肤病学代言增强了产品的可信度,鼓励追求明亮、水润肌肤的女性采用该产品。对健康美容的追求继续引起年轻消费者的共鸣,尤其是 Z 世代和千禧世代,他们要求产品功效的同时又不损害成分的完整性。

北美唇部和脸部油市场占 37.2% 的份额,2024 年产值达 24 亿美元。该地区拥有知识渊博、精通护肤的受众,他们重视成分透明度和功效。强大的品牌影响力、快速的产品创新以及成熟、清洁的美容生态系统推动持续的需求。美国和加拿大的消费者都将植物油作为日常生活的一部分,巩固了该地区在全球市场的领先地位。

市场的主要参与者包括 Kiehl's、Tata Harper Skincare、Clorox、Amorepacific、Johnson and Johnson、Clarins、The Body Shop、Beiersdorf、Herbivore Botanicals、Coty、Estee Lauder、联合利华、宝洁、资生堂和欧莱雅。这些公司正在对混合油进行创新,将美容效果与临床功效融为一体。研发工作重点在于为敏感肌肤打造轻盈、不致粉刺的配方,同时品牌也优先考虑环保包装,并利用数位故事和影响力合作来提升其市场影响力。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 定价分析

- 技术与创新格局

- 重要新闻和倡议

- 监管格局

- 製造商

- 经销商

- 零售商

- 对部队的影响

- 成长动力

- 消费者可支配所得不断增加

- 人们对眼睛健康的认识不断提高

- 消费者偏好的改变

- 产业陷阱与挑战

- 仿冒品

- 消费者偏好的改变

- 成长动力

- 成长潜力分析

- 消费者行为分析

- 人口趋势

- 影响购买决策的因素

- 产品偏好

- 首选价格范围

- 首选配销通路

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按产品类型,2021 - 2034 年(十亿美元)

- 主要趋势

- 唇油

- 有色唇油

- 透明唇油

- 丰唇油

- 脸部油

- 保湿脸部油

- 抗衰老脸部油

- 亮肤颜面精油

- 其他(平衡脸部油、镇静脸部油)

第六章:市场估计与预测:按价格区间,2021 年至 2034 年(十亿美元)

- 主要趋势

- 低的

- 中等的

- 高的

第七章:市场估计与预测:按消费者群体划分,2021 年至 2034 年(十亿美元)

- 主要趋势

- 男士

- 女性

- 孩子们

第八章:市场估计与预测:按包装,2021 - 2034 年(十亿美元)

- 主要趋势

- 滴管瓶

- 泵浦瓶

- 滚珠瓶

- 挤压管

- 贴上容器

- 其他(真空帮浦瓶等)

第九章:市场估计与预测:按配销通路,2021 - 2034 年(十亿美元)

- 主要趋势

- 在线的

- 电子商务

- 公司网站

- 离线

- 超市和大卖场

- 专卖店

- 其他零售店

第十章:市场估计与预测:按地区,2021 - 2034 年(十亿美元)

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Amorepacific

- Beiersdorf

- Clarins

- Clorox

- Coty

- Estee Lauder

- Herbivore Botanicals

- Johnson and Johnson

- Kiehl's

- L'Oreal

- Procter and Gamble

- Shiseido

- Tata Harper Skincare

- The Body Shop

- Unilever

The Global Lip and Face Oil Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 10 billion by 2034. This market is gaining traction worldwide, propelled by a surge in demand for clean beauty solutions that prioritize health, sustainability, and transparency. As consumers become increasingly mindful of what they apply to their skin, there is a marked shift toward products that offer natural, plant-based, and ethically sourced ingredients. Skincare routines are evolving into wellness rituals, prompting shoppers to seek out multifunctional oils that hydrate, nourish, and protect. Lip and face oils are becoming staples in beauty regimens as consumers recognize their ability to deliver visible, long-term skin benefits. The rise of social media influence, awareness around skin sensitivity, and growing inclination toward cruelty-free and vegan-certified products are reinforcing this shift. Alongside regulatory support and expanding organic certifications, these factors continue to reshape the beauty landscape, creating fertile ground for brands to innovate and scale globally. As beauty routines become more intentional and holistic, the lip and face oil segment is expected to capture an even larger consumer base.

Face oils generated USD 4.4 billion in 2024 and are projected to grow at a CAGR of 4.5% through 2034. Their rising popularity stems from their versatility in addressing common skincare issues such as dryness, dullness, fine lines, and inflammation. Consumers now favor face oils over traditional moisturizers due to their botanical compositions, non-comedogenic textures, and deeper hydration capabilities. These oils are formulated with lightweight, active-rich ingredients that seamlessly fit into modern multi-step skincare routines. They not only improve texture and radiance but also support skin barrier repair and offer anti-aging benefits, making them highly desirable for a broad range of skin types. Unlike lip oils, which primarily deliver moisture and shine, face oils offer targeted skincare functions, which enhances their value in a growing clean beauty market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $10 Billion |

| CAGR | 4.4% |

The women segment accounted for 70.7% share in 2024, driven by an increased emphasis on self-care and skincare awareness. Modern female consumers are proactively seeking beauty products that reflect their values-favoring clean, natural, and transparent formulations. Influencer marketing and dermatological endorsements have amplified product credibility, encouraging adoption among women seeking luminous, hydrated skin. The pursuit of wellness-driven beauty continues to resonate with younger consumers, particularly Gen Z and Millennials, who demand efficacy without compromising ingredient integrity.

The North America Lip and Face Oil Market held a 37.2% share, generating USD 2.4 billion in 2024. The region is home to an informed, skincare-savvy audience that values ingredient transparency and efficacy. Strong brand presence, rapid product innovation, and a mature, clean beauty ecosystem drive sustained demand. Consumers across the US and Canada are embracing botanical-based oils as part of their daily regimens, reinforcing the region's position as a leader in the global market.

Key players in the market include Kiehl's, Tata Harper Skincare, Clorox, Amorepacific, Johnson and Johnson, Clarins, The Body Shop, Beiersdorf, Herbivore Botanicals, Coty, Estee Lauder, Unilever, Procter and Gamble, Shiseido, and L'Oreal. These companies are innovating with hybrid oils that blend cosmetic appeal with clinical efficacy. R&D efforts are focused on creating lightweight, non-comedogenic formulas for sensitive skin, while brands are also prioritizing eco-friendly packaging and leveraging digital storytelling and influencer collaborations to elevate their market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier Landscape

- 3.3 Pricing analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Manufacturers

- 3.8 Distributors

- 3.9 Retailers

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising consumer disposable income

- 3.10.1.2 Growing awareness about eye health

- 3.10.1.3 Changing consumer preferences

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Counterfeit products

- 3.10.2.2 Changing consumer preferences

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Consumer behavior analysis

- 3.12.1 Demographic trends

- 3.12.2 Factors affecting buying decisions

- 3.12.3 Product Preference

- 3.12.4 Preferred price range

- 3.12.5 Preferred distribution channel

- 3.13 Porter’s analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 ($Bn) (Thousand Units)

- 5.1 Key trends

- 5.2 Lip oils

- 5.2.1 Tinted lip oils

- 5.2.2 Clear lip oils

- 5.2.3 Plumping lip oils

- 5.3 Face oils

- 5.3.1 Hydrating face oils

- 5.3.2 Anti-aging face oils

- 5.3.3 Brightening face oils

- 5.3.4 Others (balancing face oils, calming face oils)

Chapter 6 Market Estimates & Forecast, By Price Range, 2021 - 2034 ($Bn) (Thousand Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates & Forecast, By Consumer Group, 2021 - 2034 ($Bn) (Thousand Units)

- 7.1 Key trends

- 7.2 Men

- 7.3 Women

- 7.4 Kids

Chapter 8 Market Estimates & Forecast, By Packaging, 2021 - 2034 ($Bn) (Thousand Units)

- 8.1 Key trends

- 8.2 Dropper bottles

- 8.3 Pump bottles

- 8.4 Roll-on bottles

- 8.5 Squeeze tubes

- 8.6 Stick containers

- 8.7 Others (airless pump bottles, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-Commerce

- 9.2.2 Company website

- 9.3 Offline

- 9.3.1 Supermarkets and Hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Other retail stores

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Amorepacific

- 11.2 Beiersdorf

- 11.3 Clarins

- 11.4 Clorox

- 11.5 Coty

- 11.6 Estee Lauder

- 11.7 Herbivore Botanicals

- 11.8 Johnson and Johnson

- 11.9 Kiehl’s

- 11.10 L'Oreal

- 11.11 Procter and Gamble

- 11.12 Shiseido

- 11.13 Tata Harper Skincare

- 11.14 The Body Shop

- 11.15 Unilever

脸部保养产品市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、销售管道、地区及竞争格局划分,2021-2031年)脸部喷雾市场-全球产业规模、份额、趋势、机会和预测:按产品类型、最终用途、销售管道、地区和竞争格局划分,2021-2031年脸部擦拭巾市场-全球产业规模、份额、趋势、机会、预测:按类型、产品类型、分销管道、地区和竞争格局划分,2021-2031年

脸部保养产品市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、销售管道、地区及竞争格局划分,2021-2031年)脸部喷雾市场-全球产业规模、份额、趋势、机会和预测:按产品类型、最终用途、销售管道、地区和竞争格局划分,2021-2031年脸部擦拭巾市场-全球产业规模、份额、趋势、机会、预测:按类型、产品类型、分销管道、地区和竞争格局划分,2021-2031年 猫用湿纸巾市场按产品类型、包装类型、分销管道和最终用户划分-2026-2032年全球预测

猫用湿纸巾市场按产品类型、包装类型、分销管道和最终用户划分-2026-2032年全球预测 无麸质脸部保养用品的全球市场的评估:各产品类型,各皮肤类型,各流通管道,各地区,机会,预测(2018年~2032年)脸部保养市场:产品类型、分销管道、肤质、最终用户、价格分布和性别—2025-2032 年全球预测全球保湿乳市场按性别、肤质、产品类型、配方、分销管道和应用领域分類的预测(2025-2030 年)脸部按摩器市场按类型、功能、技术、安装类型、使用环境和分销管道划分—2025-2030 年全球预测脸部洗面乳市场按产品类型、包装类型、香型、肤质、分销管道和最终用户划分-2025-2030 年全球预测

无麸质脸部保养用品的全球市场的评估:各产品类型,各皮肤类型,各流通管道,各地区,机会,预测(2018年~2032年)脸部保养市场:产品类型、分销管道、肤质、最终用户、价格分布和性别—2025-2032 年全球预测全球保湿乳市场按性别、肤质、产品类型、配方、分销管道和应用领域分類的预测(2025-2030 年)脸部按摩器市场按类型、功能、技术、安装类型、使用环境和分销管道划分—2025-2030 年全球预测脸部洗面乳市场按产品类型、包装类型、香型、肤质、分销管道和最终用户划分-2025-2030 年全球预测 脸部油市场按产品类型、皮肤类型、配方类型、分销管道和地区划分

脸部油市场按产品类型、皮肤类型、配方类型、分销管道和地区划分