|

市场调查报告书

商品编码

1858831

个人化营养人工智慧平台市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Personalized Nutrition AI Platforms Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

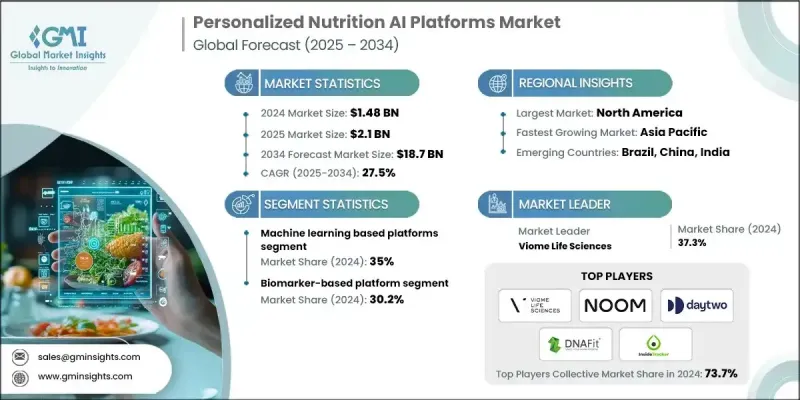

2024 年全球个人化营养 AI 平台市值为 14.8 亿美元,预计到 2034 年将以 27.5% 的复合年增长率增长至 187 亿美元。

市场成长的驱动力在于消费者对个人化健康解决方案的需求日益增长,这种解决方案超越了传统的「一刀切」模式。随着人们健康意识的增强和预防保健的日益普及,能够根据每位使用者的生物特征、生活方式和健康目标量身定制营养指导的人工智慧平台正迅速崛起。消费者现在更倾向于高度个人化的饮食计划和营养补充服务,这些服务会考虑过敏史、饮食目标和既往病史等因素。活跃人群对运动表现优化和健身饮食的日益关注也进一步推动了市场的发展。这些平台越来越多地整合了基因组学、蛋白质组学和微生物组分析等复杂的生物资料,从而提供与每个人独特生理特征相契合的营养建议。透过利用这些资料,个人化的人工智慧平台能够提供高度精准的建议,使其成为一般用户和健康专业人士信赖的工具。这些工具的便利性、精准性和即时适应性正在帮助消费者重塑他们的营养策略。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 14.8亿美元 |

| 预测值 | 187亿美元 |

| 复合年增长率 | 27.5% |

到2024年,基于机器学习的平台将占据35%的市场。这些平台依赖结构化资料集,例如穿戴式装置输出、医疗检测结果和饮食日记。随着资料集的扩展和标註的准确性不断提高,机器学习演算法也在不断发展,提供越来越精准、更具实用性的营养建议。增强型学习模型正在推动数位营养生态系统的创新,使用户能够获得随着时间推移而不断改进并适应行为、环境或健康状况变化的见解。

2024年,基于生物标誌物的细分市场占据了30.2%的市场份额,预计到2034年将以27.5%的复合年增长率成长。这些平台专注于将血液检测和临床标记资料转化为个人化建议,旨在改善心血管和代谢健康等领域。它们能够透过可测量的健康资料追踪使用者对介入措施的反应,赢得了医疗专业人员和终端用户的信任,进一步巩固了其在医疗保健和健康领域的地位。

预计到2024年,美国个人化营养人工智慧平台市场规模将达5.138亿美元,领先北美地区。这一成长主要得益于美国完善的医疗保健生态系统、不断增长的数位健康投资以及市场对人工智慧营养平台的广泛接受。监管机构对医疗器材软体(SaMD)和临床决策支援(CDS)系统等数位健康工具的支持,以及基于感测器的可穿戴设备和持续血糖监测设备的普及,正在拓展即时个人化指导的潜力。

全球个人化营养人工智慧平台市场的主要参与者包括 Viome Life Sciences、Baze、Noom Inc.、ZOE Limited、Nutrigenomix Inc.、Rootine、DNAfit (Prenetics)、InsideTracker、DayTwo Ltd. 和 Season Health。为了巩固市场地位,各公司正专注于开发由人工智慧和机器学习驱动的数据丰富的个人化引擎。他们与基因组学和诊断实验室建立合作关係,以增强多组学整合并开发专有的推荐演算法。这些平台还优先考虑透过行动优先介面和穿戴式装置实现无缝的用户体验。各公司在监管合规和临床验证方面投入巨资,以赢得消费者和医疗保健提供者的信任。此外,许多品牌正瞄准运动员、糖尿病患者和老年人群等细分消费群体,以客製化满足其特定需求的产品和服务。订阅式服务模式的采用旨在确保客户留存率和持续的收入来源。有些公司甚至整合了远距医疗和营养指导功能,从而建立端到端的个人化健康生态系统。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 慢性病盛行率不断上升

- 对个人化健康和保健解决方案的需求日益增长

- 人工智慧和机器学习的进步

- 产业陷阱与挑战

- 监理复杂性和合规成本

- 资料隐私和安全问题

- 市场机会

- 消费者对客製化健康解决方案的需求日益增长

- 与可穿戴设备和健康设备集成

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依技术类型

- 未来市场趋势

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依技术类型划分,2021-2034年

- 主要趋势

- 基于机器学习的平台

- 多组学人工智慧系统

- 预测分析平台

- 大型语言模式系统

第六章:市场估算与预测:依资料输入类型划分,2021-2034年

- 主要趋势

- 基于生物标誌物的平台

- 微生物组分析系统

- 穿戴式装置集成

- 自我报告资料平台

第七章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第八章:公司简介

- Baze

- DayTwo Ltd.

- DNAfit (Prenetics)

- InsideTracker

- Noom Inc.

- Nutrigenomix Inc.

- Rootine

- Season Health

- Viome Life Sciences

The Global Personalized Nutrition AI Platforms Market was valued at USD 1.48 billion in 2024 and is estimated to grow at a CAGR of 27.5% to reach USD 18.7 billion by 2034.

Market growth is fueled by increasing consumer demand for personalized health and wellness solutions that move beyond the conventional one-size-fits-all model. As people grow more health-conscious and seek preventive care, AI-powered platforms offering nutrition guidance tailored to each user's biological profile, lifestyle, and health goals are seeing a rapid rise in popularity. Consumers now prefer hyper-personalized meal planning and supplement services that factor in allergies, dietary goals, and medical history. The growing interest in performance optimization and fitness-focused diets among active individuals further contributes to market momentum. These platforms are increasingly integrated with complex biological data like genomics, proteomics, and microbiome analysis to deliver nutrition advice that's aligned with each individual's unique physiological traits. By harnessing this data, personalized AI-driven platforms offer a high degree of accuracy in recommendations, making them a trusted tool for both everyday users and health professionals. The convenience, precision, and real-time adaptability of these tools are helping reshape the way consumers approach their nutrition strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.48 Billion |

| Forecast Value | $18.7 Billion |

| CAGR | 27.5% |

The machine learning-based platforms segment held a 35% share in 2024. These platforms thrive on structured datasets such as wearable device outputs, medical test results, and food diaries. As datasets expand and become more accurately labeled, machine learning algorithms continue to evolve, offering increasingly precise, actionable nutrition advice. Enhanced learning models are driving innovation across digital nutrition ecosystems, enabling users to receive insights that improve over time and adapt to changes in behavior, environment, or health.

The biomarker-based segment accounted for a 30.2% share in 2024 and is forecast to grow at a CAGR of 27.5% through 2034. These platforms specialize in converting blood work and clinical marker data into individualized recommendations aimed at improving areas such as cardiovascular and metabolic health. Their ability to track how a user responds to interventions through measurable health data has earned trust from both medical professionals and end users, further solidifying their role in the healthcare and wellness landscape.

United States Personalized Nutrition AI Platforms Market generated USD 513.8 million in 2024, leading the North American region. Growth here is driven by a well-established healthcare ecosystem, increasing digital health investments, and strong market acceptance of AI-based nutrition platforms. Regulatory support for digital health tools like software as a medical device (SaMD) and clinical decision support (CDS) systems, along with the widespread use of sensor-based wearables and continuous glucose monitoring devices, is expanding the potential of personalized coaching in real time.

Key players dominating the Global Personalized Nutrition AI Platforms Market include Viome Life Sciences, Baze, Noom Inc., ZOE Limited, Nutrigenomix Inc., Rootine, DNAfit (Prenetics), InsideTracker, DayTwo Ltd., and Season Health. To solidify their position, companies are focusing on data-rich personalization engines powered by AI and machine learning. Firms are forming partnerships with genomic and diagnostic labs to enhance multi-omic integration and develop proprietary recommendation algorithms. These platforms also prioritize seamless user experience through mobile-first interfaces and connected wearables. Companies are investing heavily in regulatory compliance and clinical validations to gain credibility with both consumers and healthcare providers. Additionally, many brands are targeting niche consumer segments such as athletes, diabetics, and aging populations to tailor offerings for specific needs. Subscription-based service models are being adopted to ensure customer retention and sustained revenue streams. Some are even integrating telehealth and nutrition coaching features, creating end-to-end personalized health ecosystems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology type

- 2.2.3 Data input type

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Rising demand for personalized health and wellness solutions

- 3.2.1.3 Advancements in AI and machine learning

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory complexity & compliance costs

- 3.2.2.2 Data privacy & security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Growing consumer demand for tailored health solutions

- 3.2.3.2 Integration with wearables and health devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By technology type

- 3.8 Future market trends

- 3.9 Patent Landscape

- 3.10 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.10.1 Major importing countries

- 3.10.2 Major exporting countries

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Machine learning-based platforms

- 5.3 Multi-omics AI systems

- 5.4 Predictive analytics platforms

- 5.5 Large language model-based systems

Chapter 6 Market Estimates and Forecast, By Data Input Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Biomarker-based platforms

- 6.3 Microbiome analysis systems

- 6.4 Wearable device integration

- 6.5 Self-reported data platforms

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Baze

- 8.2 DayTwo Ltd.

- 8.3 DNAfit (Prenetics)

- 8.4 InsideTracker

- 8.5 Noom Inc.

- 8.6 Nutrigenomix Inc.

- 8.7 Rootine

- 8.8 Season Health

- 8.9 Viome Life Sciences

按品种和生命阶段分類的宠物专用营养品市场预测(至2034年):全球产品类型、生命阶段、品种体型、宠物类型、最终用户和地区分析智慧营养补充品市场预测(至2034年):全球分析(按产品类型、成分类型、剂型、个人化程度、消费群组、技术整合、应用、最终用户、分销管道和地区划分)

按品种和生命阶段分類的宠物专用营养品市场预测(至2034年):全球产品类型、生命阶段、品种体型、宠物类型、最终用户和地区分析智慧营养补充品市场预测(至2034年):全球分析(按产品类型、成分类型、剂型、个人化程度、消费群组、技术整合、应用、最终用户、分销管道和地区划分) 个人化营养市场规模、占有率及预测(依产品类型、模式、技术和应用划分)-全球预测全球个人化营养与健康市场:预测(至2034年)-按产品、通路、技术、应用、最终用户和地区进行分析

个人化营养市场规模、占有率及预测(依产品类型、模式、技术和应用划分)-全球预测全球个人化营养与健康市场:预测(至2034年)-按产品、通路、技术、应用、最终用户和地区进行分析 个人化营养市场-2026年至2031年预测个人化营养食品饮料市场预测至2032年:全球产品类型、个人化方法、形式、分销管道、应用、最终用户和区域分析人工智慧赋能营养配方市场预测至2032年:按技术、应用、最终用户和地区分類的全球分析

个人化营养市场-2026年至2031年预测个人化营养食品饮料市场预测至2032年:全球产品类型、个人化方法、形式、分销管道、应用、最终用户和区域分析人工智慧赋能营养配方市场预测至2032年:按技术、应用、最终用户和地区分類的全球分析 个人化营养市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)针对特定年龄层的个人化营养市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)基于DNA的客製化维生素配方市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

个人化营养市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)针对特定年龄层的个人化营养市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)基于DNA的客製化维生素配方市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)