|

市场调查报告书

商品编码

1892715

地下水管理市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Groundwater Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

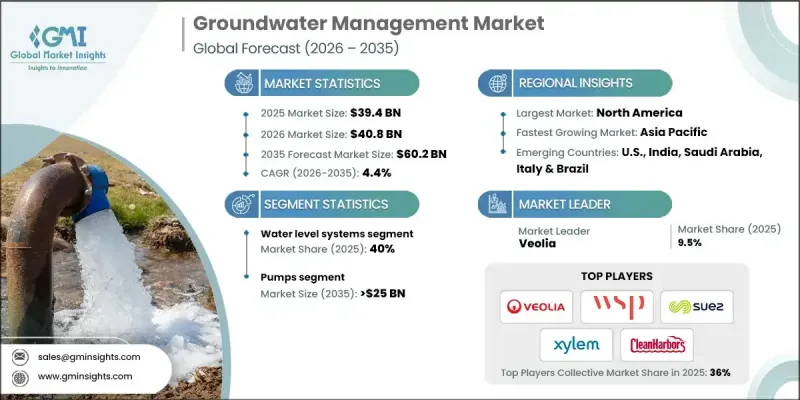

2025 年全球地下水管理市场价值为 394 亿美元,预计到 2035 年将以 4.4% 的复合年增长率增长至 602 亿美元。

市场成长的驱动力来自模组化和简化设计的持续创新以及先进的自动化技术。智慧感测器和遥测系统的部署使操作人员能够即时监测地下水位、水质和补给率。预测分析提供可操作的洞察,以防止过度开采和污染,从而推动了对地下水管理解决方案的需求。地下水管理涵盖旨在确保地下水资源永续利用和保护的专门技术和系统。其功能包括监测含水层水位、调节开采速率、防止污染和支持补给过程。该行业已从基本的水资源开采发展成为在优化资源效率、控制污染风险和支持永续发展目标方面发挥战略作用的领域。采用补给策略和处理后水的再利用进一步提高了营运效率和成本效益。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 394亿美元 |

| 预测值 | 602亿美元 |

| 复合年增长率 | 4.4% |

预计到2025年,水位监测系统市占率将达到40%。日益严格的监管要求和对可持续用水的重视正在推动先进水位监测系统的应用。对便携式、经济高效且易于安装的感测器的需求不断增长,正在促进其普及,尤其是在农村地区。这些设备现在可以精确测量pH值、浊度、溶解氧和污染物,从而确保符合严格的水质标准。

2025年,泵类设备市占率占45%,预计到2035年将成长至250亿美元。变频驱动和自动流量调节技术的整合提高了泵送效率并减少了浪费。市场对符合碳减排倡议的太阳能和混合动力泵系统的需求正在成长。製造商正致力于模组化设计和耐腐蚀材料,以确保在各种水文地质条件下都能可靠运作。

到2035年,北美地下水管理市场规模将达到180亿美元。市政和工业营运商正越来越多地部署先进感测器和自动化抽水系统,以符合严格的环境法规。公共机构和私人企业之间的密切合作,以及持续的基础设施投资,正在加速市场成长。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 原物料供应及采购分析

- 製造能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 监管环境

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

- 地下水管理成本结构分析

- 新兴机会与趋势

- 数位化与物联网集成

- 投资分析及未来展望

第四章:竞争格局

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 战略仪錶板

- 策略倡议

- 重要伙伴关係与合作

- 主要併购活动

- 产品创新与发布

- 市场扩张策略

- 竞争性标竿分析

- 创新与永续发展格局

第五章:市场规模及预测:按监测数据,2022-2035年

- 水质感测器

- 水位系统

- 物联网日誌记录器

- 地理空间分析

第六章:市场规模及预测:以开采方式划分,2022-2035年

- 水泵浦

- 钻井作业

- 井套管和筛管

- 整合式渗透系统

第七章:市场规模及预测:基于 Recharge 的数据,2022-2035 年

- 人工补给结构

- MAR系统

- 回灌井

- 雨水渗透

第八章:市场规模及预测:依治疗方法划分,2022-2035年

- 过滤系统

- 泵送和治疗

- 海水淡化和化学处理

- 生物修復和原位修復

第九章:市场规模及预测:依最终用途划分,2022-2035年

- 农业

- 市政

- 工业的

第十章:市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印尼

- 印度

- 澳洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 伊朗

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第十一章:公司简介

- Arcadis

- Black & Veatch

- Clean Harbors Environmental Services

- DMT Group

- Envirogen Technologies

- GEI Consultants

- Grundfos

- HEPACO

- HPC AG

- iFLUX

- INDUS Environmental Services

- Koop Wasserbau

- Minetek

- Remedial Construction Services

- Sensoil Innovations

- Stantec

- SUEZ

- Sweco AB

- Tetra Tech

- The Groundwater Company

- Veolia

- WJ Group

- WSP Global

- Xylem Water Solutions

The Global Groundwater Management Market was valued at USD 39.4 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 60.2 billion by 2035.

Market growth is driven by continuous innovations in modular and simplified designs combined with advanced automation technologies. The deployment of smart sensors and telemetry systems allows operators to monitor groundwater levels, water quality, and recharge rates in real time. Predictive analytics provide actionable insights to prevent over-extraction and contamination, which fuels demand for groundwater management solutions. Groundwater management encompasses specialized techniques and systems designed to ensure sustainable utilization and protection of subsurface water resources. Its functions include monitoring aquifer levels, regulating extraction rates, preventing contamination, and supporting recharge processes. The sector has evolved beyond basic water extraction to a strategic role in optimizing resource efficiency, controlling contamination risks, and supporting sustainability goals. Incorporating recharge strategies and treated water reuse further enhances operational efficiency and cost-effectiveness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.4 Billion |

| Forecast Value | $60.2 Billion |

| CAGR | 4.4% |

The water level systems segment held a 40% share in 2025. Increasing regulatory mandates and emphasis on sustainable water use are driving the adoption of advanced water level monitoring systems. Rising demand for portable, cost-effective, and easy-to-install sensors is boosting penetration, particularly in rural areas. These devices now provide accurate measurements of pH, turbidity, dissolved oxygen, and contaminants, ensuring compliance with strict water quality standards.

The pumps segment held a 45% share in 2025 and is expected to grow to USD 25 billion by 2035. The integration of variable frequency drives and automated flow regulation improves pumping efficiency and reduces wastage. Demand is rising for solar and hybrid pump systems that align with carbon reduction initiatives. Manufacturers are focusing on modular designs and corrosion-resistant materials to ensure reliability across diverse hydrogeological conditions.

North America Groundwater Management Market will reach USD 18 billion by 2035. Municipal and industrial operators are increasingly deploying advanced sensors and automated pumping systems to comply with strict environmental regulations. Strong collaboration between public agencies and private enterprises, coupled with ongoing infrastructure investments, is accelerating market growth.

Key players in the Groundwater Management Market include Arcadis, Black & Veatch, Clean Harbors Environmental Services, DMT Group, Envirogen Technologies, GEI Consultants, Grundfos, HEPACO, HPC AG, iFLUX, INDUS Environmental Services, Koop Wasserbau, Minetek, Remedial Construction Services, Sensoil Innovations, Stantec, SUEZ, Sweco AB, Tetra Tech, The Groundwater Company, Veolia, WJ Group, WSP Global, and Xylem Water Solutions.

Companies in the Groundwater Management Market are employing several strategies to enhance their market presence. They are investing in R&D to develop smart, automated, and modular systems with improved monitoring and predictive capabilities. Strategic partnerships with municipalities, industrial operators, and environmental agencies expand market reach and accelerate adoption. Businesses are also focusing on geographic expansion into regions facing water scarcity. Integration of renewable-powered pumps and corrosion-resistant materials ensures adaptability in diverse hydrogeological conditions. Additionally, companies are offering value-added services such as data analytics, maintenance support, and training programs to strengthen client relationships, enhance operational efficiency, and drive long-term growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Monitoring trends

- 2.4 Extraction trends

- 2.5 Recharge trends

- 2.6 Treatment trends

- 2.7 End use trends

- 2.8 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of groundwater management

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Monitoring, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Water quality sensors

- 5.3 Water level systems

- 5.4 IoT loggers

- 5.5 Geospatial analysis

Chapter 6 Market Size and Forecast, By Extraction, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Pumps

- 6.3 Borewell drilling

- 6.4 Well casing & screens

- 6.5 Integrated infiltration systems

Chapter 7 Market Size and Forecast, By Recharge, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Artificial recharge structures

- 7.3 MAR systems

- 7.4 Recharge wells

- 7.5 Stormwater infiltration

Chapter 8 Market Size and Forecast, By Treatment, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Filtration systems

- 8.3 Pump & treat

- 8.4 Desalination & chemical treatment

- 8.5 Biological & in-situ remediation

Chapter 9 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Agriculture

- 9.3 Municipal

- 9.4 Industrial

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 Indonesia

- 10.4.4 India

- 10.4.5 Australia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 South Africa

- 10.5.5 Egypt

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Chile

Chapter 11 Company Profiles

- 11.1 Arcadis

- 11.2 Black & Veatch

- 11.3 Clean Harbors Environmental Services

- 11.4 DMT Group

- 11.5 Envirogen Technologies

- 11.6 GEI Consultants

- 11.7 Grundfos

- 11.8 HEPACO

- 11.9 HPC AG

- 11.10 iFLUX

- 11.11 INDUS Environmental Services

- 11.12 Koop Wasserbau

- 11.13 Minetek

- 11.14 Remedial Construction Services

- 11.15 Sensoil Innovations

- 11.16 Stantec

- 11.17 SUEZ

- 11.18 Sweco AB

- 11.19 Tetra Tech

- 11.20 The Groundwater Company

- 11.21 Veolia

- 11.22 WJ Group

- 11.23 WSP Global

- 11.24 Xylem Water Solutions

2026年全球地下水管理市场报告

2026年全球地下水管理市场报告 挖掘废弃物管理市场:按废弃物类型、技术、挖掘方法、应用和最终用户划分-2026-2032年全球市场预测

挖掘废弃物管理市场:按废弃物类型、技术、挖掘方法、应用和最终用户划分-2026-2032年全球市场预测 全球挖掘废弃物管理市场规模、份额、趋势和成长分析报告:2026-2034年

全球挖掘废弃物管理市场规模、份额、趋势和成长分析报告:2026-2034年 挖掘废弃物管理服务市场-全球产业规模、份额、趋势、机会、预测:按服务、地点、废弃物类型、地区和竞争格局划分,2021-2031年

挖掘废弃物管理服务市场-全球产业规模、份额、趋势、机会、预测:按服务、地点、废弃物类型、地区和竞争格局划分,2021-2031年 挖掘废弃物管理市场规模、份额和成长分析(按类型、废弃物排放、服务、应用和地区划分)—产业预测(2026-2033 年)

挖掘废弃物管理市场规模、份额和成长分析(按类型、废弃物排放、服务、应用和地区划分)—产业预测(2026-2033 年) 固控钻井废弃物管理市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

固控钻井废弃物管理市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 钻井软体市场(按解决方案和地区划分)

钻井软体市场(按解决方案和地区划分) 全球钻井废弃物控制与处理市场海上钻井废弃物管理市场-全球产业规模、份额、趋势、机会和预测,按服务类型、废弃物类型、应用、最终用户产业、地区、竞争细分,2020-2030 年预测海上钻井废弃物管理市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

全球钻井废弃物控制与处理市场海上钻井废弃物管理市场-全球产业规模、份额、趋势、机会和预测,按服务类型、废弃物类型、应用、最终用户产业、地区、竞争细分,2020-2030 年预测海上钻井废弃物管理市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测