|

市场调查报告书

商品编码

1885902

进阶通讯解决方案市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Rich Communication Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球进阶通讯解决方案市场价值为 26.4 亿美元,预计到 2034 年将以 21.3% 的复合年增长率成长至 194.5 亿美元。

全球智慧型手机普及率的激增是RCS的关键驱动力,使这些先进的讯息系统能够触及更广泛的使用者群体。随着消费者从功能简单的手机过渡到拥有更强大连接性和更先进作业系统的智慧型手机,RCS的普及速度也正在加快。 RCS对多媒体内容、互动功能和类似应用程式的讯息体验的支援能力,推动了这一成长。日益丰富的连网设备促使电信业者部署RCS,进而扩大业务覆盖范围,并在成熟市场和新兴市场加速商业化进程。 5G网路的部署提供了更可靠、更有效率的RCS讯息传递所需的速度、频宽和低延迟环境。随着连接性的提升,高解析度媒体共享、即时通知、互动式聊天机器人和品牌讯息等功能运作更加流畅。随着营运商升级到5G,企业将有机会增强客户互动,进而提高RCS的普及率,并推动全球营收成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 26.4亿美元 |

| 预测值 | 194.5亿美元 |

| 复合年增长率 | 21.3% |

2024年,A2P细分市场占据了61%的市场份额,预计到2034年将以19%的复合年增长率成长。 A2P RCS广泛应用于各行各业,用于互动行销活动、安全警报和个人化客户互动。其作为合法通讯管道的认可进一步促进了其普及,而CPaaS提供者则简化了企业的整合流程。 A2P能够将视觉效果和互动性结合,使其成为进阶通讯解决方案市场中最具商业潜力的细分市场。

2024年,基于云端的RCS解决方案市场估值达到17.9亿美元。这些平台提供可扩展、低延迟的讯息传递基础设施,支援A2P行销活动,并具备弹性容量以因应需求波动,同时提供自动更新功能。 CPaaS供应商已透过易于存取的API将RCS转化为一项服务,简化了企业采用流程,并使其更易于在各行业部署。

预计到2024年,美国进阶通讯解决方案)市场规模将达8.916亿美元。智慧型手机的普及、5G的逐步推广以及零售、银行和电信等行业的广泛应用,都将推动市场成长。人工智慧聊天机器人、A2P即时通讯和品牌验证讯息的日益普及,增强了基于RCS的客户互动,加速了其在大型企业中的应用。

全球进阶通讯解决方案市场的主要参与者包括AT&T、中国移动、德国电信、Google、华为技术有限公司、KDDI、NTT DOCOMO、T-Mobile US、Verizon Communications和沃达丰。这些公司专注于拓展云端产品、整合人工智慧和互动功能以及与电信营运商建立策略合作伙伴关係等策略。他们强调A2P进阶通讯解决方案方案以提高企业采用率,投资可扩展的API以简化集成,并利用5G网路增强服务可靠性。许多公司还优先考虑扩大全球覆盖范围、透过丰富的讯息功能改善客户体验以及提升品牌知名度,以巩固市场地位并开拓新的收入来源。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 智慧型手机普及率

- 5G网路扩充

- 企业采用A2P讯息传递

- 从简讯转向富媒体讯息

- 产业陷阱与挑战

- 互通性挑战

- 用户隐私问题

- 市场机会

- 电子商务与零售互动

- 银行及金融服务

- 旅游及酒店服务

- 区域市场拓展(中东及非洲及亚太地区)

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 全球的

- FCC分类为资讯服务

- 国际电信联盟安全要求(ITU-T X.1817)

- GDPR及资料隐私影响

- 医疗保健应用程式的 HIPAA 合规性

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 全球的

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 技术准备度和成熟度评估

- 定价分析

- 业者定价策略(按讯息收费 vs. 按订阅收费)

- CPaaS定价模式(按需付费与企业方案)

- RCS 与 SMS 成本比较

- 按地区分類的A2P简讯费率表

- 新兴的获利模式

- 成本細項分析

- 专利分析

- GSMA专利格局

- 主要专利持有人和授权模式

- 标准必要专利(SEP)

- 诉讼与纠纷趋势

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 用例

- 进阶对话式人工智慧应用

- 扩增实境(AR)讯息传递

- 物联网和机器对机器 (M2M) 讯息传递

- 元宇宙与沉浸式体验

- 最佳情况

- 投资与融资分析

- RCS基础设施营运商资本支出

- CPaaS平台融资轮次

- 併购活动(Tata-Kaleyra,Google-Jibe)

- 创投对即时通讯新创公司的投入

- 策略伙伴关係与合资企业

- 消费者与企业情绪分析

- 消费者意识与理解

- 企业采纳情绪

- 讯息流量和网路影响分析

- 全球RCS消息量趋势

- 网路频宽和容量要求

- 基础设施负载与效能

- 服务品质 (QoS) 指标

- 网路货币化与流量管理

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

- 产品和服务基准测试

- 研发投资分析

- 供应商选择标准

第五章:市场估算与预测:依通讯类型划分,2021-2034年

- 主要趋势

- A2P

- P2A

- P2P

第六章:市场估算与预测:依部署模式划分,2021-2034年

- 主要趋势

- 云

- 现场

第七章:市场估算与预测:依组织规模划分,2021-2034年

- 主要趋势

- 大型企业

- 中小企业

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 丰富的通话和讯息功能

- 云端储存

- 行销和广告活动

- 内容散布

- 其他的

第九章:市场估计与预测:依产业垂直领域划分,2021-2034年

- 主要趋势

- 丰富的通话和讯息功能

- 云端储存

- 行销和广告活动

- 内容散布

- 其他的

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 俄罗斯

- 波兰

- 罗马尼亚

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 越南

- 印尼

- 巴基斯坦

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 伊朗

第十一章:公司简介

- Global companies

- AT&T

- China Mobile

- Deutsche Telekom

- Huawei Technologies

- Infobip

- KDDI

- Orange

- Sinch

- Tata Communications

- Telefonica

- Verizon Communications

- Vodafone Group

- 区域玩家

- Clickatell

- CM.com

- Gupshup

- Syniverse

- Tanla Platforms

- 新兴玩家

- Telnyx

- Webex Connect

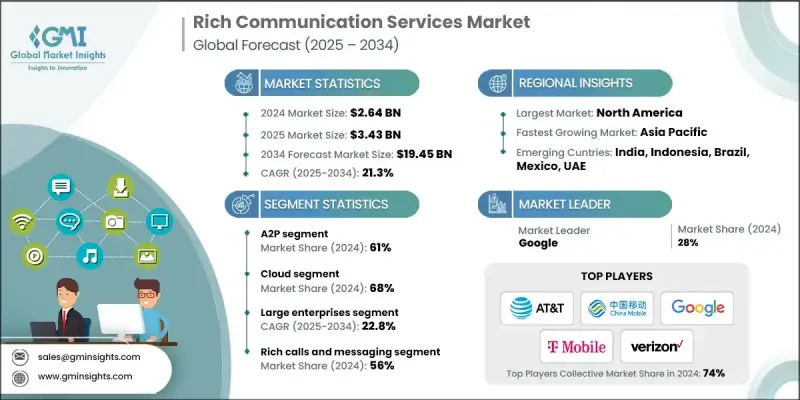

The Global Rich Communication Services Market was valued at USD 2.64 billion in 2024 and is estimated to grow at a CAGR of 21.3% to reach USD 19.45 billion by 2034.

The surge in smartphone adoption worldwide is a key driver for RCS, enabling these advanced messaging systems to reach a broader audience. As consumers transition from basic phones to smartphones with enhanced connectivity and operating systems, the pace of RCS adoption accelerates. This growth is fueled by RCS's ability to support multimedia content, interactive features, and app-like messaging experiences. The increasing variety of connected devices motivates telecom operators to implement RCS, expanding business outreach and accelerating commercialization in both mature and emerging markets. The deployment of 5G networks offers the speed, bandwidth, and low-latency environment necessary for more reliable and efficient RCS messaging. With improved connectivity, features such as high-resolution media sharing, real-time notifications, interactive chatbots, and branded messaging perform more seamlessly. As carriers upgrade to 5G, enterprises gain opportunities to enhance customer interactions, boosting adoption rates and driving revenue growth globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.64 Billion |

| Forecast Value | $19.45 Billion |

| CAGR | 21.3% |

The A2P segment held a 61% share in 2024 and is expected to grow at a CAGR of 19% through 2034. A2P RCS is widely used across sectors for interactive campaigns, secure alerts, and personalized customer engagement. Its recognition as a legitimate communication channel further strengthens its adoption, while CPaaS providers have simplified integration for enterprises. The ability to combine visuals and interactivity makes A2P the most commercially advanced segment of the Rich Communication Services Market.

The cloud-based RCS solutions segment was valued at USD 1.79 billion in 2024. These platforms provide scalable, low-latency messaging infrastructure, support for A2P campaigns, and elastic capacity to manage fluctuating demand while offering automatic updates. CPaaS providers have turned RCS into a service via accessible APIs, streamlining enterprise adoption and making it easier to deploy across industries.

United States Rich Communication Services Market reached USD 891.6 million in 2024. Strong smartphone penetration, the gradual rollout of 5G, and adoption across retail, banking, and telecom sectors support market growth. The increasing use of AI-enabled chatbots, A2P messaging, and brand-verified messaging enhances RCS-based customer engagement, accelerating its acceptance among major enterprises.

Key players in the Global Rich Communication Services Market include AT&T, China Mobile, Deutsche Telekom, Google, Huawei Technologies, KDDI, NTT DOCOMO, T-Mobile US, Verizon Communications, and Vodafone. Companies in the Rich Communication Services Market focus on strategies such as expanding cloud-based offerings, integrating AI and interactive features, and forming strategic partnerships with telecom operators. They emphasize A2P solutions to increase enterprise adoption, invest in scalable APIs for easier integration, and leverage 5G networks to enhance service reliability. Many firms also prioritize expanding global reach, improving customer experience through rich messaging features, and enhancing brand visibility to strengthen their market position and capture new revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Communication type

- 2.2.3 Deployment model

- 2.2.4 Organization size

- 2.2.5 Application

- 2.2.6 Industry vertical

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Smartphone penetration

- 3.2.1.2 5G network expansion

- 3.2.1.3 Enterprise adoption of A2P messaging

- 3.2.1.4 Shift from SMS to rich messaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Interoperability challenges

- 3.2.2.2 User privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 E-commerce & retail engagement

- 3.2.3.2 Banking & financial services

- 3.2.3.3 Travel & hospitality services

- 3.2.3.4 Regional market expansion (MEA & APAC)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global

- 3.4.1.1 FCC Classification as Information Services

- 3.4.1.2 ITU Security Requirements (ITU-T X.1817)

- 3.4.1.3 GDPR & Data Privacy Implications

- 3.4.1.4 HIPAA Compliance for Healthcare Applications

- 3.4.2 North America

- 3.4.3 Europe

- 3.4.4 Asia Pacific

- 3.4.5 Latin America

- 3.4.6 Middle East & Africa

- 3.4.1 Global

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology readiness & maturity assessment

- 3.8 Pricing analysis

- 3.8.1 Operator pricing strategies (per-message vs subscription)

- 3.8.2 CPaaS pricing models (pay-as-you-go vs enterprise plans)

- 3.8.3 RCS vs SMS cost comparison

- 3.8.4 A2P messaging rate cards by region

- 3.8.5 Emerging monetization models

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.10.1 GSMA patent landscape

- 3.10.2 Key patent holders & licensing models

- 3.10.3 Standards-Essential Patents (SEPs)

- 3.10.4 Litigation & Dispute Trends

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use cases

- 3.12.1 Advanced conversational AI applications

- 3.12.2 Augmented Reality (AR) messaging

- 3.12.3. IoT & M2 M messaging

- 3.12.4 Metaverse & immersive experiences

- 3.13 Best case scenario

- 3.14 Investment & funding analysis

- 3.14.1 Operator CAPEX in RCS Infrastructure

- 3.14.2 CPaaS Platform Funding Rounds

- 3.14.3 M&A Activity (Tata-Kaleyra, Google-Jibe)

- 3.14.4 Venture capital investment in messaging startups

- 3.14.5 Strategic partnerships & joint ventures

- 3.15 Consumer & enterprise sentiment analysis

- 3.15.1 Consumer awareness & understanding

- 3.15.2 Enterprise adoption sentiment

- 3.16 Message traffic & network impact analysis

- 3.16.1 Global RCS message volume trends

- 3.16.2 Network bandwidth & capacity requirements

- 3.16.3 Infrastructure load & performance

- 3.16.4 Quality of service (QoS) metrics

- 3.16.5 Network monetization & traffic management

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Product and service benchmarking

- 4.8 R&D investment analysis

- 4.9 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Communication Type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 A2P

- 5.3 P2A

- 5.4 P2P

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Rich calls and messaging

- 8.3 Cloud storage

- 8.4 Marketing and advertising campaign

- 8.5 Content delivery

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Industry Vertical, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Rich calls and messaging

- 9.3 Cloud storage

- 9.4 Marketing and advertising campaign

- 9.5 Content delivery

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Pakistan

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Iran

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 AT&T

- 11.1.2 China Mobile

- 11.1.3 Deutsche Telekom

- 11.1.4 Google

- 11.1.5 Huawei Technologies

- 11.1.6 Infobip

- 11.1.7 KDDI

- 11.1.8 Orange

- 11.1.9 Sinch

- 11.1.10 Tata Communications

- 11.1.11 Telefonica

- 11.1.12 Verizon Communications

- 11.1.13 Vodafone Group

- 11.2 Regional players

- 11.2.1 Clickatell

- 11.2.2 CM.com

- 11.2.3 Gupshup

- 11.2.4 Syniverse

- 11.2.5 Tanla Platforms

- 11.3 Emerging players

- 11.3.1 Telnyx

- 11.3.2 Webex Connect

进阶通讯服务市场:依通讯类型、元件、部署模式、企业规模、应用程式和产业划分-2026年至2032年全球市场预测

进阶通讯服务市场:依通讯类型、元件、部署模式、企业规模、应用程式和产业划分-2026年至2032年全球市场预测 2026年全球进阶通讯服务(RCS)市场报告2026年全球进阶通讯服务市场报告

2026年全球进阶通讯服务(RCS)市场报告2026年全球进阶通讯服务市场报告 富通信服务市场报告:按通讯类型、部署模式、组织规模、应用、产业和地区划分(2026-2034 年)

富通信服务市场报告:按通讯类型、部署模式、组织规模、应用、产业和地区划分(2026-2034 年) 进阶通讯解决方案市场-全球产业规模、份额、趋势、机会和预测,依部署模式、企业规模、应用、地区和竞争格局划分,2021-2031年预测

进阶通讯解决方案市场-全球产业规模、份额、趋势、机会和预测,依部署模式、企业规模、应用、地区和竞争格局划分,2021-2031年预测 进阶通讯服务市场规模、份额和成长分析(按类型、公司规模、应用、最终用户和地区划分)-2026-2033年产业预测

进阶通讯服务市场规模、份额和成长分析(按类型、公司规模、应用、最终用户和地区划分)-2026-2033年产业预测 进阶通讯服务(RCS)的全球市场的评估:各用途,各终端用户,不同企业规模,各最终用途产业,各地区,机会,预测(2018年~2032年)

进阶通讯服务(RCS)的全球市场的评估:各用途,各终端用户,不同企业规模,各最终用途产业,各地区,机会,预测(2018年~2032年) 进阶通讯服务:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)

进阶通讯服务:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年) 全球进阶通讯服务市场:市场规模、份额、趋势分析 - 按公司规模、类型、最终用途、区域展望、预测,2024-2031 年

全球进阶通讯服务市场:市场规模、份额、趋势分析 - 按公司规模、类型、最终用途、区域展望、预测,2024-2031 年 进阶通讯服务市场规模、份额、趋势分析报告:按类型、公司规模、最终用途、地区、细分市场预测,2024-2030 年

进阶通讯服务市场规模、份额、趋势分析报告:按类型、公司规模、最终用途、地区、细分市场预测,2024-2030 年