|

市场调查报告书

商品编码

1892885

农机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Farm Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

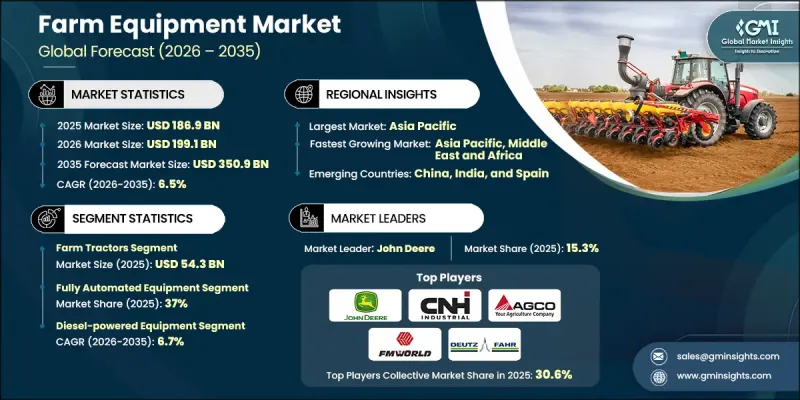

2025年全球农业设备市场价值为1,869亿美元,预计到2035年将以6.5%的复合年增长率成长至3,509亿美元。

这一稳步增长势头反映了现代农业的快速发展,而现代农业的变革正受到机械化、不断增长的粮食需求和技术突破的推动。市场涵盖了种类繁多的工具和机械,旨在提高农业生产力,减少对劳动力的依赖,并简化作物种植、畜牧管理和园艺等各个环节的作业流程。设备种类繁多,从传统的拖拉机和联合收割机到由感测器、人工智慧和导航技术驱动的新一代自动化系统,应有尽有。精准农业解决方案,包括配备GPS的机械、先进的感测器和无人机,正在透过提高投入利用率和支援数据驱动决策,重塑田间管理模式。这些技术支援变数施肥、即时监测和优化资源配置,帮助农民在提高产量的同时,降低15-20%的投入成本。发展中地区对永续农业的日益重视和机械化程度的不断提高,持续推动农业产业的扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 1869亿美元 |

| 预测值 | 3509亿美元 |

| 复合年增长率 | 6.5% |

2024年,农用曳引机市场规模达543亿美元,预计2025年至2034年间将以5.3%的复合年增长率成长。小型和多用途拖拉机的需求仍然强劲,尤其是在中小农场。旨在促进农业现代化的财政激励和补贴政策进一步提高了此类拖拉机的普及率。

预计到2035年,柴油动力设备市场将以6.7%的复合年增长率成长。柴油机械因其耐用性、在高负荷下仍能保持稳定运行以及广泛的可用性而继续受到青睐。然而,不断上涨的燃油价格和日益严格的排放法规正促使製造商提高效率并开发更清洁的替代方案。

美国农机市场占80%的市场份额,预计2025年市场规模将达206亿美元。美国市场受益于技术的快速发展、精准农业的广泛应用以及对能够胜任各种农场作业的高性能机械日益增长的需求。人们对减少收穫后损失和提高作业效率的意识不断增强,推动了收割机械市场的成长;同时,对永续水资源管理的日益重视也促进了对先进灌溉系统的需求。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依设备类型

- 监管环境

- 标准和合规要求

- 区域监理框架

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依设备类型划分,2022-2035年

- 农用拖拉机

- 四轮驱动(4WD)拖拉机

- 行栽拖拉机

- 多用途拖拉机

- 小型多用途拖拉机

- 收割机械

- 联合收割机

- 割草机/割晒机

- 饲料收割机

- 干草收割机械

- 割草机

- 翻晒干草的人

- 种植和施肥

- 耕作

- 其他(灌溉设备等)

第六章:市场估算与预测:依营运模式划分,2022-2035年

- 手动设备

- 半自动化设备

- 全自动设备

第七章:市场估算与预测:依电源类型划分,2022-2035年

- 柴油动力设备

- 电动和混合动力设备

- 替代燃料

第八章:市场估算与预测:依应用领域划分,2022-2035年

- 作物生产应用

- 耕作与土壤健康管理

- 种植和播种作业

- 作物保护

- 收割和脱粒

- 精准农业

- GPS引导的自动驾驶

- 可变利率技术

- 产量监测与测绘

- 分区控制系统

- 保护与永续性

- 保护性耕作方式

- 精准灌溉

- 有针对性的农药施用

- 畜牧业

- 乳牛养殖

- 牛/猪饲养场

第九章:市场估算与预测:依最终用途划分,2022-2035年

- 商业营运

- 中小农户

第十章:市场估价与预测:依配销通路划分,2022-2035年

- 直销

- 间接销售

第十一章:市场估计与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- AGCO Corporation

- Bomet

- CLAAS

- CNH Industrial

- Deutz-Fahr

- FMWORLD Agricultural Machinery

- JCB

- John Deere

- Kubota Corporation

- KUHN

- Mahindra & Mahindra

- SDF Group

- Vermeer Corporation

- Yanmar

The Global Farm Equipment Market was valued at USD 186.9 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 350.9 billion by 2035.

This steady momentum reflects the rapid evolution of modern agriculture, which is being shaped by mechanization, rising food demand, and technological breakthroughs. The market spans a broad spectrum of tools and machinery engineered to increase farm productivity, reduce reliance on labor, and streamline operations across crop cultivation, livestock management, and horticulture. Equipment ranges from traditional tractors and combine harvesters to next-generation automated systems powered by sensors, artificial intelligence, and guided navigation. Precision farming solutions, including GPS-enabled machinery, advanced sensors, and drones, are reshaping field management by improving input utilization and enabling data-driven decisions. These technologies support variable-rate applications, real-time monitoring, and optimized resource allocation, helping farmers improve yields while reducing input costs by 15-20%. Growing emphasis on sustainable farming and increased mechanization across developing regions continues to reinforce industry expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $186.9 Billion |

| Forecast Value | $350.9 Billion |

| CAGR | 6.5% |

The farm tractors segment generated USD 54.3 billion in 2024 and is projected to grow at a CAGR of 5.3% during 2025-2034. Demand for compact and utility tractors remains strong, particularly among small and medium-sized farms. Financial incentives and subsidies designed to promote agricultural modernization are further elevating adoption rates in this category.

The diesel-powered equipment segment is anticipated to grow at a CAGR of 6.7% through 2035. Diesel machinery continues to be preferred for its durability, resilience under heavy workloads, and widespread availability. However, rising fuel prices and stricter emissions regulations are prompting manufacturers to enhance efficiency and develop cleaner alternatives.

United States Farm Equipment Market held an 80% share and generated USD 20.6 billion in 2025. The U.S. market benefits from rapid advancements in technology, strong uptake of precision agriculture, and increasing demand for high-performance machinery capable of handling diverse farm operations. Enhanced awareness regarding reducing post-harvest losses and improving operational speed is supporting growth in harvesting machinery, while heightened attention on sustainable water management is boosting demand for advanced irrigation systems.

Key players in the Global Farm Equipment Market include John Deere, SDF Group, CLAAS, AGCO Corporation, Yanmar, KUHN, CNH Industrial, Mahindra & Mahindra, Deutz-Fahr, JCB, Vermeer Corporation, Kubota Corporation, Bomet, and FMWORLD Agricultural Machinery. Companies competing in the Farm Equipment Market are adopting multiple strategies to strengthen their market position. Leading manufacturers are heavily investing in precision farming solutions, automation, and smart machinery to improve productivity and sustainability. Expanding product lines across various horsepower segments and machinery categories allows brands to serve diverse farm sizes and operational needs. Collaborations with technology partners, digital platform development, and integration of telematics enhance equipment monitoring and performance analytics for customers. Companies are also focusing on regional expansion through distribution networks, localized manufacturing, and after-sales service programs.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Mode of operation

- 2.2.4 Power source

- 2.2.5 Application

- 2.2.6 End use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Farm tractors

- 5.2.1 4-wheel drive (4wd) tractors

- 5.2.2 Row crop tractors

- 5.2.3 Utility tractors

- 5.2.4 Compact utility tractors

- 5.3 Harvesting machinery

- 5.3.1 Combine harvester

- 5.3.2 Mower/swather

- 5.3.3 Forage harvester

- 5.4 Haying machinery

- 5.4.1 Hay mowers

- 5.4.2 Hay tedders

- 5.5 Planting & fertilizing

- 5.6 Plowing & cultivation

- 5.7 Others (Irrigation equipment etc.)

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Manual equipment

- 6.3 Semi-automated equipment

- 6.4 Fully automated equipment

Chapter 7 Market Estimates & Forecast, By Power Source, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Diesel-powered equipment

- 7.3 Electric & hybrid equipment

- 7.4 Alternative fuels

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Crop production applications

- 8.2.1 Tillage & soil health management

- 8.2.2 Planting & seeding operations

- 8.2.3 Crop protection

- 8.2.4 Harvesting & threshing

- 8.3 Precision agriculture

- 8.3.1 GPS-guided auto-steering

- 8.3.2 Variable rate technology

- 8.3.3 Yield monitoring & mapping

- 8.3.4 Section control systems

- 8.4 Conservation & sustainability

- 8.4.1 Conservation tillage practices

- 8.4.2 Precision irrigation

- 8.4.3 Targeted pesticide application

- 8.5 Livestock operations

- 8.5.1 Dairy farming

- 8.5.2 Cattle/hog feeding operations

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Commercial operations

- 9.3 Small & medium farmers

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AGCO Corporation

- 12.2 Bomet

- 12.3 CLAAS

- 12.4 CNH Industrial

- 12.5 Deutz-Fahr

- 12.6 FMWORLD Agricultural Machinery

- 12.7 JCB

- 12.8 John Deere

- 12.9 Kubota Corporation

- 12.10 KUHN

- 12.11 Mahindra & Mahindra

- 12.12 SDF Group

- 12.13 Vermeer Corporation

- 12.14 Yanmar

谷物螺旋输送机市场:按类型、动力来源、容量、应用、最终用户和分销管道划分-2026-2032年全球预测红外线沥青加热器市场:按产品类型、电源、移动性、应用、最终用户、分销管道划分,全球预测(2026-2032年)堆高机升降臂市场:按类型、容量、应用和最终用户划分,全球预测,2026-2032年挖土机底盘零件市场:按产品类型、应用、分销管道和最终用途划分,全球预测,2026-2032年重型设备底盘零件市场:按零件类型、设备类型、销售管道、最终用途产业和材料划分,全球预测,2026-2032年

谷物螺旋输送机市场:按类型、动力来源、容量、应用、最终用户和分销管道划分-2026-2032年全球预测红外线沥青加热器市场:按产品类型、电源、移动性、应用、最终用户、分销管道划分,全球预测(2026-2032年)堆高机升降臂市场:按类型、容量、应用和最终用户划分,全球预测,2026-2032年挖土机底盘零件市场:按产品类型、应用、分销管道和最终用途划分,全球预测,2026-2032年重型设备底盘零件市场:按零件类型、设备类型、销售管道、最终用途产业和材料划分,全球预测,2026-2032年 农业机械市场规模、份额和成长分析(按动力、传动系统、功能、推进、设备类型和地区划分)-2026-2033年产业预测

农业机械市场规模、份额和成长分析(按动力、传动系统、功能、推进、设备类型和地区划分)-2026-2033年产业预测 2026-2030年全球农业机械市场

2026-2030年全球农业机械市场 美国农业机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南农业机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国农业机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南农业机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球农业干燥机市场规模、份额、趋势和成长分析报告(2026-2034年)

全球农业干燥机市场规模、份额、趋势和成长分析报告(2026-2034年)