|

市场调查报告书

商品编码

1851417

託管服务:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

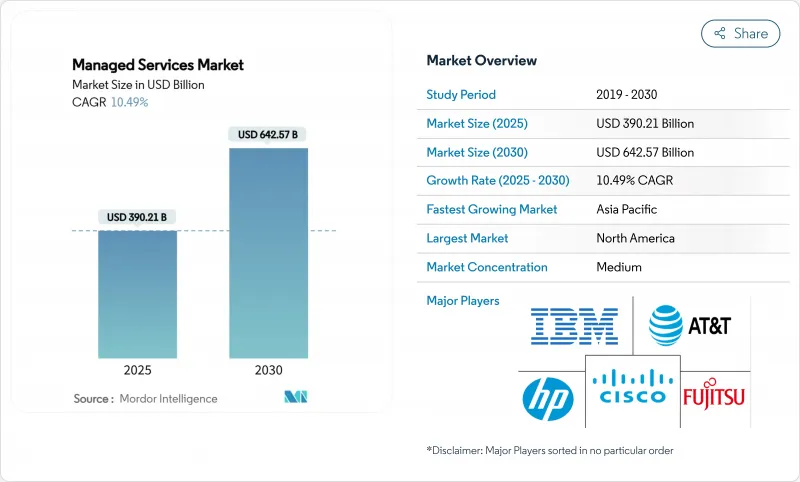

预计到 2025 年,託管服务市场规模将达到 3,902.1 亿美元,到 2030 年将扩大到 6,425.7 亿美元,复合年增长率为 10.49%。

强劲的成长反映了企业在应对混合云端复杂性、日益严峻的网路威胁和持续的预算审查时,纷纷转向外包IT营运。以云端为中心的交付模式、人工智慧的日益普及以及监管压力正在重塑服务提供者的产品和服务,而智慧自动化和垂直行业专业知识则是实现差异化竞争的关键。策略外包已从单纯的成本节约转变为数位转型的核心支柱,服务供应商正在加速投资安全营运中心、多重云端编配工具和边缘管理平台。併购活动凸显了规模经济的吸引力,服务提供者正寻求透过非内生成长来弥补技术差距并扩大地域覆盖范围。

全球託管服务市场趋势与洞察

混合云端的复杂性推动了託管服务的采用

混合云端架构融合了本地部署、私有云端和多个公共云端,增加了维运的复杂性,让内部团队难以应付。诸如微软欧盟资料边界之类的管理方案要求在地化资料处理,迫使企业选择能够保证合规性、可携性和统一安全策略的供应商。

成本优化压力推动外包决策

持续的利润压力正将固定IT成本转化为变动成本项目,例如託管服务。埃森哲与美国签订的价值16亿美元的「云一号」(Cloud One)合约等大规模转型交易表明,企业正将外包视为战略性而非战术性的倡议。服务提供者将Accenture、人工智慧工具和认证人才库打包出售,使买家能够在避免前期投资投入的同时获得新的能力。

资料主权法规限制了服务交付模式。

要求本地化处理的法规迫使服务提供者在每个司法管辖区复製基础设施,从而降低了规模经济效益,并使全球交付更加复杂。微软的欧盟资料边界意味着服务提供者必须承担额外的资本和营运成本,才能为多个地区的客户提供服务。

细分市场分析

到2024年,云端运算将占据託管服务市场52.7%的份额,随着混合云端在2030年前以12.1%的复合年增长率成长,其领先优势将进一步扩大。按需启动资源、遵守资料法规以及整合边缘工作负载的能力,正推动企业从本地部署模式迁移到云端运算。Accenture的「云端一体化」(Cloud One)计画等超大规模云端服务联盟,展现了协作创新如何促成多年期大型合约。

託管服务市场将受益于云端运算的普及,因为它允许服务供应商集中基础设施、自动修补漏洞并大规模部署人工智慧主导的成本优化。私有云端在资料敏感领域仍将保持可行性,但对于难以重构的传统工作负载,本地部署服务仍将持续存在。多重云端编配和财务营运彙报的服务提供者将最有优势赢得新的支出。

到2024年,託管基础设施服务收入将成长38.9%,这反映了维持异质设施运作的根本需求。然而,託管安全服务将引领成长,复合年增长率将达到11.9%,这反映了董事会对勒索软体和合规罚款的担忧。人工智慧驱动的威胁搜寻、零信任部署和自动化事件遏制是区分市场赢家的关键。

随着网路保险公司收紧承保标准,託管保全服务服务市场规模预计将加速成长。服务提供者正将安全营运中心即服务 (SOCaaS) 与合规报告和桌面演练捆绑销售,从而创造高利润的经常性收入。网路和通讯服务将受益于 5G 的推广,而资料中心能源管理产品也将受益于永续性要求。

託管服务市场按配置(本地部署、云端部署)、服务类型(託管资料中心、託管安全、託管通讯等)、公司规模(中小企业、大型企业)、最终用户行业(银行、金融服务和保险 (BFSI)、IT 和通讯、製造业等)以及地区进行细分。市场预测以美元计价。

区域分析

北美地区预计在2024年将维持32.7%的收入份额,这主要得益于早期云端迁移、网路安全法规以及高额的IT支出。联邦政府项目,例如美国的「云端一号」(Cloud One)计划,正在提升大型託管服务合约的透明度。银行、金融服务和保险(BFSI)以及医疗保健行业的客户持续支撑着市场需求,而服务提供者正将该地区作为人工智慧和边缘运算试点计画的启动平台。

亚太地区是成长最快的地区,预计到2030年复合年增长率将达到11.5%。中国製造业的升级、印度数位化公共基础设施的建设以及日本老旧工厂的现代化改造,都在推动对能够连接传统工作负载和云端工作负载的服务提供者的投资。超大规模资料中心营运商正与本地主机服务供应商 (MSP) 合作,以满足各国自主的云端需求,而东协各国政府也在强制推行云端优先政策并缩短销售週期。

随着GDPR、数位营运弹性法规和永续性规则的实施,合规难度日益增加,欧洲正稳步扩张。德国大力推动工业4.0,英国利用託管服务供应商(MSP)应对脱欧后的金融监管,法国则着重发展其主权云端框架。服务提供者正透过区域性资料中心和绿色能源采购来实现差异化竞争,以达成环保目标。中东和非洲仍在发展中,但智慧城市和电子政府计划正经历快速成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 向混合云营运模式转型

- 企业IT预算面临成本优化压力

- 网路威胁数量不断增加,合规要求日益严格

- 远端边缘运算部署管理服务

- 网路保险对全天候託管式侦测和回应的先决条件

- 永续性和绿色IT法规推动了电力/冷却管理

- 市场限制

- 根深蒂固的资料主权和隐私法规

- 多厂商整合和传统系统互通性挑战

- 长期MSP合约带来的供应商锁定风险和高昂的退出成本

- MSP(託管服务提供者)内部人才短缺限制了服务品质的扩充性。

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 评估市场的宏观经济因素

第五章 市场规模与成长预测

- 透过部署

- 本地部署

- 云

- 公有云

- 私有云端

- 混合云

- 按服务类型

- 託管资料中心

- 託管安全

- 管理沟通

- 主机网路

- 託管基础设施

- 行动管理

- 其他的

- 按公司规模

- 中小企业

- 大公司

- 按最终用户行业划分

- BFSI

- 资讯科技/通讯

- 医疗保健和生命科学

- 製造业

- 零售与电子商务

- 政府/公共部门

- 能源与公共产业

- 媒体与娱乐

- 其他(教育、非营利组织)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- Cisco Systems Inc.

- Fujitsu Ltd

- ATandT Inc.

- Hewlett Packard Enterprise(HPE)

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Nokia Corporation

- Deutsche Telekom AG(T-Systems)

- Rackspace Technology Inc.

- Tata Consultancy Services Ltd

- Wipro Ltd

- Accenture plc

- Capgemini SE

- HCL Technologies Ltd

- Cognizant Technology Solutions

- NTT Data Corp.

- DXC Technology Co.

- Lumen Technologies Inc.

- Orange Business Services

第七章 市场机会与未来展望

The managed services market stands at USD 390.21 billion in 2025 and is forecast to expand to USD 642.57 billion by 2030 at a 10.49% CAGR.

The strong growth reflects enterprises' pivot toward outsourced IT operations as they juggle hybrid-cloud complexity, rising cyber threats, and ongoing budget scrutiny. Cloud-centric delivery models, wider AI adoption, and regulatory pressures are reshaping provider offerings, while competitive differentiation now hinges on intelligent automation and vertical expertise. Strategic outsourcing has shifted from pure cost reduction to a core pillar of digital transformation, accelerating provider investments in security operations centers, multi-cloud orchestration tools, and edge management platforms. M&A activity underscores the appeal of scale, with providers pursuing inorganic growth to fill technology gaps and expand geographic reach.

Global Managed Services Market Trends and Insights

Hybrid-cloud complexity drives managed services adoption

Hybrid-cloud architectures combine on-premises, private, and multiple public clouds, elevating operational complexity that internal teams struggle to master. Regulatory initiatives such as the Microsoft EU Data Boundary require localized data handling, pushing enterprises toward providers that can guarantee compliance, portability, and unified security policies.Seamless workload portability and real-time policy enforcement across distributed environments cement long-term demand for managed infrastructure and security offerings.

Cost optimization pressures accelerate outsourcing decisions

Persistent margin pressure turns fixed IT overhead into a variable line item through managed services. Large transformation deals such as Accenture's USD 1.6 billion Cloud One contract with the U.S. Air Force illustrate how enterprises view outsourcing as strategic, not merely tactical. Providers bundle automation, AI tooling, and certified talent pools, allowing buyers to avoid up-front capital outlays while still accessing emerging capabilities.

Data-sovereignty regulations constrain service delivery models

Mandates requiring localized processing force providers to duplicate infrastructure in each jurisdiction, reducing economies of scale and complicating global delivery. Microsoft's EU Data Boundary illustrates the additional capital and operational overhead that providers must absorb to serve multi-region clients.

Other drivers and restraints analyzed in the detailed report include:

- Cybersecurity threat evolution demands specialized response capabilities

- Edge computing expansion creates remote management requirements

- Vendor lock-in concerns limit long-term commitments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment held 52.7% share of the managed services market in 2024 and is widening its lead as hybrid cloud posts a 12.1% CAGR through 2030. The ability to spin up resources on demand, comply with data regulations, and integrate edge workloads explains why enterprises migrate from on-premises models. Hyperscaler alliances, like Accenture's engagement on Cloud One, show how co-innovation can unlock large multiyear deals.

The managed services market benefits as cloud deployment allows providers to pool infrastructure, automate patches, and roll out AI-driven cost-optimization at scale. Private cloud remains relevant for data-sensitive sectors, while on-premises services persist for legacy workloads that cannot be refactored easily. Providers that master multi-cloud orchestration and FinOps reporting are best positioned to capture new spend.

Managed infrastructure services owned 38.9% revenue in 2024, reflecting the baseline need to keep heterogeneous estates running. Yet managed security services lead growth with an 11.9% CAGR, mirroring board-level concern over ransomware and compliance fines. AI-enabled threat hunting, zero-trust rollouts, and automated incident containment set market winners apart.

The managed services market size for security offerings is expected to accelerate as cyber-insurance carriers tighten underwriting criteria. Providers are bundling SOC-as-a-service with compliance reporting and tabletop exercises, creating high-margin recurring revenue. Network and communication services gain from 5G roll-outs, while data-center energy management products ride sustainability mandates.

Managed Services Market is Segmented by Deployment (On-Premises, Cloud), Service Type (Managed Data Center, Managed Security, Managed Communications, and More), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Vertical (BFSI, IT and Telecommunication, Manufacturing, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 32.7% revenue share in 2024, buoyed by early cloud migration, cyber regulations, and high IT spend. Federal programs such as the U.S. Air Force Cloud One create visibility for large managed services contracts. BFSI and healthcare customers continue to anchor demand, and providers use the region as a launchpad for AI and edge pilots.

Asia-Pacific is the fastest-growing region at 11.5% CAGR to 2030. China's manufacturing upgrades, India's digital-public-infrastructure push, and Japan's aging plant modernization funnel spend toward providers capable of bridging legacy and cloud workloads. Hyperscalers team with local MSPs to address sovereign-cloud requirements, while ASEAN governments adopt cloud-first mandates that shorten sales cycles.

Europe shows steady expansion as GDPR, Digital Operational Resilience Act, and sustainability rules heighten compliance complexity. Germany drives Industry 4.0 managed services, the United Kingdom leans on MSPs for post-Brexit financial regulation, and France emphasizes sovereign-cloud frameworks. Providers differentiate through localized data centers and green-energy sourcing to meet environmental targets. The Middle East and Africa remain nascent but grow quickly on smart-city and e-government projects.

- IBM Corporation

- Cisco Systems Inc.

- Fujitsu Ltd

- ATandT Inc.

- Hewlett Packard Enterprise (HPE)

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Nokia Corporation

- Deutsche Telekom AG (T-Systems)

- Rackspace Technology Inc.

- Tata Consultancy Services Ltd

- Wipro Ltd

- Accenture plc

- Capgemini SE

- HCL Technologies Ltd

- Cognizant Technology Solutions

- NTT Data Corp.

- DXC Technology Co.

- Lumen Technologies Inc.

- Orange Business Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to hybrid-cloud operating models

- 4.2.2 Cost-optimization pressure on enterprise IT budgets

- 4.2.3 Rising cyber-threat volume and compliance mandates

- 4.2.4 Edge-computing roll-outs demanding remote managed services

- 4.2.5 Cyber-insurance prerequisites for 24/7 managed detection and response

- 4.2.6 Sustainability and green-IT regulations driving managed power/cooling

- 4.3 Market Restraints

- 4.3.1 Persistent data-sovereignty and privacy regulations

- 4.3.2 Multi-vendor integration and legacy interoperability challenges

- 4.3.3 Vendor lock-in risk and high exit costs of long-term MSP contracts

- 4.3.4 Talent shortages within MSPs limiting service-quality scalability

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.1.2.1 Public Cloud

- 5.1.2.2 Private Cloud

- 5.1.2.3 Hybrid Cloud

- 5.2 By Service Type

- 5.2.1 Managed Data Center

- 5.2.2 Managed Security

- 5.2.3 Managed Communications

- 5.2.4 Managed Network

- 5.2.5 Managed Infrastructure

- 5.2.6 Managed Mobility

- 5.2.7 Others

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 IT and Telecommunication

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Media and Entertainment

- 5.4.9 Others (Education, Non-Profit)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Fujitsu Ltd

- 6.4.4 ATandT Inc.

- 6.4.5 Hewlett Packard Enterprise (HPE)

- 6.4.6 Microsoft Corporation

- 6.4.7 Verizon Communications Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Nokia Corporation

- 6.4.10 Deutsche Telekom AG (T-Systems)

- 6.4.11 Rackspace Technology Inc.

- 6.4.12 Tata Consultancy Services Ltd

- 6.4.13 Wipro Ltd

- 6.4.14 Accenture plc

- 6.4.15 Capgemini SE

- 6.4.16 HCL Technologies Ltd

- 6.4.17 Cognizant Technology Solutions

- 6.4.18 NTT Data Corp.

- 6.4.19 DXC Technology Co.

- 6.4.20 Lumen Technologies Inc.

- 6.4.21 Orange Business Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

按服务类型、部署类型、组织规模、组件和行业垂直领域分類的託管IT基础设施服务市场 - 全球预测 2025-2032 年电信託管服务市场:按部署模式、组织规模和垂直行业分類的电信託管服务 - 2025-2032 年全球预测

按服务类型、部署类型、组织规模、组件和行业垂直领域分類的託管IT基础设施服务市场 - 全球预测 2025-2032 年电信託管服务市场:按部署模式、组织规模和垂直行业分類的电信託管服务 - 2025-2032 年全球预测 管理服务的全球市场(~2035年):各服务形式,各部署类型,各类型企业,各产业类型,各地区,产业趋势,预测

管理服务的全球市场(~2035年):各服务形式,各部署类型,各类型企业,各产业类型,各地区,产业趋势,预测 2025年全球託管IT基础设施服务市场报告2025年全球託管基础设施服务市场报告2025年全球託管资讯服务市场报告2025年全球託管服务市场报告

2025年全球託管IT基础设施服务市场报告2025年全球託管基础设施服务市场报告2025年全球託管资讯服务市场报告2025年全球託管服务市场报告 全球託管通讯服务市场:2032 年预测 - 按服务类型、部署方式、组织规模、最终用户和地区进行分析2025年电信託管服务全球市场报告託管服务市场:2025-2030 年全球预测(按服务类型、合约类型、组织规模、最终用户和部署类型)

全球託管通讯服务市场:2032 年预测 - 按服务类型、部署方式、组织规模、最终用户和地区进行分析2025年电信託管服务全球市场报告託管服务市场:2025-2030 年全球预测(按服务类型、合约类型、组织规模、最终用户和部署类型)